Automotive Semiconductor Market- Global Industry Analysis by Market Share, Trend, Size, Competitive Landscape, Regional Outlook and Forecast 2026-2034

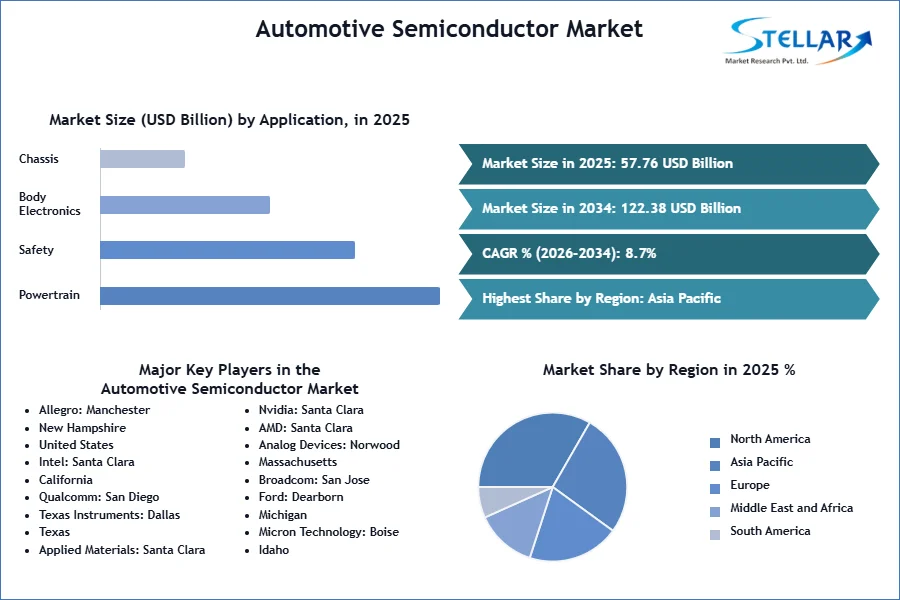

Global Automotive Semiconductor Market size was valued at USD 57.76 Bn. in 2025 and is expected to reach USD 122.38 Bn. by 2034, at a CAGR of 8.7%.

Automotive Semiconductor Market Overview

Automotive semiconductors are specialized components used in vehicles for functions such as body electronics, power electronics, chassis systems, safety features, and comfort and entertainment units. With a conductivity level between conductors and insulators, these semiconductors have enabled features like cell phone connectivity, heads-up displays, autonomous driving assistance, and enhanced comfort and performance in vehicles. In 2025, the global automotive semiconductor market was valued at USD 57.76 billion and is projected to grow at a compound annual growth rate (CAGR) of 8.7% from 2026 to 2034. This growth is driven by the increasing penetration of electronic components across all car segments, the adoption of electronic control units (ECUs) in modern vehicles, and a growing focus on vehicular safety systems.

Other factors contributing to market growth include the rise of connected cars, advanced infotainment systems, stringent automotive safety systems, and fuel efficiency standards. The growing demand for electric and hybrid vehicles presents a significant opportunity for the automotive semiconductor market. These vehicles rely on semiconductors for devices such as Advanced Driver Assistance Systems (ADAS) and ECUs to manage batteries, motors, and other critical components, creating a demand for sophisticated and specialized semiconductors. These advancements are expected to impact the supply chain, aftermarket, and manufacturers of semiconductor electronic components. Traditional diagnostic systems is replaced by onboard diagnostic systems, enabling continuous monitoring of a vehicle's mechanical and electrical components, thus ensuring higher efficiency and reliability in vehicle performance.

To get more Insights: Request Free Sample Report

Automotive Semiconductor Market Dynamics

Increasing Vehicle Electrification to Drive the Market Growth

The automotive semiconductor market is divided into multiple components and several players are entering the space to fill the demand for the technology’s adoption such as Texas Instruments, ROHM, Renesas Electronics, NXP Semiconductors, Intel, and Nvidia, etc. The advancements on the technical and partnerships end together shaping the future of technology. For instance, Toshiba Electronic Devices & Storage Corporation ("Toshiba") has started volume shipments of the SmartMCD™ Series of gate driver ICs with embedded microcontroller (MCU). The first product, "TB9M003FG," is suitable for sensorless control of three-phase brushless DC motors used in automotive applications, including water and oil pumps, fans and blowers. The growing popularity of electric vehicles and driverless vehicles have called for semiconductor technology advancements in the automotive industry, ones that would make the space smarter and energy efficient.

Innovations in semiconductor technology enable faster charging, longer battery life, and improved vehicle range, making EVs more appealing to consumers. The government incentives and stringent emission regulations worldwide are propelling automakers to invest heavily in EV technology, thereby boosting the automotive semiconductor market. The ongoing advancements in EV infrastructure, such as the expansion of charging networks, further stimulate the demand for automotive semiconductors, cementing their crucial role in the future of transportation. The shift towards electric vehicles (EVs) is a primary growth driver for the automotive semiconductor market.

The sales of electric cars are expected to maintain a robust trajectory throughout 2025. In the first quarter of 2024, more than 2.3 million electric vehicles were sold, demonstrating a remarkable 25% increase compared to last year. As the world seeks to reduce carbon emissions, the demand for EVs has surged, necessitating advanced semiconductor components. These semiconductors are essential for battery management systems, power electronics, and electric drivetrains, ensuring efficient energy usage and performance.

Government support has emerged as a crucial factor in accelerating the switch to electric cars (EVs) and promoting a sustainable transportation environment. Governments worldwide are putting in place various legislative measures to encourage the adoption of EVs as the world struggles with environmental issues and attempts to cut carbon emissions. These steps include financial incentives like tax credits, rebates, grants, and legislative and regulatory actions to encourage EV production, sales, and charging infrastructure development. Governments accelerate the transition to cleaner transportation by strongly supporting and funding electric mobility. They also help to create a future in which sustainable mobility is both a reality and a top priority.

Ways to Promote the Growth of EV Charging Infrastructure

In the FAME India scheme, the Ministry of Heavy Industries has sanctioned the construction of 2,877 EV charging stations across multiple states, as well as 1,576 stations across 16 highways and 9 expressways. These major roads cover 10,275 kilometers across India, and providing sufficient charging stations along them will significantly reduce range anxiety.

Public and private sector investments in charging infrastructure, driven by the recognition that EVs are vital in combating climate change and promoting sustainable mobility. For example, in the United States, the Biden administration has pledged to deploy 500,000 new public charging outlets by 2034. Similarly, in Europe, the EU aims to install a million public charging points by the same year. Such factors are expected to drive the Automotive Semiconductor Market growth.

The increasing popularity of electric vehicles (EVs) is transforming the automotive industry, as consumers and governments become more aware of the environmental benefits of electric mobility. As EVs become more accessible and affordable, significant efforts are being directed towards building efficient and comprehensive EV charging infrastructure. The increasing number of public charging stations per 1000 plug-in electric passenger cars significantly supports the automotive semiconductor industry. This infrastructure expansion boosts EV adoption, driving demand for semiconductors used in EV power electronics, battery management systems, and charging systems. As more charging stations are deployed, the need for advanced semiconductor technologies to manage and optimize these systems grows, positively impacting the Automotive Semiconductor Market growth and innovation.

Advancement in Autonomous Driving Systems to Boost the Market

The development of autonomous vehicles (AVs) is revolutionizing the automotive industry, with semiconductors playing a pivotal role. These vehicles rely on sensors, cameras, and artificial intelligence (AI) systems to navigate and make decisions, all of which require advanced semiconductor solutions. High-performance processors, memory chips, and specialized integrated circuits enable the real-time data processing and complex algorithms necessary for autonomous driving. The increasing investment in AV technology by major automakers and tech companies underscores the significant growth potential in this sector. As consumer interest in self-driving cars grows, driven by the promise of enhanced safety and convenience, the demand for cutting-edge semiconductor components is set to soar.

The race towards fully autonomous vehicles is thus a key driver of the automotive semiconductor market. Advanced Driver Assistance Systems (ADAS) transform driving with features like adaptive cruise control and automatic emergency braking. These systems depend on advanced semiconductors for real-time data processing and control. Rising consumer demand for safer vehicles and regulatory road safety mandates drive ADAS adoption, creating significant growth opportunities in the automotive semiconductor Industry.

