Canned Tuna Market Size, Share, Growth Trends, Consumer Demand Analysis, and Forecast 2026-2034

The Canned Tuna Market size is estimated at USD 21.49 Billion in 2025 and is expected to reach USD 33.06 Billion by 2034, at a CAGR of 4.9% during the forecast period (2026-2034)

Canned Tuna Market Overview:

The Global Canned Tuna Market is having stable growth, which is driven by increasing consumer demand for the convenient, affordable and protein-rich food options with longer shelf life. The market is expected to reach approximately 27.51 USD billion by 2034 displaying a compound annual growth rate of around 4.9%. Many factors are contributing to this development of canned tuna market, including, the increasing number of people concerned about their health and busy lifestyles has increased confidence in canned tuna such as ready-to-eat and ready-to-make food products that are easy and fast to make. Tuna has many nutritional benefits such as high-quality protein and a rich source of omega -3 fatty acids that also satisfy health-conscious consumers. The expansion of ecommerce and well -established retail channels improved the market facility, which in turn made the availability of canned tuna easier, resulting in an increase in canned tuna market.

Regionally, The Asia Pacific region is dominating the Canned Tuna Market due to rising seafood consumption, production and increasing disposable income. North America holds significant market share in consumption, driven By high consumption of convenient and protein-rich foods. Europe is also an important market, with Spain a major manufacturer and consumer.

Key players in the competitive canned tuna market are Thai Union Group, Bumble Bee Foods, Chicken of the Sea, and Frinsa del Noroeste. These companies focus on stability, product innovation (such as flavored tuna and convenient packaging), and focus on pricing strategies to maintain their market positions. The growing demand for plant-based options presents a possible challenge for market development; However, the power and versatility of canned tuna is expected to maintain its popularity.

Thailand is the third largest producer in the world of canned Tuna and is the largest exporter, which is an accounting for the global volume of 31% exports.

.webp)

To get more Insights: Request Free Sample Report

Canned Tuna Market Dynamics:

Rising Health Consciousness to Drive Demand for Consumer Preference of the Canned Tuna Market

Consumers are trying to find foods that are beneficial to their health, and most importantly, nutrient-dense. Due to its high protein, low-fat, and rich omega-3 content, canned tuna has also become a household name among health enthusiasts serving heart and brain inflammatory processes. In addition, people who are turning in towards high-protein, keto and Mediterranean diet often use tuna as a convenient protein supplement, which help to meet dietary goals. This demand is especially supported by time-strapped professionals and health-conscious people who want nutrient-rich meals fast.

Sustainable Sourcing Gains Momentum to Drive the Canned Tuna Market Growth

The shift towards canned tuna market products stems from increased competitiveness in the consumer market that values socio-environmental sustainability. To an extent, brands are also slowly changing their marketing strategies to meet the society’s eco-friendly standard by using pole-and-line or FAD-free fishing techniques instead of overfishing. In addition, companies are shifting from pouches to can packaging to be more environmentally friendly. Nowadays, the Marine Stewardship Council (MSC) along with Dolphin-Safe certifications gained prominence and became an essential factor in purchasing decisions. Supermarkets have begun to respond to these changes are more willing to stock their shelves with sustainably sourced tuna. Companies adopting such practices not only gain a better reputation but also outperform competitors who focus on sustainability as a primary marketing strategy.

Overfishing and Supply Chain Disruptions to Pose Challenges for the Canned Tuna Market

As the demand for canned tuna keeps increasing, the Canned Tuna industry struggles to cope with issues related to overfishing and unpredictable shifts in the supply chain. Excessive fishing through unsustainable methods has diminished the stocks of tunas which has led to the imposition of stricter fishing regulations and quotas. These in turn hike the production costs. In addition, geopolitical stress, increase in fuel prices within the supply chain and hurdles have affected the distribution of tuna globally. This disrupts manufacturers' ability to keep prices and availability stable. These obstacles create confusion for both brands and consumers and lead to unstable pricing and unseeding products in the market.

Packaging Defects and Products Miss: To Challenge Canned Tuna Market

One of the important restrictions in canned seafood industry is the risk of product recall due to packaging defects or contamination concerns. For example, in February 2025, the TRAI-Union Seafoods recalled a lot of selective tuna of canned tuna under brands such as Jenova, Van Camp, H-E-B, and Trader Joe. This memory was indicated by a manufacturing defect in the easy open bridge tab lids, which potentially compromised the product seal, leading to an increased risk of leakage or contamination with Clostridium botulinum, a life-threatening toxin.

Canned Tuna Market Regional Analysis:

The Asia-Pacific region has emerged as the fastest growing market in the global canned tuna industry, inspired by the confluence of structural and consumer-operated factors. Rapid urbanization, especially in Southeast Asian countries, has rebuilt dietary patterns to a great extent, in which more consumers move towards convenient, protein-rich and shelf-stable foods that align with their fast busy lifestyles. The change is particularly prominent in countries such as Thailand, the Philippines and Indonesia, which specifically straddles both ends of the price chain-they are not only high-development consumer markets, but also global production and export hubs. Among them, Thailand has established itself as a world leader at the canned Tuna Processing and Export, with the industry veteran Thai Union Group—the parent company of international brands like Chicken of the Sea, John West, and Sealect plays a central role in shaping the network. Along with this, Japan and South Korea, two of the most mature markets in the region, are looking at a change towards premiumization and health-conscious consumption.

In these countries, consumers are demanding low sodium, omega-3 rich, and permanent sour tuna options, which are motivated by awareness about heart health and maritime stability. The manufacturers are responding with value-added innovations such as tuna-to-east packaging, and alike with the ready-to-eat gourmet variants designed for functional ingredients, easy-to-packaging, and urban professionals and aging populations.

North America is the fastest growing region due to increased sea food consumption, especially canned tuna. North America's high consumer demand for convenient and protein-rich food options solidifies its position as a leading market for canned tuna.

Canned Tuna Market Segment Analysis:

Based on Type, the market is segmented into Skipjack Tuna, Yellowfin Tuna, Albacore Tuna, and Bluefin Tuna. Skipjack tuna leads the canned tuna market due to its affordability, slightly mild taste, and wide accessibility. It is the most frequently used variable in canned tuna products, making it a household product worldwide. Major canned tuna brands are StarKist, Bumble Bee, Chicken of the Sea use Skipjack Tuna widely. Their large-scale marketing and global supply further strengthen Skipjack as the default tuna variety for Billions of consumers.

Based on form, the market is segmented into Chunks, Flakes, and Shredded. Tuna comes in a wide range of variations, so consumers have the option to match the person who match their taste. Flakes are the most popular because they do not lose their size and texture even after being cooked, making it ideal for use in salads, sandwiches and pasta. Chunks is a more economical version of tuna. This type consists of smaller chunks of tuna, which are used in pre-cooked meals.

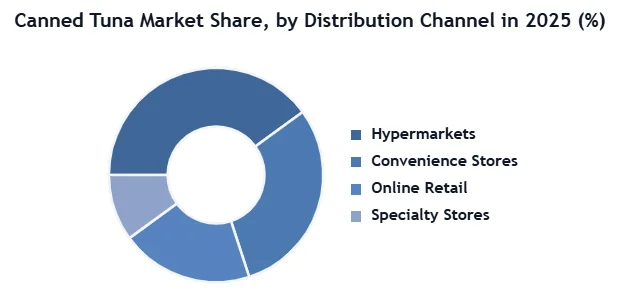

Based on Distribution Channel, Hypermarkets, Convenience Stores, Online Retail, and Specialty Stores. Hypermarkets offer most brands, bulk purchase, and regular discounts, they remain the leading channel for the distribution of canned tuna. For customers on the go, convenience stores offer small packages for quick things. Major manufacturers are promoting their products through offline retail stores such as hypermarkets & supermarkets. Moreover, several companies are opening new stores across the globe to expand their customer base. For example, Century Pacific Food, Inc. (Philippines) has extended its distribution network in China By acquiring local distributors, aiming to strengthen its presence in the Chinese market.

Competitive Landscape

Major players such as Thai Union Group, Bumble B Foods, and Starkist lead the market, while chicken of the and wild planet foods such as regional and niche brand are receiving traction by focusing on stability and product discrimination. Europe currently dominates consumption due to well-established seafood eating habits, while the Asia-Pacific region is emerging as the fastest growing market due to urbanization, disposable income and changing dietary preferences.

Skipjack Tuna continues to lead the species section due to its comprehensive availability and low cost, while Yellowfin Tuna is favored in premium product lines for its texture and milky taste. Light canned tuna, which provides a more economical option, holds the largest market share, although white tuna is rapidly being preferred by conscious consumers. There are also the trends of product innovation in the market such as petu-swas tuna, omega-3S, snack-shaped packaging, and plant-based tuna options, which are to meet consumer lifestyle and dietary needs.

With certificates such as Marine Stewardship Council (MSC), stability in the competitive landscape is a central focus, which affects consumer options. Packaging innovation-like recreational pouches and BPA-free compartment-and growing e-commerce growth are re-shaping the distribution strategies. These trends throw light on how the market players are taking advantage of environmental responsibility, health benefits and convenience to gain competitive edge. As the demand increases globally, especially in developing economies, the canned tuna industry is likely to see rapid competition, further product diversification and strategic cooperation focused on traceability and stability.

|

Canned Tuna Market Scope |

|

|

Market Size in 2025 |

USD 21.49 Billion |

|

Market Size in 2034 |

USD 33.06 Billion |

|

CAGR (2026-2034) |

4.9% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Segments |

By Type Skipjack Tuna Yellowfin Tuna Albacore Tuna Bluefin Tuna |

|

By Form Chunks Shredded |

|

|

By Distribution Channel Hypermarkets Convenience Stores Online Retail Specialty Stores |

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Russia, and Rest of Europe Asia Pacific – China, South Korea, Japan, India, Australia, Indonesia, Philippines, Malaysia, Vietnam, Thailand, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Players in the Canned Tuna Market:

North America

- StarKist Co. (USA)

- Bumble Bee Foods LLC (USA)

- Wild Planet Foods Inc. (USA)

- American Tuna Inc. (USA)

- Chicken of the Sea (USA)

Europe

- Grupo Calvo (Spain)

- Jealsa Rianxeira S.A.U. (Spain)

- Conservas Ortiz S.A. / Ortiz (Spain)

- Grupo Albacora (Spain)

- Frinsa del Noroeste S.A. (Spain)

Asia Pacific

- Thai Union Group PCL (Thailand)

- Dongwon Industries (South Korea)

- Century Pacific Food Inc. (Philippines)

- Alliance Select Foods International, Inc. (Philippines)

- PT Aneka Tuna Indonesia (Indonesia)

- FCF Fishery Co., Ltd. (Taiwan)

- Kibu Group (Singapore)

- Stehr Group (Australia)

MEA

- Oceana Group Limited (South Africa)

- Saldanha Bay Canning Company (South Africa)

- Goody (Saudi Arabia)

- Seaworld Fish Processing LLC (United Arab Emirates)

South America

- Negocios Industriales Real S.A. (NIRSA) (Ecuador)

- PINSA Group (Mexico)

Frequently Asked Questions

Market segments in the Canned Tuna Market are By Type, By Form, and By Distribution Channels.

Skipjack tuna type has the largest market share according to the Type, i.e., up to 55%.

Currently, Japan, Thailand and Philippines are leading the Canned Tuna Market.

Rising health consciousness and rising awareness about socio-environmental sustainability in market are the growth drivers of the Canned Tuna Market.

1. Canned Tuna Market Introduction

1.1. Study Assumption and Market Definition

1.2. Scope of the Study

1.3. Executive Summary

2. Global Canned Tuna Market: Competitive Landscape

2.1. Ecosystem Analysis

2.2. SMR Competition Matrix

2.3. Competitive Landscape

2.4. Key Players Benchmarking

2.4.1. Company Name

2.4.2. Business Segment

2.4.3. End-user Segment

2.4.4. Revenue (2025)

2.4.5. Company Locations

2.5. Market Structure

2.5.1. Market Leaders

2.5.2. Market Followers

2.5.3. Emerging Players

2.6. Mergers and Acquisitions Details

3. Canned Tuna Market: Dynamics

3.1. Canned Tuna Market Trends By Region

3.1.1. North America Canned Tuna Market Trends

3.1.2. Europe Canned Tuna Market Trends

3.1.3. Asia Pacific Canned Tuna Market Trends

3.1.4. Middle East and Africa Canned Tuna Market Trends

3.1.5. South America Canned Tuna Market Trends

3.2. Canned Tuna Market Dynamics

3.2.1. Global Canned Tuna Market Drivers

3.2.2. Global Canned Tuna Market Restraints

3.2.3. Global Canned Tuna Market Opportunities

3.2.4. Global Canned Tuna Market Challenges

3.3. PORTER’s Five Forces Analysis

3.4. PESTLE Analysis

3.5. Regulatory Landscape By Region

3.5.1. North America

3.5.2. Europe

3.5.3. Asia Pacific

3.5.4. Middle East and Africa

3.5.5. South America

3.6. Key Opinion Leader Analysis for Canned Tuna Industry

4. Canned Tuna Market: Global Market Size and Forecast By Segmentation (By Value in USD Billion) (2026-2034)

4.1. Canned Tuna Market Size and Forecast, By Type (2026-2034)

4.1.1. Skipjack Tuna

4.1.2. Yellowfin Tuna

4.1.3. Albacore Tuna

4.1.4. Bluefin Tuna

4.2. Canned Tuna Market Size and Forecast, By Form (2026-2034)

4.2.1. Chunks

4.2.2. Flakes

4.2.3. Shredded

4.3. Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

4.3.1. Hypermarkets

4.3.2. Convenience Stores

4.3.3. Online Retail

4.3.4. Specialty Stores

4.4. Canned Tuna Market Size and Forecast, By Region (2026-2034)

4.4.1. North America

4.4.2. Europe

4.4.3. Asia Pacific

4.4.4. Middle East and Africa

4.4.5. South America

5. North America Canned Tuna Market Size and Forecast by Segmentation (By Value in USD Billion) (2026-2034)

5.1. North America Canned Tuna Market Size and Forecast, By Type (2026-2034)

5.1.1. Skipjack Tuna

5.1.2. Yellowfin Tuna

5.1.3. Albacore Tuna

5.1.4. Bluefin Tuna

5.2. North America Canned Tuna Market Size and Forecast, By Form (2026-2034)

5.2.1. Chunks

5.2.2. Flakes

5.2.3. Shredded

5.3. Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

5.3.1. Hypermarkets

5.3.2. Convenience Stores

5.3.3. Online Retail

5.3.4. Specialty Stores

5.4. North America Canned Tuna Market Size and Forecast, By Country (2026-2034)

5.4.1. United States

5.4.1.1. United States Canned Tuna Market Size and Forecast, By Type (2026-2034)

5.4.1.1.1. Skipjack Tuna

5.4.1.1.2. Yellowfin Tuna

5.4.1.1.3. Albacore Tuna

5.4.1.1.4. Bluefin Tuna

5.4.1.2. United States Canned Tuna Market Size and Forecast, By Form (2026-2034)

5.4.1.2.1. Chunks

5.4.1.2.2. Flakes

5.4.1.2.3. Shredded

5.4.1.3. Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

5.4.1.3.1. Hypermarkets

5.4.1.3.2. Convenience Stores

5.4.1.3.3. Online Retail

5.4.1.3.4. Specialty Stores

5.4.2. Canada

5.4.2.1. Canada Canned Tuna Market Size and Forecast, By Type (2026-2034)

5.4.2.1.1. Skipjack Tuna

5.4.2.1.2. Yellowfin Tuna

5.4.2.1.3. Albacore Tuna

5.4.2.1.4. Bluefin Tuna

5.4.2.2. Canada Canned Tuna Market Size and Forecast, By Form (2026-2034)

5.4.2.2.1. Chunks

5.4.2.2.2. Flakes

5.4.2.2.3. Shredded

5.4.2.3. Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

5.4.2.3.1. Hypermarkets

5.4.2.3.2. Convenience Stores

5.4.2.3.3. Online Retail

5.4.2.3.4. Specialty Stores

5.4.3. Mexico

5.4.3.1. Mexico Canned Tuna Market Size and Forecast, By Type (2026-2034)

5.4.3.1.1. Skipjack Tuna

5.4.3.1.2. Yellowfin Tuna

5.4.3.1.3. Albacore Tuna

5.4.3.1.4. Bluefin Tuna

5.4.3.2. Mexico Canned Tuna Market Size and Forecast, By Form (2026-2034)

5.4.3.2.1. Chunks

5.4.3.2.2. Flakes

5.4.3.2.3. Shredded

5.4.3.3. Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

5.4.3.3.1. Hypermarkets

5.4.3.3.2. Convenience Stores

5.4.3.3.3. Online Retail

5.4.3.3.4. Specialty Stores

6. Europe Canned Tuna Market Size and Forecast By Segmentation (By Value in USD Billion) (2026-2034)

6.1. Europe Canned Tuna Market Size and Forecast, By Type (2026-2034)

6.2. Europe Canned Tuna Market Size and Forecast, By Form (2026-2034)

6.3. Europe Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

6.3.1. United Kingdom

6.3.1.1. United Kingdom Canned Tuna Market Size and Forecast, By Type (2026-2034)

6.3.1.2. United Kingdom Canned Tuna Market Size and Forecast, By Form (2026-2034)

6.3.1.3. United Kingdom Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

6.3.2. France

6.3.2.1. France Canned Tuna Market Size and Forecast, By Type (2026-2034)

6.3.2.2. France Canned Tuna Market Size and Forecast, By Form (2026-2034)

6.3.2.3. France Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

6.3.3. Germany

6.3.3.1. Germany Canned Tuna Market Size and Forecast, By Type (2026-2034)

6.3.3.2. Germany Canned Tuna Market Size and Forecast, By Form (2026-2034)

6.3.3.3. Germany Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

6.3.4. Italy

6.3.4.1. Italy Canned Tuna Market Size and Forecast, By Type (2026-2034)

6.3.4.2. Italy Canned Tuna Market Size and Forecast, By Form (2026-2034)

6.3.4.3. Italy Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

6.3.5. Spain

6.3.5.1. Spain Canned Tuna Market Size and Forecast, By Type (2026-2034)

6.3.5.2. Spain Canned Tuna Market Size and Forecast, By Form (2026-2034)

6.3.5.3. Spain Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

6.3.6. Sweden

6.3.6.1. Sweden Canned Tuna Market Size and Forecast, By Type (2026-2034)

6.3.6.2. Sweden Canned Tuna Market Size and Forecast, By Form (2026-2034)

6.3.6.3. Sweden Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

6.3.7. Austria

6.3.7.1. Austria Canned Tuna Market Size and Forecast, By Type (2026-2034)

6.3.7.2. Austria Canned Tuna Market Size and Forecast, By Form (2026-2034)

6.3.7.3. Austria Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

6.3.8. Rest of Europe

6.3.8.1. Rest of Europe Canned Tuna Market Size and Forecast, By Type (2026-2034)

6.3.8.2. Rest of Europe Canned Tuna Market Size and Forecast, By Form (2026-2034)

6.3.8.3. Rest of Europe Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

7. Asia Pacific Canned Tuna Market Size and Forecast By Segmentation (By Value in USD Billion) (2026-2034)

7.1. Asia Pacific Canned Tuna Market Size and Forecast, By Type (2026-2034)

7.2. Asia Pacific Canned Tuna Market Size and Forecast, By Form (2026-2034)

7.3. Asia Pacific Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

7.4. Asia Pacific Canned Tuna Market Size and Forecast, By Country (2026-2034)

7.4.1. China

7.4.1.1. China Canned Tuna Market Size and Forecast, By Type (2026-2034)

7.4.1.2. China Canned Tuna Market Size and Forecast, By Form (2026-2034)

7.4.1.3. China Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

7.4.2. S Korea

7.4.2.1. S Korea Canned Tuna Market Size and Forecast, By Type (2026-2034)

7.4.2.2. S Korea Canned Tuna Market Size and Forecast, By Form (2026-2034)

7.4.2.3. S Korea Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

7.4.3. Japan

7.4.3.1. Japan Canned Tuna Market Size and Forecast, By Type (2026-2034)

7.4.3.2. Japan Canned Tuna Market Size and Forecast, By Form (2026-2034)

7.4.3.3. Japan Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

7.4.4. India

7.4.4.1. India Canned Tuna Market Size and Forecast, By Type (2026-2034)

7.4.4.2. India Canned Tuna Market Size and Forecast, By Form (2026-2034)

7.4.4.3. India Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

7.4.5. Australia

7.4.5.1. Australia Canned Tuna Market Size and Forecast, By Type (2026-2034)

7.4.5.2. Australia Canned Tuna Market Size and Forecast, By Form (2026-2034)

7.4.5.3. Australia Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

7.4.6. Indonesia

7.4.6.1. Indonesia Canned Tuna Market Size and Forecast, By Type (2026-2034)

7.4.6.2. Indonesia Canned Tuna Market Size and Forecast, By Form (2026-2034)

7.4.6.3. Indonesia Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

7.4.7. Philippines

7.4.7.1. Philippines Spatial Computing Market Size and Forecast, By Type (2025-2032)

7.4.7.2. Philippines Spatial Computing Market Size and Forecast, By Form (2025-2032)

7.4.7.3. Philippines Spatial Computing Market Size and Forecast, By Distribution Channel (2025-2032)

7.4.8. Malaysia

7.4.8.1. Malaysia Canned Tuna Market Size and Forecast, By Type (2026-2034)

7.4.8.2. Malaysia Canned Tuna Market Size and Forecast, By Form (2026-2034)

7.4.8.3. Malaysia Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

7.4.9. Vietnam

7.4.9.1. Vietnam Canned Tuna Market Size and Forecast, By Type (2026-2034)

7.4.9.2. Vietnam Canned Tuna Market Size and Forecast, By Form (2026-2034)

7.4.9.3. Vietnam Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

7.4.10. Thailand

7.4.10.1. Thailand Canned Tuna Market Size and Forecast, By Type (2026-2034)

7.4.10.2. Thailand Canned Tuna Market Size and Forecast, By Form (2026-2034)

7.4.10.3. Thailand Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

7.4.11. Rest of Asia Pacific

7.4.11.1. Rest of Asia Pacific Canned Tuna Market Size and Forecast, By Type (2026-2034)

7.4.11.2. Rest of Asia Pacific Canned Tuna Market Size and Forecast, By Form (2026-2034)

7.4.11.3. Rest of Asia Pacific Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

8. Middle East and Africa Canned Tuna Market Size and Forecast By Segmentation (By Value in USD Billion) (2026-2034)

8.1. Middle East and Africa Canned Tuna Market Size and Forecast, By Type (2026-2034)

8.2. Middle East and Africa Canned Tuna Market Size and Forecast, By Form (2026-2034)

8.3. Middle East and Africa Canned Tuna Market Size and Forecast, By Country (2026-2034)

8.4. Middle East and Africa Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

8.5. Middle East and Africa Canned Tuna Market Size and Forecast, By Country (2026-2034)

8.5.1. South Africa

8.5.1.1. South Africa Canned Tuna Market Size and Forecast, By Type (2026-2034)

8.5.1.2. South Africa Canned Tuna Market Size and Forecast, By Form (2026-2034)

8.5.1.3. South Africa Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

8.5.2. GCC

8.5.2.1. GCC Canned Tuna Market Size and Forecast, By Type (2026-2034)

8.5.2.2. GCC Canned Tuna Market Size and Forecast, By Form (2026-2034)

8.5.2.3. GCC Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

8.5.3. Nigeria

8.5.3.1. Nigeria Canned Tuna Market Size and Forecast, By Type (2026-2034)

8.5.3.2. Nigeria Canned Tuna Market Size and Forecast, By Form (2026-2034)

8.5.3.3. Nigeria Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

8.5.4. Rest of ME&A

8.5.4.1. Rest of ME&A Canned Tuna Market Size and Forecast, By Type (2026-2034)

8.5.4.2. Rest of ME&A Canned Tuna Market Size and Forecast, By Form (2026-2034)

8.5.4.3. Rest of ME&A Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

9. South America Canned Tuna Market Size and Forecast By Segmentation (By Value in USD Billion) (2026-2034)

9.1. South America Canned Tuna Market Size and Forecast, By Type (2026-2034)

9.2. South America Canned Tuna Market Size and Forecast, By Form (2026-2034)

9.3. South America Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

9.4. South America Canned Tuna Market Size and Forecast, By Country (2026-2034)

9.4.1. Brazil

9.4.1.1. Brazil Canned Tuna Market Size and Forecast, By Type (2026-2034)

9.4.1.2. Brazil Canned Tuna Market Size and Forecast, By Form (2026-2034)

9.4.1.3. Brazil Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

9.4.2. Argentina

9.4.2.1. Argentina Canned Tuna Market Size and Forecast, By Type (2026-2034)

9.4.2.2. Argentina Canned Tuna Market Size and Forecast, By Form (2026-2034)

9.4.2.3. Argentina Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

9.4.3. Rest Of South America

9.4.3.1. Rest Of South America Canned Tuna Market Size and Forecast, By Type (2026-2034)

9.4.3.2. Rest Of South America Canned Tuna Market Size and Forecast, By Form (2026-2034)

9.4.3.3. Rest Of South America Canned Tuna Market Size and Forecast, By Distribution Channel (2026-2034)

10. Company Profile: Key Players

10.1. Thai Union Group PCL (Thailand)

10.1.1. Company Overview

10.1.2. Business Portfolio

10.1.3. Financial Overview

10.1.4. SWOT Analysis

10.1.5. Strategic Analysis

10.1.6. Recent Developments

10.2. StarKist Co. (USA)

10.3. Bumble Bee Foods LLC (USA)

10.4. Century Pacific Food Inc. (Philippines)

10.5. Grupo Calvo (Spain)

10.6. Jealsa Rianxeira S.A.U. (Spain)

10.7. Ocean Brands GP (Canada)

10.8. Wild Planet Foods Inc. (USA)

10.9. American Tuna Inc. (USA)

10.10. Bolton Group (Italy)

10.11. Dongwon Industries (South Korea)

10.12. Conservas Ortiz S.A. (Spain)

10.13. Grupo Albacora (Spain)

10.14. Chicken of the Sea (USA)

10.15. Safe Catch (USA)

10.16. Frinsa del Noroeste S.A. (Spain)

10.17. PT Aneka Tuna Indonesia (Indonesia)

10.18. Alliance Select Foods International, Inc. (Philippines)

10.19. Genova (USA)

10.20. Crown Prince, Inc. (USA)

10.21. Natural Sea (USA)

10.22. Trader Joe's (USA)

10.23. Blue Harbor Fish Co. (USA)

10.24. Tonnino (Costa Rica)

10.25. Ortiz (Spain)

10.26. Good & Gather (Target Corporation) (USA)

10.27. 365 By Whole Foods Market (USA)ZF Friedrichshafen AG (Germany)

11. Key Findings

12. Analyst Recommendations

13. Canned Tuna Market: Research Methodology