Baked Chips Market Global Industry Analysis and Forecast (2026-2032)

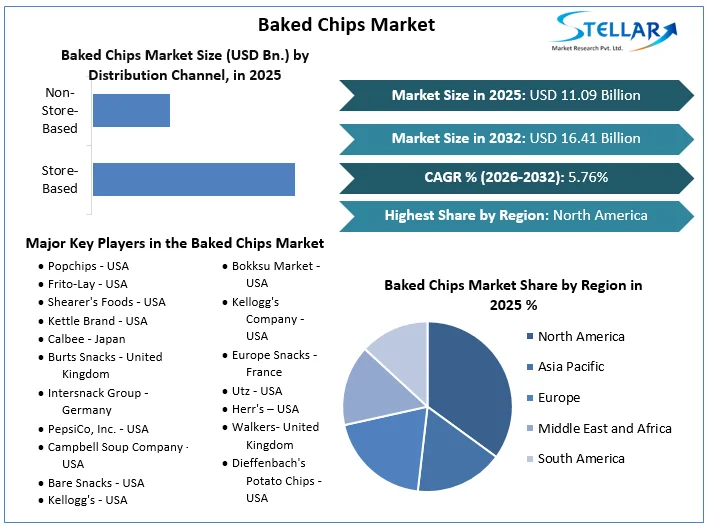

The Baked Chips Market size was valued at USD 11.09 Bn. in 2025 and the total Global Baked Chips Market size is expected to grow at a CAGR of 5.76% from 2026 to 2032, reaching nearly USD 16.41 Bn. by 2032.

Baked Chips Market Overview

Baked chips are a healthier alternative to traditional fried chips, made from sliced vegetables or grains, seasoned and baked until crisp. They cater to the growing demand for healthier snack options, as consumers become more health-conscious and seek a satisfying crunch without the excess oil and calories associated with deep-fried products. Baked chips offer a tasty and convenient snack option with reduced fat content, aligning with the trend toward healthier eating habits. The baked chips market is booming as more people seek convenient, tasty, and health-conscious snack choices.

The growing adoption of veggie and plant-based foods is a key driver behind the market's growth. Baked chips, often prepared from plant-based components, align with the growing demand for ethical and environmentally conscious food varieties. However, traditional fried chips pose a difficult challenge to the baked chips market. The baked chips market is capitalizing on expanding consumer awareness of health benefits and leveraging the demand for nutritious snack options. Innovations in flavor profiles further enhance growth prospects, allowing the industry to cater to evolving tastes while convention the rising demand for healthier alternatives and fostering opportunities for market growth.

To get more Insights: Request Free Sample Report

Baked Chips Market Dynamics:

The baked chips market is growing because of the increasing preference for baked food over fried foods. Baked dishes are considered low-cholesterol and healthier than fried ones, as they are cooked at high temperatures. Consumers are increasingly seeking health-based baked snacks that provide flavor and convenience, making them more nutritious than fried snacks. Manufacturers are introducing new items to meet customer demand for baked goods. Ancient grains, such as malt and whole grains, are gaining popularity because of their health benefits and potential to reduce the risk of cancer and diabetes.

Whole grain snack foods contain dietary fiber, protein, vitamins, and magnesium, which help reduce the risk of cancer and diabetes. Manufacturers are also introducing new items with grain ingredients in their snacks. The working millenary generation is driving the market of low-calorie, low-fat, gluten-free, complete wheat snacks, such as savory snacks and bakery products without biochemical preservers and flavours. Products like heated veggie chips, heated pita chips, and nutritious muesli bars are high in fiber, serving in weight loss and behind satiation. This change in consumer eating habits is driving the Baked Chips market growth.

Baked Chips Market Restraints:

- Competition from Fried Chips: The growth of baked chips is restricted by the continued dominance of traditional fried potato chips in the snack industry. Some consumers are able to find it difficult to switch to baked alternatives from fried chips because they have a well-known taste and texture.

- Difficulties in Sourcing components: Getting high-quality ingredients for baked chips, like fresh potatoes and root vegetables, provides logistical difficulties for producers. Seasonal changes and complex supply chains potentially impact the cost and consistency of production.

- Cost Sensitivity: Because baked chips are made using premium ingredients and baked rather than fried, they are frequently more expensive than fried chips. Customers who are concerned about costs are hesitant to move to baked chips, specifically if they think the price difference is big.

The increasing demand for fast and healthful snack choices, along with changing consumer preferences, is driving the growth of the snack sector as a whole. This presents an opportunity for manufacturers of baked chips to enter this growing sector and bring in more customers. Consumer choices for snacks are being influenced by the global movement toward health and well-being. Baked chips fit in well with this trend because of their supposed health benefits. The health benefits of baked chips and their marketing as a guilt-free treat are two ways that manufacturers are taking advantage of this potential. It is possible to bring in new customers by creating creative ingredient combinations and broadening the variety of baked chip flavors. Products that appeal to certain dietary preferences and target specific markets include baked chips that are organic, gluten-free, and non-GMO.

Baked Chips Market Segment Analysis:

Based on Source, Vegetables, fruits, cereals, grains, and other products are included in the market segmentation for baked chips. With XX% of market sales, the veggies section led the market. Vegetable-based chips provide iron, vitamin A, protein, fiber, and vitamin C. Compared to standard potato chips, they are lower in fat and calories. They are therefore a preferred snack for people who are trying to reduce weight. A more exciting crunch and chew sensation is produced by veggie chips that come in a variety of colors, shapes, sizes, and textures.

Based on Functionality, The market segmentation for baked chips includes low-calorie, low-sodium, organic, and gluten-free options. The market was dominated by organic products. These days, several pick healthier choices over deep-fried chips, preferring baked chips. Consumers are growing more aware of their health and looking for nutritious snacks that complement their diets with useful ingredients like fiber, vitamins, and antioxidants. This has influenced people to buy baked chips as they are healthy because they are low in fat and calories.

Baked Chips Market Regional Insight:

North America holds the largest market share in 2025 for baked chips, driven by increased consumption of convenience foods and health and fitness concerns. The developed retail structure in North America allows consumers to conveniently purchase food and groceries, making baked chips more accessible. The increasing demand for baked goods and shifting cultural preferences make the largest revenue producer in the baked chips market. The region is expected to continue leading the market in the upcoming years because of rising consumer behavior changes towards healthy food and beverages and lifestyle awareness. Producers are focusing on celebrity endorsement campaigns to draw consumer interest in their products and maintain their market share.

Europe has the second-largest market share for baked chips. With the rising popularity of convenience meals and baked chips in Europe, people often snack during social events or while traveling, but a growing number of consumers are choosing healthier choices. The biggest market of organic and natural snacks is healthier snacking, usually done in between meals. Also, the market of baked chips in Germany held the largest market share, while the market of baked chips in the UK increased at the fastest rate in the European Union.

Baked Chips Market Competitive Landscape:

Leading businesses in the sector are investing heavily in R&D to broaden the range of products they offer, which propel the growth of the baked chips market. New product releases, contracts, mergers and acquisitions, increased investments, and cooperation with other businesses are examples of significant market growth. In addition, market players take part in several calculated measures to broaden their global reach. To grow and endure in an increasingly demanding and competitive market, the baked chip business needs to create low-cost goods.

- Calbee, Inc. (headquartered in Chiyoda-ku, Tokyo; Makoto Ehara, Representative Director, President & CEO) (“Calbee”) is pleased to announce that the company signed a site acquisition reservation agreement with the Shimotsuma City Development Bureau on August 23, 2023, following its decision to build a new factory in Shimotsuma City, Ibaraki Prefecture. The new factory has a site area of approximately 190,000m2, the largest among the Calbee Group's domestic factories, with a land investment of approximately 4.94 billion yen.

- May 20, 2024 – Campbell Soup Company is introducing a new line to Prego®: Creamy Pesto a delicious, versatile, and kid-friendly way to increase horizons in the kitchen beyond pasta. The new offering makes pesto approachable while offering a delicious taste created by a brand families trust and love.

|

Baked Chips Market Scope |

|

|

Market Size in 2025 |

USD 11.09 Bn. |

|

Market Size in 2032 |

USD16.41 Bn. |

|

CAGR (2026-2032) |

5.76 % |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segments |

By Source Vegetable Fruits Cereals Grains Others |

|

By Functionality Organic Gluten-Free Low Calories Low Sodium Others |

|

|

By Distribution Channel Store-Based Non-Store-Based |

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Russia, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Player in the Baked Chips Market

- Popchips - USA

- Frito-Lay - USA

- Shearer's Foods - USA

- Kettle Brand - USA

- Calbee - Japan

- Burts Snacks - United Kingdom

- Intersnack Group - Germany

- PepsiCo, Inc. - USA

- Campbell Soup Company - USA

- Bare Snacks - USA

- Kellogg's - USA

- Bokksu Market - USA

- Kellogg's Company - USA

- Europe Snacks - France

- Utz - USA

- Herr's – USA

- Walkers- United Kingdom

- Dieffenbach's Potato Chips - USA

- Terra Chips - USA

- Beanfields - USA

- Rw Garcia – USA

- XX.inc

Frequently Asked Questions

North America is expected to lead the Baked Chips Market during the forecast period.

An analysis of profit trends and projections for companies in the Baked Chips Market is included, offering insights into factors driving profitability, cost management strategies, and financial performance metrics.

The Baked Chips Market size was valued at USD 11.09 Billion in 2025 and the total Global Baked Chips Market size is expected to grow at a CAGR of 5.76% from 2026 to 2032, reaching nearly USD 16.41 Billion by 2032.

The segments covered in the market report are by Source, by Functionality, and by Distribution Channel.

1. Baked Chips Market: Research Methodology

1.1. Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Assumptions

2. Baked Chips Market: Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026 – 2032) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Baked Chips Market: Competitive Landscape

3.1. Stellar Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Product Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. Product Launches and Innovation

4. Baked Chips Market: Dynamics

4.1. Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Market Drivers

4.3. Market Restraints

4.4. Market Opportunities

4.5. Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factors

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Value Chain Analysis

4.10. Regulatory Landscape by Region

4.10.1. North America

4.10.2. Europe

4.10.3. Asia Pacific

4.10.4. Middle East and Africa

4.10.5. South America

5. Baked Chips Market Size and Forecast by Segments (by Value USD Million)

5.1. Baked Chips Market Size and Forecast, By Source (2025-2032)

5.1.1. Vegetable

5.1.2. Fruits

5.1.3. Cereals

5.1.4. Grains

5.1.5. Others

5.2. Baked Chips Market Size and Forecast, By Functionality (2025-2032)

5.2.1. Organic

5.2.2. Gluten-Free

5.2.3. Low Calories

5.2.4. Low Sodium

5.2.5. Others

5.3. Baked Chips Market Size and Forecast, By Distribution Channel (2025-2032)

5.3.1. Store-Based

5.3.2. Non-Store-Based

5.4. Baked Chips Market Size and Forecast, by Region (2025-2032)

5.4.1. North America

5.4.2. Europe

5.4.3. Asia Pacific

5.4.4. Middle East and Africa

5.4.5. South America

6. North America Baked Chips Market Size and Forecast (by Value USD Million)

6.1. North America Baked Chips Market Size and Forecast, By Source (2025-2032)

6.1.1. Vegetable

6.1.2. Fruits

6.1.3. Cereals

6.1.4. Grains

6.1.5. Others

6.2. North America Baked Chips Market Size and Forecast, By Functionality (2025-2032)

6.2.1. Organic

6.2.2. Gluten-Free

6.2.3. Low Calories

6.2.4. Low Sodium

6.2.5. Others

6.3. North America Baked Chips Market Size and Forecast, By Distribution Channel (2025-2032)

6.3.1. Store-Based

6.3.2. Non-Store-Based

6.4. North America Baked Chips Market Size and Forecast, by Country (2025-2032)

6.4.1. United States

6.4.2. Canada

6.4.3. Mexico

7. Europe Baked Chips Market Size and Forecast (by Value USD Million)

7.1. Europe Baked Chips Market Size and Forecast, By Source (2025-2032)

7.2. Europe Baked Chips Market Size and Forecast, By Functionality (2025-2032)

7.3. Europe Baked Chips Market Size and Forecast, By Distribution Channel (2025-2032)

7.4. Europe Baked Chips Market Size and Forecast, by Country (2025-2032)

7.4.1. UK

7.4.2. France

7.4.3. Germany

7.4.4. Italy

7.4.5. Spain

7.4.6. Sweden

7.4.7. Austria

7.4.8. Rest of Europe

8. Asia Pacific Baked Chips Market Size and Forecast (by Value USD Million)

8.1. Asia Pacific Baked Chips Market Size and Forecast, By Source (2025-2032)

8.2. Asia Pacific Baked Chips Market Size and Forecast, By Functionality (2025-2032)

8.3. Asia Pacific Baked Chips Market Size and Forecast, By Distribution Channel (2025-2032)

8.4. Asia Pacific Baked Chips Market Size and Forecast, by Country (2025-2032)

8.4.1. China

8.4.2. S Korea

8.4.3. Japan

8.4.4. India

8.4.5. Australia

8.4.6. Indonesia

8.4.7. Malaysia

8.4.8. Vietnam

8.4.9. Taiwan

8.4.10. Bangladesh

8.4.11. Pakistan

8.4.12. Rest of Asia Pacific

9. Middle East and Africa Baked Chips Market Size and Forecast (by Value USD Million)

9.1. Middle East and Africa Baked Chips Market Size and Forecast, By Source (2025-2032)

9.2. Middle East and Africa Baked Chips Market Size and Forecast, By Functionality (2025-2032)

9.3. Middle East and Africa Baked Chips Market Size and Forecast, By Distribution Channel (2025-2032)

9.4. Middle East and Africa Baked Chips Market Size and Forecast, by Country (2025-2032)

9.4.1. South Africa

9.4.2. GCC

9.4.3. Egypt

9.4.4. Nigeria

9.4.5. Rest of ME&A

10. South America Baked Chips Market Size and Forecast (by Value USD Million)

10.1. South America Baked Chips Market Size and Forecast, By Source (2025-2032)

10.2. South America Baked Chips Market Size and Forecast, By Functionality (2025-2032)

10.3. South America Baked Chips Market Size and Forecast, By Distribution Channel (2025-2032)

10.4. South America Baked Chips Market Size and Forecast, by Country (2025-2032)

10.4.1. Brazil

10.4.2. Argentina

10.4.3. Rest of South America

11. Company Profile: Key players

11.1. Popchips - USA

11.1.1. Company Overview

11.1.2. Product Portfolio

11.1.2.1. Product Name

11.1.2.2. Product Details

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Frito-Lay - USA

11.3. Shearer's Foods - USA

11.4. Kettle Brand - USA

11.5. Calbee - Japan

11.6. Burts Snacks - United Kingdom

11.7. Intersnack Group - Germany

11.8. PepsiCo, Inc. - USA

11.9. Campbell Soup Company - USA

11.10. Bare Snacks - USA

11.11. Kellogg's - USA

11.12. Bokksu Market - USA

11.13. Kellogg's Company - USA

11.14. Europe Snacks - France

11.15. Utz - USA

11.16. Herr's – USA

11.17. Walkers- United Kingdom

11.18. Dieffenbach's Potato Chips - USA

11.19. Terra Chips - USA

11.20. Beanfields - USA

11.21. Rw Garcia – USA

11.22. XX.inc

12. Key Findings

13. Industry Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook