Bread Flour Market Global Industry Analysis and Forecast (2026-2032)

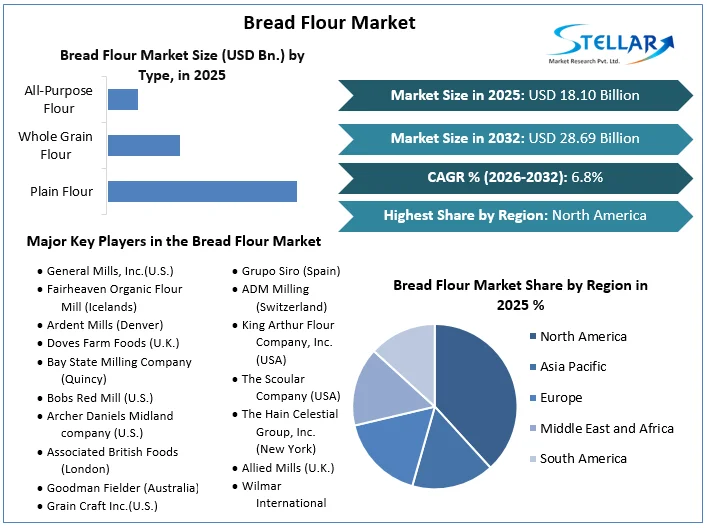

The Bread Flour Market size was valued at USD 18.10 Bn. in 2025 and the total Global Bread Flour revenue is expected to grow at a CAGR of 6.8% from 2026 to 2032, reaching nearly USD 28.69 Bn. by 2032.

Bread Flour Market Overview

Bread flour is a type of flour that is specifically formulated and milled for baking bread. It has a higher protein content, typically ranging from 11.5% to 13.5%, compared to all-purpose flour, which usually contains around 10-12% protein. Bread flour contains higher protein because of more gluten-forming proteins, essential for a strong gluten network in bread dough. The demand for convenience food from emerging countries because of hectic lifestyles, rapid urbanization, and rising disposable income driving the growth of the global bread flour market.

The Global Bread Flour Market research report contains historical data, current market trends, product consumption, environmental factors, technological innovation forecasts, upcoming technologies, and technical progress in the related industry. It categorizes the global data by manufacturer, region, type, and application. Additionally, the report analyzes market status, market share, growth rate, future trends, drivers, opportunities, challenges, risks, entry barriers, sales channels, and distributors. The report also outlines the potential of the Bread Flour market. It combines extensive quantitative analysis and exhaustive qualitative analysis, providing a deep insight into the Bread Flour market, covering all its essential aspects, from macro-overview to micro details of segment markets by type, application, and region.

- According to SMR, in North America, the United States accounts for the highest growth due to increased consumption of bread products.

- According to SMR, consumers in the United States consumed approximately 6.76 million kilograms of bread and bread rolls in 2023.

To get more Insights: Request Free Sample Report

Bread Flour Market Dynamics

Rising disposable incomes with increasing demand for bakery products

The rise in demand for ready-to-eat products is identified as one of the primary growth factors for this market. Ready-to-eat products are gaining wide popularity among consumers as they save time and effort and provide consistency in taste. The hectic lifestyles of consumers, the rising demand for convenience in food preparation, and the growing disposable incomes have increased the demand for ready-to-eat products. So, the increased number of working women across the globe also boosts the demand for ready meals driving the demand for bread flour in the market during the forecast period.

Increased disposable incomes, particularly in emerging economies, allow consumers to spend more on premium food products, including high-quality bread and specialty baked goods. This economic factor is crucial in driving the growth of the bread flour market. The global appetite for bakery items, including bread, pastries, and other baked goods, is a significant driver. This demand is spurred by changing dietary habits and the popularity of convenience foods. The development of the bakery industry directly boosts the need for bread flour. A rising global population increases the demand for staple foods, including bread. This demographic trend ensures a steady and growing market for bread flour as a key ingredient in daily diets. Consumers are willing to pay more for premium bread flour brands or products with specific attributes, such as organic or locally sourced flour, driving the growth of the bread flour market.

