High Voltage Equipment Market Global Industry Analysis and Forecast (2026-2032)

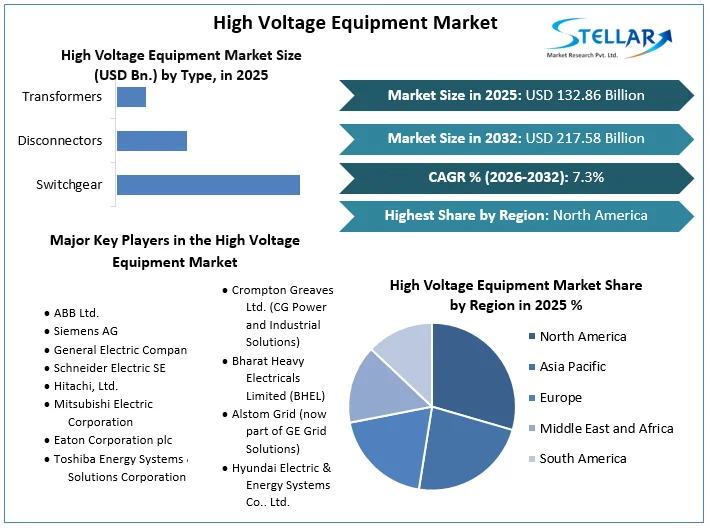

High Voltage Equipment Market was valued at USD 132.86 Billion in 2025 and expected to grow at a CAGR of 7.3% during the forecast period (2026-2032).

High Voltage Equipment Market Overview:

The market for high voltage equipment is a vibrant and crucial part of the larger electrical industry. To meet the demands of power transmission, distribution, and industrial uses, high voltage equipment consists of a variety of tools built to function effectively and safely at voltage levels above 72.5 kV. The rising demand for electricity on a global scale, the incorporation of renewable energy sources, and grid modernization activities are the main drivers of market expansion. In order to permit long-distance power transmission from renewable energy producing sites to metropolitan centers, efficient high voltage equipment is essential as countries work to switch to cleaner energy sources. The market is further boosted by the continued demand for dependable electricity distribution networks brought on by growing urbanization and industrialisation.

However, the business also faces obstacles including strict safety regulations and environmental issues, which call for constant innovation in design and production techniques. Key competitors in the market, including both established manufacturers and more recent entrants, are competing to deliver novel solutions that put an emphasis on energy efficiency, compact designs, and cutting-edge monitoring systems. The High Voltage Equipment Marketis anticipated to experience breakthroughs in insulating materials, sensor technology, and smart grid integration as technology continues to advance, thereby playing a crucial role in determining the future of the world's energy infrastructure.

To get more Insights: Request Free Sample Report

High Voltage Equipment Market Dynamics:

Drivers: A number of strong forces that are changing the energy environment are propelling the market for high voltage equipment. First and foremost, the need for effective power transmission and distribution networks is being fueled by the rising global demand for electricity, which is being driven by population increase, urbanization, and industrial expansion. There is a greater need for high voltage equipment to effectively transfer power generated from geographically dispersed renewable sites to population centers as renewable energy sources gain popularity as alternatives to conventional fossil fuels. Additionally, to increase the dependability, effectiveness, and sustainability of their electrical infrastructures, governments and utility companies around the world are funding grid modernization projects.

Opportunities: The market for high voltage equipment offers a wide range of exciting options that take into account the changing energy landscape and technical developments. The incorporation of renewable energy sources into the electrical system represents one important route. Utilizing solar, wind, and other renewable energies is becoming more important as governments and businesses throughout the world make commitments to reduce carbon emissions. In order to effectively transport and distribute the sporadic and frequently scattered electricity produced by these sources, high voltage equipment must be developed. A rich foundation for innovation is also provided by the development of smart grids and digitization.

Manufacturers of high voltage equipment have the opportunity to develop products that seamlessly connect with digital monitoring and control systems, facilitating real-time data analysis, preventative maintenance, and superior grid management. The global push for electrification in numerous industries, including transportation and industry, presents another intriguing prospect. In order to meet the rising demand for electricity, high voltage infrastructure must be expanded to include things like electric vehicle charging stations and electrified industrial operations. Additionally, as urbanization and industrialization activities pick up steam, emerging economies looking to upgrade their power infrastructures create untapped opportunities for high voltage equipment. Manufacturers might explore partnerships and collaborations in this environment to share knowledge and create solutions that address particular regional concerns.

