Gaming Chips Market- Global Industry Analysis and Forecast 2026-2032

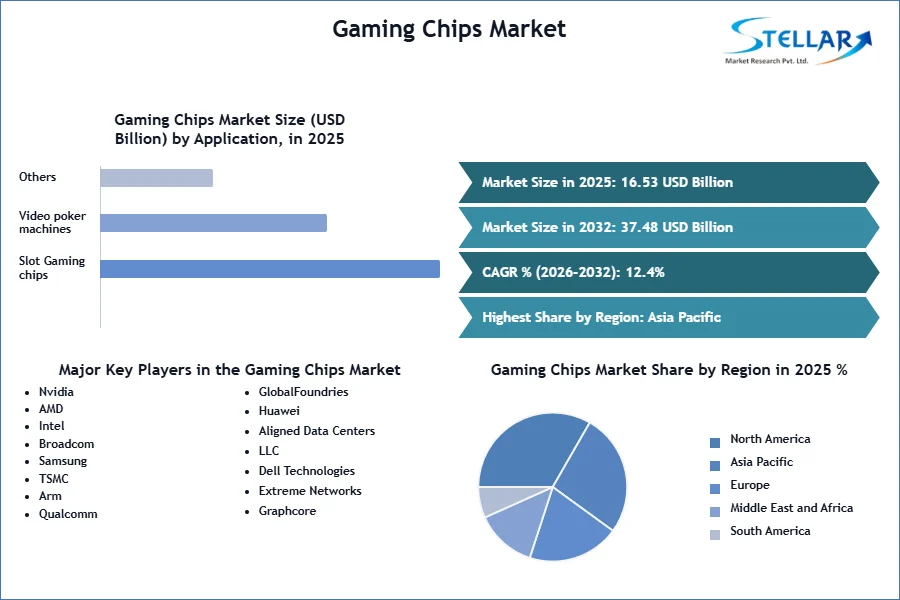

Gaming Chips Market size was valued at USD 16.53 Bn. in 2025 and the total Global Gaming Chips revenue is expected to grow at a CAGR of 12.4% from 2026 to 2032, reaching nearly USD 37.48 Bn. by 2032.

Gaming Chips Market Overview

Gaming chips are special processors made for gaming tools. They improve the capacity of gaming devices by giving them fast processing and advanced graphics skills. These chips are very important in making sure that consoles, PCs, and mobile gadgets can offer smooth and good quality gaming experiences. In the Gaming Chips Industry, these items are easily available in many places such as big electronics shops, internet sites for selling things, and specific gaming hardware services that offer products from well-known manufacturers like NVIDIA and AMD. The Gaming chip suppliers cater to various regional demands, with availability varying significantly.

Demand for gaming chips is boosted by the growing interest in high-performance gaming and the progress made in graphics technology. This trend results in a steady increase of market size. However, issues within the supply chain like production limitations and lack of semiconductors can impact the availability and pricing of gaming chips. The cost of production and manufacturing is affected by these supply issues, which then influence the cost-profit ratio as well as the profit margin for manufacturers. The expenses are managed through cost benefits and value chain analysis. Cost of services and revenue/sales show the economic dynamics of the industry.

Asia-Pacific and North America display strong performance in the Gaming Chips Market. This is because these areas have high rates of adoption for gaming as well as technological progress. In contrast, Europe and South America experience moderate growth because they show different degrees of market penetration and are influenced by economic factors too. Considering the end-user contribution to this market, it mainly comes from individual gamers and enthusiasts who have a continuous demand for top-performing hardware. On the other side of things, gaming console manufacturers along with PC builders impact this space significantly by integrating advanced chips into their products. Market trends such as units sold and import-export movements are still affecting the future of the industry.

To get more Insights: Request Free Sample Report

Gaming Chips Market Dynamics

Key Drivers and Trends in the Growing Gaming Chips Market

The Gaming Chips Market is growing strongly, supported by several important elements. The main factor that fuels this growth is the enlargement of the global gaming business. The increasing desire from customers for video games on different platforms like consoles, PCs, and mobile gadgets helps push forward the Gaming Chips Market. The increase in popularity of gaming is a reason for higher revenue/sales of gaming chip manufacturers. Technological advancements in semiconductor technology also play an important role.

Chips with more power and less energy consumption are becoming available, which greatly improves the experience of playing games by enhancing graphics quality and increasing processing speed and overall performance. Advancements like ray tracing and AI incorporation not only increase the gaming chips market but also push up units sold as gamers enhance their systems for the newest characteristics.

The new excitement around e-sports and competitive gaming has also added to the desire for gaming chips. People who play games professionally or simply enjoy them want the best and most recent gaming equipment to stay ahead of their competition. This change has caused more investments in the structure of gaming, such as advanced PCs made especially for playing games and top-quality consoles. This development is good for the gaming chips suppliers that are designed particularly for this type of use.

The increasing use of Virtual Reality (VR) and Augmented Reality (AR) in gaming needs chips that are specialized and have high performance. These chips manage the strong graphical and processing requirements of immersive gaming experiences. This improves the share for the Gaming Chips Industry and enhances the cost-profit ratio for manufacturers that produce such advanced solutions.

Challenges in the Gaming Chips Market are High Costs and Technical Problems

The Gaming Chips Market has potential for growth, but a main concern is the high costs linked to development. Making superior gaming chips requires significant research and development expenses along with complex manufacturing procedures. The expense of creating and operating foundries that make semiconductors is quite high. This might pose a significant difficulty for small firms or new participants, making it harder to compete well in the business. Supply chain disturbances also represent a strong obstacle. The industry of semiconductors is very vulnerable to problems in supply chains, as shown by current worldwide shortages of chips.

The disturbances might slow down or stop the making and supply of gaming chips. This affect the whole gaming hardware market, causing possible income reductions for those who create these chips. Overheating and power usage are technical problems that makers of gaming chips need to handle. Gaming chips that have high performance produce a lot of heat and use much power, creating difficulties in finding good cooling methods and being energy efficient at the same time. Handling these matters effectively is very important to keep chip performance and life span in good shape, which directly affects the value chain analysis for gaming chip products.

Trends and Innovations creates opportunities in the Gaming Chips Market

With the growing popularity of cloud gaming platforms, more possibilities are being opened up. Cloud gaming means one can stream games without having to possess powerful equipment, and this is creating demand for data centers and cloud infrastructure that need special chips. This shift not only expands the market for gaming chips but also gives cost benefits by lessening reliance on upgrading consumer hardware. The incorporation of AI and machine learning in gaming chips is another area where the potential is quite high. The ability to improve gaming experiences by using smart NPC behavior, graphic optimization that happens instantly, and personalized gaming could result in creating products with greater value that meet changing gamer needs.

Collaborations between gaming chip makers and game developers or platform suppliers, for instance, are a productive way to improve performance and create fresh solutions in the gaming field. These team-ups might result in mutual benefits for both hardware and software firms involved, promoting better integration within the game setup as well as an enhanced ecosystem of playfulness. Sustainability efforts - an area with rising potential. With the growing concerns related to the environment, there is a drive to create gaming chips that use less energy and which are more sustainable. If companies focus on green technologies, they might get attention from consumers who care about the environment and improve their competitive advantage by enhancing cost-benefit ratios as well as brand reputation in the Gaming Chips Industry.

Gaming Chips Market Segment Analysis

By Chip Type, the Slot Gaming Chips segment held the largest market share in the year 2024. This is mainly because of the heavy usage of slot machines found in physical and virtual casinos. Slot machines are a very common type of gaming equipment globally, creating notable demand for special gaming chips that help to run them. The chips used in slot machines are crucial for their market leadership because they need to be high-performance and dependable.

This is due to the significant part these machines play in gaming, as well as the large number of units sold within this segment. Slot machines have a dominant place with total market share - they are very much in demand because people like playing them and many different types of gaming establishments use them. Video poker machines, even though they have a much smaller share than slot gaming chips, still hold a significant share. The need for video poker machines is supported by their liking in casinos and game places, but it doesn't spread as much as slot machines.

Gaming Chips Market Regional Insights

Asia Pacific region dominated the Gaming Chips Market in the year 2024 and is expected to dominate throughout the forecast period. The position of this region is strong due to the availability of Gaming chip manufacturers and there is high demand from consumers in the fast-growing gaming market especially in countries like China, South Korea, and Japan. The substantial market share of the region is related to its large number of gaming chip suppliers and a big consumer base, showing an important tendency in the Gaming Chips Industry. Asia Pacific's strength in manufacturing is further strengthened by the favorable cost benefits it offers. This includes areas such as cost of production, cost of manufacturing, and cost of services that improve its ratio between costs and profits, along with the total profit margin.

On the other hand, the market in North America is also very important. It has a big role due to strong gaming demand and good technology setup. The market share of this region is high due to its high revenue/sales. The value chain analysis of North America shows good operations and many unit sales. Also, the import-export connection boosts its position in the market. The two regions demonstrate significant facets of the Gaming Chips Market, such as the influence of cost elements, EPS, and market trends on their positions in the worldwide gaming chips scene.

Gaming Chips Import and Export

The main countries receiving exports from the worldwide Gaming Chips Market are the United States, Peru, and India. The leading three exporters of gaming chips are China with more than 2,200 shipments, followed by the United States having over 500 shipments, and third place taken up by South Korea which has more than 250 shipments. On the other side, most gaming chips come from China, then we have the United States and South Korea as top importers. As the top country importing, the United States has more than 950 shipments. Peru and India follow with over 560 and 550 shipments. This shows the important link between demand and supply in the Gaming Chips Industry globally; these countries play a crucial role by being the main receivers of goods through the supply chain.

Gaming Chips Market Competitive Landscape

Nvidia Corporation is a dominant name in the Gaming Chips Market, and its Gaming segment plays an important part in the total revenue. In 2024, Nvidia's Gaming revenue was $10,447 million which shows progress from $9,067 million in 2023 but a small decrease compared to the top point of $12,462 million seen back in 2022. The company's Gaming segment includes sales from its GeForce series GPUs which are famous for being high-quality products.

They have advanced features like real-time ray tracing as well as performance boosts driven by artificial intelligence technology. Nvidia's GPUs, which are famous for their top-level performance, are utilized in a vast variety of gaming tools. They are found inside costly personal computers that gamers use to enjoy high-quality game experiences. Constantly improving and dedicated to offering superior experiences in games keeps Nvidia at the front of the Gaming Chips Industry.

In the Gaming Chips Market, Advanced Micro Devices (AMD) has notably enhanced its position with the introduction of Radeon series GPUs and Ryzen CPUs. The strength of AMD's competition is in providing high-performance items at cost-effective price ranges, which makes advanced gaming abilities more reachable to everyone. RDNA architecture from AMD for its Radeon GPUs provides strong performance and efficiency, suitable for both casual and serious gamers. AMD's important partnerships with big gaming console makers, like Sony for the PlayStation 5 and Microsoft for the Xbox Series X, have made AMD a strong player in the console market.

Intel Corporation, a well-known name in the CPU market for many years, is now making its presence felt in the Gaming Chips Sector with its new Intel Arc series GPUs. Intel has always been favored by gamers because of its high-performance CPUs that handle demanding gaming and multitasking tasks. By stepping into this separate GPU marketplace, Intel hopes to provide a complete solution for those who love playing games.

The Intel Arc GPUs, which are going to be released soon, intend to offer a strong gaming performance along with advanced graphics and AI-powered features. Intel's method in the Gaming Chips industry focuses on improving the cost of production, cost of manufacturing as well as cost of services so it gets good returns on its costs and also makes a profit. By using value chain investigation and managing the supply chain properly, Intel maintains a consistent delivery of high-quality gaming chips. This contributes towards its increasing revenue from units sold in the market.

The Gaming Chips Market is doing well due to the growth in the gaming industry and people wanting more games on different platforms. Progress in semiconductor technology, especially power-saving chips and new features such as ray tracing and AI are improving gaming experiences which aids market growth. E-sports and VR/AR usage also add to the need for high-performance gaming chips. Even if there are difficulties like expensive development and problems in supply chains, chances for growth exist with cloud gaming and AI blending. Understanding from different regions shows that Asia Pacific has the upper hand because of big benefits in manufacturing, while North America is still an important market. Big companies such as Nvidia, AMD, and Intel are leading the way in innovation and competition within this sector.

|

Gaming Chips Market Scope |

|

|

Market Size in 2025 |

USD 16.53 Bn. |

|

Market Size in 2032 |

USD 37.48 Bn. |

|

CAGR (2026-2032) |

12.4% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segments |

By Chip Type Slot Gaming chips Video poker machines Gaming chips Others |

|

By Application Casino Others |

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Player in the Gaming Chips Market

Frequently Asked Questions

Environmental considerations in gaming chips production include the significant energy consumption and carbon footprint associated with semiconductor manufacturing, the need for sustainable and energy-efficient production processes, and the management of electronic waste generated from outdated or discarded gaming hardware.

The challenges faced by the gaming chips market include high development and manufacturing costs, supply chain disruptions, technical issues such as overheating and power consumption, and the difficulty for smaller companies to compete with established players.

The Market size was valued at USD 16.53 Billion in 2025 and the total Market revenue is expected to grow at a CAGR of 12.4% from 2026 to 2032, reaching nearly 37.48 Billion.

The segments covered in the market report are By Chip Type, and Application.

1. Gaming Chips Market: Research Methodology

2. Global Gaming Chips Market: Competitive Landscape

2.1. Stellar Competition Matrix

2.2. Competitive Landscape

2.3. Market share analysis of major players

2.4. Products specific analysis

2.4.1. Main suppliers and their market positioning

2.4.2. Key customers and adoption rates across different sectors

2.5. Key Players Benchmarking

2.5.1. Company Name

2.5.2. Product Segment

2.5.3. End-user Segment

2.5.4. Revenue (2025)

2.5.5. Geographic distribution of major customers

2.6. Market Structure

2.6.1. Market Leaders

2.6.2. Market Followers

2.6.3. Emerging Players

2.7. Mergers and Acquisitions Details

3. Gaming Chips Market: Executive Summary

4. Gaming Chips Market: Dynamics

4.1. Market Drivers

4.2. Market Trends by Region

4.2.1. North America

4.2.2. Europe

4.2.3. Asia Pacific

4.2.4. Middle East and Africa

4.2.5. South America

4.3. Market Drivers by Region

4.3.1. North America

4.3.2. Europe

4.3.3. Asia Pacific

4.3.4. Middle East and Africa

4.3.5. South America

4.4. Market Restraints

4.5. Market Opportunities

4.6. Market Challenges

4.7. PORTER’s Five Forces Analysis

4.8. PESTLE Analysis

4.9. Strategies for New Entrants to Penetrate the Market

4.10. Regulatory Landscape by Region

4.10.1. North America

4.10.2. Europe

4.10.3. Asia Pacific

4.10.4. Middle East and Africa

4.10.5. South America

4.11. Import - Export by Countries

4.11.1. Germany

4.11.2. China

4.11.3. Netherlands

4.11.4. South Korea

4.11.5. Others

5. Gaming Chips Market Size and Forecast by Segments (by Value USD Billion)

5.1. Gaming Chips Market Size and Forecast, By Chip Type (2026-2032)

5.1.1. Slot Gaming chips

5.1.2. Video poker machines Gaming chips

5.1.3. Others

5.2. Gaming Chips Market Size and Forecast, By Application (2026-2032)

5.2.1. Casino

5.2.2. Others

5.3. Gaming Chips Market Size and Forecast, by Region (2026-2032)

5.3.1. North America

5.3.2. Europe

5.3.3. Asia Pacific

5.3.4. Middle East and Africa

5.3.5. South America

6. North American Gaming Chips Market Size and Forecast (by Value USD Billion)

6.1. North America Gaming Chips Market Size and Forecast, By Chip Type (2026-2032)

6.1.1. Slot Gaming chips

6.1.2. Video poker machines Gaming chips

6.1.3. Other

6.2. North America Gaming Chips Market Size and Forecast, By Application (2026-2032)

6.2.1. Casino

6.2.2. Others

6.3. North America Gaming Chips Market Size and Forecast, by Country (2026-2032)

6.3.1. United States

6.3.2. Canada

6.3.3. Mexico

7. Europe Gaming Chips Market Size and Forecast (by Value USD Billion)

7.1. Europe Gaming Chips Market Size and Forecast, By Chip Type (2026-2032)

7.2. Europe Gaming Chips Market Size and Forecast, By Data Center Size (2026-2032)

7.3. Europe Gaming Chips Market Size and Forecast, By Application (2026-2032)

7.4. Europe Gaming Chips Market Size and Forecast, by Country (2026-2032)

7.4.1. UK

7.4.2. France

7.4.3. Germany

7.4.4. Italy

7.4.5. Spain

7.4.6. Sweden

7.4.7. Austria

7.4.8. Rest of Europe

8. Asia Pacific Gaming Chips Market Size and Forecast (by Value USD Billion)

8.1. Asia Pacific Gaming Chips Market Size and Forecast, By Chip Type (2026-2032)

8.2. Asia Pacific Gaming Chips Market Size and Forecast, By Application (2026-2032)

8.3. Asia Pacific Gaming Chips Market Size and Forecast, by Country (2026-2032)

8.3.1. China

8.3.2. S Korea

8.3.3. Japan

8.3.4. India

8.3.5. Australia

8.3.6. Indonesia

8.3.7. Malaysia

8.3.8. Vietnam

8.3.9. Taiwan

8.3.10. Bangladesh

8.3.11. Pakistan

8.3.12. Rest of Asia Pacific

9. Middle East and Africa Gaming Chips Market Size and Forecast (by Value USD Billion)

9.1. Middle East and Africa Gaming Chips Market Size and Forecast, By Chip Type (2026-2032)

9.2. Middle East and Africa Gaming Chips Market Size and Forecast, By Application (2026-2032)

9.3. Middle East and Africa Gaming Chips Market Size and Forecast, by Country (2026-2032)

9.3.1. South Africa

9.3.2. GCC

9.3.3. Egypt

9.3.4. Nigeria

9.3.5. Rest of ME&A

10. South America Gaming Chips Market Size and Forecast (by Value USD Billion)

10.1. South America Gaming Chips Market Size and Forecast, By Chip Type (2026-2032)

10.2. South America Gaming Chips Market Size and Forecast, By Application (2026-2032)

10.3. South America Gaming Chips Market Size and Forecast, by Country (2026-2032)

10.3.1. Brazil

10.3.2. Argentina

10.3.3. Rest of South America

11. Company Profile: Key players

11.1. NVIDIA

11.1.1. Company Overview

11.1.2. Business Portfolio

11.1.3. Financial Overview

11.1.4. SWOT Analysis (Technological strengths and weaknesses)

11.1.5. Strategic Analysis (Recent strategic moves)

11.1.6. Recent Developments

11.2. AMD

11.3. Intel

11.4. Broadcom

11.5. Samsung

11.6. TSMC

11.7. Arm

11.8. Qualcomm

11.9. GlobalFoundries

11.10. Huawei

11.11. Aligned Data Centers, LLC

11.12. Dell Technologies

11.13. Extreme Networks

11.14. Graphcore

11.15. IBM

12. Key Findings

13. Industry Recommendation