The surge in demand for connected and smart vehicles is another major growth driver for the automotive semiconductor market. Modern vehicles are increasingly equipped with advanced connectivity features, including infotainment systems, navigation, and telematics, all of which require robust semiconductor solutions. These components enable seamless communication between the vehicle and external networks, enhancing the driving experience with real-time information and entertainment options.

The rise of the Internet of Things (IoT) and 5G technology is further propelling the integration of connectivity features in vehicles, demanding more sophisticated and high-performance semiconductors. Consumers' growing expectations for in-car connectivity and smart functionalities are compelling automakers to continuously innovate, driving significant growth in the semiconductor market. The evolution of connected car technology is set to redefine the automotive landscape, creating new opportunities for semiconductor manufacturers.

Smart Vehicle Revolution to Support the Growth of the Market

The rise of connected vehicles and the integration of Internet of Things (IoT) technologies are pivotal growth drivers for the automotive semiconductor market. For instance, Tesla's potential rollout of its Full Self-Driving (FSD) system in China ignite a new era of innovation in the Chinese electric vehicle (EV) market. During Elon Musk's visit to Beijing in April 2025, Tesla announced a partnership with Baidu for data collection, complying with China's data privacy regulations. This move is expected to stimulate the 'catfish effect,' where Tesla's advanced autonomous technology pressures Chinese EV startups to accelerate their research and development efforts. This dynamic mirrors the surge in EV advancements following Tesla's Shanghai plant approval in 2020, which spurred BYD and others to ramp up production and innovation.

Industry experts predict that Tesla's FSD deployment catalyze a decade-long competition among Chinese automakers to dominate the smart EV sector, fostering rapid advancements and positioning China as a leader in autonomous vehicle technology. Modern vehicles are increasingly becoming connected hubs, equipped with communication systems that enable real-time data exchange with other vehicles, infrastructure, and cloud services. This connectivity enhances navigation, entertainment, maintenance, and overall driving experience. Semiconductors play a crucial role in enabling these functionalities, from wireless communication chips to data processing units. The expansion of 5G networks further accelerates this trend, offering higher bandwidth and lower latency. As the automotive industry moves towards smarter, more connected vehicles, the demand for advanced semiconductor solutions continue to rise, driving Automotive Semiconductor industry growth.

Sustainable Mobility Solutions and Eco-Friendly Innovations to Create Lucrative Opportunity in the Market

The push towards sustainable mobility solutions offers another compelling opportunity for the automotive semiconductor market. With increasing environmental concerns and regulatory pressures, the automotive industry is focused on developing eco-friendly vehicles, including EVs, hybrid vehicles, and fuel cell vehicles. Semiconductors are critical in optimizing the efficiency and performance of these green technologies. Innovations in power management, energy storage, and electronic control units (ECUs) are essential to achieving higher energy efficiency and lower emissions.

As the world prioritizes sustainability, semiconductor companies that deliver innovative, energy-efficient solutions find significant growth opportunities in this evolving market, positioning themselves as key players in the green automotive revolution. India has set ambitious goals for electric vehicle (EV) adoption, aiming for 80% of two-wheeler and three-wheeler vehicles, 70% of commercial cars, 40% of buses, and 30% of private car sales to be electric by 2034.

Automotive Semiconductor Market Segment Analysis

By Component: Based on components, the Analog IC segment held the largest Automotive Semiconductor Market share in 2025. Electronics are the primary differentiators among competing automakers, with each vehicle typically housing hundreds of sensors, dozens of electronic control units (ECUs), extensive cable harnesses, and complex network systems. Analog ICs play a crucial role in supporting these processors, power devices, sensors, and other electronic components, enabling the transfer of control instructions and signals between systems, thereby driving significant growth in the automotive semiconductor industry.

The increasing electrification of powertrains is generating substantial demand for power devices and creating significant growth opportunities for Analog ICs. The market for logic ICs and connectivity devices is also expanding under the Analog ICs segment. Key Analog ICs used in vehicles include amplifiers, interfaces, converters, comparators, ASICs, ASSPs, regulators, drivers, logic ICs, as well as infotainment, telematics, and connectivity devices. This broad application range underscores the importance and growth potential of Analog ICs in the automotive sector.

by Vehicle Type: In 2025, the Passenger Car segment dominated the Automotive Semiconductor Market and is expected to maintain the largest market share over the forecast period. This segment includes sedans, hatchbacks, station wagons, sport utility vehicles (SUVs), multi-utility vehicles (MUVs), and vans, making it the largest segment in terms of production and demand globally. As such, it presents the most promising market for automotive semiconductors.

Passenger cars, primarily equipped with gasoline-powered engines, constitute the largest segment in the automotive industry. In China, however, there is a higher demand for electric-powered passenger vehicles compared to the rest of the world. Electric and hybrid vehicles have a higher semiconductor content than conventional passenger cars, especially in the powertrain. The growing environmental concerns are driving the demand for electric and hybrid vehicles, creating significant opportunities for automotive semiconductor manufacturers to innovate and increase their market presence.

Automotive Semiconductor Market Regional Analysis

Asia Pacific dominated the largest Automotive Semiconductor Market share in 2025. This growth is driven by the expansion of the automotive industry, particularly in emerging economies such as India, China, and Japan. The booming e-commerce industry in the region is anticipated to increase the demand for commercial vehicles. This surge in commercial vehicle manufacturing is expected to drive the usage of automotive semiconductors and boost market growth.

In 2025, China's auto sales surged by 12% to 30.09 million vehicles, with exports nearing 5 million, solidifying its position as the world's leading auto exporter, surpassing Japan. China led global advancements in electric and new-energy vehicles, with a 38% rise in sales to 9.49 million vehicles. New-energy vehicles, including plug-in hybrids and fuel cell vehicles, significantly boost China's automotive semiconductor market. Electric vehicles (EVs) and autonomous vehicles require more semiconductors than traditional cars. A Chinese automaker reported that EVs use about 1,300 semiconductors each, compared to 500 in gasoline-powered cars.

With government support, Chinese automakers like Zhejiang Geely Holding Group are developing their own semiconductors, enhancing market growth. However, domestic production of power semiconductors meets only 15% of demand, and advanced chip production for autonomous driving is less than 5%. Despite having around 300 companies in automotive semiconductor development, China relies heavily on imports, with global leadership held by Infineon Technologies, NXP Semiconductors, Renesas Electronics, and Texas Instruments. Meanwhile, Japan's Leading-edge Semiconductor Technology Center aims to boost annual semiconductor revenue to over ¥13 trillion by 2034.

Automotive Semiconductor Market Competitive Landscape Analysis

The automotive semiconductor market is marked by strategic acquisitions, collaborations, and partnerships as major players seek to expand their business and capitalize on emerging opportunities. NXP Semiconductors, for instance, partnered with Hailo in December 2021 to integrate AI solutions into automotive ECUs, combining NXP's processors with Hailo's AI processor. Infineon Technologies has been proactive, securing a supply agreement with GT Advanced Technologies in November 2020 to enhance its silicon carbide (SiC) capabilities, crucial for power semiconductors.

The Japanese government is also attracting semiconductor giants like ASML, TSMC, Samsung, and Mitsubishi Chemical Group, significantly boosting its market. In 2024, Infineon Technologies maintained its leadership with a market share increase of 14%, dominating key automotive applications. MediaTek's partnership with NVIDIA aims to revolutionize in-car experiences through AI and accelerated computing. Intel's entry into the market with new automotive AI chips and the acquisition of Silicon Mobility in January 2025 further intensifies competition with rivals NVIDIA and Qualcomm. These strategic moves underscore the dynamic and competitive nature of the automotive semiconductor market.

Conclusion: The automotive semiconductor market is experiencing robust growth driven by the increasing electrification of vehicles, advancements in autonomous driving systems, and the rise of connected and smart vehicles. The demand for semiconductors in electric and hybrid vehicles, essential for managing batteries, motors, and critical components, is escalating. Governments worldwide are supporting EV adoption through incentives and infrastructure development, further propelling market growth. Autonomous vehicle technology and advanced driver assistance systems (ADAS) are revolutionizing the industry, requiring high-performance semiconductor solutions.

The Asia Pacific region, particularly China, is leading in automotive advancements, with significant growth in electric and new-energy vehicles. Despite the high demand, domestic production in China remains low, relying heavily on imports. Companies like Infineon, NXP, and Renesas dominate the market. Overall, the push towards sustainable mobility, smart vehicle innovations, and government support are key factors driving the automotive semiconductor market's growth.

Automotive Semiconductor Market Scope

|

Automotive Semiconductor Market |

|

|

Market Size in 2025 |

USD 57.76 Bn. |

|

Market Size in 2034 |

USD 122.38 Bn. |

|

CAGR (2026- 2034) |

8.7 % |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Automotive Semiconductor Market Segments |

By Component

|

|

By Vehicle Type

|

|

|

By Propulsion Type

|

|

|

By Application

|

|

Automotive Semiconductor Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, ASEAN, Pakistan and Rest of APAC)

South America (Brazil, Argentina Rest of South America)

Middle East & Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

Automotive Semiconductor Market Key players

North America

- Allegro: Manchester, New Hampshire, United States

- Intel: Santa Clara, California, United States

- Qualcomm: San Diego, California, United States

- Texas Instruments: Dallas, Texas, United States

- Applied Materials: Santa Clara, California, United States

- Nvidia: Santa Clara, California, United States

- AMD: Santa Clara, California, United States

- Analog Devices: Norwood, Massachusetts, United States

- Broadcom: San Jose, California, United States

- Ford: Dearborn, Michigan, United States

- Micron Technology: Boise, Idaho, United States

Asia-Pacific:

- Fuji Electric: Tokyo, Japan

- Renesas: Tokyo, Japan

- Toshiba: Tokyo, Japan

- DENSO: Kariya, Japan

- MosChip Technologies: Hyderabad, India

- ROHM: Kyoto, Japan

- TSMC: Hsinchu, Taiwan

- Tata Elxsi: Bangalore, India

Europe

- NXP: Eindhoven, Netherlands

- Infineon: Neubiberg, Germany

- Robert Bosch GmbH: Gerlingen, Germany

- STMicroelectronics: Geneva, Switzerland

- ASM Technologies: Almere, Netherlands

Frequently Asked Questions

Asia Pacific is expected to dominate the Automotive Semiconductor market during the forecast period.

The Automotive Semiconductor market size is expected to reach USD 122.38 Bn by 2034.

The major top players in the Global Automotive Semiconductor Market are Allegro, Intel: and others.

The growth of the global Automotive Semiconductor market is driven by increasing electric vehicles and smart vehicle innovation are key driver of market growth.

1. Automotive Semiconductor Market: Research Methodology

2. Global Automotive Semiconductor Market: Competitive Landscape

2.1. MMR Competition Matrix

2.2. Competitive Landscape

2.3. Market share analysis of major players

2.4. Products specific analysis

2.4.1. Main suppliers and their market positioning

2.4.2. Key customers and adoption rates across different sectors

2.5. Key Players Benchmarking

2.5.1. Company Name

2.5.2. Product Segment

2.5.3. End-user Segment

2.5.4. Revenue (2025)

2.5.5. Geographic distribution of major customers

2.6. Market Structure

2.6.1. Market Leaders

2.6.2. Market Followers

2.6.3. Emerging Players

2.7. Mergers and Acquisitions Details

3. Automotive Semiconductor Market Introduction

3.1. Study Assumption and Market Definition

3.2. Scope of the Study

3.3. Executive Summary

4. Automotive Semiconductor Market: Dynamics

4.1. Automotive Semiconductor Market Trends by Region

4.1.1. North America Automotive Semiconductor Market Trends

4.1.2. Europe Automotive Semiconductor Market Trends

4.1.3. Asia Pacific Automotive Semiconductor Market Trends

4.1.4. South America Automotive Semiconductor Market Trends

4.1.5. Middle East & Africa (MEA) Automotive Semiconductor Market Trends

4.2. Automotive Semiconductor Market Dynamics by Region

4.2.1.1. Drivers

4.2.1.2. Restraints

4.2.1.3. Opportunities

4.2.1.4. Challenges

4.3. PORTER’s Five Forces Analysis

4.4. PESTLE Analysis

4.5. Regulatory Landscape by Region

4.5.1. North America

4.5.2. Europe

4.5.3. Asia Pacific

4.5.4. South America

4.5.5. MEA

4.6. Analysis of Government Schemes and Initiatives for the Automotive Semiconductor Industry

5. Import-Export Analysis of Automotive Semiconductor Market by Region

5.1.1. North America

5.1.2. Europe

5.1.3. Asia Pacific

5.1.4. South America

5.1.5. MEA

6. Automotive Semiconductor Market: Global Market Size and Forecast by Segmentation (by Value USD Bn and Volume Units) (2026-2034)

6.1. Automotive Semiconductor Market Size and Forecast, by Component (2026-2034)

6.1.1. Processor

6.1.2. Analog IC

6.1.3. Discrete Power Device

6.1.4. Sensor

6.1.5. Memory Device

6.1.6. Others

6.2. Automotive Semiconductor Market Size and Forecast, by Vehicle Type (2026-2034)

6.2.1. Passenger Car

6.2.2. Light Commercial Vehicle (LCV)

6.2.3. Heavy Commercial Vehicle (HCV)

6.3. Automotive Semiconductor Market Size and Forecast, by Propulsion Type (2026-2034)

6.3.1. Internal combustion engine (ICE)

6.3.2. Electric

6.4. Automotive Semiconductor Market Size and Forecast, by Application (2026-2034)

6.4.1. Powertrain

6.4.2. Safety

6.4.3. Body Electronics

6.4.4. Chassis

6.4.5. Telematics and infotainment

6.4.6. Others

6.5. Automotive Semiconductor Market Size and Forecast, by Region (2026-2034)

6.5.1. North America

6.5.2. Europe

6.5.3. Asia Pacific

6.5.4. South America

6.5.5. MEA

7. North America Automotive Semiconductor Market Size and Forecast by Segmentation (by Value USD Bn) (2026-2034)

7.1. North America Automotive Semiconductor Market Size and Forecast, by Component (2026-2034)

7.1.1. Processor

7.1.2. Analog IC

7.1.3. Discrete Power Device

7.1.4. Sensor

7.1.5. Memory Device

7.1.6. Others

7.2. North America Automotive Semiconductor Market Size and Forecast, by Vehicle Type (2026-2034)

7.2.1. Passenger Car

7.2.2. Light Commercial Vehicle (LCV)

7.2.3. Heavy Commercial Vehicle (HCV)

7.3. North America Automotive Semiconductor Market Size and Forecast, by Propulsion Type (2026-2034)

7.3.1. Internal combustion engine (ICE)

7.3.2. Electric

7.4. North America Automotive Semiconductor Market Size and Forecast, by Application (2026-2034)

7.4.1. Powertrain

7.4.2. Safety

7.4.3. Body Electronics

7.4.4. Chassis

7.4.5. Telematics and infotainment

7.4.6. Others

7.5. North America Automotive Semiconductor Market Size and Forecast, by Country (2026-2034)

7.5.1. United States

7.5.2. Canada

7.5.3. Mexico

8. Europe Automotive Semiconductor Market Size and Forecast by Segmentation (by Value USD Bn) (2026-2034)

8.1. Europe Automotive Semiconductor Market Size and Forecast, by Component (2026-2034)

8.2. Europe Automotive Semiconductor Market Size and Forecast, by Vehicle Type (2026-2034)

8.3. Europe Automotive Semiconductor Market Size and Forecast, by Propulsion Type (2026-2034)

8.4. Europe Automotive Semiconductor Market Size and Forecast, by Application (2026-2034)

8.5. Europe Automotive Semiconductor Market Size and Forecast, by Country (2026-2034)

8.5.1. United Kingdom

8.5.2. France

8.5.3. Germany

8.5.4. Italy

8.5.5. Spain

8.5.6. Sweden

8.5.7. Russia

8.5.8. Rest of Europe

9. Asia Pacific Automotive Semiconductor Market Size and Forecast by Segmentation (by Value USD Bn) (2026-2034)

9.1. Asia Pacific Automotive Semiconductor Market Size and Forecast, by Component (2026-2034)

9.2. Asia Pacific Automotive Semiconductor Market Size and Forecast, by Vehicle Type (2026-2034)

9.3. Asia Pacific Automotive Semiconductor Market Size and Forecast, by Propulsion Type (2026-2034)

9.4. Asia Pacific Automotive Semiconductor Market Size and Forecast, by Application (2026-2034)

9.5. Asia Pacific Automotive Semiconductor Market Size and Forecast, by Country (2026-2034)

9.5.1. China

9.5.2. S Korea

9.5.3. Japan

9.5.4. India

9.5.5. Australia

9.5.6. ASEAN

9.5.7. Rest of Asia Pacific

10. South America Automotive Semiconductor Market Size and Forecast by Segmentation (by Value USD Bn) (2026-2034)

10.1. South America Automotive Semiconductor Market Size and Forecast, by Component (2026-2034)

10.2. South America Automotive Semiconductor Market Size and Forecast, by Vehicle Type (2026-2034)

10.3. South America Automotive Semiconductor Market Size and Forecast, by Propulsion Type (2026-2034)

10.4. South America Automotive Semiconductor Market Size and Forecast, by Application (2026-2034)

10.5. South America Automotive Semiconductor Market Size and Forecast, by Country (2026-2034)

10.5.1. Brazil

10.5.2. Argentina

10.5.3. Rest Of South America

11. Middle East and Africa Automotive Semiconductor Market Size and Forecast by Segmentation (by Value USD Bn) (2026-2034)

11.1. Middle East and Africa Automotive Semiconductor Market Size and Forecast, by Component (2026-2034)

11.2. Middle East and Africa Automotive Semiconductor Market Size and Forecast, by Vehicle Type (2026-2034)

11.3. Middle East and Africa Automotive Semiconductor Market Size and Forecast, by Propulsion Type (2026-2034)

11.4. Middle East and Africa Automotive Semiconductor Market Size and Forecast, by Application (2026-2034)

11.5. Middle East and Africa Automotive Semiconductor Market Size and Forecast, by Country (2026-2034)

11.5.1. South Africa

11.5.2. GCC

11.5.3. Egypt

11.5.4. Nigeria

11.5.5. Rest Of MEA

12. Company Profile: Key Players

12.1. NXP: Eindhoven, Netherlands

12.1.1. Company Overview

12.1.2. Business Portfolio

12.1.3. Financial Overview

12.1.4. SWOT Analysis (Technological strengths and weaknesses)

12.1.5. Strategic Analysis (Recent strategic moves)

12.1.6. Recent Developments

12.2. Infineon: Neubiberg, Germany

12.3. Robert Bosch GmbH: Gerlingen, Germany

12.4. STMicroelectronics: Geneva, Switzerland

12.5. ASM Technologies: Almere, Netherlands

12.6. Allegro: Manchester, New Hampshire, United States

12.7. Intel: Santa Clara, California, United States

12.8. Qualcomm: San Diego, California, United States

12.9. Texas Instruments: Dallas, Texas, United States

12.10. Applied Materials: Santa Clara, California, United States

12.11. Nvidia: Santa Clara, California, United States

12.12. AMD: Santa Clara, California, United States

12.13. Analog Devices: Norwood, Massachusetts, United States

12.14. Broadcom: San Jose, California, United States

12.15. Ford: Dearborn, Michigan, United States

12.16. Micron Technology: Boise, Idaho, United States

12.17. Fuji Electric: Tokyo, Japan

12.18. Renesas: Tokyo, Japan

12.19. Toshiba: Tokyo, Japan

12.20. DENSO: Kariya, Japan

12.21. MosChip Technologies: Hyderabad, India

12.22. ROHM: Kyoto, Japan

12.23. TSMC (Taiwan Semiconductor Manufacturing Company): Hsinchu, Taiwan

12.24. Tata Elxsi: Bangalore, India

13. Key Findings and Analyst Recommendations