Global Fast-Food Market: Global Size, Consumption, Supply Chain, Trends, and Forecast Analysis (2026-2032)

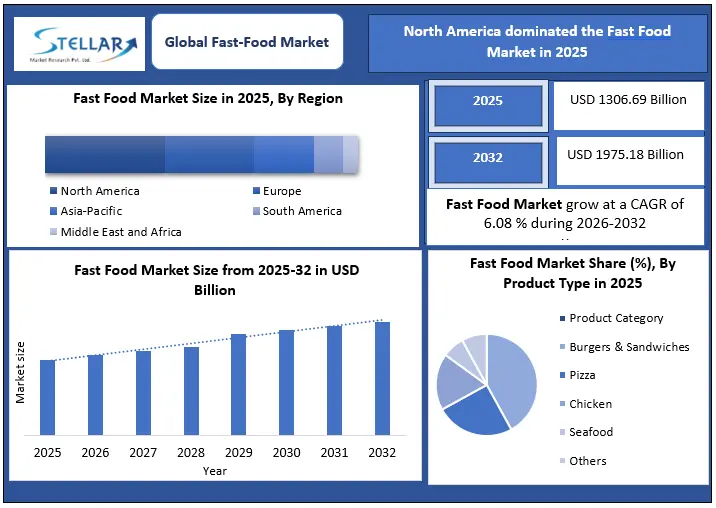

The Global Fast-Food Market is projected to grow from USD 1,306.69 billion in 2025 to USD 1,975.18 billion by 2032, registering a CAGR of 6.08% during the forecast period. Growth is supported by rising urban populations, time constrained lifestyles, and sustained demand for convenient food options across developed and emerging economies.

Global Fast-Food Market Overview:

The global fast-food market is expanding rapidly, driven by urban lifestyles, digital ordering, and evolving consumer preferences. The Global Fast-Food Market is projected to grow from USD 1,306.69 billion in 2025 to USD 1,975.18 billion by 2032, registering a CAGR of 6.08% during the forecast period. Fast food consumption remains deeply embedded in daily routines. Around 64.7% of Americans eat fast food at least once a week, with average consumption ranging from one to three visits per week. Annual spending per American is close to USD 1,200, highlighting the category’s resilience even during inflationary periods.

The market continues to evolve beyond traditional dine in formats. Off premise channels now account for nearly 75.2% of restaurant traffic. Takeout and delivery volumes have increased by 290% over the last decade; outpacing dine in recovery. Digital ordering, drive thru usage, and mobile apps have become structural rather than cyclical demand drivers.

To get more Insights: Request Free Sample Report

Fast-Food Market Dynamics:

Urbanization remains a primary demand driver. With 56% of the global population living in urban areas, fast food consumption is nearly 40.4% higher in cities than in rural regions. Reduced meal preparation time also supports demand, with Americans now spending just 37 minutes per day on cooking, a 26% decline since 2000.

Rising workforce participation and expanding middle class populations in Asia Pacific, South America, and parts of Africa are strengthening consumption momentum. Asia Pacific benefits from rapid expansion in China and India, supported by Western food adoption and localized menu formats.

Inflation and labor shortages remain key restraints. Food inflation during 2022 and 2023 pressured margins across Europe and North America. Labor availability continues to lag pre pandemic levels, with 780,340 unfilled leisure and hospitality roles reported in 2023. Ingredient, wage, and delivery costs have raised price sensitivity among consumers.

Health concerns also act as a structural constraint. Regular fast-food consumption is associated with increased risks of obesity, diabetes, and metabolic disorders. These concerns are prompting regulatory scrutiny and encouraging menu reformulation across major chains.

Global Fast-Food Market Trends

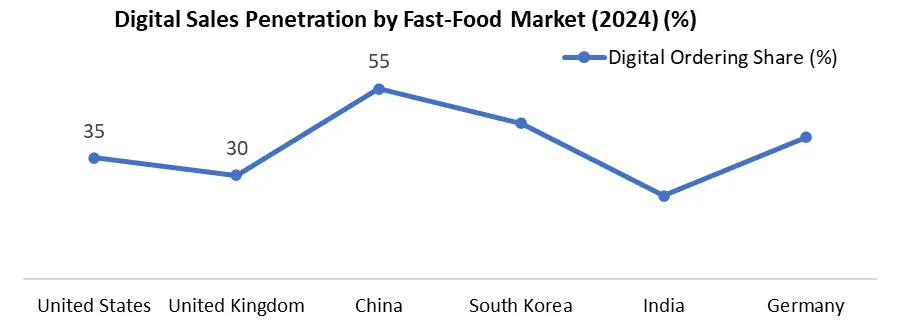

Digital transformation is reshaping operating models. About 67.6% of QSR operators are adopting labor focused technologies, while AI driven systems reduce costs by up to 50% and speed ordering by 34.7%. Digital sales now represent 34% of revenue mix at leading brands such as Chipotle.

Consumer expectations are shifting toward customization and value. 80% of consumers actively use promotional deals, while combo meals remain critical to sustaining traffic. Menu rationalization is also visible, with several U.S. QSRs reducing SKUs by 20 to 30% to improve efficiency.

Sustainability is gaining commercial relevance. Around 67% of fast food chains now use eco friendly packaging, and 38% of consumers indicate a higher likelihood of visiting brands with sustainable practices. Regulatory action has accelerated this shift, including the 2025 ban on PFAS in grease resistant packaging.

Global Fast-Food Market Regional Insights

- North America held the largest market in 2025, supported by over 212,900 fast food restaurants in the U.S. alone. California leads with more than 82,850 outlets. Fast food accounts for 35% of food away from home spending in the region.

- Europe shows mature consumption patterns, with the average consumer visiting QSRs 18 times per year. Growth is increasingly driven by plant based menus, digital loyalty programs, and contactless ordering, despite cost of living pressures.

- Asia Pacific is the fastest growing region, supported by urban expansion and rising incomes. China and India remain focal points for store expansion and localization strategies. South America benefits from a growing middle class, particularly in Mexico and Brazil.

- The Middle East shows strong outlet density, with Dubai hosting over 5,000 fast food outlets. Africa remains import dependent, with food imports reaching USD 51 billion annually, though Nigeria records around 10% annual sector growth.

Global Fast-Food Market Segment Analysis

Burgers and sandwiches dominate the product mix, accounting for 40 to 42% of U.S. fast food revenue in 2025. Americans consume roughly 20 billion burgers annually, averaging 60 burgers per person. Pizza remains the most ordered fast food item, with Domino’s leading the segment.

Quick service restaurants account for 50% of market share and over 80% of transaction volume. Fast casual formats are growing faster, recording a 3.1% increase in foot traffic versus 0.5% for QSRs in early 2024. Fast casual spending is projected to reach USD 81 billion in 2025. Delivery and takeaway services dominate consumption behavior. Seventy% of consumers order delivery or takeout, while drive thru usage remains high, with 38% of U.S. adults using it daily.

Global Fast-Food Market Competitive Landscape

The market remains highly competitive, led by global brands with scale driven advantages. McDonald’s generated over USD 130 billion in sales in 2024 with the company targeting 50,000 global units by 2027 with a run rate of over 900 gross restaurant openings across the US. Chipotle reported 7.5% same store sales growth in 2024, supported by digital adoption. Wingstop recorded 20% same store sales growth, driven by value positioning and delivery strength. Wendy’s and Jack in the Box are rationalizing store footprints to protect margins. Global players continue to invest in menu innovation, customization platforms, and regional expansion. Franchise led growth remains central to expansion strategies, particularly in emerging markets.

|

Global Fast-Food Market |

|||

|

Report Coverage |

Details |

||

|

Base Year: |

2025 |

Forecast Period: |

2026-2032 |

|

Historical Data: |

2020 to 2025 |

Market Size in 2025: |

USD 1306.69 Billion |

|

Forecast Period 2026 to 2032 CAGR: |

6.08% |

Market Size in 2032: |

USD 1975.18 Billion |

|

Fast-Food Market Segment Analysis |

By Product |

Pizza/Pasta Burgers/Sandwich Chicken Seafood Others |

|

|

By Cuisine |

American Chinese Mexican Indian Italian Others |

||

|

By Service Type |

On-Premise Delivery & Take Away |

||

|

By Distribution Channel |

Full-Service Restaurants Quick-Service restaurants Catering Others |

||

Global Fast-Food Market Key Players

-

McDonald’s (USA)

-

Starbucks (USA)

-

Subway (USA)

-

Burger King (USA/RBI)

-

Domino’s Pizza (USA)

-

Wendy’s (USA)

-

Chick-fil-A (USA)

-

Dunkin’ (USA)

-

Jollibee Foods Corporation

-

Luckin Coffee

-

Yum! Brands

-

Yum China (China)

-

Arcos Dorados

-

Carl’s Jr. (USA/CKE)

-

Dave’s Hot Chicken

-

Papa John’s International (USA)

-

Panera Bread (USA)

-

Jersey Mike’s Subs (USA)

-

Debonairs Pizza (South Africa)

-

Tim Hortons

-

Popeyes

Frequently Asked Questions

The hamburger segment held more than 30%, followed by Pizza segment in 2025.

North America held the highest share in the market in 2025.

The increasing popularity of online food and the increasing purchasing power of consumers worldwide has brought about a change in the growth of the industry.

1. Global Fast-Food Market: Research Methodology

2. Global Fast-Food Market Introduction

2.1. Market Size (2025) & Forecast (2026-2032)

2.2. Market Size (Value USD Bn. And Volume Tons) and Market Share (%) - By Segments, Regions and Country

2.3. Executive Summary

3. Global Fast-Food Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Competitive Landscape

3.3. Key Players Benchmarking

3.3.1. Company Name

3.3.2. Headquarter

3.3.3. Product Portfolio

3.3.4. Production Capacity (Tons)

3.3.5. Marketing and Flavor Innovation

3.3.6. Sustainability & Certifications

3.3.7. Technology Adoption

3.3.8. Marketing & Promotional Activities

3.3.9. Distribution & Channel Strategy

3.3.10. Packaging & Innovation in Formats

3.3.11. Regulatory Compliance & Quality Standards

3.3.12. R&D Investment (%)

3.3.13. Pricing Strategy

3.3.14. Market Share (%)

3.3.15. Market Revenue (2025)

3.3.16. Global Presence

3.4. Market Structure

3.4.1. Market Leaders

3.4.2. Market Followers

3.4.3. Emerging Players

3.5. Mergers and Acquisitions Details

3.6. Recent Developments

3.7. Market Positioning & Share Analysis

3.7.1. Company Revenue, Fast-Food Revenue, and Market Share (%)

3.7.2. SMR Competitive Positioning

3.8. Strategic Developments & Partnerships

4. Fast-Food Market: Dynamics

4.1. Fast-Food Market Trends

4.2. Fast-Food Market Dynamics

4.2.1. North America

4.2.2. Europe

4.2.3. Asia Pacific

4.2.4. Middle East and Africa

4.2.5. South America

4.3. PORTER’s Five Forces Analysis

4.4. PESTLE Analysis

5. Fast Food Consumption Analysis

5.1. Global fast food consumption value and volume trends

5.2. Per capita fast food consumption by region and key countries (2025)

5.3. Meal occasion split: breakfast, lunch, dinner, snacking

5.4. Consumption frequency by age group and income bracket

5.5. Out of home food spend share attributable to fast food

6. Fast-Food Production and Food Preparation Ecosystem

6.1. Centralized vs in store food preparation models

6.2. Role of commissary kitchens and co packing partners

6.3. Standardization and SKU rationalization practices

6.4. Fresh vs frozen ingredient usage by category

6.5. Impact of automation and semi automated kitchens

7. Global Fast-Food Market Supply Chain and Sourcing Dynamics

7.1. Raw material sourcing patterns: meat, poultry, dairy, grains, oils

7.2. Regional sourcing vs global procurement strategies

7.3. Cold chain penetration and logistics constraints

7.4. Supplier concentration and contract structures

7.5. Supply disruption risks and mitigation strategies

8. Global Fast-Food Market Demand Drivers and Demand Outlook

8.1. Urbanization and workforce participation impact

8.2. Delivery platform driven demand uplift

8.3. Price sensitivity and value menu dependence

8.4. Impact of income growth in emerging markets

8.5. Short term vs structural demand drivers

9. Consumer Behaviour and Demographics

9.1. Consumption behaviour by age cohort: Gen Z, Millennials, Gen X

9.2. Family vs individual consumption patterns

9.3. Brand loyalty vs price led switching behavior

9.4. Health perception, nutrition awareness, and menu reformulation impact

9.5. Influence of digital ordering and loyalty programs

10. Regional Fast Food Adoption Analysis

10.1. Maturity assessment of fast food markets by region

10.2. Penetration of global brands vs local chains

10.3. Cultural adaptation of menus and formats

10.4. Adoption speed in Tier 2 and Tier 3 cities

10.5. Regional growth ceilings and saturation indicators

11. Global Fast-Food Market Channel and Format Analysis

11.1. Dine in vs takeaway vs delivery contribution

11.2. Drive thru penetration by region

11.3. Mall based vs standalone outlets

11.4. Cloud kitchen integration with legacy brands

11.5. Format wise profitability considerations

12. Global Fast-Food Market Pricing, Affordability, and Menu Economics (2025)

12.1. Average ticket size by region and category (2020-2025)

12.2. Menu price inflation trends

12.3. Role of combo meals and bundling

12.4. Premium vs value positioning by brand

12.5. Consumer price tolerance thresholds

13. Global Fast-Food Market Regulatory, Health, and Policy Environment

13.1. Food safety and labeling regulations

13.2. Trans fat, sugar, and calorie disclosure norms

13.3. Local sourcing and import restrictions

13.4. Labor laws and wage pressure

13.5. Advertising restrictions targeting children

14. Global Fast-Food Market Sustainability and ESG Considerations

14.1. Packaging reduction and recyclability initiatives

14.2. Protein sourcing shifts and alternatives

14.3. Food waste management practices

14.4. Energy and water efficiency in stores

14.5. ESG impact on brand perception and demand

15. Global Fast-Food Market: Size and Forecast by Segmentation (By Value USD Million and Volume Tons) (2025-2032)

15.1. Global Fast-Food Market Size and Forecast, By Product Type

15.1.1. Pizza/Pasta

15.1.2. Burgers/Sandwich

15.1.3. Chicken

15.1.4. Seafood

15.1.5. Others

15.2. Global Fast-Food Market Size and Forecast, By Cuisine

15.2.1. American

15.2.2. Chinese

15.2.3. Mexican

15.2.4. Indian

15.2.5. Italian

15.2.6. Others

15.3. Global Fast-Food Market Size and Forecast, By Service Type

15.3.1. On-Premise

15.3.2. Delivery & Take Away

15.4. Global Fast-Food Market Size and Forecast, By Distribution Channel

15.4.1. Full-Service Restaurants

15.4.2. Quick-Service restaurants

15.4.3. Catering

15.4.4. Others

15.5. Global Fast-Food Market Size and Forecast, By Region

15.5.1. North America

15.5.2. Europe

15.5.3. Asia Pacific

15.5.4. Middle East and Africa

15.5.5. South America

16. North America Fast-Food Market Size and Forecast By Segmentation (By Value USD Million and Volume Tons) (2025-2032)

16.1. North America Market Size and Forecast, By Product Type

16.2. North America Market Size and Forecast, By Cuisine

16.3. North America Market Size and Forecast, By Service Type

16.4. North America Market Size and Forecast, By Distribution Channel

16.5. North America Market Size and Forecast, By Country

16.5.1. United States

16.5.2. Canada

16.5.3. Mexico

17. Europe Fast-Food Market Size and Forecast By Segmentation (By Value USD Million and Volume Tons) (2025-2032)

17.1. Europe Market Size and Forecast, By Product Type

17.2. Europe Market Size and Forecast, By Cuisine

17.3. Europe Market Size and Forecast, By Service Type

17.4. Europe Market Size and Forecast, By Distribution Channel

17.5. Europe Market Size and Forecast, By Country

17.5.1. United Kingdom

17.5.2. France

17.5.3. Germany

17.5.4. Italy

17.5.5. Spain

17.5.6. Sweden

17.5.7. Russia

17.5.8. Rest of Europe

18. Asia Pacific Fast-Food Market Size and Forecast By Segmentation (By Value USD Million and Volume Tons) (2025-2032)

18.1. Asia Pacific Market Size and Forecast, By Product Type

18.2. Asia Pacific Market Size and Forecast, By Cuisine

18.3. Asia Pacific Market Size and Forecast, By Service Type

18.4. Asia Pacific Market Size and Forecast, By Distribution Channel

18.5. Asia Pacific Market Size and Forecast, By Country

18.5.1. China

18.5.2. Japan

18.5.3. South Korea

18.5.4. India

18.5.5. Australia

18.5.6. Malaysia

18.5.7. Thailand

18.5.8. Vietnam

18.5.9. Indonesia

18.5.10. Philippines

18.5.11. Rest of Asia Pacific

19. Middle East and Africa Fast-Food Market Size and Forecast By Segmentation (By Value USD Million and Volume Tons) (2025-2032)

19.1. Middle East and Africa Market Size and Forecast, By Product Type

19.2. Middle East and Africa Market Size and Forecast, By Cuisine

19.3. Middle East and Africa Market Size and Forecast, By Service Type

19.4. Middle East and Africa Market Size and Forecast, By Distribution Channel

19.5. Middle East and Africa Market Size and Forecast, By Country

19.5.1. South Africa

19.5.2. GCC

19.5.3. Nigeria

19.5.4. Egypt

19.5.5. Turkey

19.5.6. Rest of ME&A

20. South America Fast-Food Market Size and Forecast By Segmentation (By Value USD Million and Volume Tons) (2025-2032)

20.1. South America Market Size and Forecast, By Product Type

20.2. South America Market Size and Forecast, By Cuisine

20.3. South America Market Size and Forecast, By Finish

20.4. South America Market Size and Forecast, By Distribution Channel

20.5. South America Market Size and Forecast, By Country

20.5.1. Brazil

20.5.2. Argentina

20.5.3. Colombia

20.5.4. Chile

20.5.5. Rest Of South America

21. Company Profile: Key Players

21.1. McDonald’s (USA)

21.1.1. Company Overview

21.1.2. Business Portfolio

21.1.3. Financial Overview

21.1.4. SWOT Analysis

21.1.5. Strategic Analysis

21.1.6. Recent Developments

21.2. Starbucks (USA)

21.3. Subway (USA)

21.4. Burger King (USA/RBI)

21.5. Domino’s Pizza (USA)

21.6. Wendy’s (USA)

21.7. Chick-fil-A (USA)

21.8. Dunkin’ (USA)

21.9. Panda Express

21.10. Jollibee Foods Corporation

21.11. Luckin Coffee

21.12. Yum! Brands

21.13. Yum China (China)

21.14. Arcos Dorados

21.15. Carl’s Jr. (USA/CKE)

21.16. Dave’s Hot Chicken

21.17. Papa John’s International (USA)

21.18. Panera Bread (USA)

21.19. Jersey Mike’s Subs (USA)

21.20. Debonairs Pizza (South Africa)

21.21. Tim Hortons

21.22. Popeyes

22. Key Findings

23. Industry Recommendations