Banking as a Service Market: Global Market Size, Growth Outlook, Embedded Finance, and API Ecosystem Analysis (2026-2032)

Banking-as-a-Service (BaaS) Market size was valued at USD 823.16 Billion in 2025 and the total Banking-as-a-Service (BaaS) revenue is expected to grow at 18% through 2026 to 2032, reaching nearly USD 2622.15 Billion while reshaping financial infrastructure through API driven banking, embedded finance, and bank fintech partnerships, supported by strong digital banking adoption and rising demand from non-financial enterprises.

Banking-as-a-Service (BaaS) Market Overview

Banking-as-a-Service (BaaS) Market has moved from an enabling technology layer to a core growth engine for the modern financial ecosystem. This growth is tightly linked to the structural shift in how banking products are built, distributed, and consumed. Market size was valued at USD 823.16 Billion in 2025 and the total Banking-as-a-Service (BaaS) revenue is expected to grow at 18% through 2026 to 2032, reaching nearly USD 2622.15 Billion.

Global digital banking adoption has reached scale, with over 3.58 billion users worldwide and mobile apps now the primary banking interface for more than half of U.S. consumers. In India alone, digital banking users exceed 290 million. This behavioral shift has created a natural demand for Banking as a Service platforms that allow banks, fintechs, and non-financial enterprises to embed payments, accounts, cards, and lending directly into digital journeys.

For banks, the Banking as a Service market represents a monetization pathway for regulated infrastructure and balance sheets. For fintech companies and enterprises, it provides faster time to market, lower compliance burden, and flexible product innovation. As digital channels are expected to account for nearly 89.5% of global banking interactions, Banking as a Service is becoming foundational rather than optional.

-Market-Overview.webp)

To get more Insights: Request Free Sample Report

Banking-as-a-Service (BaaS) Market Dynamics

Banking-as-a-Service (BaaS) Market Drivers

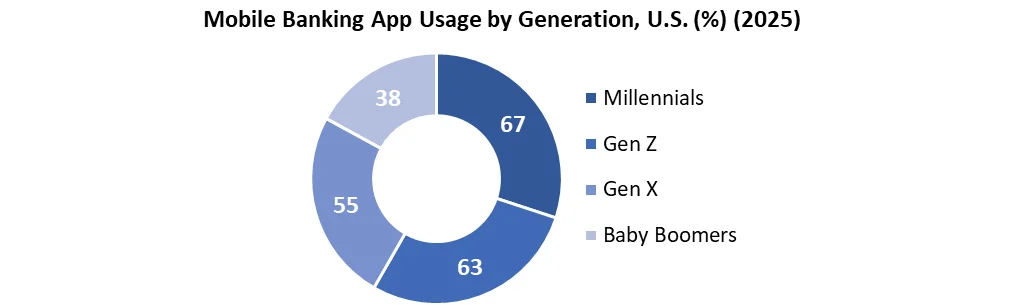

The primary driver of the Banking as a Service market is sustained digital banking adoption across all age groups. In 2025, in the U.S., over 50% of consumers now rely on mobile apps as their primary banking method, while 67% of millennials and 63% of Gen Z prefer mobile first banking experiences. Financial institutions are responding, with over 80% of financial leaders viewing Banking as a Service as a new revenue model and 60% treating it as a strategic priority.

Embedded finance demand is accelerating adoption across e commerce platforms, marketplaces, and non-financial enterprises. The ability to integrate payments, accounts, and credit directly into customer workflows is driving high frequency usage and recurring transaction volumes. Cost efficiency is another key driver, as digital acquisition costs can be as low as 1% of traditional branch-based models, while operating costs can decline by roughly 20 to 40% with platform led architectures.

Banking-as-a-Service (BaaS) Market Restraints and Challenges

Legacy infrastructure remains a structural constraint. Nearly 55% of financial institutions still operate on legacy systems, and 50% cite these systems as the biggest barrier to transformation. Regulatory scrutiny is also intensifying, with 14% of severe enforcement actions in 2024 targeting banks involved in Banking as a Service models. Compliance ownership, data localization, and cross border regulatory alignment continue to limit scalability.

Banking-as-a-Service (BaaS) Market Regional Insights

In 2025, North America held the largest market share and remains a mature and high-value region in the Banking-as-a-Service (BaaS) market, supported by deep fintech penetration, strong API adoption, and high mobile banking usage. The U.S. alone has over 215 million digital banking users, with 80% of the population expected to use digital banking by 2030.

Europe shows strong adoption driven by open banking regulations and licensed Banking as a Service providers, particularly in the UK and EU. Asia Pacific represents the fastest growth region, supported by mobile first consumers, high real time payment adoption, and expanding fintech ecosystems. India and Southeast Asia stand out as long term growth markets due to scale, cost sensitivity, and embedded finance use cases across commerce platforms.

Banking-as-a-Service (BaaS) Market Segment Analysis

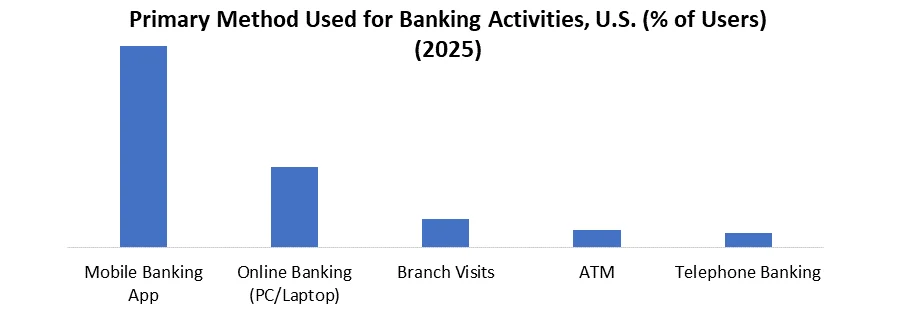

Banking-as-a-Service (BaaS) Market size by Type: Payment gateway services represent one of the highest volume segments within the Banking as a Service market in 2025. Mobile apps account for nearly 50% of bill payments and person to person transfers, compared to 38 to 44% via traditional online channels. With 35% of users accessing mobile banking apps daily, payment APIs generate high transaction frequency and recurring revenue for Banking as a Service providers.

Banking-as-a-Service (BaaS) Market size by End User: Fintech Companies remain a core demand segment, leveraging Banking as a Service platform to launch accounts, cards, and lending products without owning banking licenses. As over 60% of consumers indicate willingness to switch to digital only banks, fintech led offerings continue to scale rapidly, driving API usage, customer onboarding volumes, and cross selling opportunities across the Banking as a Service market.

Banking-as-a-Service (BaaS) Market Competitive Landscape

The Banking as a Service market is moderately fragmented, comprising licensed banks, regulated BaaS platforms, core banking technology providers, and payment infrastructure specialists. Competition is driven by sponsor bank access, regulatory coverage, API reliability, and transaction scale rather than as attributed to the price alone.

Leading Banking as a Service providers such as Marqeta, a leading modern card issuing and API platform used widely in BaaS ecosystems, reported total processing volume (TPV) of approximately USD 291 billion in 2024, reflecting strong adoption across fintech and embedded finance use cases. Core banking and platform providers including Mambu, Temenos, and FintechOS support hundreds of banks and fintech deployments globally, highlighting their role in powering digital only banks and BaaS ecosystems.

Sponsor banks remain a structural bottleneck in the Banking as a Service market. Public disclosures indicate that a limited number of regulated banks support dozens of fintech programs simultaneously, increasing buyer focus on sponsor bank stability, compliance capability, and balance sheet capacity.

Overall, competitive differentiation in the Banking as a Service market increasingly depends on proven transaction scale, regulatory resilience, and the ability to support long term embedded finance growth.

|

Global Banking-as-a-Service Market Scope |

|

|

Market Size in 2025 |

USD 823.16 Bn. |

|

Market Size in 2032 |

USD 2622.15 Bn. |

|

CAGR (2026-2032) |

18% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segments Analysis |

By Type Payment Gateway Bank Account/Core Banking Lending and Credit Services Embedded Finance Others |

|

By Component Platform/API Services Account Management Services Payment Processing Services Lending & Credit Services Compliance & Regulatory Services Investment & Wealth Management Services Others |

|

|

By Deployment Hybrid On-Premise |

|

|

By Enterprise Size SMEs Large Enterprises |

|

|

By End User Banks and Financial Institutions Fintech Companies E-commerce Platforms & Marketplaces Non-Financial Enterprises |

|

Banking-as-a-Service (BaaS) Market by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Russia, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Thailand, Vietnam, Philippines, and Rest of APAC)

Middle East and Africa (South Africa, GCC, Nigeria, Egypt, Turkey, and Rest of ME&A)

South America (Brazil, Argentina, Colombia, Chile, Peru, and the Rest of South America)

Banking-as-a-Service (BaaS) Market Key Players

-

Solaris

-

Railsr

-

Bankable

-

Treezor

-

Engine by Starling

-

Marqeta

-

Mambu

-

Green Dot

-

BBVA Open Platform

-

Treasury Prime

-

Unit

-

Fidor

-

Contis

-

Q2

-

Temenos

-

The Bancorp

-

Griffin

-

FintechOS

-

Mbanq

-

Solid

-

Stripe Treasury

-

Currencycloud

-

Sarvatra Technologies

-

OneConnect

Regional Breakdown:

Europe Banking-as-a-Service (BaaS) Market: Industry Analysis and Forecast (2024-2030)

Frequently Asked Questions

One of the major drivers of the BaaS market is various integrated applications offered by BaaS. E.g. Card payments processing.

Another driver of the BaaS market is that it allows efficient and hassle-free ID verification services in Know Your Client (KYC) procedures.

Banking-as-a-Service (BaaS) Market size was valued at USD 823.16 Billion in 2025 and the total Banking-as-a-Service (BaaS) revenue is expected to grow at 18% through 2026 to 2032, reaching nearly USD 2622.15 Billion.

The segments covered are Type, Enterprise, Service and, Region.

1. Global Banking-as-a-Service Market: Research Methodology

2. Global Banking-as-a-Service Market Introduction

2.1. Executive Summary

2.2. Market Size (2025) & Forecast (2026-2032)

2.3. Market Size (USD) and Market Share (%) - By Segments, Regions and Country

3. Global Banking-as-a-Service Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Competitive Landscape

3.3. Key Players Benchmarking

3.3.1. Company Name

3.3.2. Product Portfolio

3.3.3. End User Reach

3.3.4. Market Share (%)

3.3.5. Revenue (2025)

3.3.6. R&D Investment

3.3.7. Revenue Growth Rate (%)

3.3.8. Geographical Presence

3.4. Market Structure

3.4.1. Market Leaders

3.4.2. Market Followers

3.4.3. Emerging Players

3.5. Mergers and Acquisitions Details

3.6. Recent Developments

3.7. Market Positioning & Share Analysis

3.7.1. Company Revenue, Banking-as-a-Service Revenue, and Market Share (%)

3.7.2. SMR Competitive Positioning

3.8. Strategic Developments & Partnerships

4. Banking-as-a-Service Market: Dynamics

4.1. Banking-as-a-Service Market Trends

4.2. Banking-as-a-Service Market Dynamics

4.2.1. Drivers

4.2.2. Restraints

4.2.3. Challenges

4.2.4. Opportunities

4.3. PORTER’s Five Forces Analysis

4.4. PESTLE Analysis

5. BaaS Value Chain and Ecosystem Structure

5.1. Role of licensed banks and sponsor banks

5.2. BaaS platform providers and API aggregators

5.3. Middleware, compliance, and infrastructure enablers

5.4. Fintechs and non-financial enterprises as demand-side players

5.5. Value capture and margin distribution across the ecosystem

6. Banking-as-a-Service Market Technology Architecture and API Stack Analysis

6.1. Core banking infrastructure and ledger architecture

6.2. API orchestration and integration layers

6.3. Payments, accounts, cards, and lending module architecture

6.4. Data security, encryption, and access control frameworks

6.5. Scalability, uptime, and system resilience considerations

7. Banking-as-a-Service Market Embedded Finance Use Case Penetration Analysis

7.1. Embedded payments adoption by industry vertical

7.2. Embedded banking accounts and card issuance use cases

7.3. Embedded lending and credit enablement models

7.4. Revenue contribution by embedded finance use case

7.5. Enterprise vs fintech-led embedded finance deployments

8. Banking-as-a-Service Market Regulatory and Compliance Landscape Impacting BaaS

8.1. Licensing structures and regulatory ownership models

8.2. KYC, AML, and transaction monitoring responsibilities

8.3. Data localization and cross-border compliance challenges

8.4. Regional regulatory divergence and its impact on scalability

8.5. Regulatory risks and compliance cost implications

9. Banking-as-a-Service Market Commercial Models and Revenue Economics

9.1. Subscription-based pricing models

9.2. Transaction-based and usage-led revenue models

9.3. Hybrid pricing structures across services

9.4. Unit economics across payments, lending, and accounts

9.5. Cost drivers and margin sensitivity analysis

10. Bank–Fintech Partnership and Operating Models

10.1. Direct bank-to-fintech partnership structures

10.2. Aggregator-led and multi-bank routing models

10.3. Risk sharing and liability allocation frameworks

10.4. Operational complexity and scalability trade-offs

10.5. Case-based comparison of partnership models

11. Go-to-Market Strategies and Customer Acquisition Dynamics

11.1. API-first and developer-led adoption strategies

11.2. Vertical-specific BaaS offerings

11.3. Enterprise sales vs fintech-led GTM approaches

11.4. Customer onboarding timelines and friction points

11.5. Retention drivers and switching barriers

12. Regional Banking-as-a-Service Market Maturity and Adoption Readiness

12.1. BaaS adoption maturity by region

12.2. Regulatory readiness and sponsor bank availability

12.3. API infrastructure and cloud penetration impact

12.4. Region-wise barriers to scaling BaaS

12.5. Near-term vs long-term growth pockets

13. Use Case Economics and Profitability Benchmarks

13.1. Revenue per API and per customer benchmarks

13.2. Cost-to-serve by use case payments vs accounts vs lending

13.3. Breakeven timelines for fintechs using BaaS

13.4. High-margin vs low-margin BaaS services

13.5. Cross-subsidization dynamics within platforms

14. Banking-as-a-Service Market: Sponsor Bank Strategy and Capacity Analysis

14.1. Number and type of sponsor banks by region

14.2. Balance sheet capacity constraints

14.3. Risk appetite and sector exposure limits

14.4. Impact of bank exits on platform continuity

14.5. Strategic importance of banks in BaaS negotiations

15. Banking-as-a-Service Market Data Ownership, Monetization, and Privacy Considerations

15.1. Ownership of transaction and customer data

15.2. Data monetization opportunities and limits

15.3. Privacy regulations and consent management

15.4. Data portability and switching risks

15.5. Strategic value of data in BaaS ecosystems

16. Global Banking-as-a-Service Market: Size and Forecast by Segmentation (By Value USD Billion) (2025-2032)

16.1. Global Banking-as-a-Service Market Size and Forecast, By Type

16.1.1. Payment Gateway

16.1.2. Bank Account/Core Banking

16.1.3. Lending and Credit Services

16.1.4. Embedded Finance

16.1.5. Others

16.2. Global Banking-as-a-Service Market Size and Forecast, By Component

16.2.1. Platform/API

16.2.2. Services

16.2.2.1. Account Management Services

16.2.2.2. Payment Processing Services

16.2.2.3. Lending & Credit Services

16.2.2.4. Compliance & Regulatory Services

16.2.2.5. Investment & Wealth Management Services

16.2.2.6. Others

16.3. Global Banking-as-a-Service Market Size and Forecast, By Deployment

16.3.1. Hybrid

16.3.2. On-Premise

16.4. Global Banking-as-a-Service Market Size and Forecast, By Enterprise Size

16.4.1. SMEs

16.4.2. Large Enterprises

16.5. Global Banking-as-a-Service Market Size and Forecast, By End User

16.5.1. Banks and Financial Institutions

16.5.2. Fintech Companies

16.5.3. E-commerce Platforms & Marketplaces

16.5.4. Non-Financial Enterprises

16.6. Global Banking-as-a-Service Market Size and Forecast, By Region

16.6.1. North America

16.6.2. Europe

16.6.3. Asia Pacific

16.6.4. Middle East and Africa

16.6.5. South America

17. North America Banking-as-a-Service Market Size and Forecast By Segmentation (By Value USD Billion) (2025-2032)

17.1. North America Market Size and Forecast, By Type

17.2. North America Market Size and Forecast, By Component

17.3. North America Market Size and Forecast, By Deployment

17.4. North America Market Size and Forecast, By Enterprise Size

17.5. North America Market Size and Forecast, By End User

17.6. North America Market Size and Forecast, By Country

17.6.1. United States

17.6.2. Canada

17.6.3. Mexico

18. Europe Banking-as-a-Service Market Size and Forecast By Segmentation (By Value USD Billion) (2025-2032)

18.1. Europe Market Size and Forecast, By Type

18.2. Europe Market Size and Forecast, By Component

18.3. Europe Market Size and Forecast, By Deployment

18.4. Europe Market Size and Forecast, By Enterprise Size

18.5. Europe Market Size and Forecast, By End User

18.6. Europe Market Size and Forecast, By Country

18.6.1. United Kingdom

18.6.2. France

18.6.3. Germany

18.6.4. Italy

18.6.5. Spain

18.6.6. Sweden

18.6.7. Russia

18.6.8. Rest of Europe

19. Asia Pacific Banking-as-a-Service Market Size and Forecast by Segmentation (By Value USD Billion) (2025-2032)

19.1. Asia Pacific Market Size and Forecast, By Type

19.2. Asia Pacific Market Size and Forecast, By Component

19.3. Asia Pacific Market Size and Forecast, By Deployment

19.4. Asia Pacific Market Size and Forecast, By Enterprise Size

19.5. Asia Pacific Market Size and Forecast, By End User

19.6. Asia Pacific Market Size and Forecast, By Country

19.6.1. China

19.6.2. Japan

19.6.3. South Korea

19.6.4. India

19.6.5. Australia

19.6.6. Malaysia

19.6.7. Thailand

19.6.8. Vietnam

19.6.9. Indonesia

19.6.10. Philippines

19.6.11. Rest of Asia Pacific

20. Middle East and Africa Banking-as-a-Service Market Size and Forecast By Segmentation (By Value USD Billion) (2025-2032)

20.1. Middle East and Africa Market Size and Forecast, By Type

20.2. Middle East and Africa Market Size and Forecast, By Component

20.3. Middle East and Africa Market Size and Forecast, By Deployment

20.4. Middle East and Africa Market Size and Forecast, By Enterprise Size

20.5. Middle East and Africa Market Size and Forecast, By End User

20.6. Middle East and Africa Market Size and Forecast, By Country

20.6.1. South Africa

20.6.2. GCC

20.6.3. Nigeria

20.6.4. Egypt

20.6.5. Turkey

20.6.6. Rest of ME&A

21. South America Banking-as-a-Service Market Size and Forecast By Segmentation (By Value USD Billion) (2025-2032)

21.1. South America Market Size and Forecast, By Type

21.2. South America Market Size and Forecast, By Component

21.3. South America Market Size and Forecast, By Finish

21.4. South America Market Size and Forecast, By Enterprise Size

21.5. South America Market Size and Forecast, By End User

21.6. South America Market Size and Forecast, By Country

21.6.1. Brazil

21.6.2. Argentina

21.6.3. Colombia

21.6.4. Chile

21.6.5. Rest Of South America

22. Company Profile: Key Players

22.1. Solaris

22.1.1. Company Overview

22.1.2. Business Portfolio

22.1.3. Financial Overview

22.1.4. SWOT Analysis

22.1.5. Strategic Analysis

22.1.6. Recent Developments

22.2. Railsr

22.3. Bankable

22.4. Treezor

22.5. ClearBank

22.6. Engine by Starling

22.7. Marqeta

22.8. Mambu

22.9. Green Dot

22.10. BBVA Open Platform

22.11. Treasury Prime

22.12. Unit

22.13. Fidor

22.14. Contis

22.15. Q2

22.16. Temenos

22.17. The Bancorp

22.18. Griffin

22.19. FintechOS

22.20. Mbanq

22.21. Solid

22.22. Stripe Treasury

22.23. Currencycloud

22.24. Sarvatra Technologies

22.25. OneConnect

23. Banking-as-a-Service Market Key Findings

24. Banking-as-a-Service Industry Recommendations