Restraints: If the market for high voltage equipment has a lot of promise, there are some obstacles that could slow its expansion. The strict regulatory framework and safety requirements that control the design, production, and use of high voltage equipment are one of the main challenges. To safeguard the safety of workers, communities, and the environment, manufacturers must traverse complicated compliance standards, which frequently increases development costs and extends time to market. The capital-intensive nature of high voltage projects also presents a challenge, especially for developing nations that may find it difficult to get the funding required for significant infrastructure projects.

Market expansion may also be hampered by economic ambiguity, volatility in raw material prices, and financial issues. Additionally, the adoption of innovative high voltage solutions may be hampered by the relatively sluggish rate of grid modernization and extension in some locations, postponing the market's potential for growth. Entry obstacles can also be caused by environmental issues and public opposition to the installation of high voltage equipment due to alleged health dangers linked with electromagnetic fields.

High Voltage Equipment Market Segment Analysis:

By Type, Through a segmentation based on several equipment types, which each play a significant role in facilitating effective power transmission, distribution, and associated applications, the High Voltage Equipment Market can be thoroughly examined. Circuit breakers, which come in a variety of forms like air, oil, gas, and vacuum circuit breakers, act as crucial safeguards, preventing overloads and short circuits on electrical circuits. Voltage conversion is made possible by transformers, which range from power transformers for transferring large amounts of energy to distribution transformers for regional distribution networks.

Surge arresters, also known as lightning arresters, are essential parts that deflect excess electrical energy brought on by lightning strikes or switching events, protecting high voltage systems and equipment. Insulators, on the other hand, protect possible threats by blocking electrical current passage between conductive components, maintaining the integrity of power lines and substations. Disconnect switches, fuses, and circuit breakers are examples of switchgear, which provides essential control and protection mechanisms to isolate electrical equipment, improving safety and dependability. Last but not least, disconnectors, sometimes referred to as isolators, offer the capacity to de-energize particular power system segments for maintenance or isolation purposes, functioning as essential elements in the overall power infrastructure.

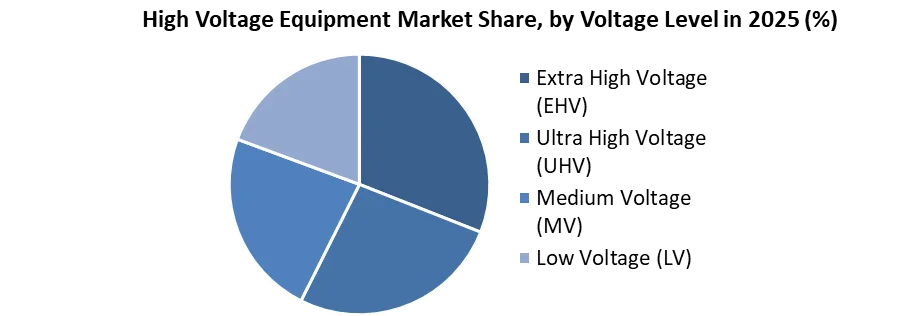

By Voltage Level, a classification that highlights the distinctive functions and uses of numerous pieces of equipment in the power sector. Long-distance power transmission networks are supported by Extra High Voltage (EHV) equipment, which is made for voltages between 132 kV and 330 kV. The widespread distribution of energy is made possible by the ability of EHV equipment to transfer electricity effectively over vast areas. This is made possible by the connection of power producing sources to distribution networks. Urban centers, industrial complexes, and commercial areas all have localized distribution networks that depend on medium voltage (MV) equipment, which runs between 1 kV and 52 kV. This group ensures dependable power supply to a variety of industries by acting as a vital link between high voltage transmission networks and low voltage end users.

The High Voltage Equipment Market may be divided into segments based on voltage level to provide a thorough understanding of how various equipment types accommodate various energy delivery, transmission, and consumption phases. Stakeholders can utilize this segmentation strategy to customize their strategies to the particular requirements and opportunities given by each voltage level as the energy environment changes as a result of rising demand, greater renewable integration, and developing technologies.

By Application, the market meets the demand for effective long-distance energy transportation from producing facilities to substations and distribution networks by starting with power transmission. Extra high voltage (EHV) and ultra high voltage (UHV) equipment is used in this section to provide low power losses during transmission, promoting the sustainability of energy. By enabling the conversion of higher voltage electricity to levels acceptable for local consumption, Medium Voltage (MV) equipment plays a key role in power distribution by guaranteeing a steady and dependable supply of electricity to residential, commercial, and industrial regions. Another crucial application is substations, which control voltage levels and enable efficient distribution by using a variety of high-voltage devices like transformers, circuit breakers, and switchgear.

A growing application area, the grid integration of renewable energy sources calls for specialist high voltage equipment to manage the intermittent and erratic outputs of sources like solar and wind. The global transition to cleaner energy systems depends on this section. Whether in manufacturing, data centers, mining, or other industrial applications, industries depend on high voltage equipment to power necessary processes and ensure operational reliability. In order to consistently supply electricity for numerous activities, from lights to complicated systems in transportation hubs and commercial complexes, infrastructure projects also make use of high voltage equipment. High voltage equipment is changing to accept smart grid technologies in the context of grid modernization, improving grid efficiency, reliability, and resilience by enabling real-time monitoring and control.

High Voltage Equipment Market Regional Insights:

The market for high voltage equipment in North America is impacted by a heavy emphasis on grid upgrading. The need to invest in equipment upgrades for better efficiency, dependability, and integration of smart grid technologies is driven by the deteriorating state of the electrical infrastructure in nations like the United States and Canada. Additionally, the switch to greener energy sources fuels a demand for machinery capable of integrating renewable energy sources into the power system. The market landscape is also changing as a result of initiatives to electrify transportation, including electric vehicles and charging infrastructure.

When it comes to sustainable energy options, Europe is in the forefront. The market for high voltage equipment is shaped by the European Union's focus on decarbonization, energy efficiency, and renewable energy integration. The demand for technology capable of combining sporadic sources like wind and solar is driven by the region's aggressive renewable energy ambitions, such as the European Green Deal. The need for dependable high voltage equipment for international power exchange is increased by cross-border interconnections and initiatives to establish a single energy market.

In the Asia-Pacific area, urbanization, industrialisation, and energy consumption are all happening quickly. To accommodate the rising demand for electricity, nations like China and India are making significant investments in increasing their power generation and distribution facilities. The demand for high voltage equipment suitable for both conventional and renewable energy sources rises as these countries embrace renewable energy as part of their sustainability goals. The usage of modern high voltage solutions is accelerating due to the growth of smart cities and industrial complexes.

A growing interest in renewable energy sources coexists with the Middle East's emphasis on oil and gas extraction. The region's nations are investing in renewable energy initiatives like solar farms, which require high voltage equipment to be integrated into the grid. Advanced high voltage solutions can be used in large-scale infrastructure projects, particularly those in distant locations, to guarantee a consistent and dependable power supply.

|

High Voltage Equipment Scope |

|

|

Market Size in 2025 |

USD 132.86 Bn. |

|

Market Size in 2032 |

USD 217.58 Bn. |

|

CAGR (2026-2032) |

7.3% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segment Scope |

By Type

|

|

By Voltage Level

|

|

|

By Application

|

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

High Voltage Equipment Market Key Players:

- ABB Ltd.

- Siemens AG

- General Electric Company

- Schneider Electric SE

- Hitachi, Ltd.

- Mitsubishi Electric Corporation

- Eaton Corporation plc

- Toshiba Energy Systems & Solutions Corporation

- Crompton Greaves Ltd. (CG Power and Industrial Solutions)

- Bharat Heavy Electricals Limited (BHEL)

- Alstom Grid (now part of GE Grid Solutions)

- Hyundai Electric & Energy Systems Co., Ltd.

- TBEA Co., Ltd.

- Fuji Electric Co., Ltd.

- Nissin Electric Co., Ltd.

Frequently Asked Questions

The global High Voltage Equipment Market is studied from 2025 to 2032.

North America region held the highest share in 2025.

The CAGR for High Voltage Equipment Market is 7.3%.

The segments covered in the market report are by type, voltage level, application and region.

1. High Voltage Equipment Market: Research Methodology

2. High Voltage Equipment Market: Executive Summary

3. High Voltage Equipment Market: Competitive Landscape

3.1. Stellar Competition Matrix

3.2. Competitive Landscape

3.3. Key Players Benchmarking

3.4. Market Structure

3.4.1. Market Leaders

3.4.2. Market Followers

3.4.3. Emerging Players

3.5. Consolidation of the Market

4. High Voltage Equipment Market: Dynamics

4.1. Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Market Drivers by Region

4.2.1. North America

4.2.2. Europe

4.2.3. Asia Pacific

4.2.4. Middle East and Africa

4.2.5. South America

4.3. Market Restraints

4.4. Market Opportunities

4.5. Market Challenges

4.6. PORTER’s Five Forces Analysis

4.7. PESTLE Analysis

4.8. Value Chain Analysis

4.9. Regulatory Landscape by Region

4.9.1. North America

4.9.2. Europe

4.9.3. Asia Pacific

4.9.4. Middle East and Africa

4.9.5. South America

5. High Voltage Equipment Market Size and Forecast by Segments (by Value USD and Volume Units)

5.1. High Voltage Equipment Market Size and Forecast, By Type (2025-2032)

5.1.1. Switchgear

5.1.2. Disconnectors

5.1.3. Transformers

5.2. High Voltage Equipment Market Size and Forecast, By Voltage Level (2025-2032)

5.2.1. Extra High Voltage (EHV)

5.2.2. Ultra High Voltage (UHV)

5.2.3. Medium Voltage (MV)

5.2.4. Low Voltage (LV)

5.3. High Voltage Equipment Market Size and Forecast, By Application(2025-2032)

5.3.1. Power Transmission

5.3.2. Power Distribution

5.4. High Voltage Equipment Market Size and Forecast, by Region (2025-2032)

5.4.1. North America

5.4.2. Europe

5.4.3. Asia Pacific

5.4.4. Middle East and Africa

5.4.5. South America

6. North America High Voltage Equipment Market Size and Forecast (by Value USD and Volume Units)

6.1. North America High Voltage Equipment Market Size and Forecast, By Type (2025-2032)

6.1.1. Switchgear

6.1.2. Disconnectors

6.1.3. Transformers

6.2. North America High Voltage Equipment Market Size and Forecast, By Voltage Level (2025-2032)

6.2.1. Extra High Voltage (EHV)

6.2.2. Ultra High Voltage (UHV)

6.2.3. Medium Voltage (MV)

6.2.4. Low Voltage (LV)

6.3. North America High Voltage Equipment Market Size and Forecast, By Application(2025-2032)

6.3.1. Power Transmission

6.3.2. Power Distribution

6.4. North America High Voltage Equipment Market Size and Forecast, by Country (2025-2032)

6.4.1. United States

6.4.2. Canada

6.4.3. Mexico

7. Europe High Voltage Equipment Market Size and Forecast (by Value USD and Volume Units)

7.1. Europe High Voltage Equipment Market Size and Forecast, By Type (2025-2032)

7.1.1. Switchgear

7.1.2. Disconnectors

7.1.3. Transformers

7.2. Europe High Voltage Equipment Market Size and Forecast, By Voltage Level (2025-2032)

7.2.1. Extra High Voltage (EHV)

7.2.2. Ultra High Voltage (UHV)

7.2.3. Medium Voltage (MV)

7.2.4. Low Voltage (LV)

7.3. Europe High Voltage Equipment Market Size and Forecast, By Application(2025-2032)

7.3.1. Power Transmission

7.3.2. Power Distribution

7.4. Europe High Voltage Equipment Market Size and Forecast, by Country (2025-2032)

7.4.1. UK

7.4.2. France

7.4.3. Germany

7.4.4. Italy

7.4.5. Spain

7.4.6. Sweden

7.4.7. Austria

7.4.8. Rest of Europe

8. Asia Pacific High Voltage Equipment Market Size and Forecast (by Value USD and Volume Units)

8.1. Asia Pacific High Voltage Equipment Market Size and Forecast, By Type (2025-2032)

8.1.1. Switchgear

8.1.2. Disconnectors

8.1.3. Transformers

8.2. Asia Pacific High Voltage Equipment Market Size and Forecast, By Voltage Level (2025-2032)

8.2.1. Extra High Voltage (EHV)

8.2.2. Ultra High Voltage (UHV)

8.2.3. Medium Voltage (MV)

8.2.4. Low Voltage (LV)

8.3. Asia Pacific High Voltage Equipment Market Size and Forecast, By Application(2025-2032)

8.3.1. Power Transmission

8.3.2. Power Distribution

8.4. Asia Pacific High Voltage Equipment Market Size and Forecast, by Country (2025-2032)

8.4.1. China

8.4.2. S Korea

8.4.3. Japan

8.4.4. India

8.4.5. Australia

8.4.6. Indonesia

8.4.7. Malaysia

8.4.8. Vietnam

8.4.9. Taiwan

8.4.10. Bangladesh

8.4.11. Pakistan

8.4.12. Rest of Asia Pacific

9. Middle East and Africa High Voltage Equipment Market Size and Forecast (by Value USD and Volume Units)

9.1. Middle East and Africa High Voltage Equipment Market Size and Forecast, By Type (2025-2032)

9.1.1. Switchgear

9.1.2. Disconnectors

9.1.3. Transformers

9.2. Middle East and Africa High Voltage Equipment Market Size and Forecast, By Voltage Level (2025-2032)

9.2.1. Extra High Voltage (EHV)

9.2.2. Ultra High Voltage (UHV)

9.2.3. Medium Voltage (MV)

9.2.4. Low Voltage (LV)

9.3. Middle East and Africa High Voltage Equipment Market Size and Forecast, By Application(2025-2032)

9.3.1. Power Transmission

9.3.2. Power Distribution

9.4. Middle East and Africa High Voltage Equipment Market Size and Forecast, by Country (2025-2032)

9.4.1. South Africa

9.4.2. GCC

9.4.3. Egypt

9.4.4. Nigeria

9.4.5. Rest of ME&A

10. South America High Voltage Equipment Market Size and Forecast (by Value USD and Volume Units)

10.1. South America High Voltage Equipment Market Size and Forecast, By Type (2025-2032)

10.1.1. Switchgear

10.1.2. Disconnectors

10.1.3. Transformers

10.2. South America High Voltage Equipment Market Size and Forecast, By Voltage Level (2025-2032)

10.2.1. Extra High Voltage (EHV)

10.2.2. Ultra High Voltage (UHV)

10.2.3. Medium Voltage (MV)

10.2.4. Low Voltage (LV)

10.3. South America High Voltage Equipment Market Size and Forecast, By Application(2025-2032)

10.3.1. Power Transmission

10.3.2. Power Distribution

10.4. South America High Voltage Equipment Market Size and Forecast, by Country (2025-2032)

10.4.1. Brazil

10.4.2. Argentina

10.4.3. Rest of South America

11. Company Profile: Key players

11.1. ABB Ltd.

11.1.1. Company Overview

11.1.2. Financial Overview

11.1.3. Business Portfolio

11.1.4. SWOT Analysis

11.1.5. Business Strategy

11.1.6. Recent Developments

11.2. Siemens AG

11.3. General Electric Company

11.4. Schneider Electric SE

11.5. Hitachi, Ltd.

11.6. Mitsubishi Electric Corporation

11.7. Eaton Corporation plc

11.8. Toshiba Energy Systems & Solutions Corporation

11.9. Crompton Greaves Ltd. (CG Power and Industrial Solutions)

11.10. Bharat Heavy Electricals Limited (BHEL)

11.11. Alstom Grid (now part of GE Grid Solutions)

11.12. Hyundai Electric & Energy Systems Co., Ltd.

11.13. TBEA Co., Ltd.

11.14. Fuji Electric Co., Ltd.

11.15. Nissin Electric Co., Ltd.

12. Key Findings

13. Industry Recommendation