Coffee Concentrate Market Industry Analysis and Forecast (2026-2032)

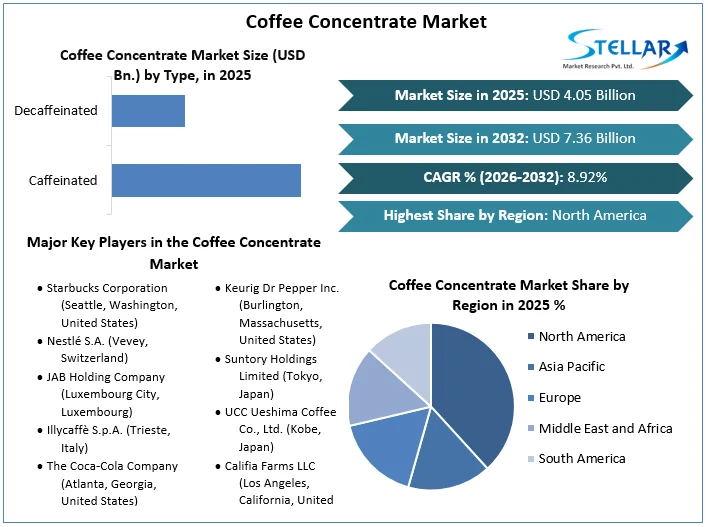

The Coffee Concentrate Market size was valued at USD 4.05 Bn. in 2025 and the total Global Paper Products revenue is expected to grow at a CAGR of 8.92% from 2026 to 2032, reaching nearly USD 7.36 Bn. by 2032.

Coffee Concentrate Market Overview

The research methodology employed in studying the Coffee Concentrate Market typically involves a combination of qualitative and quantitative approaches. Qualitative research includes comprehensive literature reviews, interviews with industry experts, and industry reports and publications analysis to understand market trends, dynamics, and challenges.

Quantitative research involves gathering and analyzing numerical data related to market size, growth rates, revenue, and other relevant metrics. This includes surveys, data mining, and statistical analysis of market data from reputable sources such as industry associations, government agencies, and market research firms. By combining these methodologies, researchers comprehensively understand the Coffee Concentrate Market, including its size, growth drivers, competitive landscape, and future outlook. This enables stakeholders to make informed decisions regarding investments, product development, marketing strategies, and more within the paper products industry.

To get more Insights: Request Free Sample Report

Coffee Concentrate Market Dynamics

The rapid increase in demand for convenient coffee options is boosting the Coffee concentrate Market.

The upgrading lifestyle and continuous routine changes drive the demand in the coffee concentrate market. The demand for rapid convenient caffeine options has been a significant driver in boosting the market demand for coffee concentrates. In a current fast-paced work environment, professionals often the coffee concentrate market is primarily driven by demand for convenient and ready-to-drink beverages. Consumers are increasingly seeking quick and easy coffee solutions that do not compromise on quality or flavor.

The rise of the on-the-go lifestyle and busy schedules has made coffee concentrates a popular choice. Also, the proliferation of specialty coffee shops and the trend of premiumization in the coffee industry in the coffee industry are further fuelling the coffee concentrate market. Innovations in cold brew and nitro coffee also contribute to the growing demand for coffee concentrate, as these beverages gain popularity for their smooth taste and lower acidity.

The shift towards health-conscious and are looking for products that offer functional benefits, such as added vitamins, antioxidants, or plant-based ingredients.

Sustainability is another significant trend, with brands focusing on eco-friendly packaging and ethically sourced coffee beans. The rise of e-commerce and direct-to-consumer sales channel has also impacted the market, allowing brands to reach a broader audience and offer subscription-based models for regular delivery of coffee concentrate.

The coffee concentrate market presents several opportunities for growth and innovation. Such as companies can capitalize on the rising trend of at-home gourmet coffee experience by offering premium and artisanal coffee shop beverages. There’s also potential in developing new flavors and variations, such as seasonal or limited-edition offerings, to attract adventurous consumers. Rising into emerging markets where coffee culture is still developing can provide substantial growth opportunities. Collaborating with health and wellness brands to create fortified or functional coffee concentrate can appeal to the health-conscious segment of consumers.

Coffee Concentrate Market Regional Analysis

The coffee Concentrate Market experienced a robust demand for convenient and high-quality coffee options in North America. With a culture that values efficiency and premium experiences, consumers in North America are increasingly turning to coffee concentrates, particularly cold brews, as a convenient yet flavourful alternative to traditional brewed coffee. Major players like Starbucks and Nestle dominate the market, offering a variety of ready-to-drink options to cater to diverse consumer preferences. The region's strong distribution infrastructure, including supermarkets, online retail, and food service channels, ensures widespread availability of coffee concentrates, further fuelling market growth.

The coffee concentrate market is facing steady growth driven by the continent's evolving coffee culture and increasing demand for specialty and premium beverages in the European Market. Consumers are embracing the trend of cold brew coffee, appreciating its smooth taste and versatility. European consumers also prioritize sustainability and ethical sourcing, leading to a rise in demand for responsibly sourced coffee concentrates. Key players like Illy and Lavazza are expanding their product offerings to meet these preferences, while local and regional brands are gaining traction by offering unique flavor profiles and niche products. Distribution channels such as supermarkets, specialty stores, and online platforms play a crucial role in making coffee concentrates accessible to European consumers.

Emerging as a dynamic and rapidly growing market for coffee concentrates, driven by urbanization, changing lifestyles, and burgeoning coffee culture in the Asian Market. Countries like Japan, South Korea, China, and India are witnessing a surge in demand for innovative and convenient coffee solutions, with cold brew coffee gaining popularity among younger demographics. International players like Suntory and Maxim are leading the market alongside local brands that cater to specific regional tastes. Convenience stores, supermarkets, and e-commerce platforms are key distribution channels in the region, capitalizing on the tech-savvy and convenience-seeking consumer base. As disposable incomes rise and coffee consumption continues to grow, the Asia Pacific coffee concentrate market presents significant opportunities for both established players and new entrants.

Coffee Concentrate Market Segment Analysis

By Type: Caffeinated coffee concentrates dominate the market, appealing to consumers seeking the familiar taste and energizing effects of traditional coffee. This segment captures a significant share of the market due to the widespread preference for caffeinated beverages among coffee enthusiasts and casual drinkers alike. On the other hand, the decaffeinated coffee concentrate segment, while smaller, is experiencing growth as consumers prioritize wellness and seek flavourful alternatives without the stimulating effects of caffeine. This segment caters to health-conscious individuals or those sensitive to caffeine, offering a satisfying coffee experience at any time of day.

By Distribution Channel :Supermarkets and hypermarkets serve as primary distribution channels for coffee concentrates, offering a diverse range of brands and packaging options to consumers during routine grocery shopping trips. Convenience stores provide quick and on-the-go options, catering to busy individuals seeking convenient refreshment solutions. Online retail platforms have witnessed rapid growth, especially with the increasing popularity of e-commerce, offering convenience and a wide variety of options delivered directly to consumers' doorsteps. Other distribution channels include specialty stores, food service channels, direct-to-consumer sales, and international markets, each catering to specific consumer preferences and market segments.

By Packaging: Coffee concentrates are packaged in various formats to meet consumer needs and usage occasions. Bottles offer convenience and portability, allowing consumers to enjoy their favourite beverages on the go. Pouch packaging provides flexibility and ease of use, particularly for single-serve or portion-controlled products. Other packaging options such as cans, cartons, and bulk containers offer unique advantages in terms of shelf-life, storage, and environmental sustainability. Each packaging format caters to different consumer preferences, ensuring that coffee concentrate products are accessible and convenient for a wide range of consumers.

By Source: Arabica coffee concentrates are favored for their smooth flavor profile and aromatic qualities, appealing to discerning coffee enthusiasts seeking a premium drinking experience. This segment commands a significant share of the market, reflecting the popularity of Arabica coffee beans globally. Robusta coffee concentrates, known for their bold flavor and higher caffeine content, cater to consumers seeking a more robust coffee taste. While representing a smaller segment, Robusta coffee concentrates offer an intense coffee experience for those who prefer it. Other sources, including blends of Arabica and Robusta beans and specialty coffee varieties, provide diverse flavor profiles to meet the varied preferences of coffee enthusiasts.

|

Coffee Concentrate Market Scope |

|

|

Market Size in 2025 |

USD 4.05 Bn. |

|

Market Size in 2032 |

USD 7.36 Bn. |

|

CAGR (2026-2032) |

8.92% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segments |

By Type Caffeinated Decaffeinated |

|

By Distribution Channel Supermarkets and Hypermarkets Convenience Stores Online Retail Platforms Others |

|

|

By Packaging Bottles Pouches Others |

|

|

By Source Arabica Robusta Others |

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Russia, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Players in the Coffee Concentrate Market

- Starbucks Corporation (Seattle, Washington, United States)

- Nestlé S.A. (Vevey, Switzerland)

- JAB Holding Company (Luxembourg City, Luxembourg)

- Illycaffè S.p.A. (Trieste, Italy)

- The Coca-Cola Company (Atlanta, Georgia, United States)

- Keurig Dr Pepper Inc. (Burlington, Massachusetts, United States)

- Suntory Holdings Limited (Tokyo, Japan)

- UCC Ueshima Coffee Co., Ltd. (Kobe, Japan)

- Califia Farms LLC (Los Angeles, California, United States)

- La Colombe Coffee Roasters (Philadelphia, Pennsylvania, United States)

- Concentric Coffee Co. (Nairobi, Kenya)

- Stumptown Coffee Roasters (Portland, Oregon, United States)

- Lucky Jack Coffee (San Francisco, California, United States)

- Secret Squirrel Cold Brew Coffee (San Diego, California, United States)

- Bizzy Coffee (Minneapolis, Minnesota, United States)

- Chameleon Cold-Brew (Austin, Texas, United States)

- High Brew Coffee (Austin, Texas, United States)

- Kohana Coffee (Austin, Texas, United States)

- Wandering Bear Coffee Co. (New York City, New York, United States)

- Others

Frequently Asked Questions

Current trends in the coffee concentrate market include the rising popularity of cold brew coffee, the introduction of innovative flavors and formulations, the expansion of distribution channels, and increased consumer interest in health-conscious and sustainable coffee products.

Some challenges facing the coffee concentrate market include intense competition from traditional brewed coffee, concerns about product quality and taste consistency, regulatory hurdles related to labeling and health claims, and environmental sustainability issues regarding packaging and production processes.

Pricing strategies in the coffee concentrate market vary based on factors such as brand positioning, product quality, packaging format, distribution channel, and regional market dynamics. Companies may adopt premium pricing for specialty and organic products, while also offering competitive pricing for mainstream offerings to capture a broader consumer base.

Significant growth is observed in North America, particularly in countries like US and Canada, as well as in Europe.

1. Coffee Concentrate Market: Research Methodology

1.1. Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market breakdown and Data Triangulation

1.4. Assumptions

2. Coffee Concentrate Market: Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026– 2032) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Coffee Concentrate Market: Competitive Landscape

3.1. Stellar Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Product Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. Product Launches and Innovation

4. Coffee Concentrate Market: Dynamics

4.1. Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Market Drivers

4.3. Market Restraints

4.4. Market Opportunities

4.5. Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factors

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Value Chain Analysis

4.10. Trade Analysis

4.10.1. Import Scenario

4.10.2. Export Scenario

4.11. Regulatory Landscape

4.11.1. Market Regulation by Region

4.11.1.1. North America

4.11.1.2. Europe

4.11.1.3. Asia Pacific

4.11.1.4. Middle East and Africa

4.11.1.5. South America

4.11.2. Impact of Regulations on Market Dynamics

4.11.3. Government Schemes and Initiatives

5. Coffee Concentrate Market Size and Forecast by Segments (by Value USD Million and Volume in Litre)

5.1. Coffee Concentrate Market Size and Forecast, By Type (2025-2032)

5.1.1. Caffeinated

5.1.2. Decaffeinated

5.2. Coffee Concentrate Market Size and Forecast, By Distribution Channel (2025-2032)

5.2.1. Supermarkets and Hypermarkets

5.2.2. Convenience Stores

5.2.3. Online Retail Platforms

5.2.4. Others

5.3. Coffee Concentrate Market Size and Forecast, By Packaging (2025-2032)

5.3.1. Bottles

5.3.2. Pouches

5.3.3. Others

5.4. Coffee Concentrate Market Size and Forecast, By Source (2025-2032)

5.4.1. Arabica

5.4.2. Robusta

5.4.3. Others

5.5. Coffee Concentrate Market Size and Forecast, by Region (2025-2032)

5.5.1. North America

5.5.2. Europe

5.5.3. Asia Pacific

5.5.4. Middle East and Africa

5.5.5. South America

6. North America Coffee Concentrate Market Size and Forecast (by Value USD Million and Volume in Litre)

6.1. North America Coffee Concentrate Market Size and Forecast, By Type (2025-2032)

6.1.1. Caffeinated

6.1.2. Decaffeinated

6.2. North America Coffee Concentrate Market Size and Forecast, By Distribution Channel (2025-2032)

6.2.1. Supermarkets and Hypermarkets

6.2.2. Convenience Stores

6.2.3. Online Retail Platforms

6.2.4. Others

6.3. North America Coffee Concentrate Market Size and Forecast, By Packaging (2025-2032)

6.3.1. Bottles

6.3.2. Pouches

6.3.3. Others

6.4. North America Coffee Concentrate Market Size and Forecast, By Source (2025-2032)

6.4.1. Arabica

6.4.2. Robusta

6.4.3. Others

6.5. North America Coffee Concentrate Market Size and Forecast, by Country (2025-2032)

6.5.1. United States

6.5.2. Canada

6.5.3. Mexico

7. Europe Coffee Concentrate Market Size and Forecast (by Value USD Million and Volume in Litre)

7.1. Europe Coffee Concentrate Market Size and Forecast, By Type (2025-2032)

7.2. Europe Coffee Concentrate Market Size and Forecast, By Distribution Channel (2025-2032)

7.3. Europe Coffee Concentrate Market Size and Forecast, By Packaging (2025-2032)

7.4. Europe Coffee Concentrate Market Size and Forecast, By Source (2025-2032)

7.5. Europe Coffee Concentrate Market Size and Forecast, by Country (2025-2032)

7.5.1. UK

7.5.2. France

7.5.3. Germany

7.5.4. Italy

7.5.5. Spain

7.5.6. Sweden

7.5.7. Austria

7.5.8. Rest of Europe

8. Asia Pacific Coffee Concentrate Market Size and Forecast (by Value USD Million and Volume in Litre)

8.1. Asia Pacific Coffee Concentrate Market Size and Forecast, By Type (2025-2032)

8.2. Asia Pacific Coffee Concentrate Market Size and Forecast, By Distribution Channel (2025-2032)

8.3. Asia Pacific Coffee Concentrate Market Size and Forecast, By Packaging (2025-2032)

8.4. Asia Pacific Coffee Concentrate Market Size and Forecast, By Source (2025-2032)

8.5. Asia Pacific Coffee Concentrate Market Size and Forecast, by Country (2025-2032)

8.5.1. China

8.5.2. S Korea

8.5.3. Japan

8.5.4. India

8.5.5. Australia

8.5.6. Indonesia

8.5.7. Malaysia

8.5.8. Vietnam

8.5.9. Taiwan

8.5.10. Bangladesh

8.5.11. Pakistan

8.5.12. Rest of Asia Pacific

9. Middle East and Africa Coffee Concentrate Market Size and Forecast (by Value USD Million and Volume in Litre)

9.1. Middle East and Africa Coffee Concentrate Market Size and Forecast, By Type (2025-2032)

9.2. Middle East and Africa Coffee Concentrate Market Size and Forecast, By Distribution Channel (2025-2032)

9.3. Middle East and Africa Coffee Concentrate Market Size and Forecast, By Packaging (2025-2032)

9.4. Middle East and Africa Coffee Concentrate Market Size and Forecast, By Source (2025-2032)

9.5. Middle East and Africa Coffee Concentrate Market Size and Forecast, by Country (2025-2032)

9.5.1. South Africa

9.5.2. GCC

9.5.3. Egypt

9.5.4. Nigeria

9.5.5. Rest of ME&A

10. South America Coffee Concentrate Market Size and Forecast (by Value USD Million and Volume in Litre)

10.1. South America Coffee Concentrate Market Size and Forecast, By Type (2025-2032)

10.2. South America Coffee Concentrate Market Size and Forecast, By Distribution Channel (2025-2032)

10.3. South America Coffee Concentrate Market Size and Forecast, By Packaging (2025-2032)

10.4. South America Coffee Concentrate Market Size and Forecast, By Source (2025-2032)

10.5. South America Coffee Concentrate Market Size and Forecast, by Country (2025-2032)

10.5.1. Brazil

10.5.2. Argentina

10.5.3. Rest of South America

11. Company Profile: Key players

11.1. Starbucks Corporation (Seattle, Washington, United States)

11.1.1. Company Overview

11.1.2. Product Portfolio

11.1.2.1. Product Name

11.1.2.2. Product Details

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Nestlé S.A. (Vevey, Switzerland)

11.3. JAB Holding Company (Luxembourg City, Luxembourg)

11.4. Illycaffè S.p.A. (Trieste, Italy)

11.5. The Coca-Cola Company (Atlanta, Georgia, United States)

11.6. Keurig Dr Pepper Inc. (Burlington, Massachusetts, United States)

11.7. Suntory Holdings Limited (Tokyo, Japan)

11.8. UCC Ueshima Coffee Co., Ltd. (Kobe, Japan)

11.9. Califia Farms LLC (Los Angeles, California, United States)

11.10. La Colombe Coffee Roasters (Philadelphia, Pennsylvania, United States)

11.11. Concentric Coffee Co. (Nairobi, Kenya)

11.12. Stumptown Coffee Roasters (Portland, Oregon, United States)

11.13. Lucky Jack Coffee (San Francisco, California, United States)

11.14. Secret Squirrel Cold Brew Coffee (San Diego, California, United States)

11.15. Bizzy Coffee (Minneapolis, Minnesota, United States)

11.16. Chameleon Cold-Brew (Austin, Texas, United States)

11.17. High Brew Coffee (Austin, Texas, United States)

11.18. Kohana Coffee (Austin, Texas, United States)

11.19. Wandering Bear Coffee Co. (New York City, New York, United States)

11.20. Others

12. Key Findings

13. Industry Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook