Drilling Polymers Market Global Industry Analysis and Forecast (2026-2032) Trends, Statistics, Dynamics, Segment Analysis

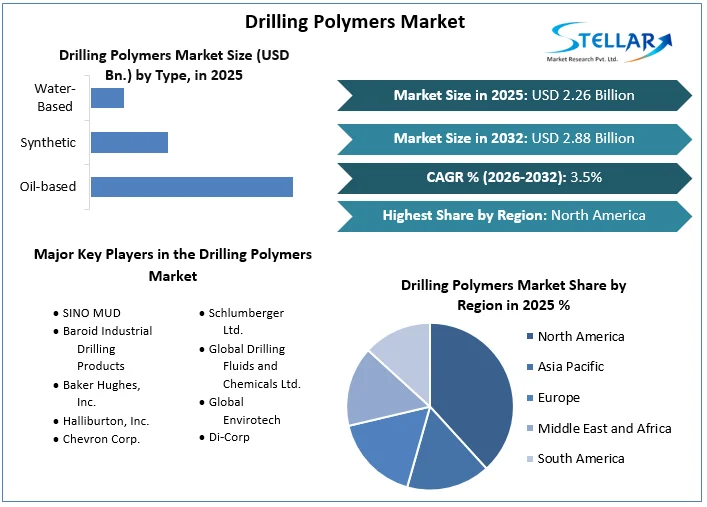

The Global Drilling Polymers Market was estimated to be worth USD 2.26 Billion in 2025 from 2026 to 2032, it is anticipated to grow at a compound annual growth rate (CAGR) of 3.5%, reaching US$ 2.88 Billion.

Drilling Polymers Market Overview:

The production and sale of polymers used in drilling operations is referred to as the "drilling polymers market" in the energy sector. These polymers are essential to the structure of drilling fluids, the resilience of wellbore walls, and the overall efficiency of drilling.

Due to a surge in demand from a number of end-use industries, including as the mining, construction, oil & gas, and geothermal industries, the drilling polymer sector is genuinely growing. In order to improve the overall effectiveness of drilling operations, notably in the oil and gas industry, drilling polymers are used as crucial chemical additives that are added to drilling fluids. Adding drilling polymers to the drilling fluid can have several advantageous effects. These polymers enhance the drilling fluid's viscosity and stability, ensuring that it keeps its ideal properties throughout the drilling process. They also increase the fluid's carrying capacity, making it more efficient at moving drill cuttings to the surface.

To get more Insights: Request Free Sample Report

Drilling Polymers Market Dynamics:

Growing Oil and Gas Exploration and Production

Drilling polymer demand and oil and gas production are closely connected. The need for energy on a global basis is increasing, which calls for increased exploration and production activities. For a variety of drilling techniques, including wellbore stability, fluid loss management, and shale inhibition, drilling polymers are essential.

More sophisticated drilling operations are now possible thanks to modern drilling equipment. High-performance drilling polymers are needed to overcome the difficulties faced by deep-water drilling, horizontal drilling, and unconventional resource extraction techniques like hydraulic fracturing (fracking). These advances necessitate innovation in polymer solutions.

The cost-effectiveness of drilling operations is a significant driver. Drilling polymers can help reduce drilling time, minimize downtime, and optimize drilling fluid properties. This, in turn, reduces overall drilling costs and enhances operational efficiency.

Increasing preference for water-based drilling fluids over oil-based fluids due to environmental considerations is driving the demand for drilling polymers compatible with water-based systems.

High Research and Development Costs

Developing new and improved drilling polymers with enhanced properties or lower environmental impact can be expensive. Profitability can be hampered by the significant investments that businesses in this sector must make in R&D to remain competitive.

Drilling firms are continually looking for drilling solutions that are more effective and economical as technology develops. This can lead to competition from alternative drilling fluids and technologies that may not rely on polymers.

Market players for drilling polymers rely on a convoluted worldwide supply chain. Drilling polymers may become harder to come by if the supply chain is disrupted, whether as a result of a natural disaster, geopolitical unrest, or other circumstances.

The drilling polymers market is closely tied to the oil and gas industry. Fluctuations in oil prices can directly impact drilling activity. When oil prices are low, drilling companies may reduce their exploration and drilling activities, leading to reduced demand for drilling polymers.

Drilling Polymers Market Opportunities:

Market Diversification

Expanding the application of drilling polymers beyond oil and gas, such as in geothermal drilling or mining operations, can diversify revenue streams and reduce dependence on the oil and gas sector.

Developing recycling processes for used drilling polymers and promoting a circular economy approach can address sustainability concerns and create opportunities for eco-friendly polymer solutions.

Incorporating digital technologies and data analytics into drilling operations is becoming more common. Drilling polymers that work synergistically with digital tools to optimize drilling processes and reduce downtime can be highly sought after.

Drilling Polymers Market Challenges:

Fluctuating raw material prices

Drilling polymers are made from raw ingredients including acrylamide and guar gum, the prices of which are volatile and subject to large swings. Planning budgets and operations for drilling businesses may be challenging as a result.

Environmental laws: Drilling fluids, especially drilling polymers, are subject to an increasing number of environmental laws. Because of this, creating and using drilling polymers that abide by these rules may become more challenging and expensive.

Substitutes' competition Drilling polymers can be replaced with a variety of materials, including clay, cellulose, and starch. These alternatives can be less priced and have comparable results. Prices for drilling polymers may fall as a result of this.

Drilling Polymers Market Trends:

In order to create new polymers that are more effective, efficient, and ecologically friendly, drilling polymers is the subject of continuing research and development.

The utilization of bio-based drilling polymers is expanding Bio-based drilling polymers are created using renewable resources like soy protein and cornstarch. They are becoming more and more well-liked as a more environmentally friendly substitute for conventional drilling polymers.

Construction and mining are two additional industries that employ drilling plastics. The expansion of these sectors is anticipated to open up new market prospects for drilling polymers.

Drilling Polymers Market Regional Insights:

In 2025, North America is anticipated to represent over 30% of the global drilling polymers market, making it the largest market in the globe. Because of the growing need for oil and gas exploration and production activities, the United States is the key market driver in this sector.

With more than 20% of the world's drilling polymer industry, Europe is the second-largest market. With a CAGR of more than 4% over the predicted term, Asia Pacific has the drilling polymers market's fastest growth. Despite being less developed markets for drilling polymers than North America and Europe, South America and the Middle East & Africa are expected to grow significantly throughout the estimated time frame.

Drilling Polymers Market Segment Analysis:

By Type, Oil-based, synthetic, and water-based drilling polymers are the three divisions of the market. Since they are less harmful to the environment than polymers based on oil, water-based drilling polymers are the most used variety. Since synthetic drilling polymers have more benefits than natural ones such as superior viscosity, stability, and carrying capacity, they are becoming more and more popular.

By Technique, The drilling polymers market is segmented into DTH drills, diamond drilling, top hammer drilling, reverse circulation drilling, and others. The most popular kind of drilling equipment is a DTH drill, which is used for a range of tasks like drilling water wells, oil and gas wells, and building holes. Diamond drilling is employed to penetrate tough, abrasive materials like rock formations. Top hammer drilling is used for drilling through soft materials, such as soil and sand. Reverse circulation drilling is used for drilling deep wells, and it is often used in offshore drilling applications.

By Application, The two market segments for drilling polymers are offshore drilling and onshore drilling. Onshore drilling is the most prevalent application sector because it makes up the majority of drilling activities worldwide. Offshore drilling is projected to increase more swiftly as a result of the increased offshore oil and gas exploration and production.

By End-Use Industry, Mining, construction, oil and gas, and other areas make up the drilling polymers market. The greatest end-use industry for drilling polymers is the oil and gas sector, which conducts the majority of drilling operations globally. The mining industry is the second-largest end-use sector and uses drilling polymers for a variety of tasks, including mineral exploration and extraction. The third-largest end-use industry is the construction sector, which uses drilling polymers for a range of tasks like foundation drilling and piling.

Drilling Polymers Market Competitive Landscape:

In September 2023, Baker Hughes announced that it had signed an agreement with Tellurian Inc. to provide liquefaction equipment for the Driftwood LNG project in Louisiana. The project is expected to produce up to 27.6 million tons of LNG per year.

In August 2023, Halliburton announced that it had launched the Obex EcoLock® Casing Annulus Packer to help prevent sustained casing pressure. The packer is designed to be more environmentally friendly than traditional packers.

In September 2023, Baroid announced that it had launched the EZ-MUD® Xtreme Drilling Fluid Additive. The additive is designed to improve the performance of water-based drilling fluids in challenging conditions, such as high temperatures and pressures.

In August 2023, Baroid announced that it had introduced the QUIK-GEL® Xtreme Drilling Fluid Additive. The additive is designed to improve the gel strength and fluid loss control of water-based drilling fluids.

|

Drilling Polymers Market Scope |

|

|

Market Size in 2025 |

USD 2.26 Billion. |

|

Market Size in 2032 |

USD 2.88 Billion. |

|

CAGR (2026-2032) |

3.5% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segment Scope |

By Type

|

|

By Technique

|

|

|

By Application

|

|

|

By End-Use Industry

|

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Drilling Polymers Market Key Players:

- SINO MUD

- Baroid Industrial Drilling Products

- Baker Hughes, Inc.

- Halliburton, Inc.

- Chevron Corp.

- Schlumberger Ltd.

- Global Drilling Fluids and Chemicals Ltd.

- Global Envirotech

- Di-Corp

Frequently Asked Questions

The Drilling Polymers Market size is expected to reach USD 2.88 Billion by 2032.

The major players in the Drilling Polymers Market include SINO MUD Baroid Industrial Drilling Products Baker Hughes, Inc. Halliburton, Inc. Chevron Corp. Schlumberger Ltd. Global Drilling Fluids and Chemicals Ltd. Global Envirotech Di-Corp.

The expected CAGR of the Drilling Polymers Market is 3.5% from 2026 to 2032.

The North American market dominated the Drilling Polymers Market by Region in 2025.

1. Global Drilling Polymers Market: Research Methodology

2. Global Drilling Polymers Market: Executive Summary

3. Global Drilling Polymers Market: Competitive Landscape

3.1. Stellar Competition Matrix

3.2. Competitive Landscape

3.3. Key Players Benchmarking

3.4. Market Structure

3.4.1. Market Leaders

3.4.2. Market Followers

3.4.3. Emerging Players

3.5. Consolidation of the Market

4. Global Drilling Polymers Market: Dynamics

4.1. Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Market Drivers by Region

4.2.1. North America

4.2.2. Europe

4.2.3. Asia Pacific

4.2.4. Middle East and Africa

4.2.5. South America

4.3. Market Restraints

4.4. Market Opportunities

4.5. Market Challenges

4.6. PORTER’s Five Forces Analysis

4.7. PESTLE Analysis

4.8. Value Chain Analysis

4.9. Regulatory Landscape by Region

4.9.1. North America

4.9.2. Europe

4.9.3. Asia Pacific

4.9.4. Middle East and Africa

4.9.5. South America

5. Global Drilling Polymers Market Size and Forecast by Segments (by Value USD and Volume Units)

5.1. Global Drilling Polymers Market Size and Forecast, by Type (2025-2032)

5.1.1. Oil-based

5.1.2. Synthetic

5.1.3. Water-based

5.2. Global Drilling Polymers Market Size and Forecast, by Technique (2025-2032)

5.2.1. DTH drills

5.2.2. Diamond drilling

5.2.3. Top hammer drilling

5.2.4. Reverse circulation drilling

5.2.5. Others

5.3. Global Drilling Polymers Market Size and Forecast, by Application (2025-2032)

5.3.1. Offshore drilling

5.3.2. Onshore drilling

5.4. Global Drilling Polymers Market Size and Forecast, by End-Use Industry (2025-2032)

5.4.1. Mining

5.4.2. Construction

5.4.3. Oil and gas

5.4.4. Other

5.5. Global Drilling Polymers Market Size and Forecast, by Region (2025-2032)

5.5.1. North America

5.5.2. Europe

5.5.3. Asia Pacific

5.5.4. Middle East and Africa

5.5.5. South America

6. North America Global Drilling Polymers Market Size and Forecast (by Value USD and Volume Units)

6.1. North America Global Drilling Polymers Market Size and Forecast, by Type (2025-2032)

6.1.1. Oil-based

6.1.2. Synthetic

6.1.3. Water-based

6.2. North America Global Drilling Polymers Market Size and Forecast, by Technique (2025-2032)

6.2.1. DTH drills

6.2.2. Diamond drilling

6.2.3. Top hammer drilling

6.2.4. Reverse circulation drilling

6.2.5. Others

6.3. North America Global Drilling Polymers Market Size and Forecast, by Application (2025-2032)

6.3.1. Offshore drilling

6.3.2. Onshore drilling

6.4. North America Global Drilling Polymers Market Size and Forecast, by End-Use Industry (2025-2032)

6.4.1. Mining

6.4.2. Construction

6.4.3. Oil and gas

6.4.4. Other

6.5. North America Global Drilling Polymers Market Size and Forecast, by Country (2025-2032)

6.5.1. United States

6.5.2. Canada

6.5.3. Mexico

7. Europe Global Drilling Polymers Market Size and Forecast (by Value USD and Volume Units)

7.1. Europe Global Drilling Polymers Market Size and Forecast, by Type (2025-2032)

7.1.1. Oil-based

7.1.2. Synthetic

7.1.3. Water-based

7.2. Europe Global Drilling Polymers Market Size and Forecast, by Technique (2025-2032)

7.2.1. DTH drills

7.2.2. Diamond drilling

7.2.3. Top hammer drilling

7.2.4. Reverse circulation drilling

7.2.5. Others

7.3. Europe Global Drilling Polymers Market Size and Forecast, by Application (2025-2032)

7.3.1. Offshore drilling

7.3.2. Onshore drilling

7.4. Europe Global Drilling Polymers Market Size and Forecast, by End-Use Industry (2025-2032)

7.4.1. Mining

7.4.2. Construction

7.4.3. Oil and gas

7.4.4. Other

7.5. Europe Global Drilling Polymers Market Size and Forecast, by Country (2025-2032)

7.5.1. UK

7.5.2. France

7.5.3. Germany

7.5.4. Italy

7.5.5. Spain

7.5.6. Sweden

7.5.7. Austria

7.5.8. Rest of Europe

8. Asia Pacific Global Drilling Polymers Market Size and Forecast (by Value USD and Volume Units)

8.1. Asia Pacific Global Drilling Polymers Market Size and Forecast, by Type (2025-2032)

8.1.1. Oil-based

8.1.2. Synthetic

8.1.3. Water-based

8.2. Asia Pacific Global Drilling Polymers Market Size and Forecast, by Technique (2025-2032)

8.2.1. DTH drills

8.2.2. Diamond drilling

8.2.3. Top hammer drilling

8.2.4. Reverse circulation drilling

8.2.5. Others

8.3. Asia Pacific Global Drilling Polymers Market Size and Forecast, by Application (2025-2032)

8.3.1. Offshore drilling

8.3.2. Onshore drilling

8.4. Asia Pacific Global Drilling Polymers Market Size and Forecast, by End-Use Industry (2025-2032)

8.4.1. Mining

8.4.2. Construction

8.4.3. Oil and gas

8.4.4. Other

8.5. Asia Pacific Global Drilling Polymers Market Size and Forecast, by Country (2025-2032)

8.5.1. China

8.5.2. S Korea

8.5.3. Japan

8.5.4. India

8.5.5. Australia

8.5.6. Indonesia

8.5.7. Malaysia

8.5.8. Vietnam

8.5.9. Taiwan

8.5.10. Bangladesh

8.5.11. Pakistan

8.5.12. Rest of Asia Pacific

9. Middle East and Africa Global Drilling Polymers Market Size and Forecast (by Value USD and Volume Units)

9.1. Middle East and Africa Global Drilling Polymers Market Size and Forecast, by Type (2025-2032)

9.1.1. Oil-based

9.1.2. Synthetic

9.1.3. Water-based

9.2. Middle East and Africa Global Drilling Polymers Market Size and Forecast, by Technique (2025-2032)

9.2.1. DTH drills

9.2.2. Diamond drilling

9.2.3. Top hammer drilling

9.2.4. Reverse circulation drilling

9.2.5. Others

9.3. Middle East and Africa Global Drilling Polymers Market Size and Forecast, by Application (2025-2032)

9.3.1. Offshore drilling

9.3.2. Onshore drilling

9.4. Middle East and Africa Global Drilling Polymers Market Size and Forecast, by End-Use Industry (2025-2032)

9.4.1. Mining

9.4.2. Construction

9.4.3. Oil and gas

9.4.4. Other

9.5. Middle East and Africa Global Drilling Polymers Market Size and Forecast, by Country (2025-2032)

9.5.1. South Africa

9.5.2. GCC

9.5.3. Egypt

9.5.4. Nigeria

9.5.5. Rest of ME&A

10. South America Global Drilling Polymers Market Size and Forecast (by Value USD and Volume Units)

10.1. South America Global Drilling Polymers Market Size and Forecast, by Type (2025-2032)

10.1.1. Oil-based

10.1.2. Synthetic

10.1.3. Water-based

10.2. South America Global Drilling Polymers Market Size and Forecast, by Technique (2025-2032)

10.2.1. DTH drills

10.2.2. Diamond drilling

10.2.3. Top hammer drilling

10.2.4. Reverse circulation drilling

10.2.5. Others

10.3. South America Global Drilling Polymers Market Size and Forecast, by Application (2025-2032)

10.3.1. Offshore drilling

10.3.2. Onshore drilling

10.4. South America Global Drilling Polymers Market Size and Forecast, by End-Use Industry (2025-2032)

10.4.1. Mining

10.4.2. Construction

10.4.3. Oil and gas

10.4.4. Other

10.5. South America Global Drilling Polymers Market Size and Forecast, by Country (2025-2032)

10.5.1. Brazil

10.5.2. Argentina

10.5.3. Rest of South America

11. Company Profile: Key players

11.1. SINO MUD

11.1.2. Company Overview

11.1.3. Financial Overview

11.1.4. Business Portfolio

11.1.5. SWOT Analysis

11.1.6. Business Strategy

11.1.7. Recent Developments

11.2. Baroid Industrial Drilling Products

11.3. Baker Hughes, Inc.

11.4. Halliburton, Inc.

11.5. Chevron Corp.

11.6. Schlumberger Ltd.

11.7. Global Drilling Fluids and Chemicals Ltd.

11.8. Global Envirotech

11.9. Di-Corp

12. Key Findings

13. Industry Recommendation