Autonomous Driverless Cars Market Global Industry Analysis and Forecast (2026-2032)

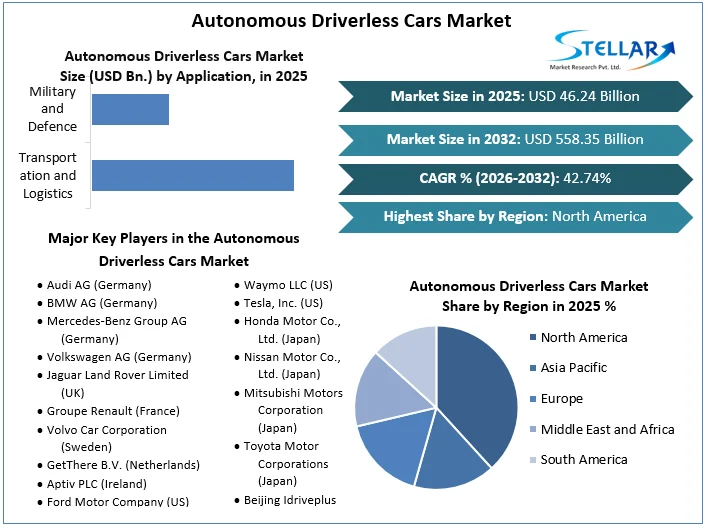

The Autonomous Driverless Cars Market size was valued at USD 46.24 Bn. in 2025 and the total Global Autonomous Driverless Cars revenue is expected to grow at a CAGR of 42.74 % from 2026 to 2032, reaching nearly USD 558.35 Bn. by 2032.

Autonomous Driverless Cars Market Overview

The Autonomous Driverless Car Market has witnessed unprecedented growth, driven by rapid technological advancements and increasing consumer demand for safer, more efficient transportation solutions.

Qualitative factors are also driving the market's growth. Regulatory bodies and governments worldwide are actively promoting the adoption of autonomous vehicles, recognizing their potential to reduce accidents caused by human error, alleviate traffic congestion, and improve overall transportation efficiency. Also, the integration of cutting-edge technologies like artificial intelligence (AI), machine learning, and advanced sensors is enabling automakers to develop increasingly sophisticated and reliable autonomous driving systems, fostering consumer confidence and demand in the market.

Major automotive brands, including Volkswagen, Toyota, General Motors, Ford, Nissan, Daimler (Mercedes-Benz), BMW, Volvo, and Tesla, are at the forefront of this revolutionary market, investing heavily in research and development to stay ahead of the curve.

- In January 2021, Automotive Grade Linux announced that it had included Aicas, AVL, and Citos as new bronze members. AGL is an open-source project at the Linux Foundation that brings together automakers, suppliers, and technology companies to accelerate the development of all vehicle technologies, including autonomous driving.

- In January 2021, automotive technology company Veoneer Inc. and Qualcomm Technologies Inc. signed an agreement under which the companies will collaborate on delivering scalable Advanced Driver Assistance Systems (ADAS) and Collaborative and Autonomous Driving (AD) solutions.

To get more Insights: Request Free Sample Report

Autonomous Driverless Cars Market Dynamics

Technological Advancements and Strategic Partnerships Fuel Growth in Autonomous Driverless Cars Market

The autonomous driverless cars market has been driven by key developments and technological advancements. One significant driver is the continuous enhancement of vehicle safety systems, exemplified by the integration of rear cross traffic alert technology, which enhances safety by detecting vehicles crossing behind a driverless car when backing up. Another major driver is the collaboration between leading automotive and technology companies to improve vehicle capabilities.

- For instance, General Motors and OneD Battery Sciences are working together to enhance the energy density of Ultium battery cells, promising longer ranges and lower costs for electric autonomous vehicles.

- An article published in the Times of India in 2025 mentions that the advent of autonomous vehicle is acting as a renaissance for the automotive industry with an estimated revenue generation of $ 450 Billion to $ 600 Billion globally.

- The recent technological advancements in the fields of artificial intelligence, machine learning, and other sensors like RADAR, LIDAR, GPS, and computer vision, have enabled manufacturers to increase self-driving capabilities in cars.

Also, the market has witnessed significant investments and strategic partnerships aimed at accelerating the development and commercialization of autonomous driving technology. Toyota's substantial investment in Pony.ai and Volkswagen's collaboration with Mobileye Global to introduce Level 4 autonomous vehicles highlight the industry's commitment to advancing self-driving technologies. Also, the launch of new models like the Hyundai Ioniq 5 robotaxi and Citroen's semi-autonomous C5 X SUV demonstrates the increasing availability and sophistication of autonomous vehicles. These innovations and collaborations collectively drive the market by pushing the boundaries of autonomous driving capabilities and fostering consumer confidence in the safety and efficiency of driverless cars.

Technical Limitations and High Development Costs

Achieving full autonomy presents complex technical challenges, requiring sophisticated AI and machine learning algorithms that can handle all driving scenarios. Reliability and safety concerns persist, as autonomous systems must prove their capability to perform flawlessly in diverse conditions. The market also demands substantial R&D investments to innovate and refine these technologies. Furthermore, integrating advanced technologies into vehicles is costly, impacting the overall affordability and market penetration of autonomous cars. These factors collectively slow the pace of adoption and development in the autonomous driverless car market.

Autonomous Driverless Cars Market Trends

- The autonomous cars market has experienced significant advancements driven by ongoing improvements in technology. These include enhancements in sensors, Al algorithms, and connectivity, which are making autonomous driving more reliable and feasible for everyday use. For Instance, Cyngn Inc., announced that it has been granted a new patent in the United States which covers its autonomous vehicle AV solution as well as driver solutions.

- Autonomous vehicles are increasingly being integrated into ride-sharing on-demand models. This integration promises cost reductions for ride-sharing companies, leading to enhanced profitability and scalability. This trend is expected to continue as ride-sharing services incorporate more autonomous vehicles into their fleets.

- Investments in research and development aim to address safety concerns and improve operational efficiency, building consumer trust in autonomous driving systems.

- AVs have the potential of reducing accidents by 90%, amounting to approximately USD 190 billion a year in savings.

- One of the significant trends in the autonomous cars or driverless cars market is the increasing integration of Advanced Driving Assistance Systems (ADAS) aimed at maximizing driving safety.

- There is a growing focus on enhancing safety features and optimizing performance capabilities of autonomous vehicles.

Figure 1. Future of Autonomous Vehicles

Autonomous Driverless Cars Market Segment Analysis

By Level of Automation, According to SMR research, the Level of Automation segment is divided into L1, L2, L3, L4 and L5. Within the level of automation segment, Level 3 has been widely adopted because it offers a good balance between functionality and safety features and estimated to be the leading segment with XXX% market share in 2025. Level 3 systems drive autonomously under limited conditions but still require a human driver to be responsive to take control if needed. This hybrid approach appeals to both automakers and consumers as it incrementally increases autonomous ability while maintaining human oversight for assurance. Level 3 vehicles use advanced driver assistance features for highway driving, but Autonomous driving system still require human monitoring and keep the steering wheel for handling complex situations.

The development of level 3 systems has been given top priority by major automakers as the next step toward full autonomy. The goal is to implement fully automated highway driving in the next five years, which handles all necessary tasks and maintain driver availability for backup in unpredictable circumstances. Consumers also favor level 3 technologies as an affordable way to gain benefits of autonomous driving without requiring complete reliance on Al systems. Increasing capabilities of level 3 promote its highest share of the current autonomous car market until truly driverless cars at levels 4 and 5 can operate without human intervention in all conditions.

Autonomous Driverless Cars Market Regional Analysis

The North America region held the highest market share in 2025 and is expected to grow in the forecast period (2026-2032). The North American region is spearheading the autonomous driverless cars market, driven by the presence of industry giants, substantial investments, and favorable government initiatives. The region's advanced infrastructure, technological prowess, and consumer demand for cutting-edge innovations have fueled the development and deployment of self-driving vehicles. Key players like Tesla, Waymo, and Cruise have made significant strides in autonomous driving technology, contributing to North America's dominance in this burgeoning market. Additionally, the region's focus on safety regulations and ethical considerations have shaped the responsible growth of the autonomous vehicle industry.

- The United States had 42,915 vehicle fatalities in 2023, with 94% of accidents caused by human error. Autonomous cars have the potential to reduce human error and reduce mortality.

- In March 2021, Motional proclaimed that it would be using the all-electric Hyundai IONIQ 5 as the vehicle platform for its next-generation robotaxi. Through its partnership, consumers in select markets to book a Motional robotaxi through the Lyft app starting in 2023. Motional's IONIQ 5 equipped with Level 4 autonomous driving capabilities.

- In February 2021, Vietnam's domestic automaker Vin Fast declared that it had obtained a permit to test autonomous vehicles on California's public streets. The company sought this permit to commercialize its electric vehicles in the US market.

- In April 2021, Honda and Verizon declared that they are working at MCity to explore Verizon 5G Ultra-Wideband and 5G Mobile Edge Compute (MEC). The companies are testing how using Verizon 5G Ultra-Wideband and MEC in the Honda SAFE SWARM can reduce the need for AI onboard each vehicle.

Autonomous Driverless Cars Market Competitive Landscape

The competitive landscape of the autonomous driverless cars market is characterized by intense rivalry among key players striving to innovate and establish market dominance. Companies such as Tesla, Waymo, General Motors, and Ford are at the forefront, investing heavily in research and development to enhance autonomous driving technologies. Strategic partnerships and collaborations are common, as seen with Waymo's partnership with Jaguar for self-driving cars. Also, new entrants and startups are emerging, adding further dynamism and competition to the market.

- In March 2024, Volkswagen Group proclaimed a collaboration with Mobileye Global, a major player in autonomous driving technology. The companies will cooperate to bring Level 4 autonomous vehicles to the commercial market. This collaboration will also focus on integrating Mobileye's self-driving technology into future Volkswagen cars across the group of brands.

- September 2022- In order to significantly increase the energy density of GM's Ultium battery cells for a longer range and lower cost, OneD Battery Sciences and General Motors Co. signed a joint research and development agreement. The Series C funding round for OneD, which the business recently closed at USD 25 million, also included GM Ventures and Volta Energy Technologies.

- In April 2021, Citroen unveiled its new model, C5 X SUV. This new model was offered in both gasoline and plug-in hybrid versions. C5 X offers semi-autonomous Level 2 driving in compliance with current legislation.

- In April 2021, Beijing Hyundai Motor Co. Ltd launched the new Tucson L, a compact crossover SUV. The vehicle is built on the i-GMP platform, and it is equipped with a 1.5 liters turbocharged engine (maximum power output of 147 kW, peak torque of 253 Nm), mated to a 7-speed dual-clutch transmission. The vehicle features the Hyundai Smart Sense system, which includes 23 safety and assistance functions and supports Level 2 autonomous driving.

- In March 2023, Toyota invested USD 500 million in Pony.ai, a Chinese company developing the technology to drive cars and trucks autonomously. This investment will help Pony.ai increase its research and development efforts and accelerate the commercialization of its technology.

- In 2023, Mercedes-Benz introduced the first Level 3 system, Drive Pilot, for sale in the United States, though as of this writing, it’s only approved for use in California and Nevada. Level 3 requires state-by-state approval, and Mercedes is far ahead of any other automaker in this regard, yet the Mercedes system still isn’t “full self-driving” and Mercedes doesn’t market it as such.

- In July 2023, Tesla declared plans to license Full Self-Driving hardware and software to other automakers, and revealed they’re already in talks with one, but didn’t name names. As of early 2024, these plans were still in the works, though Elon Musk told news sources that other automakers were skeptical about this technology.

|

Autonomous Driverless Cars Market Scope |

|

|

Market Size in 2025 |

USD 46.24 Bn. |

|

Market Size in 2032 |

USD 558.35 Bn. |

|

CAGR (2026-2032) |

42.74 % |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segments |

By Type Semi-autonomous Vehicles Fully-autonomous Vehicles |

|

By Level of Autonomy L1 L2 L3 L4 L5 |

|

|

By Component Hardware Software and Services |

|

|

By Application Transportation and Logistics Military and Defence |

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Recent Developments:

- In April 2024, Hyundai loniq 5 robotaxi passed the U.S. driver's licence test. In its campaign film, Hyundai Motor Company showed that IONIQ 5's all-electric and self-driving robotaxi passed a test equivalent to the U.S. driver's license exam with flying colors. This achievement highlights the reliability of the IONIQ 5 robotaxi and the inclusion of its autonomous vehicle technology, highlighting its potential for safe mobility for all.

- October 2023: Rear cross traffic alert: This technology helps the driverless car to detect vehicles crossing behind it when backing up.

Key Player in the Autonomous Driverless Cars

1. Audi AG (Germany)

2. BMW AG (Germany)

3. Mercedes-Benz Group AG (Germany)

4. Volkswagen AG (Germany)

5. Jaguar Land Rover Limited (UK)

6. Groupe Renault (France)

7. Volvo Car Corporation (Sweden)

8. GetThere B.V. (Netherlands)

9. Aptiv PLC (Ireland)

10. Ford Motor Company (US)

11. General Motors Company (US)

12. Waymo LLC (US)

13. Tesla, Inc. (US)

14. Honda Motor Co., Ltd. (Japan)

15. Nissan Motor Co., Ltd. (Japan)

16. Mitsubishi Motors Corporation (Japan)

17. Toyota Motor Corporations (Japan)

18. Beijing Idriveplus Technology Co., Ltd. (China)

19. BYD Auto Co., Ltd. (China)

20. SAIC Motor Corp. (China)

21. Tata Elxsi (India)

22. Hyundai Motor Group (South Korea)

Frequently Asked Questions

The growth of the autonomous driverless cars market is driven by technological advancements, strategic partnerships, increasing consumer acceptance, and supportive regulatory developments.

The range of an autonomous driverless car on a single battery charge varies by model, but many can travel between 250 to 400 miles, with some high-end models exceeding 400 miles.

The Autonomous Driverless Cars Market size was valued at USD 46.24 Billion in 2025 and the total Global Autonomous Driverless Cars revenue is expected to grow at a CAGR of 42.74 % from 2026 to 2032, reaching nearly USD 558.35 Billion by 2032.

The Autonomous Driverless Cars is segmented by Type, Level of Autonomy, Component, Application and Geography.

1. Research Methodology

1.1 Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Research Assumption

2. Autonomous Driverless Cars Market: Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026 – 2032) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Global Autonomous Driverless Cars Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Product Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. Product Launches and Innovations

4. Autonomous Driverless Cars Market: Dynamics

4.1. Autonomous Driverless Cars Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Autonomous Driverless Cars Market Drivers

4.3. Autonomous Driverless Cars Market Restraints

4.4. Autonomous Driverless Cars Market Opportunities

4.5. Autonomous Driverless Cars Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factor

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Analysis

4.8.1. Sensor Fusion Technology

4.8.2. Development of Imaging Radars

4.8.3. Quantum Computing and Self-driving

4.8.4. Development Of AI-based cameras For Self-Driving Vehicles

4.8.5. ADAS Applications

4.8.6. Autonomous Vehicles: Cybersecurity and Data Privacy

4.8.7. Impact of Self-Driving Cars on Ride-Hailing

4.8.8. Self-Driving Vehicles and Vehicle Connectivity

4.8.9. HD Maps Portfolio for All Automation Levels

4.8.10. HD Mapping for Autonomous Vehicle Proving Grounds

4.8.11. Key Suppliers of HD Maps and their Product Details

4.8.12. Technological Roadmap

4.9. Value Chain Analysis and Supply Chain Analysis

4.10. Regulatory Landscape

4.10.1. Market Regulation by Region

4.10.1.1. North America

4.10.1.2. Europe

4.10.1.3. Asia Pacific

4.10.1.4. Middle East and Africa

4.10.1.5. South America

4.10.2. Impact of Regulations on Market Dynamics

4.10.3. Government Schemes and Initiatives

5. Autonomous Driverless Cars Market: Global Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Units) (2025-2032)

5.1. Autonomous Driverless Cars Market Size and Forecast, by Type (2025-2032)

5.1.1. Semi-autonomous Vehicles

5.1.2. Fully-autonomous Vehicles

5.2. Autonomous Driverless Cars Market Size and Forecast, by Level of Autonomy (2025-2032)

5.2.1. L1

5.2.2. L2

5.2.3. L3

5.2.4. L4

5.2.5. L5

5.3. Autonomous Driverless Cars Market Size and Forecast, by Component (2025-2032)

5.3.1. Hardware

5.3.2. Software and Services

5.4. Autonomous Driverless Cars Market Size and Forecast, by Application (2025-2032)

5.4.1. Transportation and Logistics

5.4.2. Military and Defence

5.5. Autonomous Driverless Cars Market Size and Forecast, by Region (2025-2032)

5.5.1. North America

5.5.2. Europe

5.5.3. Asia Pacific

5.5.4. Middle East and Africa

5.5.5. South America

6. North America Autonomous Driverless Cars Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Units) (2025-2032)

6.1. North America Autonomous Driverless Cars Market Size and Forecast, by Type (2025-2032)

6.1.1. Semi-autonomous Vehicles

6.1.2. Fully-autonomous Vehicles

6.2. North America Autonomous Driverless Cars Market Size and Forecast, by Level of Autonomy (2025-2032)

6.2.1. L1

6.2.2. L2

6.2.3. L3

6.2.4. L4

6.2.5. L5

6.3. North America Autonomous Driverless Cars Market Size and Forecast, by Component (2025-2032)

6.3.1. Hardware

6.3.2. Software and Services

6.4. North America Autonomous Driverless Cars Market Size and Forecast, by Application (2025-2032)

6.4.1. Transportation and Logistics

6.4.2. Military and Defence

6.5. North America Autonomous Driverless Cars Market Size and Forecast, by Country (2025-2032)

6.5.1. United States

6.5.2. Canada

6.5.3. Mexico

7. Europe Autonomous Driverless Cars Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Units) (2025-2032)

7.1. Europe Autonomous Driverless Cars Market Size and Forecast, by Type (2025-2032)

7.2. Europe Autonomous Driverless Cars Market Size and Forecast, by Level of Autonomy (2025-2032)

7.3. Europe Autonomous Driverless Cars Market Size and Forecast, by Component (2025-2032)

7.4. Europe Autonomous Driverless Cars Market Size and Forecast, by Application (2025-2032)

7.5. Europe Autonomous Driverless Cars Market Size and Forecast, by Country (2025-2032)

7.5.1. United Kingdom

7.5.2. France

7.5.3. Germany

7.5.4. Italy

7.5.5. Spain

7.5.6. Sweden

7.5.7. Austria

7.5.8. Rest of Europe

8. Asia Pacific Autonomous Driverless Cars Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Units) (2025-2032)

8.1. Asia Pacific Autonomous Driverless Cars Market Size and Forecast, by Type (2025-2032)

8.2. Asia Pacific Autonomous Driverless Cars Market Size and Forecast, by Level of Autonomy (2025-2032)

8.3. Asia Pacific Autonomous Driverless Cars Market Size and Forecast, by Component (2025-2032)

8.4. Asia Pacific Autonomous Driverless Cars Market Size and Forecast, by Application (2025-2032)

8.5. Asia Pacific Autonomous Driverless Cars Market Size and Forecast, by Country (2025-2032)

8.5.1. China

8.5.2. S Korea

8.5.3. Japan

8.5.4. India

8.5.5. Australia

8.5.6. Indonesia

8.5.7. Malaysia

8.5.8. Vietnam

8.5.9. Taiwan

8.5.10. Rest of Asia Pacific

9. Middle East and Africa Autonomous Driverless Cars Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Units) (2025-2032)

9.1. Middle East and Africa Autonomous Driverless Cars Market Size and Forecast, by Type (2025-2032)

9.2. Middle East and Africa Autonomous Driverless Cars Market Size and Forecast, by Level of Autonomy (2025-2032)

9.3. Middle East and Africa Autonomous Driverless Cars Market Size and Forecast, by Component (2025-2032)

9.4. Middle East and Africa Autonomous Driverless Cars Market Size and Forecast, by Application (2025-2032)

9.5. Middle East and Africa Autonomous Driverless Cars Market Size and Forecast, by Country (2025-2032)

9.5.1. South Africa

9.5.2. GCC

9.5.3. Nigeria

9.5.4. Rest of ME&A

10. South America Autonomous Driverless Cars Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Units) (2025-2032)

10.1. South America Autonomous Driverless Cars Market Size and Forecast, by Type (2025-2032)

10.2. South America Autonomous Driverless Cars Market Size and Forecast, by Level of Autonomy (2025-2032)

10.3. South America Autonomous Driverless Cars Market Size and Forecast, by Component (2025-2032)

10.4. South America Autonomous Driverless Cars Market Size and Forecast, by Application (2025-2032)

10.5. South America Autonomous Driverless Cars Market Size and Forecast, by Country (2025-2032)

10.5.1. Brazil

10.5.2. Argentina

10.5.3. Rest Of South America

11. Company Profile: Key Players

11.1. Audi AG (Germany)

11.1.1. Company Overview

11.1.2. Product Portfolio

11.1.2.1. Product Name

11.1.2.2. Product Details (Price, Features, etc.)

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. BMW AG (Germany)

11.3. Mercedes-Benz Group AG (Germany)

11.4. Volkswagen AG (Germany)

11.5. Jaguar Land Rover Limited (UK)

11.6. Groupe Renault (France)

11.7. Volvo Car Corporation (Sweden)

11.8. GetThere B.V. (Netherlands)

11.9. Aptiv PLC (Ireland)

11.10. Ford Motor Company (US)

11.11. General Motors Company (US)

11.12. Waymo LLC (US)

11.13. Tesla, Inc. (US)

11.14. Honda Motor Co., Ltd. (Japan)

11.15. Nissan Motor Co., Ltd. (Japan)

11.16. Mitsubishi Motors Corporation (Japan)

11.17. Toyota Motor Corporations (Japan)

11.18. Beijing Idriveplus Technology Co., Ltd. (China)

11.19. BYD Auto Co., Ltd. (China)

11.20. SAIC Motor Corp. (China)

11.21. Tata Elxsi (India)

11.22. Hyundai Motor Group (South Korea)

11.23. XXX.Inc

12. Key Findings

13. Analyst Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook