Bread Market: Global Industry Analysis and Forecast (2026-2034) by Product Type, Ingredient and Region

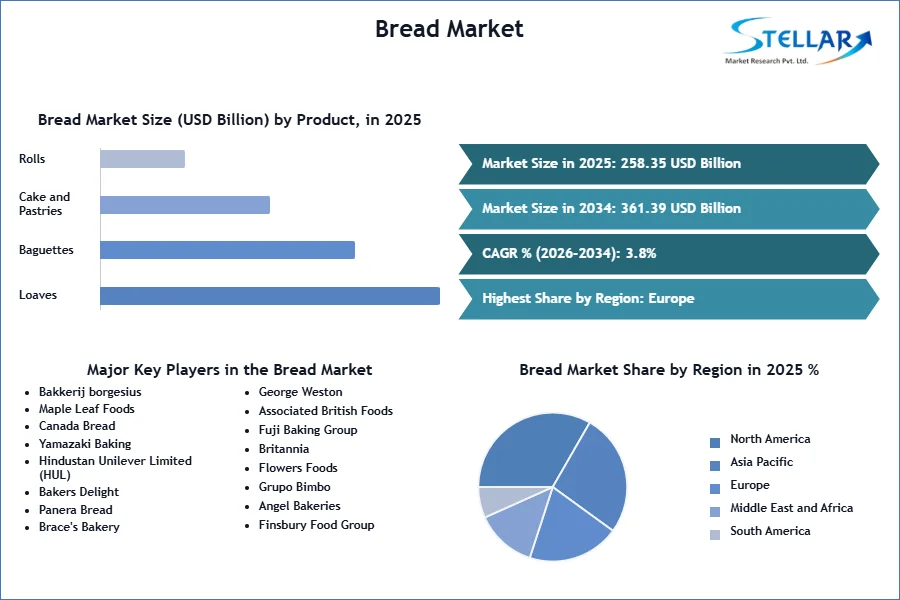

Global Bread Market size was valued at USD 258.35 Bn. in 2025 and is expected to reach USD 361.39 Bn. by 2034, at a CAGR of 3.8%.

Bread Market Overview

Bread is a staple food that was consumed by 80% of the world’s population in 2025. Key growth factors include a rising population and increasing demand for healthier, and more nutritious bread options like whole grain and gluten-free varieties. Innovation in the bakery industry, such as new specialty breads, is also driving bread market expansion. Geographically, Europe is the largest bread market, while Italy is the most bread-consuming country with 199.6kg per capita per year.

Manufacturers have adapted their product lines to align with changing consumer tastes and declining sales in key segments. Bread, a staple, now includes whole grain, multigrain, sprouted, gluten-free, and low-carb options. Desserts feature reduced sugar and fat content, whole grains, and naturally sourced ingredients, with diabetic-friendly options available. Major players in the global bread market include Maple Leaf Foods, George Weston, Fuji Baking Group, and Angel Bakeries. The bread market is relatively fragmented, with low market concentration.

To get more Insights: Request Free Sample Report

Bread Market Dynamics

Changing Consumer Preferences and Lifestyles Drive Demand for Innovative Bread Market

Changing consumer habits, busy lifestyles, and a desire for healthier options are driving increased demand for the bread market. Key factors include: Shifting consumer preferences towards more convenient, ready-to-eat bakery products due to busy lifestyles. Growing interest in healthier bread options made with low-carb, high-fiber, multi-vitamin, fortified, high antioxidant, and omega-3 ingredients among health-conscious consumers Rising demand for clean-label, gluten-free, and sodium-reduced breads High demand for breads made with whole wheat, multi-grains, and free from salt, gluten, and trans-fats.

To meet this demand, manufacturers are innovating to improve shelf life and texture using enzymes and adopting new production techniques like frozen dough, and packaged and par-baked products. This allows them to decrease waste and increase sales by providing breads with longer shelf life.

Lack of skilled personnel is the major challenge in the bread market.

The Bread market is facing a significant challenge in finding and retaining qualified personnel. The production of high-quality baked goods requires specialized technical skills and expertise, but many bakery workers are hired without prior experience and receive limited training. By 2025, the U.S. manufacturing sector is projected to create nearly 3.5 million job openings, but a significant skills gap is anticipated to leave approximately 2 million of these positions unfilled.

Meanwhile, the bakery production workforce has seen a decline from around 85,000 to 75,000 workers between 2020 and 2025. Notably, 65% of bakeries employ fewer than ten people, while only 1.2% have 500 or more employees, highlighting the industry's dominance by small to medium-sized bakeries. Additionally, talented young individuals often prefer pursuing university or professional careers that offer higher salaries and growth opportunities, creating a workforce gap.

Bread Market Segment Analysis

By Product Type, the cake and pastries segment is the fastest-growing segment in the bread market in 2024. This growth is driven by the high demand for customized cakes and pastries, which are rich in cream, taste, flavor, and nutrition. These products are particularly popular for celebrations such as parties and birthdays. The high cost of cakes and pastries compared to regular bread does not deter customers, who are attracted by the wide range of choices, customization options, and the ability to order online. This trend fuels revenue growth for the segment and the industry as a whole.

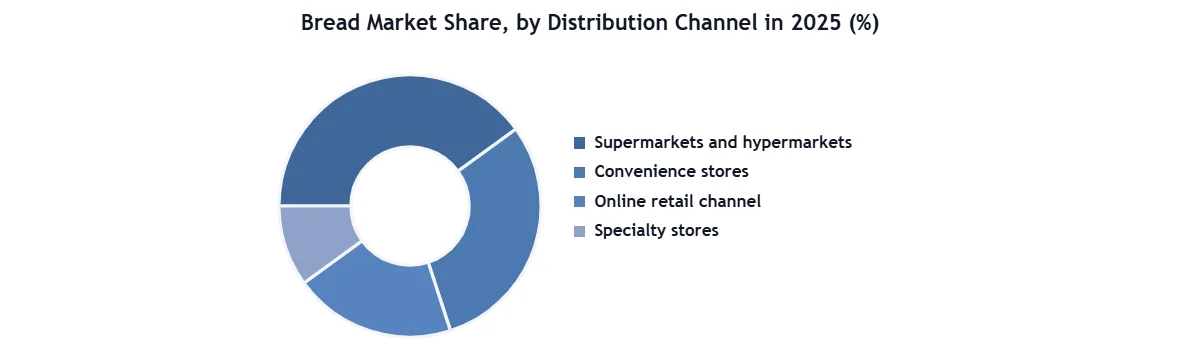

By Distribution Channels, The bread market distribution channel is dominated by supermarkets and hypermarkets, which account for XX% of the market share in 2024. Supermarkets and hypermarket channels offer a wide variety of bread products, including private label and own-brand offerings, and benefit from substantial production volumes, although this comes at the expense of narrower profit margins.

Other significant segments include convenience stores, which cater to the needs of busy consumers; the catering segment, which accounts for around XX% of the market and is driven by individually packaged pre-cooked bread; the hotels and restaurants segment, which accounts for XX% of the market and is driven by the popularity of continental breakfasts featuring baking industry products; as well as specialty stores, online retail, bake-off outlets and franchised sales points, variety stores, and other distribution channels, each playing important roles in meeting the diverse needs and preferences of bread consumers across different geographic locations and consumer behaviors.

Bread Market Regional Insights, Europe continues to dominate the global bread market. The region's large aging population is driving increased demand for healthier bakery products, supporting market growth. Key trends in the European bread market include rising demand for quality bread from local and specialty bakeries, new business models and innovations, sustainable labeling and packaging, and the adoption of organic bread.

Consumers in Europe are increasingly preferring value-added, ethnic, fresh, and artisanal bread, which is the primary factor driving sales. However, the bread market in Europe has been impacted by the Russia-Ukraine war, as European countries imported raw materials from these regions. As a result, the average price of bread across Europe was XX.X% higher in August 2025 compared to August 2024.

- Italy has a rich and strong tradition in bakery products, with over 350 different types of bread developed across the country's 20 regions. Italy is the most bread-consuming country with 199.6kg per capita per year, indicating a strong preference for traditional bread in their daily diet.

The report aims to provide industry stakeholders with a thorough study of the global bread market. The research presents the industry's historical and present state together with projected market size and trends, analyzing complex data in an easy-to-read manner. The research includes PORTER and PESTEL analyses along with the possible effects of bread market microeconomic factors. The analysis of both internal and external elements that could have a good or negative impact on the firm will provide decision-makers with a clear picture of the industry's future. By understanding the market segments and projecting the size of the global bread market, the reports also help in understanding the market's dynamics and structure.

Bread Market Scope

|

Bread Market |

|

|

Market Size in 2025 |

USD 258.35 Bn. |

|

Market Size in 2034 |

USD 361.39 Bn. |

|

CAGR (2026-2034) |

3.8% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Bread Market Segments |

By Product Type Loaves Baguettes Cake and Pastries Rolls Burger buns Sandwich slices Ciabatta Frozen bread Other |

|

By Ingredient White bread Whole wheat bread Multigrain bread Artisanal bread |

|

|

By Nutritional Value High-fiber bread Low-carb bread Gluten-free bread Functional bread Other nutritional values |

|

|

By Distribution Channel Supermarkets and hypermarkets Convenience stores Online retail channel Specialty stores |

|

|

Regional Scope |

North America (United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Russia, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa (South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Bread Market Key players

- Bakkerij borgesius

- Maple Leaf Foods,

- Canada Bread,

- Yamazaki Baking

- Hindustan Unilever Limited (HUL)

- Bakers Delight

- Panera Bread

- Brace's Bakery

- George Weston

- Associated British Foods

- Fuji Baking Group

- Britannia

- Flowers Foods

- Grupo Bimbo

- Angel Bakeries

- Finsbury Food Group

Frequently Asked Questions

Europe is expected to dominate the Bread Market during the forecast period.

The Bread Market size is expected to reach USD 361.39 Billion by 2034.

The major top players in the Global Bread Market include Maple Leaf Foods, George Weston, Fuji Baking Group, Angel Bakeries, and others.

Increasing demand for gluten-free bread and consumer preference towards healthier lifestyles is expected to drive market growth during the forecast period.

1. Research Methodology

1.1 Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Research Assumption

2. Bread Market: Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026 – 2034) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Global Bread Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Product Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

4. Bread Market: Dynamics

4.1. Bread Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Bread Market Drivers

4.3. Bread Market Restraints

4.4. Bread Market Opportunities

4.5. Bread Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factor

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Value Chain Analysis

4.10. Regulatory Landscape

4.10.1. Market Regulation by Region

4.10.1.1. North America

4.10.1.2. Europe

4.10.1.3. Asia Pacific

4.10.1.4. Middle East and Africa

4.10.1.5. South America

4.10.2. Impact of Regulations on Market Dynamics

4.10.3. Government Schemes and Initiatives

5. Bread Market: Global Market Size and Forecast by Segmentation (by Value in USD Billion and Volume in Kilogram) (2026-2034)

5.1. Bread Market Size and Forecast, by Product Type (2026-2034)

5.1.1. Loaves

5.1.2. Baguettes

5.1.3. Cake and Pastries

5.1.4. Rolls

5.1.5. Burger buns

5.1.6. Sandwich slices

5.1.7. Ciabatta

5.1.8. Frozen bread

5.1.9. Other

5.2. Bread Market Size and Forecast, by Ingredient (2026-2034)

5.2.1. White bread

5.2.2. Whole wheat bread

5.2.3. Multigrain bread

5.2.4. Artisanal bread

5.3. Bread Market Size and Forecast, by Nutritional Value (2026-2034)

5.3.1. High-fiber bread

5.3.2. Low-carb bread

5.3.3. Gluten-free bread

5.3.4. Functional bread

5.3.5. Other nutritional values

5.4. Bread Market Size and Forecast, by Distribution Channel (2026-2034)

5.4.1. Supermarkets and hypermarkets

5.4.2. Convenience stores

5.4.3. Online retail channel

5.4.4. Specialty stores

5.5. Bread Market Size and Forecast, by Region (2026-2034)

5.5.1. North America

5.5.2. Europe

5.5.3. Asia Pacific

5.5.4. Middle East and Africa

5.5.5. South America

6. North America Bread Market Size and Forecast by Segmentation (by Value in USD Billion and Volume in Kilogram) (2026-2034)

6.1. North America Bread Market Size and Forecast, by Product Type (2026-2034)

6.1.1. Loaves

6.1.2. Baguettes

6.1.3. Cake and Pastries

6.1.4. Rolls

6.1.5. Burger buns

6.1.6. Sandwich slices

6.1.7. Ciabatta

6.1.8. Frozen bread

6.1.9. Other

6.2. North America Bread Market Size and Forecast, by Ingredient (2026-2034)

6.2.1. White bread

6.2.2. Whole wheat bread

6.2.3. Multigrain bread

6.2.4. Artisanal bread

6.3. North America Bread Market Size and Forecast, by Nutritional Value (2026-2034)

6.3.1. High-fiber bread

6.3.2. Low-carb bread

6.3.3. Gluten-free bread

6.3.4. Functional bread

6.3.5. Other nutritional values

6.4. North America Bread Market Size and Forecast, by Distribution Channel (2026-2034)

6.4.1. Supermarkets and hypermarkets

6.4.2. Convenience stores

6.4.3. Online retail channel

6.4.4. Specialty stores

6.5. North America Bread Market Size and Forecast, by Country (2026-2034)

6.5.1. United States

6.5.2. Canada

6.5.3. Mexico

7. Europe Bread Market Size and Forecast by Segmentation (by Value in USD Billion and Volume in Kilogram) (2026-2034)

7.1. Europe Bread Market Size and Forecast, by Product Type (2026-2034)

7.2. Europe Bread Market Size and Forecast, by Ingredient (2026-2034)

7.3. Europe Bread Market Size and Forecast, by Nutritional Value (2026-2034)

7.4. Europe Bread Market Size and Forecast, by Distribution Channel (2026-2034)

7.5. Europe Bread Market Size and Forecast, by Country (2026-2034)

7.5.1. United Kingdom

7.5.2. France

7.5.3. Germany

7.5.4. Italy

7.5.5. Spain

7.5.6. Sweden

7.5.7. Russia

7.5.8. Rest of Europe

8. Asia Pacific Bread Market Size and Forecast by Segmentation (by Value in USD Billion and Volume in Kilogram) (2026-2034)

8.1. Asia Pacific Bread Market Size and Forecast, by Product Type (2026-2034)

8.2. Asia Pacific Bread Market Size and Forecast, by Ingredient (2026-2034)

8.3. Asia Pacific Bread Market Size and Forecast, by Nutritional Value (2026-2034)

8.4. Asia Pacific Bread Market Size and Forecast, by Distribution Channel (2026-2034)

8.5. Asia Pacific Bread Market Size and Forecast, by Country (2026-2034)

8.5.1. China

8.5.2. India

8.5.3. Japan

8.5.4. South Korea

8.5.5. Australia

8.5.6. ASEAN

8.5.7. Rest of Asia Pacific

9. Middle East and Africa Bread Market Size and Forecast by Segmentation (by Value in USD Billion and Volume in Kilogram) (2026-2034)

9.1. Middle East and Africa Bread Market Size and Forecast, by Product Type (2026-2034)

9.2. Middle East and Africa Bread Market Size and Forecast, by Ingredient (2026-2034)

9.3. Middle East and Africa Bread Market Size and Forecast, by Nutritional Value (2026-2034)

9.4. Middle East and Africa Bread Market Size and Forecast, by Distribution Channel (2026-2034)

9.5. Middle East and Africa Bread Market Size and Forecast, by Country (2026-2034)

9.5.1. South Africa

9.5.2. GCC

9.5.3. Egypt

9.5.4. Rest of the Middle East and Africa

10. South America Bread Market Size and Forecast by Segmentation (by Value in USD Billion and Volume in Kilogram) (2026-2034)

10.1. South America Bread Market Size and Forecast, by Product Type (2026-2034)

10.2. South America Bread Market Size and Forecast, by Ingredient (2026-2034)

10.3. South America Bread Market Size and Forecast, by Nutritional Value (2026-2034)

10.4. South America Bread Market Size and Forecast, by Distribution Channel (2026-2034)

10.5. South America Bread Market Size and Forecast, by Country (2026-2034)

10.5.1. Brazil

10.5.2. Argentina

10.5.3. Rest Of South America

11. Company Profile: Key Players

11.1. Bakkerij borgesius

11.1.1. Company Overview

11.1.2. Product Portfolio

11.1.2.1. Product Name

11.1.2.2. Product Details (Price, Features, etc.)

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Maple Leaf Foods,

11.3. Canada Bread,

11.4. Yamazaki Baking

11.5. Hindustan Unilever Limited (HUL)

11.6. Bakers Delight

11.7. Panera Bread

11.8. Brace's Bakery

11.9. George Weston

11.10. Associated British Foods

11.11. Fuji Baking Group

11.12. Britannia

11.13. Flowers Foods

11.14. Grupo Bimbo

11.15. Angel Bakeries

11.16. Finsbury Food Group

12. Key Findings

13. Analyst Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook