Fire Department Software Market - Global Industry Analysis and Forecast (2026-2032) Trends, Statistics, Dynamics, Segment Analysis

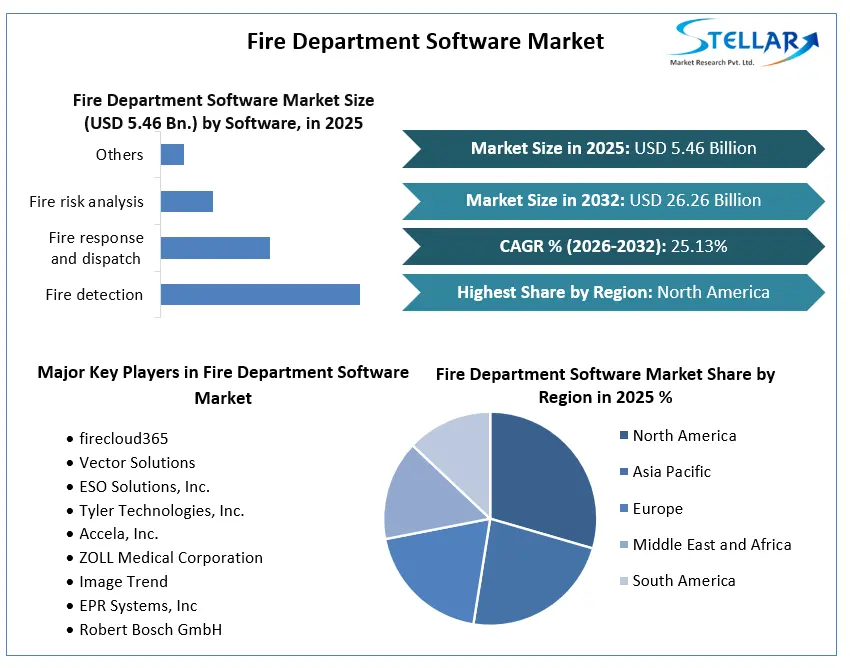

The Global Fire Department Software Market size reached USD 5.46 Billion in 2025 and expects the market to reach USD 26.26 billion by 2032, exhibiting a CAGR of 25.13% during 2026-2032.

Fire Department Software Market Overview:

The market for software designed specifically for fire departments and emergency services is known as the "fire department software market." These software programs are intended to improve response times, increase firefighter safety, and efficiently allocate resources while streamlining many areas of fire department operations.

Agility, affordability, and practicality are the three factors driving the use of fire department software. The need for fire department software solutions is growing as a result of dynamic reporting requirements brought on by shifting legislation and operational standards. For instance, the records that fire departments must maintain are outlined in NFPA Standard 1221. The importance of pre-incident preparations that provide firemen with crucial information before they leave is stressed by another standard, NFPA 1620.

Regardless of their size or budget, fire departments must oversee and manage their personnel, incident reporting, maintenance, training, and equipment. The increasing need for modernization and the use of software solutions to better manage a fire department's needs, as well as the rising investment by market players in research and innovation to offer new solutions and software, are some of the major factors influencing the market's growth. As a result of the increased need for software solutions throughout the government sector, particularly in the relatively small but rapidly growing fire department software market, a number of new market players have emerged, including ESO, stationSMARTS, GovPilot, and SmartServ.

To get more Insights: Request Free Sample Report

Fire Department Software Market Dynamics:

Increasing Demand for Efficiency, Data Management and Analysis, etc.

Fire departments are under pressure to react to situations promptly and effectively. Managing resources, enhancing response times, and streamlining processes are key to saving people's lives and property.

The amount of information from numerous sources, such as incident reports, records of equipment maintenance, and training logs, is accumulating. Software for fire departments can assist in managing and analyzing this data in order to improve overall operations, distribute resources wisely, and make educated decisions.

In order to effectively battle fires and respond to emergencies, it is crucial to allocate resources, such as personnel and equipment, as best as possible. The program assists in monitoring resource availability and allocating them where they are most required.