Rising raw material Costs

Bread flour is primarily made from wheat also fluctuations in wheat prices because of factors like weather conditions, crop yields, and trade policies, fluctuations in commodity prices put pressure on profit margins for bread flour manufacturers that affect the productivity and pricing of bread flour, restraining market growth.

There has been an increasing awareness and concern about the potential health risks associated with a high-gluten diet, such as gluten intolerance, celiac disease, and other digestive issues. This has led some consumers to reduce their consumption of bread and bakery products made with bread flour. Changing consumer preferences, such as increased demand for organic and gluten-free products, require companies to adapt quickly. It leads to increased production costs and the need for new product development, usually not possible for manufacturers.

Bread Flour Market Trends

The bread flour market is experiencing significant changes owing to shifting consumer preferences and dietary choices. Product offerings are evolving in response to health-conscious trends such as the demand for whole grain and gluten-free options. Additionally, sustainability concerns and the rise of artisanal baking methods are shaping the market's direction, prompting innovation and diversification in bread flour products. The increasing preference for clean-label products with transparent and simple ingredient lists driving the demand for organic bread flour. Consumers seeking minimally processed and additive-free products, extending to organic baking ingredients, including bread flour.

Bread Flour Market Segment Analysis

Based on the Type, the All-purpose Flour segment held the largest market share of about 53.1% in the Bread Flour Market in 2025. According to the SMR analysis, the segment is expected to grow at a CAGR of 6.8 % during the forecast period and maintain its dominance till 2032. All-purpose flour is highly versatile and used for a wide range of baking applications, including bread, pastries, cakes, cookies, and more. It is a popular choice among home bakers, commercial bakeries, and food service establishments, contributing to its large market share.

Compared to Other flours like Plain flour or whole wheat flour, all-purpose flour is generally more affordable and readily available, making it an economical choice for many consumers and businesses. Bread flour consumption occurs at the household level, where all-purpose flour is the preferred choice for everyday baking needs, such as making sandwich bread, dinner rolls, pizza dough, and various other bread varieties. In Commercial Bakeries the artisan bread makers prefer to use all-purpose flour, which driving the growth of the Bread Flour market

Bread Flour Market Regional Analysis

North America has dominated the Bread Flour Market, which held the largest market share accounting for 46.80% in 2025, the region is expected to grow during the forecast period and maintain its dominance by 2032. North Americans have a high consumption of bread and bakery products, leading to a higher demand for bread flour. The bread-eating culture is deeply rooted in North American diets, with products like sandwich bread, bagels, and artisanal loaves are widely popular Products.

The United States and Canada are major consumers and producers of bread flour, driven by the large commercial bakery industry and consumer demand for various bread products. Some of the largest bread flour manufacturers and suppliers are based in North America, such as Ardent Mills, Archer Daniels Midland Company, Cargill, Incorporated, and Conagra Brands, Inc. These companies have a strong presence and distribution networks across the region.

Europe represents a mature market for the Bread Flour industry, holding a market share of XX% and experiencing significant growth during its forecast period. Europe has a rich bread-baking tradition and a well-established bakery industry, the market is more split with various regional and local players catering to specific consumer preferences. The bread flour industry in Europe is focusing on stringent food safety regulations, quality standards, and labeling requirements set by various governing bodies, such as the European Union. Compliance with these regulations is a hallmark of a mature market. Market concentration in the bread flour industry in Europe has increased owing to larger players acquiring smaller regional brands and companies.

Bread Flour Market Competitive Landscape

The bread flour market is highly competitive, with many regional and local players catering to specific markets and consumer preferences. Factors such as product quality, pricing, distribution channels, and brand loyalty play a significant role in determining market dominance. The Bread Flour Market is always changing, with new leaders emerging and established players adjusting their strategies. One important strategy for a key company is its continuous focus on research and development (R&D) to stay at the forefront of technological advancements. To stay competitive in the global market, major players in the Bread Flour market have found that product launches are essential.

The key players in the Bread Flour market are Ardent Mills, Archer Daniels Midland Company, Cargill, Incorporated, Associated British Foods plc, Wilmar International Limited, Conagra Brands, Inc., Hodgson Mill, Inc., King Arthur Baking Company, Bob's Red Mill Natural Foods. These companies employ strategies like product/service launches, acquisitions, partnerships, regulations, and consumer demand for healthy and natural food products, driving collaborations to strengthen their market presence. The market is characterized by the government Bread Flour industry's growth.

- In May 2023, General Mills announced the acquisition of Tyson Foods' pet treats business for $1.2 billion. The strategic move allows General Mills to expand its presence in the growing pet food market and diversify its product portfolio beyond traditional consumer foods like bread flour.

- In August 2023, Rudi’s Rocky Mountain Bakery, the new brand introduced earlier this year by Rudi’s Organic Bakery and Rudi’s Gluten-free Bakery, launched Organic Seeded Multigrain Bread. The bread is made with organic whole wheat flour, rolled oats, flax seeds, pumpkin seeds, sunflower seeds, and poppy seeds. It also has a 24-hour fermentation process that, according to the manufacturer, improves gut health and results in a richer flavor and softer texture.

|

Bread Flour Market Scope |

|

|

Market Size in 2025 |

USD 18.10 Bn. |

|

Market Size in 2032 |

USD 28.69 Bn. |

|

CAGR (2026-2032) |

6.8 % |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segment |

by Source Rice Rye Wheat Others |

|

by Type Plain Flour Whole Grain Flour All-Purpose Flour |

|

|

by Feature Organic Unbleached Bleached Gluten-Free |

|

|

By Application Household Commercial |

|

|

by Distribution Channels Hypermarket & Supermarket Specialty Stores Retail Stores Online |

|

|

Regional Scope |

North America(United States), Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Player in the Bread Flour Market

- General Mills, Inc.(U.S.)

- Fairheaven Organic Flour Mill (Icelands)

- Ardent Mills (Denver)

- Doves Farm Foods (U.K.)

- Bay State Milling Company (Quincy)

- Bobs Red Mill (U.S.)

- Archer Daniels Midland company (U.S.)

- Associated British Foods (London)

- Goodman Fielder (Australia)

- Grain Craft Inc.(U.S.)

- ConAgra Foods, Inc. (Chicago)

- Hodgson Mill (USA)

- Grupo Siro (Spain)

- ADM Milling (Switzerland)

- King Arthur Flour Company, Inc. (USA)

- The Scoular Company (USA)

- The Hain Celestial Group, Inc. (New York)

- Allied Mills (U.K.)

- Wilmar International Limited (Singapore)

- Nisshin Flour Milling Inc. (Japan)

- Manildra Group (Australia)

- Odlums Group (Ireland)

- Nippon Flour Mills (Japan)

- Wilmar International (Singapore)

- Cargill, Incorporated (U.S.)

- XX.Inc.

Frequently Asked Questions

North America is expected to hold the highest share of the Bread Flour Market.

The Bread Flour Market size was valued at USD 18.10 Billion in 2025 reaching nearly USD 28.69 Billion in 2032.

There is a growing consumer preference for healthier and more nutritious food options. It includes a higher demand for organic, whole grain, and fortified bread flour. These products cater to health-conscious consumers looking for products with higher nutritional value and fewer additives quality are opportunities of market growth.

The segments covered in the Bread Flour Market report are based on Source, Type, Feature, Application form, and Distribution Channels.

1. Bread Flour Market: Research Methodology

1.1. Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market breakdown and Data Triangulation

1.4. Assumptions

2. Bread Flour Market: Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026– 2032) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Bread Flour Market: Competitive Landscape

3.1. Stellar Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Product Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. Product Launches and Innovation

4. Bread Flour Market: Dynamics

4.1. Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Market Drivers

4.3. Market Restraints

4.4. Market Opportunities

4.5. Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factors

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Value Chain Analysis

4.10. Regulatory Landscape by Region

4.10.1. North America

4.10.2. Europe

4.10.3. Asia Pacific

4.10.4. Middle East and Africa

4.10.5. South America

5. Bread Flour Market Size and Forecast by Segments (by Value USD Million and Volume in Kilogram)

5.1. Bread Flour Market Size and Forecast, By Source (2025-2032)

5.1.1. Rice

5.1.2. Rye

5.1.3. Wheat

5.1.4. Others

5.2. Bread Flour Market Size and Forecast, By Type (2025-2032)

5.2.1. Plain Flour

5.2.2. Whole Grain Flour

5.2.3. All-Purpose Flour

5.3. Bread Flour Market Size and Forecast, By Feature (2025-2032)

5.3.1. Organic

5.3.2. Unbleached

5.3.3. Bleached

5.3.4. Gluten-Free

5.4. Bread Flour Market Size and Forecast, By Application (2025-2032)

5.4.1. Household

5.4.2. Commercial

5.5. Bread Flour Market Size and Forecast, By Distribution Channel (2025-2032)

5.5.1. Hypermarket & Supermarket

5.5.2. Specialty Stores

5.5.3. Retail Stores

5.5.4. Online

5.6. Bread Flour Market Size and Forecast, by Region (2025-2032)

5.6.1. North America

5.6.2. Europe

5.6.3. Asia Pacific

5.6.4. Middle East and Africa

5.6.5. South America

6. North America Bread Flour Market Size and Forecast (by Value USD Million and Volume in Kilogram)

6.1. North America Bread Flour Market Size and Forecast, By Source (2025-2032)

6.1.1. Rice

6.1.2. Rye

6.1.3. Wheat

6.1.4. Others

6.2. North America Bread Flour Market Size and Forecast, By Type (2025-2032)

6.2.1. Plain Flour

6.2.2. Whole Grain Flour

6.2.3. All-Purpose Flour

6.3. North America Bread Flour Market Size and Forecast, By Feature (2025-2032)

6.3.1. Organic

6.3.2. Unbleached

6.3.3. Bleached

6.3.4. Gluten-Free

6.4. North America Bread Flour Market Size and Forecast, By Application (2025-2032)

6.4.1. Household

6.4.2. Commercial

6.5. North America Bread Flour Market Size and Forecast, By Distribution Channel (2025-2032)

6.5.1. Hypermarket & Supermarket

6.5.2. Specialty Stores

6.5.3. Retail Stores

6.5.4. Online

6.6. North America Bread Flour Market Size and Forecast, by Country (2025-2032)

6.6.1. United States

6.6.2. Canada

6.6.3. Mexico

7. Europe Bread Flour Market Size and Forecast (by Value USD Million and Volume in Kilogram)

7.1. Europe Bread Flour Market Size and Forecast, By Source (2025-2032)

7.2. Europe Bread Flour Market Size and Forecast, By Type (2025-2032)

7.3. Europe Bread Flour Market Size and Forecast, By Feature (2025-2032)

7.4. Europe Bread Flour Market Size and Forecast, By Application (2025-2032)

7.5. Europe Bread Flour Market Size and Forecast, By Distribution Channel (2025-2032)

7.6. Europe Bread Flour Market Size and Forecast, by Country (2025-2032)

7.6.1. UK

7.6.2. France

7.6.3. Germany

7.6.4. Italy

7.6.5. Spain

7.6.6. Sweden

7.6.7. Austria

7.6.8. Rest of Europe

8. Asia Pacific Bread Flour Market Size and Forecast (by Value USD Million and Volume in Kilogram)

8.1. Asia Pacific Bread Flour Market Size and Forecast, By Source (2025-2032)

8.2. Asia Pacific Bread Flour Market Size and Forecast, By Type (2025-2032)

8.3. Asia Pacific Bread Flour Market Size and Forecast, By Feature (2025-2032)

8.4. Asia Pacific Bread Flour Market Size and Forecast, By Application (2025-2032)

8.5. Asia Pacific Bread Flour Market Size and Forecast, By Distribution Channel (2025-2032)

8.6. Asia Pacific Bread Flour Market Size and Forecast, by Country (2025-2032)

8.6.1. China

8.6.2. S Korea

8.6.3. Japan

8.6.4. India

8.6.5. Australia

8.6.6. Indonesia

8.6.7. Malaysia

8.6.8. Vietnam

8.6.9. Taiwan

8.6.10. Bangladesh

8.6.11. Pakistan

8.6.12. Rest of Asia Pacific

9. Middle East and Africa Bread Flour Market Size and Forecast (by Value USD Million and Volume in Kilogram)

9.1. Middle East and Africa Bread Flour Market Size and Forecast, By Source (2025-2032)

9.2. Middle East and Africa Bread Flour Market Size and Forecast, By Type (2025-2032)

9.3. Middle East and Africa Bread Flour Market Size and Forecast, By Feature (2025-2032)

9.4. Middle East and Africa Bread Flour Market Size and Forecast, By Application (2025-2032)

9.5. Middle East and Africa Bread Flour Market Size and Forecast, By Distribution Channel (2025-2032)

9.6. Middle East and Africa Bread Flour Market Size and Forecast, by Country (2025-2032)

9.6.1. South Africa

9.6.2. GCC

9.6.3. Egypt

9.6.4. Nigeria

9.6.5. Rest of ME&A

10. South America Bread Flour Market Size and Forecast (by Value USD Million and Volume in Kilogram)

10.1. South America Bread Flour Market Size and Forecast, By Source (2025-2032)

10.2. South America Bread Flour Market Size and Forecast, By Type (2025-2032)

10.3. South America Bread Flour Market Size and Forecast, By Feature (2025-2032)

10.4. South America Bread Flour Market Size and Forecast, By Application (2025-2032)

10.5. South America Bread Flour Market Size and Forecast, By Distribution Channel (2025-2032)

10.6. South America Bread Flour Market Size and Forecast, by Country (2025-2032)

10.6.1. Brazil

10.6.2. Argentina

10.6.3. Rest of South America

11. Company Profile: Key players

11.1. General Mills, Inc.(U.S.)

11.1.1. Company Overview

11.1.2. Product Portfolio

11.1.2.1. Product Name

11.1.2.2. Product Details

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Fairheaven Organic Flour Mill (Icelands)

11.3. Ardent Mills (Denver)

11.4. Doves Farm Foods (U.K.)

11.5. Bay State Milling Company (Quincy)

11.6. Bobs Red Mill (U.S.)

11.7. Archer Daniels Midland company (U.S.)

11.8. Associated British Foods (London)

11.9. Goodman Fielder (Australia)

11.10. Grain Craft Inc.(U.S.)

11.11. ConAgra Foods, Inc. (Chicago)

11.12. Hodgson Mill (USA)

11.13. Grupo Siro (Spain)

11.14. ADM Milling (Switzerland)

11.15. King Arthur Flour Company, Inc. (USA)

11.16. The Scoular Company (USA)

11.17. The Hain Celestial Group, Inc. (New York)

11.18. Allied Mills (U.K.)

11.19. Wilmar International Limited (Singapore)

11.20. Nisshin Flour Milling Inc. (Japan)

11.21. Manildra Group (Australia)

11.22. Odlums Group (Ireland)

11.23. Nippon Flour Mills (Japan)

11.24. Wilmar International (Singapore)

11.25. Cargill, Incorporated (U.S.)

11.26. XX.Inc.

12. Key Findings

13. Industry Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook