Craft Wine Market - Global Industry Analysis and Forecast 2026-2034

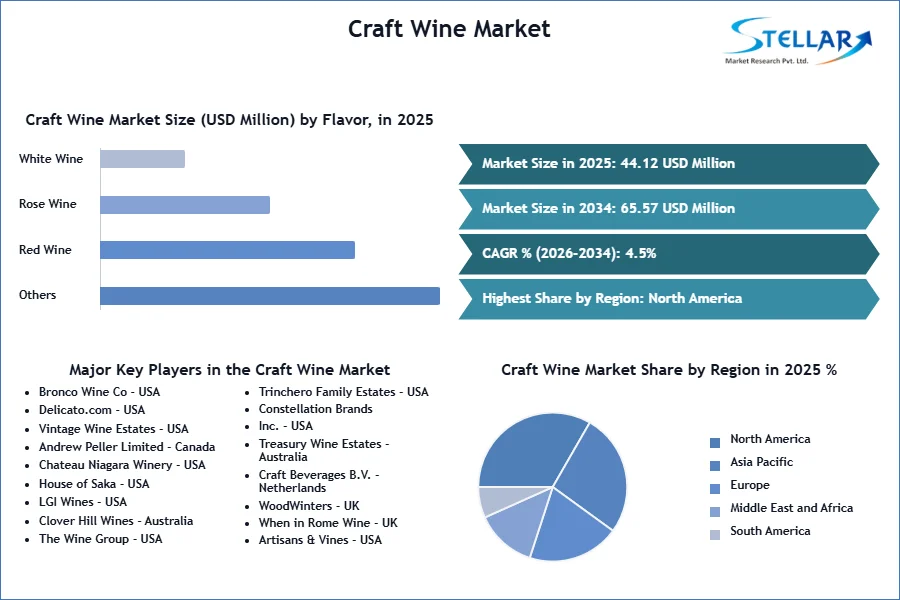

The Craft Wine Market size was valued at USD 44.12 Bn. in 2025 and the total Craft Wine Market revenue is expected to grow at a CAGR of 4.5% from 2026 to 2034, reaching nearly USD 65.57 Bn. by 2034.

Craft Wine Market Overview

The global craft wine market is growing because of the increasing trend of premium drinks and the availability of various flavours. Consumer spending on healthy and functional beverages boosts the immune system, and innovations in craft wine packaging create opportunities. Single-serve wine bottles, which are user-friendly and cost-effective, are replacing the standard 750 ml bottle. Craft wine offers health benefits because of its organic substance and bitter taste, attracting consumers. The demand for flavourful and high-quality drinks is also increasing, as the organic substance in craft wine has a bitter taste. Overall, the craft wine industry market is expected to grow during the forecast period from 2026 to 2034.

Craft wine, according to the American Heart Association, is beneficial for hair and skin, maintaining a healthy body weight, and aiding blood formation. Red grape skin contains tannins that reduce bad cholesterol and increase good cholesterol levels, promoting healthy blood vessels. Also, craft wine contains resveratrol, an antioxidant and anti-inflammatory substance, which protects against diseases like cancer, diabetes, and Alzheimer's.

To get more Insights: Request Free Sample Report

Craft Wine Market Dynamics:

The craft wine market has experienced significant growth in recent years because of the growing demand for unique and high-quality wines. Craft wine is small-batch, artisanal wines produced by independent wineries using traditional methods, focusing on quality rather than mass production. These wines are sourced from small vineyards and showcase unique flavors and characteristics. Craft winemakers emphasize the artistry and craftsmanship involved in the wine-making process, producing limited quantities of premium wines.

They aim to provide an authentic and personalized experience for wine lovers who appreciate the attention to detail and the story behind each bottle. Craft wine aligns with the growing consumer preference for artisanal products, offering unique and handcrafted wines that stand out from mass-produced options. Also, craft wineries are committed to sustainable and organic farming practices, catering to the growing demand for eco-friendly products.

The market growth of wine-based cocktails is expected to increase because of the increasing demand among millennials, who prefer minimalist, flavourful cocktails with a few ingredients. Popular options include sangria, mango passion, French pear martini, and bishop cocktail. This preference for high-quality craft beverages is driven by the desire for excellent taste and flavor Encouraging manufacturers to introduce creative cocktails in the market growth.

The Craft Wine Market faces difficulties in its operations and customer experience because of its tiny footprint, irregular availability resulting from small-scale production, and more expensive prices in comparison to larger merchants. Despite these limitations, the industry thrives by utilizing its carefully chosen inventory, experienced staff, and focus on quality to provide wine lovers with an exceptional and unforgettable experience. The Craft Wine Market has ongoing challenges from competition from larger retailers and online platforms. To stand out, the company must provide distinctive offers and provide individualized customer care.

The growth of e-commerce platforms has enabled craft wineries to sell their products directly to consumers, bypassing traditional distribution channels. This allows them to reach a wider audience and establish direct relationships with customers. Wine tourism is also leveraged by craft wineries to attract visitors and showcase their unique wines. Offering tasting experiences, vineyard tours, and wine-related events fosters brand loyalty and increases sales. Collaborations with local food establishments enhance visibility and reach, while export opportunities are explored to tap into global markets with a growing interest in premium and specialty products. Overall, leveraging e-commerce and wine tourism helps craft wineries reach a wider audience and increase sales.

The demand for new flavors in craft wine has led to manufacturers offering various types like red, rose, and white wine. These unique flavors are in high demand because of their taste and color. Major industry players are introducing new unique craft wines, creating opportunities for the craft wine market. Embracing novel blending processes encourages consumers to buy artisan wines.

Craft Wine Market Segment Analysis:

Based on Flavor, The red wine market which accounting for 60% of market size, is expected to grow because of rising health consciousness among consumers. The trend towards healthy eating is driven by the need for food and beverage products that align with ethical, sustainable, and health-conscious standards. Red wine, rich in plant compounds, offers health benefits like reduced inflammation, reduced cancer risk, and an extended lifespan. Its alcohol content and antioxidants also help prevent coronary artery disease. The International Food Information Council's survey shows that 54% of consumers and 63% of those aged 50 and above express concerns about the healthfulness of their food and beverages.

The on-trade segment, accounting for 60% of market revenue and provides consumers with social settings, live music, and culinary experiences in restaurants and lounges. Some wineries even allow customers to participate in the wine-making process and making it an engaging point of interest and contributing to the growth of on-trade sales in the craft alcoholic beverage market.

Craft Wine Market Regional Insight:

The North America region holds the largest market share in the Craft Wine Market, largely because of its leading manufacturing companies and the availability of high-quality craft wine beverages. This dominance is further reinforced by the increasing demand for craft wine because of its versatility and long-lasting characteristics. The craft wine market is experiencing growth thanks to increased consumption in major US and Canadian countries. For instance,

- Andrew Peller Limited, a leading producer of quality wines and craft beverage alcohol products and reported a 2.6% increase in sales because of product launches and rising prices.

Consumer disposable income and spending on craft wine also contribute to market growth. North America maintains the largest market share, largely thanks to its leading manufacturing companies and the availability of high-quality craft wine beverages. The increasing demand for craft wine, driven by its versatility and long-lasting characteristics, further solidifies its dominance in the craft wine market.

Craft Wine Market Competitive Landscape:

Leading market players are investing in research and development to increase their product lines, boosting the Craft Wine market. They are also undertaking strategic activities like new product launches, contractual agreements, mergers and acquisitions, higher investments, and collaborations. To survive in a competitive market, the Craft Wine industry must offer cost-effective items.

- In 2024, The Wine Group Expands its National Distribution Alignment with Southern Glazer’s Wine & Spirits the world’s preeminent distributor of beverage alcohol they announced have further expanded their national distribution agreement to include the open markets of Hawaii, Iowa, and Minnesota, Nebraska, North Dakota, and South Dakota.

- In 2023, Trinchero Family Estates (TFE) is making a significant investment in a series of sustainability projects, spanning four properties and exemplifying its proactive approach to reducing its carbon footprint. These projects scheduled for completion include solar installations at four California wineries Westside Winery in Lodi, Main Street Winery in St. Helena, Trinchero Central Coast Winery in Paso Robles, and Green Island Road Winery in American Canyon. Together, annual solar production across the four sites reaches 11.5 million kWh.

- Constellation Brands is a leading international producer and marketer of beer, wine, and spirits with operations in the U.S., Mexico, New Zealand, and Italy. Our mission is to build brands that people love because we believe elevating human connections is Worth Reaching For. It’s worth our dedication, hard work, and calculated risks to expect market trends and deliver more for our consumers, shareholders, employees, and industry. This dedication is what has driven us to become one of the fastest-growing, large CPG companies in the U.S. at retail, and it drives our pursuit to deliver.

|

Craft Wine Market Scope |

|

|

Market Size in 2025 |

USD 44.12 Bn. |

|

Market Size in 2034 |

USD 65.57 Bn. |

|

CAGR (2026-2034) |

4.5 % |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Segments |

By Type Sparkling Wine Still Wine Others |

|

By Flavor Red Wine Rose Wine White Wine |

|

|

By Distribution Channel On-trade Off-Trade |

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Russia, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Player in the Craft Wine Market

- Bronco Wine Co - USA

- Delicato.com - USA

- Vintage Wine Estates - USA

- Andrew Peller Limited - Canada

- Chateau Niagara Winery - USA

- House of Saka - USA

- LGI Wines - USA

- Clover Hill Wines - Australia

- The Wine Group - USA

- Trinchero Family Estates - USA

- Constellation Brands, Inc. - USA

- Treasury Wine Estates - Australia

- Craft Beverages B.V. - Netherlands

- WoodWinters - UK

- When in Rome Wine - UK

- Artisans & Vines - USA

- Handpicked Wines - Australia

- Barelle Vineyards - USA

- Heritage Estate Winery and Cidery - Canada

- Hiyori corp.com - Japan

- Wine of Japan – Japan

- XX.inc

Frequently Asked Questions

North America is expected to lead the Craft Wine Market during the forecast period.

An analysis of profit trends and projections for companies in the Craft Wine Market is included, offering insights into factors driving profitability, cost management strategies, and financial performance metrics.

The Craft Wine Market size was valued at USD 44.12 Billion in 2025 and the total Craft Wine Market size is expected to grow at a CAGR of 4.5% from 2026 to 2034, reaching nearly USD 65.57 Billion by 2034.

The segments covered in the market report are by Type, by Flavor, and by Distribution Channel.

1. Research Methodology

1.1 Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Research Assumption

2. Craft Wine Market: Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026– 2034) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Global Craft Wine Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Product Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. Product Launches and Innovations

4. Craft Wine Market: Dynamics

4.1. Craft Wine Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Craft Wine Market Drivers

4.3. Craft Wine Market Restraints

4.4. Craft Wine Market Opportunities

4.5. Craft Wine Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factor

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Value Chain Analysis

4.10. Trade Analysis

4.11. Regulatory Landscape by Region

4.11.1. North America

4.11.2. Europe

4.11.3. Asia Pacific

4.11.4. Middle East and Africa

4.11.5. South America

5. Craft Wine Market: Global Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

5.1. Craft Wine Market Size and Forecast, by Type (2026-2034)

5.1.1. Sparkling Wine

5.1.2. Still Wine

5.1.3. Others

5.2. Craft Wine Market Size and Forecast, by Flavor (2026-2034)

5.2.1. Red Wine

5.2.2. Rose Wine

5.2.3. White Wine

5.3. Craft Wine Market Size and Forecast, by Distribution Channel (2026-2034)

5.3.1. On-trade

5.3.2. Off-Trade

5.4. Craft Wine Market Size and Forecast, by Region (2026-2034)

5.4.1. North America

5.4.2. Europe

5.4.3. Asia Pacific

5.4.4. Middle East and Africa

5.4.5. South America

6. North America Craft Wine Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

6.1. North America Craft Wine Market Size and Forecast, by Type (2026-2034)

6.1.1. Sparkling Wine

6.1.2. Still Wine

6.1.3. Others

6.2. North America Craft Wine Market Size and Forecast, by Flavor (2026-2034)

6.2.1. Red Wine

6.2.2. Rose Wine

6.2.3. White Wine

6.3. North America Craft Wine Market Size and Forecast, by Distribution Channel (2026-2034)

6.3.1. On-trade

6.3.2. Off-Trade

6.4. North America Craft Wine Market Size and Forecast, by Country (2026-2034)

6.4.1. United States

6.4.2. Canada

6.4.3. Mexico

7. Europe Craft Wine Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

7.1. Europe Craft Wine Market Size and Forecast, by Type (2026-2034)

7.2. Europe Craft Wine Market Size and Forecast, by Flavor (2026-2034)

7.3. Europe Craft Wine Market Size and Forecast, by Distribution Channel (2026-2034)

7.4. Europe Craft Wine Market Size and Forecast, by Country (2026-2034)

7.4.1. United Kingdom

7.4.2. France

7.4.3. Germany

7.4.4. Italy

7.4.5. Spain

7.4.6. Sweden

7.4.7. Austria

7.4.8. Rest of Europe

8. Asia Pacific Craft Wine Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

8.1. Asia Pacific Craft Wine Market Size and Forecast, by Type (2026-2034)

8.2. Asia Pacific Craft Wine Market Size and Forecast, by Flavor (2026-2034)

8.3. Asia Pacific Craft Wine Market Size and Forecast, by Distribution Channel (2026-2034)

8.4. Asia Pacific Craft Wine Market Size and Forecast, by Country (2026-2034)

8.4.1. China

8.4.2. S Korea

8.4.3. Japan

8.4.4. India

8.4.5. Australia

8.4.6. Indonesia

8.4.7. Malaysia

8.4.8. Vietnam

8.4.9. Taiwan

8.4.10. Rest of Asia Pacific

9. Middle East and Africa Craft Wine Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

9.1. Middle East and Africa Craft Wine Market Size and Forecast, by Type (2026-2034)

9.2. Middle East and Africa Craft Wine Market Size and Forecast, by Flavor (2026-2034)

9.3. Middle East and Africa Craft Wine Market Size and Forecast, by Distribution Channel (2026-2034)

9.4. Middle East and Africa Craft Wine Market Size and Forecast, by Country (2026-2034)

9.4.1. South Africa

9.4.2. GCC

9.4.3. Nigeria

9.4.4. Rest of ME&A

10. South America Craft Wine Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

10.1. South America Craft Wine Market Size and Forecast, by Type (2026-2034)

10.2. South America Craft Wine Market Size and Forecast, by Flavor (2026-2034)

10.3. South America Craft Wine Market Size and Forecast, by Distribution Channel (2026-2034)

10.4. South America Craft Wine Market Size and Forecast, by Country (2026-2034)

10.4.1. Brazil

10.4.2. Argentina

10.4.3. Rest Of South America

11. Company Profile: Key Players

11.1. Bronco Wine Co - USA

11.1.1. Company Overview

11.1.2. Product Portfolio

11.1.2.1. Product Name

11.1.2.2. Product Details (Price, Features, etc.)

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Delicato.com - USA

11.3. Vintage Wine Estates - USA

11.4. Andrew Peller Limited - Canada

11.5. Chateau Niagara Winery - USA

11.6. House of Saka - USA

11.7. LGI Wines - USA

11.8. Clover Hill Wines - Australia

11.9. The Wine Group - USA

11.10. Trinchero Family Estates - USA

11.11. Constellation Brands, Inc. - USA

11.12. Treasury Wine Estates - Australia

11.13. Craft Beverages B.V. - Netherlands

11.14. WoodWinters - UK

11.15. When in Rome Wine - UK

11.16. Artisans & Vines - USA

11.17. Handpicked Wines - Australia

11.18. Barelle Vineyards - USA

11.19. Heritage Estate Winery and Cidery - Canada

11.20. Hiyori corp.com - Japan

11.21. Wine of Japan – Japan

11.22. XX.inc

12. Key Findings

13. Analyst Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook