Automotive Smart Display Market - Global Industry Analysis and Forecast (2026-2032) by Service Type, Dynamics, segment Analysis

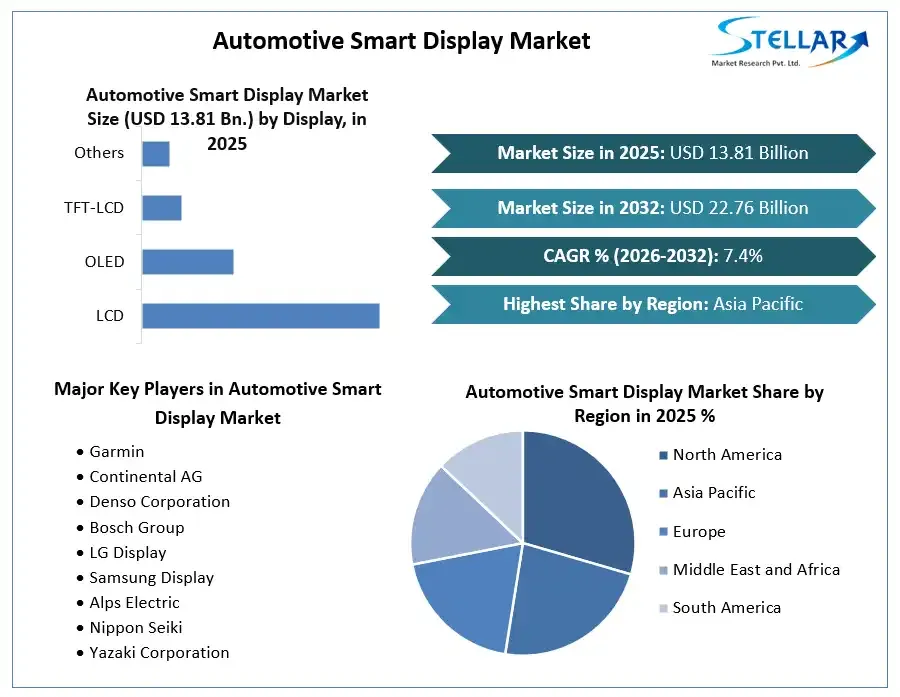

Automotive Smart Display Market size was valued at USD 13.81Bn. in 2025 and is expected to reach USD 22.76 Bn. by 2032, at a CAGR of 7.4 % forecast year.

Global Automotive Smart display market Overview

Autonomous vehicles and semi-autonomous vehicles are high in demand due to segments involved for rising of the market. Unlike a smart speaker, a smart displays touchscreen lets you refine your command and gives you better results faster. Plus, perks like following recipes, acting as a photo frames or even using the device as a clock when other features aren’t being utilized, are all exclusive to the smart screen. The increasing demand for improved in vehicle experience and the changing consumer buying behaviour, along with the growth of luxury, premium, and high end cars worldwide.

To get more Insights: Request Free Sample Report

The surge in demand for vehicle navigation and connectivity systems in the automotive sector led to a growth in the usage of automotive visualization technology. Visualization technology has played a significant role in advancement of the cockpit technology, which has led to the incorporation of interactive and smart display in several vehicles launched by prominent automakers such as jaguar, land rover, Mercedes Benz, Volkswagen, Audi, and bmw.

Global Automotive Smart Display Market Drivers

Factors that are driving the automotive smart display market growth include the demand for semi-autonomous and autonomous vehicles, demand for improved consumer experience in vehicles, and high growth in the luxury and high end cars segments

The syncing of smartphones with infotainment systems, such as android auto, spotify, and apple car play, will increase the demand for smart displays in vehicles. Both apple car play and android auto are similar in that they involve the usage of smartphones to run the operating systems, which have been optimized for road applications. The system enable easy navigation, integration of advanced features with cockpit electronics, easy access to music, phone call management etc. all of which without distracting the driver. Both the operating systems even integrate voice assistants, such as apple Siri and Google assistant, to deliver a hands free experience. Cars must have the correct kit to run the operating systems, and more manufacturer are embracing them, often allowing a support features as a standard inclusion on their infotainment systems or at least as an option.

Global Automotive Smart Display Market opportunities and growth

The 5g technologies is expected to create more opportunities for the automotive smart display market. 5g offers high speed internet, which helps in integrating automotive smart display systems with innovative applications, such as virtual reality, augmented reality, cloud gaming and media streaming. These applications will require better quality display screens, which will trigger the demand for automotive smart displays. The 5g enables the integration of automotive applications with smart display systems. Hence, large size integrated display panels will be required in vehicles, instead of the conventional dashboards. AR and VR devices leverage 5g to offer a better experiences. Both AR and VR devices require higher resolution panels for a display to offer better performance. Compared to 4g LTE technology, 5g offers a faster speed of up to 5 times and 10 times lower latency.

The automobile industry developing newly advanced technologies and facilitating information on the display for easy access, convenience and luxurious look of the vehicle boost the market growth. Automated vehicles less human control and more robotic developments inculcated in vehicles.

Global Automotive Smart Display Market restraining factors

Globally, with the rapid adoption of advanced technologies, the majority of modern vehicles are equipped with the latest features that usually use wireless technologies which ultimately increase of cyber-attacks. Further, increased vehicles connectivity through various devices such as smartphones, navigation systems, tablets, and music player also heightens the network breaching risk in vehicles. When these portable devices are connected to vehicle, malicious software and viruses may attack the electronic systems through the vehicle information terminal or vehicle entertainment system.

Excessive and vulnerable connections also increase the threat of being hacked. Since security and privacy are the foundations of telematics offerings, the current global economic situations shows that the inclination of people is shifting towards advanced technologies. The information collected may be misused through telematics.

Global Automotive Smart Display Market challenges

The automatic smart display market is still in its early stages of development and faces a number of challenges, such as high cost, complexity, lack of standards, security and privacy concerns etc. and some general challenges are limited functionality, reliability issues, lack of consumer awareness, and others.

The cost of automatic smart display is still relatively high, which can be barrier to adoption for consumers. Automatic smart displays are complex devices that rely on variety of technologies, including AI, computer vision, and machine learning. This complexity can make it difficult to develop and maintain reliable and affordable products. The automatic smart displays collect a lot of data about users which raises concerns about security and privacy. Users need to be confident that their data is being protected and used responsibly.

Global Automotive Smart Display Market Regional insights.

Based on region, the market is segmented into North America, Europe, Asia Pacific, Latin America and Middle East & Africa (MEA). North America region is further bifurcated into countries such as U.S., and Canada. Asia Pacific emerged as the largest market for automotive smart display market with 40 % share of the market revenue in 2025.

The Europe region is further categorized into U.K., France, Germany, Italy, Spain, Russia, and Rest of Europe. After Asia Pacific, North America contributed 30 % to globally worldwide. The Europe region is further categorized into U.K., France, Germany, Italy, Spain, Russia, and Rest of Europe. After North America, Europe contributed 20% to globally worldwide. Latin America region is further segmented into Brazil, Mexico, and Rest of Latin America, and the MEA region is further divided into GCC, Turkey, South Africa, and Rest of MEA.

Global Automotive Smart Display Market Segment Analysis

This report forecasts revenue growth at global, regional and country levels and provides analysis of the latest industry trends and opportunities in each of the sub segments from 2025 to 2032. For this study, stellar market research has segmented the Global Automotive smart display report based on by vehicle class, by display type, by electric vehicle, by application and by vehicle type.

The luxury vehicle class is expected to dominate the automotive smart display market in the coming years by vehicle class, the centre stack displays segment is expected to account for the largest share of industry of by display type. The BEV segment is expected to witness the fastest growth in the coming years by electric vehicle. Passenger cars are expected to account for largest share by vehicle type.

Global Automotive Smart Display Market Competitive Landscape

The competitive analysis of the Market includes the Market size, growth rate and key trends. The report provides information about the Key companies, such as their size, display market services, Global automotive smart display market share, and geographic presence. The report provides such type of competitive landscape of all Key Players to assist new market entrants. The report provides such type of competitive landscape of all Global automotive smart display market Key Players to assist new market entrants. The report offers Competitive benchmarking of the Global automotive smart display market through the Market revenue, share and size of the key players.

The key players in automotive smart display are, Garmin, jabil, Nippon seiki, Flextronics, Samsung display, continental AG, BOSCH Group, LG Display. These players are focusing on expanding their product portfolio, investing in research and development, and expanding their distribution channels to gain a competitive edge in the market.

|

Automotive Smart Display Market Scope |

|

|

Market Size in 2025 |

USD 13.81 Bn. |

|

Market Size in 2032 |

USD 22.76 Bn. |

|

CAGR (2026-2032) |

7.4% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segment scope |

By Vehicle Class

|

|

By Display Type

|

|

|

By Electric Vehicle

|

|

|

By Application

|

|

|

By Vehicle Type

|

|

Global Automotive Smart Display Market Key Players

- Continental AG

- Denso Corporation

- Bosch Group

- LG Display

- Samsung Display

- Alps Electric

- Nippon Seiki

- Yazaki Corporation

- Jabil

- Flextronics

- Harman International

- Garmin

- Gentex Corporation

- Magna International

- Panasonic Corporation

- Visteon Corporation

Frequently Asked Questions

Asia Pacific is expected to dominate the Global automotive smart display market during the forecast period.

The Global automotive smart display market is expected to reach USD 22.76 Bn by 2032.

The major top players in the Global automotive smart display market are, Bosch, continental, DENSO, Pioneer, Yazaki, HARMAN, LG Electronics, Visteon, and others.

Factors that are driving the automotive smart display market growth include the demand for semi-autonomous and autonomous vehicles, demand for improved consumer experience in vehicles, and high growth in the luxury and high end cars segments.

1. Global Automotive smart display Market: Research Methodology

2. Global Automotive smart display Market: Executive Summary

3. Global Automotive smart display Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Competitive Landscape

3.3. Key Players Benchmarking

3.4. Market Structure

3.4.1. Market Leaders

3.4.2. Market Followers

3.4.3. Emerging Players

3.5. Consolidation of the Market

4. Global Automotive smart display Market: Dynamics

4.1. Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Market Drivers by Region

4.2.1. North America

4.2.2. Europe

4.2.3. Asia Pacific

4.2.4. Middle East and Africa

4.2.5. South America

4.3. Market Restraints

4.4. Market Opportunities

4.5. Market Challenges

4.6. PORTER’s Five Forces Analysis

4.7. PESTLE Analysis

4.8. Value Chain Analysis

4.9. Regulatory Landscape by Region

4.9.1. North America

4.9.2. Europe

4.9.3. Asia Pacific

4.9.4. Middle East and Africa

4.9.5. South America

5. Global Automotive smart display Market Size and Forecast by Segments (by Value USD and Volume Units)

5.1. Global Automotive smart display Market Size and Forecast, By vehicle class(2026-2032)

5.1.1. Economy

5.1.2. Mid segment

5.1.3. Luxury

5.2. Global Automotive smart display Market Size and Forecast, By display type (2026-2032)

5.2.1. LCD

5.2.2. OLED

5.2.3. TFT-LCD

5.2.4. Others

5.3. Global Automotive smart display Market Size and Forecast, By electric vehicle (2026-2032)

5.3.1. BEV

5.3.2. FCEV

5.3.3. HEV

5.3.4. PHEV

5.4. Global Automotive smart display Market Size and Forecast, By application (2026-2032)

5.4.1. Center stack

5.4.2. Digital instrument cluster

5.4.3. Head up display

5.4.4. Rear seat entertainment

5.5. Global Automotive smart display Market Size and Forecast, By vehicle type (2026-2032)

5.5.1. Passenger car

5.5.2. Light commercial vehicle

5.5.3. Heavy commercial vehicle

5.6. Global Automotive smart display Market Size and Forecast, by Region (2026-2032)

5.6.1. North America

5.6.2. Europe

5.6.3. Asia Pacific

5.6.4. Middle East and Africa

5.6.5. South America

6. North America Global Automotive smart display Market Size and Forecast (by Value USD and Volume Units)

6.1. North America Global Automotive smart display Market Size and Forecast, By vehicle class(2026-2032)

6.1.1. Economy

6.1.2. Mid segment

6.1.3. Luxury

6.2. North America Global Automotive smart display Market Size and Forecast, By display type (2026-2032)

6.2.1. LCD

6.2.2. OLED

6.2.3. TFT-LCD

6.2.4. Others

6.3. North America Global Automotive smart display Market Size and Forecast, By electric vehicle (2026-2032)

6.3.1. BEV

6.3.2. FCEV

6.3.3. HEV

6.3.4. PHEV

6.4. North America Global Automotive smart display Market Size and Forecast, By application (2026-2032)

6.4.1. Center stack

6.4.2. Digital instrument cluster

6.4.3. Head up display

6.4.4. Rear seat entertainment

6.5. North America Global Automotive smart display Market Size and Forecast, By vehicle type (2026-2032)

6.5.1. Passenger car

6.5.2. Light commercial vehicle

6.5.3. Heavy commercial vehicle

6.6. North America Global Automotive smart display Market Size and Forecast, by Country (2026-2032)

6.6.1. United States

6.6.2. Canada

6.6.3. Mexico

7. Europe Global Automotive smart display Market Size and Forecast (by Value USD and Volume Units)

7.1. Europe Global Automotive smart display Market Size and Forecast, By vehicle class(2026-2032)

7.1.1. Economy

7.1.2. Mid segment

7.1.3. Luxury

7.2. Europe Global Automotive smart display Market Size and Forecast, By display type (2026-2032)

7.2.1. LCD

7.2.2. OLED

7.2.3. TFT-LCD

7.2.4. Others

7.3. Europe Global Automotive smart display Market Size and Forecast, By electric vehicle (2026-2032)

7.3.1. BEV

7.3.2. FCEV

7.3.3. HEV

7.3.4. PHEV

7.4. Europe Global Automotive smart display Market Size and Forecast, By application (2026-2032)

7.4.1. Center stack

7.4.2. Digital instrument cluster

7.4.3. Head up display

7.4.4. Rear seat entertainment

7.5. Europe Global Automotive smart display Market Size and Forecast, By vehicle type (2026-2032)

7.5.1. Passenger car

7.5.2. Light commercial vehicle

7.5.3. Heavy commercial vehicle

7.6. Europe Global Automotive smart display Market Size and Forecast, by Country (2026-2032)

7.6.1. UK

7.6.2. France

7.6.3. Germany

7.6.4. Italy

7.6.5. Spain

7.6.6. Sweden

7.6.7. Austria

7.6.8. Rest of Europe

8. Asia Pacific Global Automotive smart display Market Size and Forecast (by Value USD and Volume Units)

8.1. Asia Pacific Global Automotive smart display Market Size and Forecast, By vehicle class(2026-2032)

8.1.1. Economy

8.1.2. Mid segment

8.1.3. Luxury

8.2. Asia Pacific Global Automotive smart display Market Size and Forecast, By display type (2026-2032)

8.2.1. LCD

8.2.2. OLED

8.2.3. TFT-LCD

8.2.4. Others

8.3. Asia Pacific Global Automotive smart display Market Size and Forecast, By electric vehicle (2026-2032)

8.3.1. BEV

8.3.2. FCEV

8.3.3. HEV

8.3.4. PHEV

8.4. Asia Pacific Global Automotive smart display Market Size and Forecast, By application (2026-2032)

8.4.1. Center stack

8.4.2. Digital instrument cluster

8.4.3. Head up display

8.4.4. Rear seat entertainment

8.5. Asia Pacific Global Automotive smart display Market Size and Forecast, By vehicle type (2026-2032)

8.5.1. Passenger car

8.5.2. Light commercial vehicle

8.5.3. Heavy commercial vehicle

8.6. Asia Pacific Global Automotive smart display Market Size and Forecast, by Country (2026-2032)

8.6.1. China

8.6.2. S Korea

8.6.3. Japan

8.6.4. India

8.6.5. Australia

8.6.6. Indonesia

8.6.7. Malaysia

8.6.8. Vietnam

8.6.9. Taiwan

8.6.10. Bangladesh

8.6.11. Pakistan

8.6.12. Rest of Asia Pacific

9. Middle East and Africa Global Automotive smart display Market Size and Forecast (by Value USD and Volume Units)

9.1. Middle East and Africa Global Automotive smart display Market Size and Forecast, By vehicle class(2026-2032)

9.1.1. Economy

9.1.2. Mid segment

9.1.3. Luxury

9.2. Middle East and Africa Global Automotive smart display Market Size and Forecast, By display type (2026-2032)

9.2.1. LCD

9.2.2. OLED

9.2.3. TFT-LCD

9.2.4. Others

9.3. Middle East and Africa Global Automotive smart display Market Size and Forecast, By electric vehicle (2026-2032)

9.3.1. BEV

9.3.2. FCEV

9.3.3. HEV

9.3.4. PHEV

9.4. Middle East and Africa Global Automotive smart display Market Size and Forecast, By application (2026-2032)

9.4.1. Center stack

9.4.2. Digital instrument cluster

9.4.3. Head up display

9.4.4. Rear seat entertainment

9.5. Middle East and Africa Global Automotive smart display Market Size and Forecast, By vehicle type (2026-2032)

9.5.1. Passenger car

9.5.2. Light commercial vehicle

9.5.3. Heavy commercial vehicle

9.6. Middle East and Africa Global Automotive smart display Market Size and Forecast, by Country (2026-2032)

9.6.1. South Africa

9.6.2. GCC

9.6.3. Egypt

9.6.4. Nigeria

9.6.5. Rest of ME&A

10. South America Global Automotive smart display Market Size and Forecast (by Value USD and Volume Units)

10.1. South America Global Automotive smart display Market Size and Forecast, By vehicle class(2026-2032)

10.1.1. Economy

10.1.2. Mid segment

10.1.3. Luxury

10.2. South America Global Automotive smart display Market Size and Forecast, By display type (2026-2032)

10.2.1. LCD

10.2.2. OLED

10.2.3. TFT-LCD

10.2.4. Others

10.3. South America Global Automotive smart display Market Size and Forecast, By electric vehicle (2026-2032)

10.3.1. BEV

10.3.2. FCEV

10.3.3. HEV

10.3.4. PHEV

10.4. South America Global Automotive smart display Market Size and Forecast, By application (2026-2032)

10.4.1. Center stack

10.4.2. Digital instrument cluster

10.4.3. Head up display

10.4.4. Rear seat entertainment

10.5. South America Global Automotive smart display Market Size and Forecast, By vehicle type (2026-2032)

10.5.1. Passenger car

10.5.2. Light commercial vehicle

10.5.3. Heavy commercial vehicle

10.6. South America Global Automotive smart display Market Size and Forecast, by Country (2026-2032)

10.6.1. Brazil

10.6.2. Argentina

10.6.3. Rest of South America

11. Company Profile: Key players

11.1. Continental AG

11.1.1. Company Overview

11.1.2. Financial Overview

11.1.3. Business Portfolio

11.1.4. SWOT Analysis

11.1.5. Business Strategy

11.1.6. Recent Developments

11.2. Deso corporation

11.3. Bosch Group

11.4. LG Display

11.5. Samsung Display

11.6. Alps Electric

11.7. Nippon Seiki

11.8. Yazaki Corporation

11.9. Jabil

11.10. Flextronics

11.11. Harman International

11.12. Garmin

11.13. Gentex Corporation

11.14. Magna International

11.15. Panasonic Corporation

11.16. Visteon Corporation

12. Key Findings

13. Industry Recommendation