Flame Retardants for Aerospace Plastics Market Global Industry Analysis and Forecast (2026-2032)

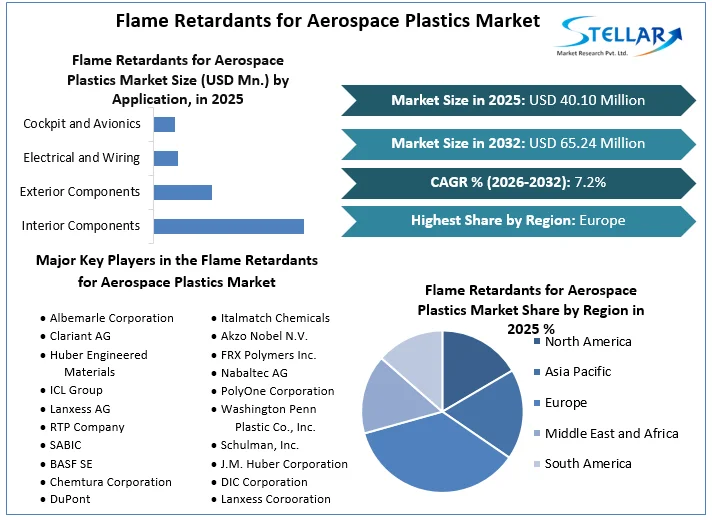

Flame Retardants for Aerospace Plastics Market Size was valued at USD 40.10 Mn in 2024 and is expected to reach USD 65.24 Mn by 2032 at a CAGR of 7.2 % over the forecast period.

Flame Retardants for Aerospace Plastics Market Overview

The market for flame retardants for aerospace plastics has shown tremendous growth globally. The demand for flame-retardant additives in plastics used for airplane components has increased due to the aerospace industry's strict safety standards. These chemicals contribute to the materials improved fire resistance, assuring the safety of the crew and passengers. Manufacturers and airlines emphasize products that adhere to strict safety standards, therefore the industry has had consistent growth. This pattern is anticipated to continue as the aerospace industry develops, highlighting the demand for dependable flame-retardant plastics.

To get more Insights: Request Free Sample Report

Flame Retardants for Aerospace Plastics Market Dynamics

Strict restrictions requiring the use of flame-retardant materials have been implemented in the aircraft industry due to the critical importance of passenger and crew safety. This has increased demand for cutting-edge flame-retardant chemicals in plastics, which is propelling market expansion. The demand for these materials is also fuelled by the ongoing growth of the commercial aviation industry and the rising fleet size of aircraft. Opportunities arise from the expanding use of lightweight polymers in aerospace components as manufacturers try to strike a balance between safety and fuel efficiency. Market growth is being aided by technological developments in flame-retardant formulations that offer high performance and environmental compliance. The global market for flame retardants for aerospace plastics is driven by the confluence of safety standards, industry growth, material innovation, and environmental concerns.

Flame Retardants for Aerospace Plastics Market Restraints

The Flame Retardants for Aerospace Plastics market has strong growth potential, but it is constrained by a number of significant factors globally. More sustainable and environmentally friendly flame retardants are in demand due to strict regulatory requirements and changing environmental standards. For conventional flame-retardant formulations that can include dangerous materials, this transition presents difficulties. A further obstacle to the aviation industry's ongoing efforts to cut weight and improve fuel efficiency is that some flame-retardant chemicals may adversely impact the characteristics of particular materials and add weight overall.

The high expenditures of research and development involved in creating new flame-retardant solutions matched to particular plastics and strict flight regulations may inhibit market expansion. Maintaining the Flame Retardants for Aerospace Plastics market will require striking a balance between these restrictions and the requirement for safety.

Flame Retardants for Aerospace Plastics Market Opportunities

The market for flame retardants in aerospace plastics offers a number of significant potential prospects. The rising demand for lightweight and fuel-efficient aircraft, which has increased the usage of innovative plastics in aerospace construction, is one of the main factors. Given that safety is still of utmost importance, this shift towards lighter materials opens up a huge market for flame retardants. Also encouraging the use of flame-retardant polymers in aircraft interiors and parts is the growing global demand for more severe fire safety regulations.

There is a chance to create environmentally friendly flame retardants that are in line with sustainable standards as environmental concerns become more prominent. Partnerships between producers of flame retardants, aerospace firms, and academic institutions might result in advances in testing and product development processes. As airlines look to improve the safety features of their current fleets, the aftermarket for modifications and refurbishments of aircraft is expanding, which further increases the demand for flame retardants. Due to a convergence of industry-driven, safety-related, and regulatory reasons, the market for flame retardants for aerospace plastics is well-positioned to take advantage of these opportunities.

Flame Retardants for Aerospace Plastics Market Challenge

The market for flame retardants for aerospace plastics confronts numerous significant obstacles. The ongoing quest for lightweight materials to increase aviation fuel efficiency and lower emissions is one significant problem. Due to their ability to increase weight and change the mechanical properties of polymers, flame retardant chemicals are presented with a difficulty in this situation. Manufacturers are being forced by strict environmental laws to create flame retardants that are more environmentally friendly without sacrificing effectiveness.

A tricky task is preserving the desired material qualities while balancing the demand for increased fire safety. Furthermore, for certain producers, particularly those in developing regions, the price of modern flame retardant technologies may be prohibitive. These issues emphasize the intricate interplay in the economy between safety, performance, regulations, and economics.

Flame Retardants for Aerospace Plastics Market Trends

Creating flame-retardant solutions that are not only efficient but also environmentally responsible is becoming more and more important. In order to meet regulatory and environmental issues, this includes researching flame retardants that are bio-based or halogen-free. The market is being impacted by developments in composite materials and additive manufacturing. The requirement for flame retardants that can smoothly work with cutting-edge production processes without affecting the materials overall performance is growing as new manufacturing methods are developed.

The demand for lightweight yet fire-resistant materials is being driven by the push for more electric aircraft and urban air mobility alternatives. Manufacturers of flame retardants are increasingly working with aerospace businesses and academic institutions. In order to ensure that flame retardants are optimized for particular aircraft applications and meet the industry's strict safety regulations, a collaborative approach to problem-solving is encouraged. Trends that emphasize sustainability, compatibility with new production techniques, alignment with developing aviation technology, and more industry collaboration are being seen in the market for flame retardants for aerospace plastics.

Regional Insights for Flame Retardants for Aerospace Plastics Market

Certainly, here are some regional insights into the Flame Retardants for Aerospace Plastics Market across different countries.

Europe: The Flame Retardants for Aerospace Plastics market in Europe is expanding significantly. European aerospace manufacturers are actively looking for cutting-edge flame-retardant technologies with a particular focus on passenger safety and environmental issues. The requirement for powerful yet lightweight flame retardants is further highlighted by the push for lightweight materials to increase fuel efficiency. The adoption of halogen-free and eco-friendly flame retardants is being prompted by the strict environmental rules in the European Union.

Asia Pacific: The Flame Retardants for Aerospace Plastics market is rising significantly in the Asia Pacific region. There is a growing need for air travel in nations like China, Japan, and India, which is fuelling the demand for safer airplane parts. Aerospace manufacturers are using cutting-edge flame-retardant systems because to strict restrictions and a heightened focus on passenger safety. The development of regional aerospace businesses and research institutions is promoting the development of new flame-retardant technologies.

North America: The Flame Retardants for Aerospace Plastics market in North America is expanding rapidly. The use of flame-retardant materials in airplane components is driven by strict safety rules as well as a desire for high-performance materials. The regions emphasis on technological development and research helps to create novel flame retardants that satisfy changing industrial demands. Effective flame retardants are also crucial given the need for more ecologically friendly and fuel-efficient aircraft. Collaboration between North American flame retardant providers and aircraft manufacturers guarantees the ongoing improvement of fire safety features in aerospace polymers.

Flame Retardants for Aerospace Plastics Market Segment Analysis

By Type of Flame Retardants: The type of flame retardants employed can be utilized to segment the global Flame Retardants for Aerospace Plastics market. Halogenated, phosphorous-based, and non-halogenated flame retardants are often included in these categories. Because of their effectiveness, halogenated flame retardants like brominated chemicals have historically been employed. The performance and environmental concerns are balanced by phosphorus-based flame retardants. The popularity of non-halogenated flame retardants, such as those based on nitrogen, is growing as a result of their less negative environmental effects. With regard to a variety of aircraft applications, this division reflects the industry's aim to maximize fire safety while accommodating concerns about regulatory compliance and sustainable material options.

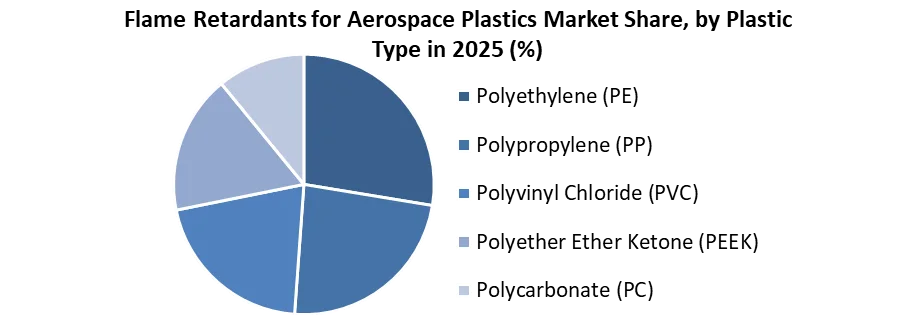

By Plastic Type: To meet the varied needs of the aerospace sector, the flame retardants for aerospace plastics market is divided globally based on plastic types. Due to their outstanding heat resistance and mechanical strength, thermoset polymers including epoxy resins, phenolic resins, and polyimides are essential for structural components. Polyetheretherketone (PEEK) and polyphenylene sulphide (PPS), two thermoplastic polymers with versatility, are used in interior applications.

In high-temperature situations, fluoropolymers like polytetrafluoroethylene (PTFE) find utility. The difficulty of establishing fire resistance while preserving performance qualities vary depending on the type of plastic used. In order to ensure compliance with safety laws and performance criteria in aircraft applications, the market now provides a variety of flame retardant solutions specifically suited for these particular plastic categories.

By Application: The market for flame retardants for aerospace plastics is divided into many important categories based on application. These include the interior parts of the vehicle, such as the seats, overhead bins, and cabin panels, where flame-retardant plastics are essential for ensuring passenger safety. Engine covers and structural elements are examples of outside applications where fire resistance is crucial to avoid catastrophic failures. Flame-retardant materials are also necessary for electrical and electronic systems in aircraft to prevent fires that could endanger crucial equipment.

The division by application highlights the numerous and important functions that flame retardants perform in securing various areas of aerospace operations, guaranteeing compliance with safety requirements, and maintaining overall aircraft integrity.

Flame Retardants for Aerospace Plastics Market: Competitive Landscape

Flame Retardants for Aerospace Plastics market competition is characterized by a mix of well-established competitors and creative newcomers. Leading chemical firms with broad product portfolios, technical know-how, and robust global presences like BASF SE, Clariant AG, and Dow Inc. which dominates the market. These industry frequently concentrate on research and development to produce cutting-edge flame retardant products that satisfy the exacting standards of the aerospace industry. Smaller businesses and startups have also shown success in recent years by providing specialty flame retardant chemicals catered to particular aerospace uses. They can quickly adopt new trends and technologies in the aviation sector because to their agility.

Collaborations between these newcomers and the aerospace industry are becoming more widespread. In order to assure compliance with changing safety regulations, the industry is also seeing cooperation between regulatory agencies and makers of flame retardants. This partnership helps in the creation of solutions that not only adhere to current rules but also foresee requirements in the future. The market for flame retardants for aircraft plastics is competitive overall, with a mix of well-established competitors, quick-moving startups, and joint ventures all seeking to improve the performance and safety of plastics used in aerospace applications.

|

Flame Retardants for Aerospace Plastics Market Scope |

|

|

Market Size in 2025 |

USD 40.10 Bn. |

|

Market Size in 2032 |

USD 65.24 Bn. |

|

CAGR (2026-2032) |

7.2% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segment Scope |

By Application

|

|

By Plastic Type

|

|

|

By Type of Flame Retardants

|

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Flame Retardants for Aerospace Plastics Market Key players

- Albemarle Corporation

- Clariant AG

- Huber Engineered Materials

- ICL Group

- Lanxess AG

- RTP Company

- SABIC

- BASF SE

- Chemtura Corporation

- DuPont

- Italmatch Chemicals

- Akzo Nobel N.V.

- FRX Polymers Inc.

- Nabaltec AG

- PolyOne Corporation

- Washington Penn Plastic Co., Inc.

- Schulman, Inc.

- J.M. Huber Corporation

- DIC Corporation

- Lanxess Corporation

Frequently Asked Questions

Europe region is expected to dominate the Flame Retardants for Aerospace Plastics Market over the forecast period.

The market size of the Flame Retardants for Aerospace Plastics Market is expected to reach USD 65.24 Bn by 2032.

The major key players in the Global Flame Retardants for Aerospace Plastics Market are Albemarle Corporation, Clariant AG, Huber Engineered Materials, ICL Group, Lanxess AG, RTP Company, SABIC, BASF SE.

Increased demand for commercial aircraft and increased fire safety standards and regulations are the factors expected to drive the flame retardants for aerospace plastics market growth over the forecast period (2026-2032).

1. Flame Retardants for Aerospace Plastics Market: Research Methodology

2. Flame Retardants for Aerospace Plastics Market: Executive Summary

3. Flame Retardants for Aerospace Plastics Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Competitive Landscape

3.3. Key Players Benchmarking

3.4. Market Structure

3.4.1. Market Leaders

3.4.2. Market Followers

3.4.3. Emerging Players

3.5. Consolidation of the Market

4. Flame Retardants for Aerospace Plastics Market: Dynamics

4.1. Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Market Drivers by Region

4.2.1. North America

4.2.2. Europe

4.2.3. Asia Pacific

4.2.4. Middle East and Africa

4.2.5. South America

4.3. Market Restraints

4.4. Market Opportunities

4.5. Market Challenges

4.6. PORTER’s Five Forces Analysis

4.7. PESTLE Analysis

4.8. Value Chain Analysis

4.9. Regulatory Landscape by Region

4.9.1. North America

4.9.2. Europe

4.9.3. Asia Pacific

4.9.4. Middle East and Africa

4.9.5. South America

5. Flame Retardants for Aerospace Plastics Market Size and Forecast by Segments (by Value USD and Volume Units)

5.1. Flame Retardants for Aerospace Plastics Market Size and Forecast, by Application (2025-2032)

5.1.1. Interior Components

5.1.2. Exterior Components

5.1.3. Electrical and Wiring

5.1.4. Cockpit and Avionics

5.1.5. Others

5.2. Flame Retardants for Aerospace Plastics Market Size and Forecast, by Plastic Type (2025-2032)

5.2.1. Polyethylene (PE)

5.2.2. Polypropylene (PP)

5.2.3. Polyvinyl Chloride (PVC)

5.2.4. Polyether Ether Ketone (PEEK)

5.2.5. Polycarbonate (PC)

5.2.6. Others

5.3. Flame Retardants for Aerospace Plastics Market Size and Forecast, by Type of Flame Retardants (2025-2032)

5.3.1. Halogenated Flame Retardants

5.3.2. Phosphorus-Based Flame Retardants

5.3.3. Aluminum Hydroxide (ATH)

5.3.4. Magnesium Hydroxide (MDH)

5.3.5. Intumescent Flame Retardants

5.3.6. Others

5.4. Flame Retardants for Aerospace Plastics Market Size and Forecast, by Region (2025-2032)

5.4.1. North America

5.4.2. Europe

5.4.3. Asia Pacific

5.4.4. Middle East and Africa

5.4.5. South America

6. North America Flame Retardants for Aerospace Plastics Market Size and Forecast (by Value USD and Volume Units)

6.1. North America Flame Retardants for Aerospace Plastics Market Size and Forecast, by Application (2025-2032)

6.1.1. Interior Components

6.1.2. Exterior Components

6.1.3. Electrical and Wiring

6.1.4. Cockpit and Avionics

6.1.5. Others

6.2. North America Flame Retardants for Aerospace Plastics Market Size and Forecast, by Plastic Type (2025-2032)

6.2.1. Polyethylene (PE)

6.2.2. Polypropylene (PP)

6.2.3. Polyvinyl Chloride (PVC)

6.2.4. Polyether Ether Ketone (PEEK)

6.2.5. Polycarbonate (PC)

6.2.6. Others

6.3. North America Flame Retardants for Aerospace Plastics Market Size and Forecast, by Type of Flame Retardants (2025-2032)

6.3.1. Halogenated Flame Retardants

6.3.2. Phosphorus-Based Flame Retardants

6.3.3. Aluminum Hydroxide (ATH)

6.3.4. Magnesium Hydroxide (MDH)

6.3.5. Intumescent Flame Retardants

6.3.6. Others

6.4. North America Flame Retardants for Aerospace Plastics Market Size and Forecast, by Country (2025-2032)

6.4.1. United States

6.4.2. Canada

6.4.3. Mexico

7. Europe Flame Retardants for Aerospace Plastics Market Size and Forecast (by Value USD and Volume Units)

7.1. Europe Flame Retardants for Aerospace Plastics Market Size and Forecast, by Application (2025-2032)

7.1.1. Interior Components

7.1.2. Exterior Components

7.1.3. Electrical and Wiring

7.1.4. Cockpit and Avionics

7.1.5. Others

7.2. Europe Flame Retardants for Aerospace Plastics Market Size and Forecast, by Plastic Type (2025-2032)

7.2.1. Polyethylene (PE)

7.2.2. Polypropylene (PP)

7.2.3. Polyvinyl Chloride (PVC)

7.2.4. Polyether Ether Ketone (PEEK)

7.2.5. Polycarbonate (PC)

7.2.6. Others

7.3. Europe Flame Retardants for Aerospace Plastics Market Size and Forecast, by Type of Flame Retardants (2025-2032)

7.3.1. Halogenated Flame Retardants

7.3.2. Phosphorus-Based Flame Retardants

7.3.3. Aluminum Hydroxide (ATH)

7.3.4. Magnesium Hydroxide (MDH)

7.3.5. Intumescent Flame Retardants

7.3.6. Others

7.4. Europe Flame Retardants for Aerospace Plastics Market Size and Forecast, by Country (2025-2032)

7.4.1. UK

7.4.2. France

7.4.3. Germany

7.4.4. Italy

7.4.5. Spain

7.4.6. Sweden

7.4.7. Austria

7.4.8. Rest of Europe

8. Asia Pacific Flame Retardants for Aerospace Plastics Market Size and Forecast (by Value USD and Volume Units)

8.1. Asia Pacific Flame Retardants for Aerospace Plastics Market Size and Forecast, by Application (2025-2032)

8.1.1. Interior Components

8.1.2. Exterior Components

8.1.3. Electrical and Wiring

8.1.4. Cockpit and Avionics

8.1.5. Others

8.2. Asia Pacific Flame Retardants for Aerospace Plastics Market Size and Forecast, by Plastic Type (2025-2032)

8.2.1. Polyethylene (PE)

8.2.2. Polypropylene (PP)

8.2.3. Polyvinyl Chloride (PVC)

8.2.4. Polyether Ether Ketone (PEEK)

8.2.5. Polycarbonate (PC)

8.2.6. Others

8.3. Asia Pacific Flame Retardants for Aerospace Plastics Market Size and Forecast, by Type of Flame Retardants (2025-2032)

8.3.1. Halogenated Flame Retardants

8.3.2. Phosphorus-Based Flame Retardants

8.3.3. Aluminum Hydroxide (ATH)

8.3.4. Magnesium Hydroxide (MDH)

8.3.5. Intumescent Flame Retardants

8.3.6. Others

8.4. Asia Pacific Flame Retardants for Aerospace Plastics Market Size and Forecast, by Country (2025-2032)

8.4.1. China

8.4.2. S Korea

8.4.3. Japan

8.4.4. India

8.4.5. Australia

8.4.6. Indonesia

8.4.7. Malaysia

8.4.8. Vietnam

8.4.9. Taiwan

8.4.10. Bangladesh

8.4.11. Pakistan

8.4.12. Rest of Asia Pacific

9. Middle East and Africa Flame Retardants for Aerospace Plastics Market Size and Forecast (by Value USD and Volume Units)

9.1. Middle East and Africa Flame Retardants for Aerospace Plastics Market Size and Forecast, by Application (2025-2032)

9.1.1. Interior Components

9.1.2. Exterior Components

9.1.3. Electrical and Wiring

9.1.4. Cockpit and Avionics

9.1.5. Others

9.2. Middle East and Africa Flame Retardants for Aerospace Plastics Market Size and Forecast, by Plastic Type (2025-2032)

9.2.1. Polyethylene (PE)

9.2.2. Polypropylene (PP)

9.2.3. Polyvinyl Chloride (PVC)

9.2.4. Polyether Ether Ketone (PEEK)

9.2.5. Polycarbonate (PC)

9.2.6. Others

9.3. Middle East and Africa Flame Retardants for Aerospace Plastics Market Size and Forecast, by Type of Flame Retardants (2025-2032)

9.3.1. Halogenated Flame Retardants

9.3.2. Phosphorus-Based Flame Retardants

9.3.3. Aluminum Hydroxide (ATH)

9.3.4. Magnesium Hydroxide (MDH)

9.3.5. Intumescent Flame Retardants

9.3.6. Others

9.4. Middle East and Africa Flame Retardants for Aerospace Plastics Market Size and Forecast, by Country (2025-2032)

9.4.1. South Africa

9.4.2. GCC

9.4.3. Egypt

9.4.4. Nigeria

9.4.5. Rest of ME&A

10. South America Flame Retardants for Aerospace Plastics Market Size and Forecast (by Value USD and Volume Units)

10.1. South America Flame Retardants for Aerospace Plastics Market Size and Forecast, by Application (2025-2032)

10.1.1. Interior Components

10.1.2. Exterior Components

10.1.3. Electrical and Wiring

10.1.4. Cockpit and Avionics

10.1.5. Others

10.2. South America Flame Retardants for Aerospace Plastics Market Size and Forecast, by Plastic Type (2025-2032)

10.2.1. Polyethylene (PE)

10.2.2. Polypropylene (PP)

10.2.3. Polyvinyl Chloride (PVC)

10.2.4. Polyether Ether Ketone (PEEK)

10.2.5. Polycarbonate (PC)

10.2.6. Others

10.3. South America Flame Retardants for Aerospace Plastics Market Size and Forecast, by Type of Flame Retardants (2025-2032)

10.3.1. Halogenated Flame Retardants

10.3.2. Phosphorus-Based Flame Retardants

10.3.3. Aluminum Hydroxide (ATH)

10.3.4. Magnesium Hydroxide (MDH)

10.3.5. Intumescent Flame Retardants

10.3.6. Others

10.4. South America Flame Retardants for Aerospace Plastics Market Size and Forecast, by Country (2025-2032)

10.4.1. Brazil

10.4.2. Argentina

10.4.3. Rest of South America

11. Company Profile: Key players

11.1. Albemarle Corporation

11.1.1. Company Overview

11.1.2. Financial Overview

11.1.3. Business Portfolio

11.1.4. SWOT Analysis

11.1.5. Business Strategy

11.1.6. Recent Developments

11.2. Clariant AG

11.3. Huber Engineered Materials

11.4. ICL Group

11.5. Lanxess AG

11.6. RTP Company

11.7. SABIC

11.8. BASF SE

11.9. Chemtura Corporation

11.10. DuPont

11.11. Italmatch Chemicals

11.12. Akzo Nobel N.V.

11.13. FRX Polymers Inc.

11.14. Nabaltec AG

11.15. PolyOne Corporation

11.16. Washington Penn Plastic Co., Inc.

11.17. A. Schulman, Inc.

11.18. J.M. Huber Corporation

11.19. DIC Corporation

11.20. Lanxess Corporation

12. Key Findings

13. Industry Recommendation