Firefighting apparatus and infrastructure are being upgraded with sensors and Internet of Things (IoT) technology. These devices can communicate with fire department software to deliver real-time information on environmental factors and equipment status. Route planning, incident site mapping, and resource allocation all rely on geographic information systems (GIS) and mapping software. For better decision-making, these tools are incorporated into fire department software.

Fire Department Software Market Restraints:

Budget Constraints, Integration Complexity, Data Security Concerns, etc.

Investing in pricey software solutions for fire departments can be difficult because they sometimes have small budgets. The adoption of cutting-edge software for fire departments with extensive features and capabilities can be hampered by limited funding.

It might take a lot of effort and time to integrate new software into existing workflows and systems. Legacy system compatibility problems can be problematic, especially for smaller fire departments with constrained IT resources. It is crucial to protect the security of fire departments' data because it is private and sensitive. Cloud-based software solutions adoption may be slowed down by worries about data breaches or illegal access. It might be difficult and expensive to switch to another software solution in the future if you choose the wrong software vendor since vendor lock-in results from making the wrong choice.

Fire Department Software Market Opportunities:

Incident Management Software, Mobile Apps for Firefighters, etc.

Software that can assist fire departments in effectively managing events from the time they are reported until they are resolved is in greater demand. Real-time event tracking, resource allocation, and dispatching are a few examples of these systems.

There is a high need for mobile applications that give on-the-go firefighters immediate access to vital data. These apps may provide information about the incident, maps, safety guidelines, and communication options. Fire departments are always seeking methods to enhance employee training. A useful tool for firefighters is simulation software, which enables them to rehearse different scenarios in a secure setting.

Strong cybersecurity solutions are becoming more and more necessary as fire departments rely more and more on digital systems and data to safeguard sensitive data and vital infrastructure.

Fire Department Software Market Challenges:

Interoperability, Data Security and Privacy, etc.

In order to manage incidents, deploy personnel, and maintain records, fire departments frequently use a variety of software programs. It is quite difficult to make sure that these systems can communicate and share data in real time. Interoperability problems might result in inefficiencies and sluggish emergency response times.

Fire departments deal with private information, such as the personal and medical information of those involved in crises. Consistent compliance with data protection laws (such as GDPR and HIPAA) might be difficult, but it is essential to guarantee the security and privacy of this data.

To effectively handle emergencies, fire departments must allocate their resources. Achieving the ideal balance between demand and available resources can be difficult, but software that aids in resource management and optimization is essential.

Fire Department Software Market Regional Insights:

The largest fire department software market in the world is located in North America. The region's dominance is partly attributable to the widespread use of fire department software in the United States and Canada. Additionally, two of the top manufacturers of fire department software, Northrop Grumman Corporation and Motorola Solutions, Inc., have their headquarters nearby.

The second-largest fire department software market in the world is located in Europe. The main factor fostering the region's expansion is the rising use of fire department software in Germany, the United Kingdom, and France. Some of the major software developers for fire departments, like Hexagon AB and Airbus SE, have their headquarters in this area.

The world's fire department software industry is expanding at the quickest rate in this area. The main driver of the region's expansion is the rising use of fire department software in China, India, and Japan. Some of the top manufacturers of fire department software, like Honeywell International Inc., are based in the area.

Fire Department Software Market Segment Analysis:

By Software Type: The software type segment is divided into Fire detection, Fire response and dispatch, Fire risk analysis, and others. The sector for fire detection is expected to develop at the fastest rate over the anticipated time frame due to the growing demand for cutting-edge fire detection systems and solutions.

By Deployment Type: The deployment type segment is divided into Cloud-based and On-premise. It is anticipated that the cloud-based segment will expand more quickly than the on-premise segment due to benefits like scalability, flexibility, and affordability that cloud computing offers.

By Enterprise Size: The Enterprise Size segment is divided into Small and medium enterprises (SMEs) and Large enterprises. The large enterprise sector will be expected to retain the largest market share throughout the anticipated time frame as a result of the growing use of fire department software by large fire departments.

By End-User: The End-User segment is divided into Fire departments and emergency responders, Building owners and property managers, Insurance companies, and Regulatory bodies. The segment representing fire departments and emergency responders will be expected to retain the largest market share throughout the estimated time frame due to the increased requirement for fire department software to improve operational effectiveness and efficiency.

Fire Department Software Market Competitive Landscape:

FireCloud365 now integrates with a number of other public safety software solutions, including CAD systems, RMS systems, and GIS systems. This allows fire departments to share data between their different systems and to streamline their operations.

FireCloud365 is developing new data analytics tools to help fire departments identify trends and patterns in their data. This information can be used to improve decision-making and to allocate resources more effectively.

FirePrograms Software's recent developments include:

A mobile program that gives firefighters access to tools and data for fire defense from their tablets and smartphones. Preplans, incident reporting, and asset tracking are elements of FirePrograms Mobile.

An analytics platform in the cloud that offers fire departments access to their data. FirePrograms Analytics can be used to monitor trends, pinpoint areas for development, and enhance resource allocation choices.

A framework that enables fire departments to connect FirePrograms Software to additional platforms, such as CAD/RMS and GIS. This enhances data sharing and allows fire departments to automate activities.

|

Fire Department Software Market Scope |

|

|

Market Size in 2025 |

USD 5.46 billion. |

|

Market Size in 2032 |

USD 26.26 billion. |

|

CAGR (2026-2032) |

25.13% |

|

Historic Data |

2020-2032 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segment Scope |

By Software Type:

|

|

By Deployment Type:

|

|

|

By Enterprise Size:

|

|

|

By End-User:

|

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Fire Department Software Market Key Players:

- firecloud365

- Vector Solutions

- ESO Solutions, Inc.

- Tyler Technologies, Inc.

- Accela, Inc.

- ZOLL Medical Corporation

- ImageTrend

- EPR Systems, Inc

- Robert Bosch GmbH

- Eaton

- Gentex Corp.

- United Technologies Corp

- Space Age Electronics

- Halma plc

- Hitachi Ltd.

- Siemens Building Technologies

- Hochiki Corp.

- Nittan Company, Ltd.

- Honeywell International, Inc.

- Napco Security Technologies, Inc.

- Johnson Controls

- FirePrograms Software

- StationSmarts

- CivicPlus

- Adashi Systems, LLC

Frequently Asked Questions

The Fire Department Software Market size is expected to reach USD 26.26 billion by 2032.

The major players in the Fire Department Software Market include firecloud365 Vector Solutions ESO Solutions, Inc. Tyler Technologies, Inc Accela, Inc. ZOLL Medical Corporation ImageTrend EPR Systems, Inc Robert Bosch GmbH Eaton Gentex Corp. United Technologies Corp Space Age Electronics Halma plc Hitachi Ltd. Siemens Building Technologies Hochiki Corp. Nittan Company, Ltd. Honeywell International, Inc. Napco Security Technologies, Inc. Johnson Controls FirePrograms Software StationSmarts CivicPlus Adashi Systems, LLC

The expected CAGR of the Fire Department Software Market is 25.13% from 2026 to 2032.

The North American market dominated the Fire Department Software Market by Region in 2025.

1. Global Fire Department Software Market: Research Methodology

2. Global Fire Department Software Market: Executive Summary

3. Global Fire Department Software Market: Competitive Landscape

3.1. Stellar Competition Matrix

3.2. Competitive Landscape

3.3. Key Players Benchmarking

3.4. Market Structure

3.4.1. Market Leaders

3.4.2. Market Followers

3.4.3. Emerging Players

3.5. Consolidation of the Market

4. Global Fire Department Software Market: Dynamics

4.1. Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Market Drivers by Region

4.2.1. North America

4.2.2. Europe

4.2.3. Asia Pacific

4.2.4. Middle East and Africa

4.2.5. South America

4.3. Market Restraints

4.4. Market Opportunities

4.5. Market Challenges

4.6. PORTER’s Five Forces Analysis

4.7. PESTLE Analysis

4.8. Value Chain Analysis

4.9. Regulatory Landscape by Region

4.9.1. North America

4.9.2. Europe

4.9.3. Asia Pacific

4.9.4. Middle East and Africa

4.9.5. South America

5. Global Fire Department Software Market Size and Forecast by Segments (by Value USD and Volume Units)

5.1. Global Fire Department Software Market Size and Forecast, by Software Type (2026-2032)

5.1.1. Fire detection

5.1.2. Fire response and dispatch

5.1.3. Fire risk analysis

5.1.4. Others

5.2. Global Fire Department Software Market Size and Forecast, by Deployment Type (2026-2032)

5.2.1. Cloud-based

5.2.2. On-premise

5.3. Global Fire Department Software Market Size and Forecast, by Enterprise Size (2026-2032)

5.3.1. Small and medium enterprises (SMEs)

5.3.2. Large enterprises

5.4. Global Fire Department Software Market Size and Forecast, by End-User (2026-2032)

5.4.1. Fire departments and emergency responders

5.4.2. Building owners and property managers

5.4.3. Insurance companies

5.4.4. Regulatory bodies

5.5. Global Fire Department Software Market Size and Forecast, by Region (2026-2032)

5.5.1. North America

5.5.2. Europe

5.5.3. Asia Pacific

5.5.4. Middle East and Africa

5.5.5. South America

6. North America Global Fire Department Software Market Size and Forecast (by Value USD and Volume Units)

6.1. North America Global Fire Department Software Market Size and Forecast, by Software Type (2026-2032)

6.1.1. Fire detection

6.1.2. Fire response and dispatch

6.1.3. Fire risk analysis

6.1.4. Others

6.2. North America Global Fire Department Software Market Size and Forecast, by Deployment Type (2026-2032)

6.2.1. Cloud-based

6.2.2. On-premise

6.3. North America Global Fire Department Software Market Size and Forecast, by Enterprise Size (2026-2032)

6.3.1. Small and medium enterprises (SMEs)

6.3.2. Large enterprises

6.4. North America Global Fire Department Software Market Size and Forecast, by End-User (2026-2032)

6.4.1. Fire departments and emergency responders

6.4.2. Building owners and property managers

6.4.3. Insurance companies

6.4.4. Regulatory bodies

6.5. North America Global Fire Department Software Market Size and Forecast, by Country (2026-2032)

6.5.1. United States

6.5.2. Canada

6.5.3. Mexico

7. Europe Global Fire Department Software Market Size and Forecast (by Value USD and Volume Units)

7.1. Europe Global Fire Department Software Market Size and Forecast, by Software Type (2026-2032)

7.1.1. Fire detection

7.1.2. Fire response and dispatch

7.1.3. Fire risk analysis

7.1.4. Others

7.2. Europe Global Fire Department Software Market Size and Forecast, by Deployment Type (2026-2032)

7.2.1. Cloud-based

7.2.2. On-premise

7.3. Europe Global Fire Department Software Market Size and Forecast, by Enterprise Size (2026-2032)

7.3.1. Small and medium enterprises (SMEs)

7.3.2. Large enterprises

7.4. Europe Global Fire Department Software Market Size and Forecast, by End-User (2026-2032)

7.4.1. Fire departments and emergency responders

7.4.2. Building owners and property managers

7.4.3. Insurance companies

7.4.4. Regulatory bodies

7.5. Europe Global Fire Department Software Market Size and Forecast, by Country (2026-2032)

7.5.1. UK

7.5.2. France

7.5.3. Germany

7.5.4. Italy

7.5.5. Spain

7.5.6. Sweden

7.5.7. Austria

7.5.8. Rest of Europe

8. Asia Pacific Global Fire Department Software Market Size and Forecast (by Value USD and Volume Units)

8.1. Asia Pacific Global Fire Department Software Market Size and Forecast, by Software Type (2026-2032)

8.1.1. Fire detection

8.1.2. Fire response and dispatch

8.1.3. Fire risk analysis

8.1.4. Others

8.2. Asia Pacific Global Fire Department Software Market Size and Forecast, by Deployment Type (2026-2032)

8.2.1. Cloud-based

8.2.2. On-premise

8.3. Asia Pacific Global Fire Department Software Market Size and Forecast, by Enterprise Size (2026-2032)

8.3.1. Small and medium enterprises (SMEs)

8.3.2. Large enterprises

8.4. Asia Pacific Global Fire Department Software Market Size and Forecast, by End-User (2026-2032)

8.4.1. Fire departments and emergency responders

8.4.2. Building owners and property managers

8.4.3. Insurance companies

8.4.4. Regulatory bodies

8.5. Asia Pacific Global Fire Department Software Market Size and Forecast, by Country (2026-2032)

8.5.1. China

8.5.2. S Korea

8.5.3. Japan

8.5.4. India

8.5.5. Australia

8.5.6. Indonesia

8.5.7. Malaysia

8.5.8. Vietnam

8.5.9. Taiwan

8.5.10. Bangladesh

8.5.11. Pakistan

8.5.12. Rest of Asia Pacific

9. Middle East and Africa Global Fire Department Software Market Size and Forecast (by Value USD and Volume Units)

9.1. Middle East and Africa Global Fire Department Software Market Size and Forecast, by Software Type (2026-2032)

9.1.1. Fire detection

9.1.2. Fire response and dispatch

9.1.3. Fire risk analysis

9.1.4. Others

9.2. Middle East and Africa Global Fire Department Software Market Size and Forecast, by Deployment Type (2026-2032)

9.2.1. Cloud-based

9.2.2. On-premise

9.3. Middle East and Africa Global Fire Department Software Market Size and Forecast, by Enterprise Size (2026-2032)

9.3.1. Small and medium enterprises (SMEs)

9.3.2. Large enterprises

9.4. Middle East and Africa Global Fire Department Software Market Size and Forecast, by End-User (2026-2032)

9.4.1. Fire departments and emergency responders

9.4.2. Building owners and property managers

9.4.3. Insurance companies

9.4.4. Regulatory bodies

9.5. Middle East and Africa Global Fire Department Software Market Size and Forecast, by Country (2026-2032)

9.5.1. South Africa

9.5.2. GCC

9.5.3. Egypt

9.5.4. Nigeria

9.5.5. Rest of ME&A

10. South America Global Fire Department Software Market Size and Forecast (by Value USD and Volume Units)

10.1. South America Global Fire Department Software Market Size and Forecast, by Software Type (2026-2032)

10.1.1. Fire detection

10.1.2. Fire response and dispatch

10.1.3. Fire risk analysis

10.1.4. Others

10.2. South America Global Fire Department Software Market Size and Forecast, by Deployment Type (2026-2032)

10.2.1. Cloud-based

10.2.2. On-premise

10.3. South America Global Fire Department Software Market Size and Forecast, by Enterprise Size (2026-2032)

10.3.1. Small and medium enterprises (SMEs)

10.3.2. Large enterprises

10.4. South America Global Fire Department Software Market Size and Forecast, by End-User (2026-2032)

10.4.1. Fire departments and emergency responders

10.4.2. Building owners and property managers

10.4.3. Insurance companies

10.4.4. Regulatory bodies

10.5. South America Global Fire Department Software Market Size and Forecast, by Country (2026-2032)

10.5.1. Brazil

10.5.2. Argentina

10.5.3. Rest of South America

11. Company Profile: Key players

11.1.1. firecloud365

11.1.2. Company Overview

11.1.3. Financial Overview

11.1.4. Business Portfolio

11.1.5. SWOT Analysis

11.1.6. Business Strategy

11.1.7. Recent Developments

11.2. Vector Solutions

11.3. ESO Solutions, Inc.

11.4. Tyler Technologies, Inc.

11.5. Accela, Inc.

11.6. ZOLL Medical Corporation

11.7. ImageTrend

11.8. EPR Systems, Inc

11.9. Robert Bosch GmbH

11.10. Eaton

11.11. Gentex Corp.

11.12. United Technologies Corp

11.13. Space Age Electronics

11.14. Halma plc

11.15. Hitachi Ltd.

11.16. Siemens Building Technologies

11.17. Hochiki Corp.

11.18. Nittan Company, Ltd.

11.19. Honeywell International, Inc.

11.20. Napco Security Technologies, Inc.

11.21. Johnson Controls

11.22. FirePrograms Software

11.23. StationSmarts

11.24. CivicPlus

11.25. Adashi Systems, LLC

12. Key Findings

13. Industry Recommendation