Hot Dip Galvanizing Market - Global Industry Analysis and Forecast 2026 to 2034

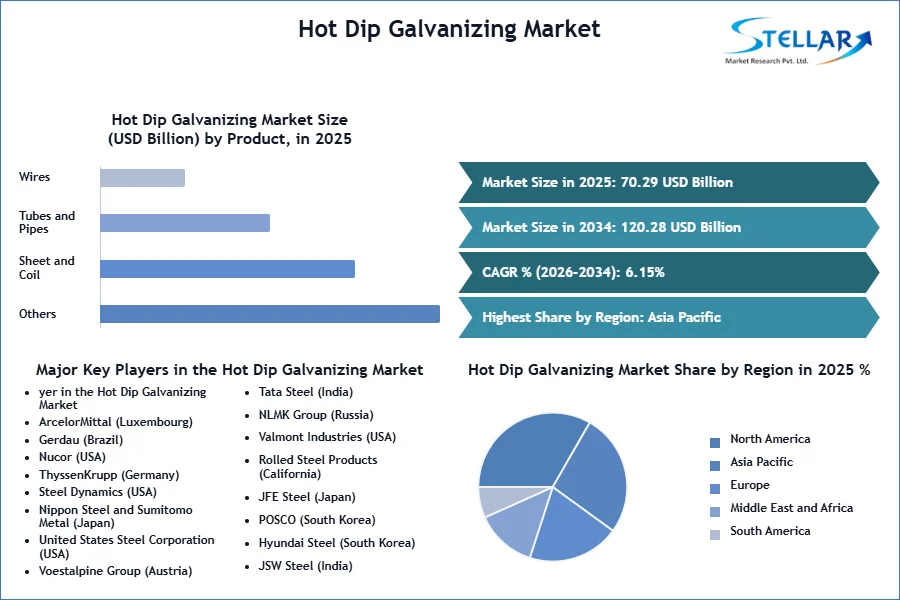

The Hot Dip Galvanizing Market size was valued at USD 70.29 Bn. in 2025 and the total Global Hot Dip Galvanizing revenue is expected to grow at a CAGR of 6.15 % from 2026 to 2034 , reaching nearly USD 120.28 Bn. by 2034.

Hot Dip Galvanizing Market Overview

Hot-dip galvanizing (HDG) is a highly effective process for protecting steel by immersing it in molten zinc to create a strong barrier against corrosion. This makes it suitable for various industrial applications.

- According to SMR analysis, implementing corrosion prevention best practices results in a global savings of 15-35% of the cost of damage, or between $375-875 billion USD.

The Stellar Market Research report focuses on the Hot Dip Galvanizing Market, aiming to predict its growth trends and provide insights into its supply chain dynamics. The hot dip galvanizing market has experienced significant growth in recent years, driven by the increasing demand for corrosion-resistant steel products across various industries. This market covers a wide range of applications, with the construction and infrastructure sectors being the primary drivers.

The need for durable and long-lasting structures has led to the increased use of hot dip galvanized steel in bridges, buildings, and other civil engineering projects. The automotive industry has also played a significant role in the market's growth, as galvanized steel components are increasingly used in vehicle manufacturing to improve safety and extend product lifespan. The hot dip galvanizing market is highly competitive, with numerous players operating across the value chain, including steel manufacturers, galvanizing service providers, and suppliers of equipment and raw materials. Strategic partnerships, mergers, and acquisitions have become common as companies strive to gain a competitive edge and expand their market share.

The report utilizes quantitative research methods to provide statistical data on the effectiveness of Hot Dip Galvanizing in various applications and their impact on market trends. Additionally, the report presents PORTER and PESTEL analyses, considering the potential impact of macroeconomic factors on the market. Both external and internal factors that positively or negatively affect the business are analyzed, offering decision-makers a clear futuristic view of the industry.

A comprehensive competitive analysis of key players in the Hot Dip Galvanizing market, including design, price, financial position, product portfolio, growth strategies, and regional presence, makes the report an investor’s guide.

To get more Insights: Request Free Sample Report

Hot Dip Galvanizing Market Dynamics

Infrastructure Investments Drive Growth

Infrastructure development, including areas such as transportation, energy, and urban development, requires the use of strong and long-lasting materials. Hot dip galvanizing offers a cost-efficient solution for this requirement by significantly prolonging the lifespan of steel structures through excellent corrosion protection driving the demand of the hot sip galvanizing market. The cost of producing hot dip galvanized steel is competitive compared to other corrosion protection methods. The efficiency of the zinc and steel supply chain, which are integral components of the galvanizing process, further supports the scalability of the hot dip galvanizing market.

Countries like China and India are major consumers of galvanized steel, while regions like North America and Europe are key exporters. This international trade helps grow the hot dip galvanizing market by ensuring the availability of galvanized steel across different regions. The industry life cycle of hot dip galvanizing is currently experiencing a growth phase, characterized by increasing demand and technological innovations. Additionally, government initiatives focused on urbanization, transportation networks, and renewable energy infrastructure create a fertile ground for the hot dip galvanizing market.

• The Indian government's National Infrastructure Pipeline, with a budget of $1.5 trillion allocated over five years, underscores the significant opportunities for market growth.

Technological innovation trends, such as the development of high-performance coatings and automated galvanizing processes, further drive the hot dip galvanizing market. The increasing investments in infrastructure projects globally are a crucial driver for the hot dip galvanizing market. The combination of cost-effective manufacturing, efficient supply chains, robust import/export dynamics, and market consolidation by leading companies positions the hot dip galvanizing market as a critical component in modern infrastructure development.

Impact of Environmental Regulations on the Hot Dip Galvanizing Market

Environmental regulations are a major challenge for the global hot dip galvanizing market, affecting its cost-profit ratio and creating significant barriers to entry. Strict regulations like the European Union’s REACH (Registration, Evaluation, Authorization, and Restriction of Chemicals) and the U.S. Clean Air Act impose rigorous standards on emissions and waste management. Adhering to these regulations requires substantial investment in advanced filtration and waste treatment systems, which raises operational costs and reduces profit margins. Differences in regulations between regions complicate international trade, affecting the supply chain dynamics for zinc and steel, the primary raw materials for hot dip galvanizing. For example, the imposition of tariffs on steel imports by the U.S. under Section 232 has led to fluctuations in raw material prices, impacting the overall cost structure and pricing strategies of galvanizing companies.

These trade barriers further worsen market volatility, leading to unpredictable cost scenarios that hinder stable financial planning and pricing strategies. The hot dip galvanizing sector is heavily influenced by market dominance, with a few major players holding control and having the capacity to handle environmental compliance costs more effectively. This results in an imbalanced competition landscape, putting smaller companies at a greater financial disadvantage due to regulatory expenses. Consequently, market consolidation may occur as these smaller entities either get bought out or forced out of the market.

Disparities in operational costs arise from varying subsidies and tax benefits for sustainable practices in different regions, impacting global pricing strategies and posing challenges in maintaining competitive pricing worldwide. The environmental regulations place significant operational and financial burdens on the hot dip galvanizing market. The need for substantial investment in compliance, combined with the complexities introduced by trade policies and market dominance, creates a challenging environment for both existing players and potential new entrants.

Hot Dip Galvanizing Market Segment Analysis

By Product Type, According to SMR research, the Sheet and Coil segment held the largest market share and dominated the Hot Dip Galvanizing market in 2025. The dominance of the segment is owing to its crucial role in sectors such as automotive, construction, and appliances, where durability and resistance to corrosion are very important. In the automotive industry, hot dip galvanized sheets and coils are crucial for making body panels and structural components, ensuring longevity and safety. The construction sector also heavily depends on these materials for roofing, walling, and structural steel, where there is a high demand for long-lasting, maintenance-free solutions. Additionally, the appliance industry uses galvanized sheets and coils in products like refrigerators and washing machines, which require both aesthetic appeal and functional resilience.

The strong demand for galvanized sheets and coils is also driven by their cost-effectiveness and superior performance compared to other methods of corrosion protection. Technological advancements in galvanizing processes have improved the quality and efficiency of production, making these materials more accessible and appealing to a wider range of industries. The continuous growth of urbanization and infrastructure development, particularly in emerging economies, has increased the need for galvanized materials, ensuring steady market growth. The increasing awareness of sustainability and environmental impact has led to a growing preference for galvanized steel, given its recyclability and reduced need for frequent replacements.

This aligns with the global shift towards more sustainable construction practices and automotive manufacturing. Market players are also investing in research and development to innovate and improve the properties of galvanized sheets and coils, addressing specific industry requirements and expanding their application scope. The dominance of the Sheet and Coil sector in the global hot dip galvanizing market is supported by its essential role in key industries, technological advancements, economic benefits, and alignment with sustainability trends. This sector's strength is expected to continue, driven by ongoing industrial growth and evolving market demands.

- In 2025, China's total exports of galvanized sheets (strip) reached 1,099,100 tons.

Hot Dip Galvanizing Market Regional Analysis

Asia Pacific dominated the Hot Dip Galvanizing market in 2025, with China leading as the top producer and a significant influencer in international trade. The region has established itself as the leading global market for hot dip galvanizing, driven by a strong demand for corrosion-resistant steel products in various industries. This dominance is the result of several factors, including rapid urbanization, infrastructure development, and a growing manufacturing sector. The hot dip galvanizing market dominance of the region is built upon its strong construction and infrastructure growth.

Governments in the region have prioritized the use of hot dip galvanized steel structures owing to their exceptional durability and long lifespan. The demand for galvanized steel has risen significantly, driven by the construction of tall buildings and extensive transportation networks, further boosting hot dip galvanizing market growth. Additionally, the increasing automotive industry is a key driver of the hot dip galvanizing market and has played a significant role in the region's rise to dominance. Strict safety regulations and consumer preferences for corrosion-resistant vehicles have led to increased use of galvanized steel components, ensuring longer product lifespan and reliability.

The Asia Pacific region has a strong manufacturing ecosystem, covering industries such as machinery, appliances, and industrial equipment. The need for corrosion protection in these sectors has led to the widespread use of hot dip galvanized steel. With ample raw materials and a skilled labor force, Asia Pacific has become a hub for manufacturing, enabling efficient production and distribution of hot dip galvanized steel products to global markets. As the global economy shifts towards Asia Pacific, the region's dominance in the hot dip galvanizing market is expected to strengthen further. With governments prioritizing infrastructure development, manufacturers seeking cost-effective corrosion protection solutions, and consumers requesting durable products, the demand for galvanized steel is set to increase, solidifying Asia Pacific's position as a key player in the hot dip galvanizing market.

Hot Dip Galvanizing Market Competitive Landscape

Analysis within this comprehensive study emphasizes the transformative nature of the industry, spotlighting major players such as ArcelorMittal (Luxembourg), Gerdau (Brazil), Nucor (USA), ThyssenKrupp (Germany), Steel Dynamics (USA), Nippon Steel and Sumitomo Metal (Japan), United States Steel Corporation (USA), Voestalpine Group (Austria), etc among others. These companies are pushing boundaries, investing in research and development to expand their product lines, and undertaking strategic activities including contractual agreements, mergers and acquisitions, and collaborations with other organizations. The future of the Hot Dip Galvanizing Market promises to be vibrant and dynamic, driven by the use of cutting-edge coating technologies that provide superior corrosion protection.

- In 2025, ArcelorMittal acquired Riwald Recycling, a state-of-the-art ferrous scrap metal recycling business in the Netherlands. This acquisition is part of ArcelorMittal's decarbonization strategy.

- In 2024, ThyssenKrupp Steel launched a new hot dip galvanizing line, FBA 10, in Dortmund with a capacity of 600,000 metric tons per year. The investment exceeds a quarter of a billion euros. This, along with the existing FBA 8 line, will increase annual production to around one million metric tons in Dortmund, solidifying its position in high-quality surface technologies in Europe.

|

Hot Dip Galvanizing Market Scope |

|

|

Market Size in 2025 |

USD 70.28 Billion. |

|

Market Size in 2034 |

USD 120.29 Billion. |

|

CAGR (2026-2034) |

6.15% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Segments |

By Product Type Sheet and Coil Tubes and Pipes Wires Others |

|

By End Use Industry Construction Automotive Chemical Electronic Appliances Others |

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Player in the Hot Dip Galvanizing Market

- ArcelorMittal (Luxembourg)

- Gerdau (Brazil)

- Nucor (USA)

- ThyssenKrupp (Germany)

- Steel Dynamics (USA)

- Nippon Steel and Sumitomo Metal (Japan)

- United States Steel Corporation (USA)

- Voestalpine Group (Austria)

- Tata Steel (India)

- NLMK Group (Russia)

- Valmont Industries (USA)

- Rolled Steel Products (California)

- JFE Steel (Japan)

- POSCO (South Korea)

- Hyundai Steel (South Korea)

- JSW Steel (India)

- Baosteel (China)

- Shougang (China)

- Ansteel Group (China)

- Magang Group (China)

- SMC (Japan)

- China Steel Corporation (Taiwan)

- XX Inc

Frequently Asked Questions

Rapid urbanization, infrastructure development, and the thriving automotive industry are fueling growth in the global Hot Dip Galvanizing market.

Investors capitalize on opportunities in the Hot Dip Galvanizing market by investing in companies that manufacture galvanized steel products, provide hot dip galvanizing services, or supply equipment and materials to the industry.

The Market size was valued at USD 70.28 Billion in 2025 and the total Market revenue is expected to grow at a CAGR of 6.15% from 2026 to 2034, reaching nearly USD 120.29 Billion.

The segments covered in the market report are product type, end-use industry, and region.

1. Research Methodology

1.1 Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Research Assumption

2. Hot Dip Galvanizing Market Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026– 2034) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Global Hot Dip Galvanizing Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Business Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

4. Hot Dip Galvanizing Market: Dynamics

4.1. Hot Dip Galvanizing Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Hot Dip Galvanizing Market Drivers

4.3. Hot Dip Galvanizing Market Restraints

4.4. Hot Dip Galvanizing Market Opportunities

4.5. Hot Dip Galvanizing Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factor

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Regulatory Landscape by Region

4.9.1. North America

4.9.2. Europe

4.9.3. Asia Pacific

4.9.4. Middle East and Africa

4.9.5. South America

5. Hot Dip Galvanizing Market: Global Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

5.1. Hot Dip Galvanizing Market Size and Forecast, by Product Type (2026-2034)

5.1.1. Sheet and Coil

5.1.2. Tubes and Pipes

5.1.3. Wires

5.1.4. Others

5.2. Hot Dip Galvanizing Market Size and Forecast, by End Use Industry (2026-2034)

5.2.1. Construction

5.2.2. Automotive

5.2.3. Chemical

5.2.4. Electronic Appliances

5.2.5. Others

5.3. Hot Dip Galvanizing Market Size and Forecast, by Region (2026-2034)

5.3.1. North America

5.3.2. Europe

5.3.3. Asia Pacific

5.3.4. Middle East and Africa

5.3.5. South America

6. North America Hot Dip Galvanizing Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

6.1. North America Hot Dip Galvanizing Market Size and Forecast, by Product Type (2026-2034)

6.1.1. Sheet and Coil

6.1.2. Tubes and Pipes

6.1.3. Wires

6.1.4. Others

6.2. North America Hot Dip Galvanizing Market Size and Forecast, by End Use Industry (2026-2034)

6.2.1. Construction

6.2.2. Automotive

6.2.3. Chemical

6.2.4. Electronic Appliances

6.2.5. Others

6.3. North America Hot Dip Galvanizing Market Size and Forecast, by Country (2026-2034)

6.3.1. United States

6.3.2. Canada

6.3.3. Mexico

7. Europe Hot Dip Galvanizing Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

7.1. Europe Hot Dip Galvanizing Market Size and Forecast, by Product Type (2026-2034)

7.2. Europe Hot Dip Galvanizing Market Size and Forecast, by End Use Industry (2026-2034)

7.3. Europe Hot Dip Galvanizing Market Size and Forecast, by Country (2026-2034)

7.3.1. United Kingdom

7.3.2. France

7.3.3. Germany

7.3.4. Italy

7.3.5. Spain

7.3.6. Sweden

7.3.7. Austria

7.3.8. Rest of Europe

8. Asia Pacific Hot Dip Galvanizing Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

8.1. Asia Pacific Hot Dip Galvanizing Market Size and Forecast, by Product Type (2026-2034)

8.2. Asia Pacific Hot Dip Galvanizing Market Size and Forecast, by End Use Industry (2026-2034)

8.3. Asia Pacific Hot Dip Galvanizing Market Size and Forecast, by Country (2026-2034)

8.3.1. China

8.3.2. S Korea

8.3.3. Japan

8.3.4. India

8.3.5. Australia

8.3.6. Indonesia

8.3.7. Malaysia

8.3.8. Vietnam

8.3.9. Taiwan

8.3.10. Rest of Asia Pacific

9. Middle East and Africa Hot Dip Galvanizing Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

9.1. Middle East and Africa Hot Dip Galvanizing Market Size and Forecast, by Product Type (2026-2034)

9.2. Middle East and Africa Hot Dip Galvanizing Market Size and Forecast, by End Use Industry (2026-2034)

9.3. Middle East and Africa Hot Dip Galvanizing Market Size and Forecast, by Country (2026-2034)

9.3.1. South Africa

9.3.2. GCC

9.3.3. Nigeria

9.3.4. Rest of ME&A

10. South America Hot Dip Galvanizing Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

10.1. South America Hot Dip Galvanizing Market Size and Forecast, by Product Type (2026-2034)

10.2. South America Hot Dip Galvanizing Market Size and Forecast, by End Use Industry (2026-2034)

10.3. South America Hot Dip Galvanizing Market Size and Forecast, by Country (2026-2034)

10.3.1. Brazil

10.3.2. Argentina

10.3.3. Rest Of South America

11. Company Profile: Key Players

11.1. ArcelorMittal (Luxembourg)

11.1.1. Company Overview

11.1.2. Business Portfolio

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Gerdau (Brazil)

11.3. Nucor (USA)

11.4. ThyssenKrupp (Germany)

11.5. Steel Dynamics (USA)

11.6. Nippon Steel and Sumitomo Metal (Japan)

11.7. United States Steel Corporation (USA)

11.8. Voestalpine Group (Austria)

11.9. Tata Steel (India)

11.10. NLMK Group (Russia)

11.11. Valmont Industries (USA)

11.12. Rolled Steel Products (California)

11.13. JFE Steel (Japan)

11.14. POSCO (South Korea)

11.15. Hyundai Steel (South Korea)

11.16. JSW Steel (India)

11.17. Baosteel (China)

11.18. Shougang (China)

11.19. Ansteel Group (China)

11.20. Magang Group (China)

11.21. SMC (Japan)

11.22. China Steel Corporation (Taiwan)

11.23. XX Inc

12. Key Findings

13. Analyst Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook