Global Compound Semiconductor Market - Increasing Product Demand in Light-Emitting Diode (Led) Applications to Boost Market Growth

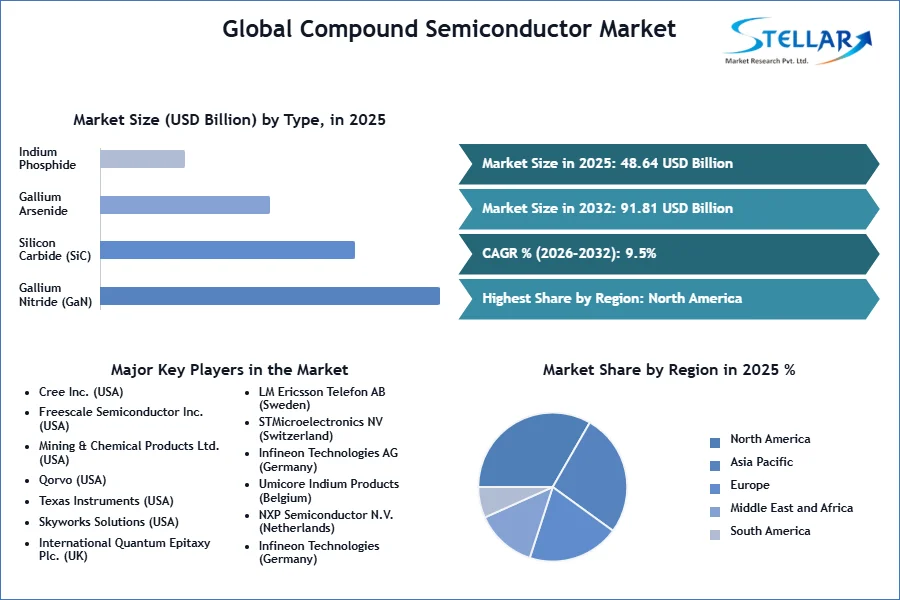

The Compound Semiconductor Market size was valued at USD 48.64 Billion in 2025 and the total Global Compound Semiconductor revenue is expected to grow at a CAGR of 9.5% from 2026 to 2032, reaching nearly USD 91.81 Billion by 2032.

Compound Semiconductor Market Overview

Compound semiconductors are specialized materials integral to modern technology, found in electric cars, solar panels, satellites, spacecraft, and smartphones. These advanced materials are crucial for future technologies such as driverless cars and artificial intelligence. By making electronic devices smaller, faster, and more efficient, compound semiconductors enhance energy production from solar panels and extend the range of electric vehicles. They contribute significantly to environmental sustainability and the pursuit of Net Zero goals by improving energy efficiency and reducing emissions.

Comparison to Traditional Semiconductors

Traditional semiconductors typically use a single material, silicon (Si), which constitutes 80% of the global semiconductor market. In contrast, compound semiconductors, which make up 20% of the market, are composed of two or more materials. This multi-material composition enables compound semiconductors to perform tasks that silicon cannot.

Advantages of Compound Semiconductors

- Power Handling: Compound semiconductors handle more power than silicon, making them ideal for use in electric cars, solar panels, wind turbines, and spacecraft.

- Speed: They are 100 times faster than silicon, which is why they are essential for 5G communications.

- Light Detection and Emission: Superior at detecting and emitting light, they are used in fiber-optic communications, medical scanners, and smartphone cameras.

With a proposed investment of USD 700 million, homegrown SaaS unicorn Zoho is venturing into the chipmaking industry, targeting the rapidly growing compound semiconductor market. Although the company has yet to comment publicly on this development, reports indicate that Zoho is seeking government incentives to support this initiative. The timing of Zoho's entry into the semiconductor market is strategic, as the Indian government recently approved USD 15.2 billion in investments to establish three semiconductor fabrication plants.

Among these, Tata Electronics' proposal to build a mega semiconductor fabrication facility in Dholera, Gujarat, in partnership with Taiwan’s Powerchip Semiconductor Manufacturing Corporation (PSMC), stands out. This facility produce 50,000 wafers a month and aims to manufacture three billion chips annually, utilizing next-generation factory automation capabilities with data analytics and machine learning to maximize efficiency. With an investment of up to ?91,000 crore, this project is set to generate over 20,000 direct and indirect skilled jobs. Zoho's move into compound semiconductors positions it to tap into this lucrative market, leveraging governmental support and the increasing demand for advanced electronic components.

To get more Insights: Request Free Sample Report

Compound Semiconductor Market Dynamics

The Increasing Product Demand in Light-Emitting Diode (Led) Applications Across the Globe is Creating a Positive Outlook for Compound Semiconductor Market Growth

The compound semiconductor market is experiencing significant growth driven by the increasing demand for Light-Emitting Diode (LED) applications worldwide. Compound semiconductors are essential for emitting and sensing different colors of light, making them indispensable in general lighting and signage displays. The rapid expansion of the electronics industry further propels market growth as these semiconductors are crucial in high-frequency devices, information displays, and optical devices. Besides, the adoption of advanced technologies such as machine learning (ML), artificial intelligence (AI), and the Internet of Things (IoT) in manufacturing processes enhances inventory control, quality, and operational efficiency, providing a robust impetus to the market. The automotive industry's rising demand for compound semiconductors in autonomous and electric vehicles also significantly contributes to market growth.

Also, the healthcare sector's increasing use of compound semiconductors in diagnostic imaging equipment and surgical instruments is driving market growth. Government initiatives promoting energy-efficient lighting solutions further stimulate the demand for compound semiconductors, as these materials are pivotal in creating efficient lighting systems. These factors, combined with technological advancements and industry-specific applications, underscore the dynamic growth trajectory of the compound semiconductor market, positioning it for continued expansion and innovation.

The rapid growth of critical technologies like 5G telecommunications and electric mobility bolsters new opportunities for the compound semiconductor market

The rapid growth of critical technologies such as 5G telecommunications and electric mobility demands higher power densities, faster-switching frequencies, and greater thermal resilience than conventional silicon-based semiconductors offer. This need drives the semiconductor industry to explore alternative materials, with gallium nitride (GaN) emerging as a promising candidate. GaN's impressive breakdown field strength, high electron mobility, and wide bandgap make it ideally suited for the next generation of high-power, high-frequency electronic systems, paving the way for energy-efficient and high-performance devices.

The growing adoption of GaN semiconductors presents a major opportunity for the United States, which already leads in GaN technology research. With the right mix of government policy and private initiatives in developing and commercializing this new material, the United States is at the forefront of the next generation of semiconductor innovation.

In the automotive sector, the increasing focus on developing autonomous and electric vehicles opens up vast opportunities for compound semiconductors, which are crucial for high-performance, energy-efficient components. The healthcare industry also provides a promising avenue for market growth, with compound semiconductors playing a vital role in diagnostic imaging equipment and surgical instruments. Government initiatives promoting the adoption of energy-efficient technologies further boost Compound Semiconductor market, making compound semiconductors an attractive investment for companies looking to capitalize on these trends. These opportunities highlight the compound semiconductor market's potential for sustained growth and technological advancement across various sectors.

Transformative Influence Across Industries is the Ultimate Trend in the Compound Semiconductor industry

Compound semiconductors have emerged as a transformative influence across various industries. Silicon carbide (SiC) is dominant in the automotive sector, particularly with the rise of 800V electric vehicles (EVs), driving a billion-dollar market. Concurrently, gallium nitride (GaN) power electronics are expanding their presence in both consumer and automotive fields.

In anticipation of a resurgence, RF gallium arsenide (GaAs) aligns itself with 5G and automotive connectivity, while RF GaN establishes its presence in defense, telecommunications, and space industries, targeting high-power applications. Within the realm of photonics, indium phosphide (InP) and GaAs take the lead. InP is experiencing a resurgence fueled by AI applications, while GaAs photonics sees modest growth influenced by various market dynamics.

Compound Semiconductor Market Regional Analysis

The rapid and far-reaching changes in public policy for semiconductor manufacturing in the US and European Union during 2022 significantly impact the compound semiconductor industry in Asia-Pacific economies. Legislation in the US and EU aims to boost domestic and regional compound semiconductor manufacturing, potentially rebalancing global production away from Asia Pacific economies. In 2020, Taiwan, South Korea, Japan, and mainland China accounted for 72% of global compound semiconductor production, with previous production locations like the US and Japan focusing more on the profitable design segment. The December 2025 announcement by Taiwan Semiconductor Manufacturing Co. (TSMC) to triple investment in manufacturing capacity in the US signals changing geographic dynamics in the sector. Policies favoring economic nationalism and supply chain security in Japan, South Korea, and India, encouraging local manufacturing development, further adjust the landscape as more locations seek to develop onshore production and reduce reliance on supply from Taiwan.

In the three- to five-year outlook, policy factors are likely to fundamentally alter the sector landscape, with increased investment and new business opportunities outside Asia Pacific for compound semiconductor manufacturing and greater competition within the region. In response to supply chain disruptions during the pandemic, the US has pursued proactive policies to re-establish domestic production, supported by legislation and new restrictions on exports of advanced compound semiconductor technology to mainland China. The EU is reshuffling existing funding programs into targeted measures to support compound semiconductor technologies and processor chip development while focusing on expanding cooperation with like-minded partners to mitigate supply chain risks.

Taiwan remains the global leader in high-value contract-based compound semiconductor manufacturing, with ongoing efforts to re-shore manufacturing and improve domestic equipment supply. South Korea's "K-semiconductor Strategy" and Japan's strategic autonomy initiatives aim to develop comprehensive manufacturing supply chains and reduce dependence on mainland China. India is positioning itself as a new player in the sector, encouraged by policies favoring self-sufficiency. Meanwhile, mainland China continues to invest heavily in developing end-to-end "sanction-proof" supply chains to counter US sanctions and leverage its position as a key trading partner in the region.

Compound Semiconductor Market Segment Analysis

Type Analysis: Gallium nitride (GaN) stands out in the compound semiconductor market due to its high electron mobility, facilitating faster switching speeds, and reduced energy losses, crucial for high-frequency applications. Its superior durability, ability to handle higher power densities, and wide operating bandwidth make GaN a preferred choice over silicon in various sectors, including automotive, data centers, and defense. With applications ranging from power electronics to radar systems and emerging technologies like MicroLEDs, GaN's integration onto silicon substrates expands its utility across diverse industries. As the United States and China vie for leadership in GaN technology, securing access to GaN resources and fostering domestic capabilities becomes increasingly vital for maintaining technological and strategic advantages in global competition.

End-User Industry Analysis: IT & Telecom accounted for the major Compound Semiconductor market value share of nearly 43% in 2025 and is expected to witness substantial growth over the analysis period. This is attributed to the rising demand for semiconductor elements in wireless and mobile communications. High efficiency and speed offered by the compound semiconductor over silicon semiconductors are the prime factors driving its application in advanced communication technologies. Furthermore, the integration of numerous upcoming technologies such as IoT, artificial intelligence, and machine learning are creating more need for the usage of high-speed semiconductor devices, thereby influencing positively the market growth of compound semiconductors.

On the other hand, consumer electronics are projected to register the most lucrative growth rate during the forecast period. Increasing end-use applications such as LED, mobile phones, television, and other entertainment devices are predicted to contribute to significant market growth.

Compound Semiconductor Market Import Export Analysis

Import Analysis for the Compound Semiconductor Market:

In 2024, global imports of semiconductive compounds totaled 2.6 thousand shipments, sourced by 200 importers from 106 suppliers worldwide. The majority of these imports were sourced from South Korea, India, and the United States, reflecting their significant roles as key suppliers in the global compound semiconductor market. The United States led import volumes with 739 shipments, followed closely by India with 495 shipments, and Egypt secured the third position with 257 shipments. This distribution highlights the strategic sourcing patterns and key import hubs shaping the global supply chain for semiconductive compounds.

Export Analysis for the Compound Semiconductor Market:

In 2024, global exports of semiconductive compounds also totaled 2.6 thousand shipments, facilitated by 106 exporters to 200 buyers across the world. The primary destinations for these exports were the United States, India, and Egypt, indicating their strong demand for semiconductive compounds in various applications. South Korea emerged as the top exporter with 994 shipments, underscoring its dominant role in supplying semiconductive compounds globally. India followed closely with 885 shipments, while the United States ranked third with 271 shipments, highlighting its position as a key player in both imports and exports within the compound semiconductor market. These export dynamics illustrate the global distribution channels and export hubs crucial for meeting international demand for semiconductive compounds.

Recent Developments in Compound Semiconductor Market

In 2024, the Chinese province Southern Guangdong announced to fund 30 billion yuan or $ 4.37 billion to invest in the production of compound semiconductors, semiconductors, automotive semiconductor chips, and other semiconductor components.

Changsha, China in 2023 announced to start of USD 7.2 billion worth of subsidies to support semiconductor industries including third-generation semiconductors.

Between 2020 and 2022, the United States-based and foreign-headquartered firms stated over USD 200 billion for private investments in the semiconductor manufacturing industry.

In 2022, Japan’s Ministry of Economy, Trade and Industry approved subsidies worth USD 3.5 billion for the construction of a semiconductor foundry in the country.

Intel, a prominent manufacturer of semiconductor chips stated in January 2023 that it has invested USD 20 billion in two new semiconductor chips factories in Ohio.

China alone produces 80% gallium, which is an essential component in compound semiconductors. According to the Chinese Customs, the nation exported 94 metric tons of gallium in 2022.

In Conclusion: The global compound semiconductor market, valued at USD 44.42 billion in 2024, is projected to reach nearly USD 91.81 billion by 2032, driven by increasing demand for LED applications and advantages over traditional silicon semiconductors. In 2024, the market saw 2.6K import shipments mainly from South Korea, India, and the United States, with the top importers being the United States, India, and Egypt. Similarly, the top exporters were South Korea, India, and the United States, reflecting the strategic importance and widespread demand for compound semiconductors across various high-performance and energy-efficient applications.

|

Compound Semiconductor Market Scope |

|

|

Market Size in 2025 |

USD 48.64 Bn. |

|

Market Size in 2032 |

USD 91.81 Bn. |

|

CAGR (2026-2032) |

9.5% |

|

Historic Data |

2020-2026 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segments |

By Type Gallium Nitride (GaN) Silicon Carbide (SiC) Gallium Arsenide (GaAs) Indium Phosphide (InP) |

|

By Application Inverters Power Amplifiers Sensors Others |

|

|

By End-User Industry Automotive IT and Telecom Consumer Goods Electronics Industrial Manufacturing Others |

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Russia, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Players in the Compound Semiconductor Market

North America

- Cree Inc. (USA)

- Freescale Semiconductor Inc. (USA)

- Mining & Chemical Products Ltd. (USA)

- Qorvo (USA)

- Texas Instruments (USA)

- Skyworks Solutions (USA)

Europe

- International Quantum Epitaxy Plc. (UK)

- LM Ericsson Telefon AB (Sweden)

- STMicroelectronics NV (Switzerland)

- Infineon Technologies AG (Germany)

- Umicore Indium Products (Belgium)

- NXP Semiconductor N.V. (Netherlands)

- Infineon Technologies (Germany)

Asia Pacific

- Taiwan Semiconductor Manufacturing Company Ltd. (Taiwan)

- Renesas Electronics Corporation (Japan)

- Toshiba Corporation (Japan)

- Nichia Corporation (Japan)

- Samsung Electronics (South Korea)

- Others

Frequently Asked Questions

Ans. APAC is expected to dominate the Compound Semiconductor Market during the forecast period.

Ans. The Compound Semiconductor Market size is expected to reach USD 91.81 Bn by 2032.

Ans. The major top players in the Global Compound Semiconductor Market are Freescale Semiconductor Inc., Mining & Chemical Products Ltd., and others.

Ans. The increasing use of compound semiconductors in mobile devices for components like radio frequency (RF) amplifiers and LEDs drives market growth.

Ans. China held the largest Compound Semiconductor Market share in 2025.

1. Research Methodology

1.1 Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Research Assumption

2. Compound Semiconductor Market: Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026 – 2032) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Global Compound Semiconductor Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Product Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2024)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. Product Launches and Innovations

4. Compound Semiconductor Market: Dynamics

4.1. Compound Semiconductor Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Compound Semiconductor Market Drivers

4.3. Compound Semiconductor Market Restraints

4.4. Compound Semiconductor Market Opportunities

4.5. Compound Semiconductor Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factor

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Value Chain Analysis

4.10. Regulatory Landscape by Region

4.10.1. North America

4.10.2. Europe

4.10.3. Asia Pacific

4.10.4. Middle East and Africa

4.10.5. South America

5. Compound Semiconductor Market: Global Market Size and Forecast by Segmentation (by Value in USD Million) (2026-2032)

5.1. Compound Semiconductor Market Size and Forecast, by Type (2026-2032)

5.1.1. Gallium Nitride (GaN)

5.1.2. Silicon Carbide (SiC)

5.1.3. Gallium Arsenide (GaAs)

5.1.4. Indium Phosphide (InP)

5.2. Compound Semiconductor Market Size and Forecast, by Application (2026-2032)

5.2.1. Inverters

5.2.2. Power Amplifiers

5.2.3. Sensors

5.2.4. Others

5.3. Compound Semiconductor Market Size and Forecast, by End-User Industry (2026-2032)

5.3.1. Automotive

5.3.2. IT and Telecom

5.3.3. Consumer Goods Electronics

5.3.4. Industrial Manufacturing

5.3.5. Others

5.4. Compound Semiconductor Market Size and Forecast, by Region (2026-2032)

5.4.1. North America

5.4.2. Europe

5.4.3. Asia Pacific

5.4.4. Middle East and Africa

5.4.5. South America

6. North America Compound Semiconductor Market Size and Forecast by Segmentation (by Value in USD Million) (2026-2032)

6.1. North America Compound Semiconductor Market Size and Forecast, by Type (2026-2032)

6.1.1. Gallium Nitride (GaN)

6.1.2. Silicon Carbide (SiC)

6.1.3. Gallium Arsenide (GaAs)

6.1.4. Indium Phosphide (InP)

6.2. North America Compound Semiconductor Market Size and Forecast, by Application (2026-2032)

6.2.1. Inverters

6.2.2. Power Amplifiers

6.2.3. Sensors

6.2.4. Others

6.3. North America Compound Semiconductor Market Size and Forecast, by End-User Industry (2026-2032)

6.3.1. Automotive

6.3.2. IT and Telecom

6.3.3. Consumer Goods Electronics

6.3.4. Industrial Manufacturing

6.3.5. Others

6.4. North America Compound Semiconductor Market Size and Forecast, by Country (2026-2032)

6.4.1. United States

6.4.2. Canada

6.4.3. Mexico

7. Europe Compound Semiconductor Market Size and Forecast by Segmentation (by Value in USD Million) (2026-2032)

7.1. Europe Compound Semiconductor Market Size and Forecast, by Type (2026-2032)

7.2. Europe Compound Semiconductor Market Size and Forecast, by Application (2026-2032)

7.3. Europe Compound Semiconductor Market Size and Forecast, by End-User Industry (2026-2032)

7.4. Europe Compound Semiconductor Market Size and Forecast, by Country (2026-2032)

7.4.1. United Kingdom

7.4.2. France

7.4.3. Germany

7.4.4. Italy

7.4.5. Spain

7.4.6. Sweden

7.4.7. Russia

7.4.8. Rest of Europe

8. Asia Pacific Compound Semiconductor Market Size and Forecast by Segmentation (by Value in USD Million) (2026-2032)

8.1. Asia Pacific Compound Semiconductor Market Size and Forecast, by Type (2026-2032)

8.2. Asia Pacific Compound Semiconductor Market Size and Forecast, by Application (2026-2032)

8.3. Asia Pacific Compound Semiconductor Market Size and Forecast, by End-User Industry (2026-2032)

8.4. Asia Pacific Compound Semiconductor Market Size and Forecast, by Country (2026-2032)

8.4.1. China

8.4.2. India

8.4.3. Japan

8.4.4. South Korea

8.4.5. Australia

8.4.6. ASEAN

8.4.7. Rest of Asia Pacific

9. Middle East and Africa Compound Semiconductor Market Size and Forecast by Segmentation (by Value in USD Million) (2026-2032)

9.1. Middle East and Africa Compound Semiconductor Market Size and Forecast, by Type (2026-2032)

9.2. Middle East and Africa Compound Semiconductor Market Size and Forecast, by Application (2026-2032)

9.3. Middle East and Africa Compound Semiconductor Market Size and Forecast, by End-User Industry (2026-2032)

9.4. Middle East and Africa Compound Semiconductor Market Size and Forecast, by Country (2026-2032)

9.4.1. South Africa

9.4.2. GCC

9.4.3. Egypt

9.4.4. Rest of the Middle East and Africa

10. South America Compound Semiconductor Market Size and Forecast by Segmentation (by Value in USD Million) (2026-2032)

10.1. South America Compound Semiconductor Market Size and Forecast, by Type (2026-2032)

10.2. South America Compound Semiconductor Market Size and Forecast, by Application (2026-2032)

10.3. South America Compound Semiconductor Market Size and Forecast, by End-User Industry (2026-2032)

10.4. South America Compound Semiconductor Market Size and Forecast, by Country (2026-2032)

10.4.1. Brazil

10.4.2. Argentina

10.4.3. Rest Of South America

11. Company Profile: Key Players

11.1. Cree Inc. (USA)

11.1.1. Company Overview

11.1.2. Product Portfolio

11.1.2.1. Product Name

11.1.2.2. Product Details

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Freescale Semiconductor Inc. (USA)

11.3. Mining & Chemical Products Ltd. (USA)

11.4. Qorvo (USA)

11.5. Texas Instruments (USA)

11.6. Skyworks Solutions (USA)

11.7. International Quantum Epitaxy Plc. (UK)

11.8. LM Ericsson Telefon AB (Sweden)

11.9. STMicroelectronics NV (Switzerland)

11.10. Infineon Technologies AG (Germany)

11.11. Umicore Indium Products (Belgium)

11.12. NXP Semiconductor N.V. (Netherlands)

11.13. Infineon Technologies (Germany)

11.14. Taiwan Semiconductor Manufacturing Company Ltd. (Taiwan)

11.15. Renesas Electronics Corporation (Japan)

11.16. Toshiba Corporation (Japan)

11.17. Nichia Corporation (Japan)

11.18. Samsung Electronics (South Korea)

11.19. Others

12. Key Findings

13. Analyst Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook