Automotive Fuel Cell Market Perspective on Upcoming Impacts and Forecast Analysis (2026-2032) by Vehicle Type, Power Capacity, Operating Miles, and Region

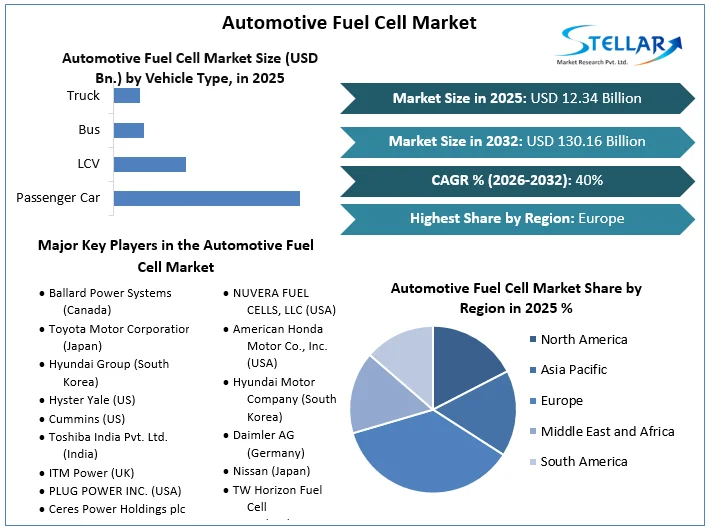

Automotive Fuel Cell Market size was valued at US$ 12.34 Billion in 2025 and the total Automotive Fuel Cell Market revenue is expected to grow at 40% through 2026 to 2032, reaching nearly US$ 130.16 Billion.

Automotive Fuel Cell Market Overview:

Fuel cells are used to power automobiles, which are propelled by hydrogen fuel. This sort of fuel is stored in high-pressure tanks and then supplied into a fuel cell stack, where oxygen and hydrogen from the air react to generate electricity. Unlike typical fuel cell vehicles, which usually run on diesel or gasoline, fuel cell vehicles generate electricity using a combination of oxygen and hydrogen. Fuel stacks for these fuel cells are available for a variety of vehicles, including RVs, cars, trucks, and buses. Automotive Fuel Cell market is expected to register CAGR of 40% during the forecast period.

To get more Insights: Request Free Sample Report

Automotive Fuel Cell Market Dynamics:

Increasing need for Better Fuel Economy:

Compared to ICE vehicles, FCEVs have a superior fuel economy. On highways, an FCEV has a fuel economy of roughly 63 miles per gallon gasoline equivalent (MPGge), while an ICE car has a fuel efficiency of 29 MPGge. Hybridization can boost an FCEV's fuel economy by up to 3.2 percent. The fuel economy of an FCEV on city roads is roughly 55 MPGge, compared to 20 MPGge for ICE vehicles. On either a full tank or a full charge, the driving range of FCEVs and BEVs differs significantly. FCEVs have a range of about 300 miles before requiring recharging. With a fully charged battery, a BEV's typical range is roughly 110 miles. The Honda Clarity boasts the highest EPA rating of any zero-emission vehicle on the automotive fuel cell market.

Current and future number of Fuel Cell vehicles by type and geography:

|

|

|

Passenger vehicles |

Buses and coaches |

Trucks |

Forklifts |

Refueling stations |

|

US |

Current |

7,271 4 |

35 active, 39 in development |

prototype test |

>30,000 |

~42 online |

|

Target |

|

5,300,000 FCEVs on US roads by 2030 |

|

300,000 by 2030 |

7,100 by 2030 |

|

|

China |

Current |

0 |

2,000+ |

1,500+ |

2 |

23 |

|

Target |

3,000 by 2020 87 1,000,000 by 2030 |

11,600 commercial vehicles by 2020 |

|

|

100 by 2020 500 by 2030 |

Rising Adoption of Fuel Cell vehicles:

FCEVs have a long driving range, quick refueling, quiet operation, and no greenhouse gas or air pollution emissions. As a result, fuel cells are well suited to transportation and automotive applications. Fuel cells are a versatile and scalable source of electricity that may be utilized in a wide range of transportation applications, including material handling vehicles, buses, trains, autos, defense vehicles, and light commercial vehicles (LCVs). In commercial applications, fuel cells are also used as stationary fuel sources. Fuel cells can be used as a major power source, a backup power source, and to create heat and power in CHP systems. Furthermore, governments are taking steps to promote and encourage the use of fuel cells in transportation, which could increase demand in the automotive fuel cell market.

Challenges related to cost of fuel cells:

The high cost of fuel cells is a major hurdle for the automotive fuel cell market. A membrane, bipolar plates, stacks, gas diffusion layers, and a catalyst are used to construct a fuel cell. In a fuel cell, hydrogen atoms are oxidized into protons and electrons. The chemical reaction is aided by the application of a catalyst. Platinum is commonly employed as a catalyst in PEM fuel cells, which are mostly used in automobiles. Platinum is one of the most expensive metals available. The catalyst accounts for around 46% of the entire fuel cell cost, making fuel cells more expensive than BEV batteries. Furthermore, thanks to improved R&D in battery technology, the cost of batteries is steadily decreasing.

Fuel cells, on the other hand, have a cheaper maintenance cost than batteries. In the United States, the 2019 Toyota Mirai costs over USD 58,500, whereas the 2019 Tesla Model 3 costs USD 36,000. The significant price disparity between battery electric and fuel cell vehicles is a fundamental barrier to FCEV sales growth. As a result, the cost of fuel cells must be reduced in order to growth in the automotive fuel cell market. The cost of fuel cells, on the other hand, has dropped dramatically in recent years. Additionally, fuel cell manufacturers and government agencies are taking steps and doing research and development to reduce the cost of fuel cells even lower.

Automotive Fuel Cell Market Segmentation:

Commercial Vehicles are dominating the fuel cell market:

Many governments and environmental agencies are establishing strict emission rules and laws in response to growing environmental concerns, which are projected to raise the production cost of fuel-efficient diesel engines in the future years. As a result, growth in the new commercial vehicle diesel engines category is projected to be slow in the near term. Furthermore, traditional fossil fuel-powered commercial vehicles, particularly trucks and buses, are contributing to rising transportation emissions. The introduction of fuel cell commercial vehicles, which are considered low- or zero-emission cars, is expected to cut heavy commercial vehicle emissions. E.g. Beiqi Foton Motor, a Chinese truck and bus manufacturer supported by the Chinese government, said in November 2019 that it would invest USD 2.6 billion in alternative energy vehicles, including fuel cell engines. By 2025, the business hopes to have deployed 200,000 new-energy commercial vehicles.

The market is divided into three categories based on power output: below 100 KW, 100–200 KW, and beyond 200 KW. Fuel cells with a power output of less than 100 kilowatts are used in automobiles, with outputs ranging from 50 to 125 kilowatts. Buses and vehicles employ fuel cells with outputs more than 200kW. Alkaline fuel cells (AFC) and phosphoric acid fuel cells (PAFC) are used in fuel cells below 100kW. (PAFCs). Polymer electrolyte membranes or proton exchange membranes are commonly used in fuel cells with outputs more than 200kW. (PEMFC). In the anticipated timeframe, demand in the automotive fuel cell market expected to increase.

Automotive Fuel cell market Trends:

- Home refueling:

The most significant impediment to the usage of fuel cell automobiles is the lack of hydrogen infrastructure. In California, there are more than 25 hydrogen stations in operation, with plans for another 100 in the pipeline. While home refuelling is still in its infancy in the Northeast, it may be an appealing alternative for consumers due to its quick, clean, and convenient service. SimpleFuel, the $1 million H2 Refuel H-Prize winner, offers a home-scale refuelling appliance that can provide a 1-kilogram fill to a fuel cell vehicle in 15 minutes or less, allowing it to go more than 300 miles. It uses hydrogen produced by water electrolysis and boasts a low-cost design that reduces the system's physical footprint. This type of infrastructure could pave the way for more widespread hydrogen vehicle infrastructure in the future.

- Cargo Delivery Trucks:

The United Parcel Service and FedEx's vehicle manufacturers are collaborating with the US Department of Energy (DOE) to demonstrate the benefits of fuel cell-battery electric cargo transport trucks. Medium-duty trucks can practically increase the amount of miles they can traverse by combining battery electric vehicles with a fuel cell. The vehicles in a hybrid fuel cell battery system are powered largely by the fuel cell, but have additional battery power during high load operations. Argonne National Laboratory will collect and evaluate data and input from the study. This information will be utilised to guide future research and development efforts in the early stages. The first trucks are slated to arrive in New York this summer.

Recent Developments by key players:

- 1Toyota created the Packaged Fuel Cell System Module in February 2021, which combines key functionalities such as Fuel Cell Stacks into a compact package that is suitable with Toyota's forthcoming Bus and Truck Projects.

- 2Hyundai created HTWO in January 2021 to promote its world-class hydrogen fuel cell systems. A plant in Guangzhou, China, was built to generate 6,500 fuel cells each year. Hyundai will introduce a new Tucson model in September 2020 with best-in-class features and class-leading capabilities. It is the fourth generation of the Tucson vehicle, and it can run on a variety of fuels. There is also a hybrid version.

- 3Nuvera will debut its E-60 fuel cell engine in November 2020. It was created for the purpose of handling huge trucks, buses, and other off-road vehicles. It is based on the E-45 engine architecture and delivers 60 KW of power.

- 4Proton motor power systems created a custom hydrogen fuel cell system for rail milling machines in underground railway tunnels with 214 KW installed fuel cell power in November 2020.

Automotive Fuel Cell Market Regional Insights:

European Region is expected to grow at a significant rate:

Several European businesses are involved in the automotive fuel cell market. For example, Robert Bosch GmbH declared in March 2021 that it will develop and market vehicle fuel cell (FC) system components by 2022. In addition to FC stacks, the business said that it will be developing integrated systems that include critical components of fuel cell vehicles (FCVs), such as hydrogen gas injectors and air valves. The region's businesses are constantly developing novel materials and fuel cell technology. In addition, they are investing in the growth of its facilities. These trends are projected to continue in the next years, as some firms have announced their plans to invest in fuel cell technology.

E.g. Ricardo announced a GBP 2.5 million investment in a hydrogen development and test facility at its Shoreham Technical Center in the United Kingdom in January 2021. The company's existing efforts in hydrogen fuel cells and green alternative fuels will be supported by the new facility.

outh In Asia Oceania, Korea, China, and Japan are now leading the automotive fuel cell market. For FCEVs, China is concentrating on buses and trucks. Japanese OEMs like Toyota and Honda, as well as South Korean OEMs like Hyundai, are increasing their production capacity investments. Toyota, for example, is tripling its fuel cell car investments in order to expand manufacturing and lower the cost of hydrogen fuel cell automobiles. Japan is expected to be Asia Oceania's fastest-growing market. India and Australia will see tremendous increase as well. Commercialization of hydrogen vehicles has only recently begun in some nations. However, in the near future, the countries will experience a big opportunity.

The market for hydrogen fuel stations in North America is rapidly expanding. The United States has a huge number of hydrogen fueling stations to serve the market. Both the United States and Canada have boosted demand for low-emission vehicles. In some states, such as California in the United States and British Columbia in Canada, fuel cell vehicles are in great demand. Their pollution rules and laws that favour the growth of zero-emission vehicles have aided the rise of FCEVs.

The objective of the report is to present a comprehensive analysis of the Automotive Fuel Cell Market to the stakeholders in the industry. The report provides trends that are most dominant in the Automotive Fuel Cell Market and how these trends will influence new business investments and market development throughout the forecast period. The report also aids in the comprehension of the market dynamics and competitive structure of the market by analyzing market leaders, market followers, and regional players.

The qualitative and quantitative data provided in the Automotive Fuel Cell Market report is to help understand which market segments, regions are expected to grow at higher rates, factors affecting the market, and key opportunity areas, which will drive the industry and market growth through the forecast period. The report also includes the competitive landscape of key players in the industry along with their recent developments in the Automotive Fuel Cell Market. The report studies factors such as company size, market share, market growth, revenue, production volume, and profits of the key players in the market.

The report provides Porter's Five Force Model, which helps in designing the business strategies in the market. The report helps in identifying how many rivals are existing, who they are, and how their product quality is in the Market. The report also analyses if the Automotive Fuel Cell Market is easy for a new player to gain a foothold in the market, do they enter or exit the market regularly if the market is dominated by a few players, etc.

The report also includes a PESTEL Analysis, which aids in the development of company strategies. Political variables help in figuring out how much a government can influence the Market. Economic variables aid in the analysis of economic performance drivers that have an impact on the Market. Understanding the impact of the surrounding environment and the influence of environmental concerns on the Automotive Fuel Cell Market is aided by legal factors.

Automotive Fuel Cell Market Scope:

|

Automotive Fuel Cell Market |

|

|

Market Size in 2025 |

USD 12.34 Bn. |

|

Market Size in 2032 |

USD 130.16 Bn. |

|

CAGR (2026-2032) |

40% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segment Scope |

by Vehicle Type

|

|

by Power Capacity

|

|

|

By Operating Miles

|

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Automotive Fuel Cell Market Regional Analysis:

- North America

- Europe

- Asia Pacific

- South America

- Middle East and Africa

Automotive Fuel Cell Market Players:

- Ballard Power Systems (Canada)

- Toyota Motor Corporation (Japan)

- Hyundai Group (South Korea)

- Hyster Yale (US)

- Cummins (US)

- Toshiba India Pvt. Ltd. (India)

- ITM Power (UK)

- PLUG POWER INC. (USA)

- Ceres Power Holdings plc (UK)

- Nedstack Fuel Cell Technology BV (Netherlands)

- NUVERA FUEL CELLS, LLC (USA)

- American Honda Motor Co., Inc. (USA)

- Hyundai Motor Company (South Korea)

- Daimler AG (Germany)

- Nissan (Japan)

- TW Horizon Fuel Cell Technologies (Singapore)

- Altergy (USA)

- Intelligent Energy Limited (UK)

- K- Pas Instronic Engineers India Private Limited (India)

- Fuji Electric Co. (japan)

Frequently Asked Questions

European region have the highest growth rate in the Automotive Fuel Cell market.

Ballard Power Systems (Canada), Toyota Motor Corporation (Japan), Hyundai Group (South Korea), Hyster Yale (US),Cummins (US), Toshiba India Pvt. Ltd. (India), ITM Power (UK), PLUG POWER INC. (USA), Ceres Power Holdings plc (UK), Nedstack Fuel Cell Technology BV (Netherlands), NUVERA FUEL CELLS, LLC (USA), American Honda Motor Co., Inc. (USA), Hyundai Motor Company (South Korea) and others are the key players in the Automotive Fuel Cell market.

Commercial cars segment is dominating the market owing to increasing penetration of fuel cell technology in LCVs across Europe and North America.

Chapter 1 Scope of the Report

Chapter 2 Research Methodology

2.1.Research Process

2.2.Global Automotive Fuel Cell Market: Target Audience

2.3.Global Automotive Fuel Cell Market: Primary Research (As per Client Requirement)

2.4.Global Automotive Fuel Cell Market: Secondary Research

Chapter 3 Executive Summary

Chapter 4 Competitive Landscape

4.1.Market Share Analysis, By Region, 2025-2032(In %)

4.1.1.North America Market Share Analysis, By Value, 2025-2032 (In %)

4.1.2.Europe Market Share Analysis, By Value, 2025-2032 (In %)

4.1.3.Asia Pacific Market Share Analysis, By Value, 2025-2032 (In %)

4.1.4.South America Market Share Analysis, By Value, 2025-2032 (In %)

4.1.5.Middle East and Africa Market Share Analysis, By Value, 2025-2032 (In %)

4.2.Market Dynamics

4.2.1.Market Drivers

4.2.2.Market Restraints

4.2.3.Market Opportunities

4.2.4.Market Challenges

4.2.5.PESTLE Analysis

4.2.6.PORTERS Five Force Analysis

4.2.7.Value Chain Analysis

4.3.Global Automotive Fuel Cell Market Segmentation Analysis, 2025-2032 (Value US$ MN)

4.3.1.Global Market Share Analysis, By Power Capacity, 2025-2032 (Value US$ MN)

4.3.1.1.<150 kW

4.3.1.2.150-250 kW

4.3.1.3.>250 kW

4.3.2. Global Market Share Analysis, By Vehicle Type, 2025-2032 (Value US$ MN)

4.3.2.1.Passenger Car

4.3.2.2.LCV

4.3.2.3.Bus

4.3.2.4.Truck

4.3.3.Global Market Share Analysis, By Operating Miles, 2025-2032 (Value US$ MN)

4.3.3.1.0-250 Miles

4.3.3.2.251-500 Miles

4.3.3.3.Above 500 Miles

4.4.North America Automotive Fuel Cell Market Segmentation Analysis, 2025-2032 (Value US$ MN)

4.4.1.North America Market Share Analysis, By Power Capacity, 2025-2032 (Value US$ MN)

4.4.1.1.<150 kW

4.4.1.2.150-250 kW

4.4.1.3.>250 kW

4.4.2. North America Market Share Analysis, By Vehicle Type, 2025-2032 (Value US$ MN)

4.4.2.1.Passenger Car

4.4.2.2.LCV

4.4.2.3.Bus

4.4.2.4.Truck

4.4.3. North America Market Share Analysis, By Operating Miles, 2025-2032 (Value US$ MN)

4.4.3.1.0-250 Miles

4.4.3.2.251-500 Miles

4.4.3.3.Above 500 Miles

4.4.4. North America Market Share Analysis, By Country, 2025-2032 (Value US$ MN)

4.4.4.1.US

4.4.4.2.Canada

4.4.4.3.Mexico

4.5. Europe Automotive Fuel Cell Market Segmentation Analysis, 2025-2032 (Value US$ MN)

4.5.1.Europe Market Share Analysis, By Power Capacity, 2025-2032 (Value US$ MN)

4.5.2.Europe Market Share Analysis, By Vehicle Type, 2025-2032 (Value US$ MN)

4.5.3.Europe Market Share Analysis, By Operating Miles, 2025-2032 (Value US$ MN)

4.5.4.Europe Market Share Analysis, By Country, 2025-2032 (Value US$ MN)

4.5.4.1.UK

4.5.4.2.France

4.5.4.3.Germany

4.5.4.4.Italy

4.5.4.5.Spain

4.5.4.6.Sweden

4.5.4.7.Austria

4.5.4.8.Rest Of Europe

4.6. Asia Pacific Automotive Fuel Cell Market Segmentation Analysis, 2025-2032 (Value US$ MN)

4.6.1.Asia Pacific Market Share Analysis, By Power Capacity, 2025-2032 (Value US$ MN)

4.6.2.Asia Pacific Market Share Analysis, By Vehicle Type, 2025-2032 (Value US$ MN)

4.6.3.Asia Pacific Market Share Analysis, By Operating Miles, 2025-2032 (Value US$ MN)

4.6.4.Asia Pacific Market Share Analysis, By Country, 2025-2032 (Value US$ MN)

4.6.4.1.China

4.6.4.2.India

4.6.4.3.Japan

4.6.4.4.South Korea

4.6.4.5.Australia

4.6.4.6.ASEAN

4.6.4.7.Rest Of APAC

4.7. South America Automotive Fuel Cell Market Segmentation Analysis, 2025-2032 (Value US$ MN)

4.7.1.South America Market Share Analysis, By Power Capacity, 2025-2032 (Value US$ MN)

4.7.2.South America Market Share Analysis, By Vehicle Type, 2025-2032 (Value US$ MN)

4.7.3.South America Market Share Analysis, By Operating Miles, 2025-2032 (Value US$ MN)

4.7.4.South America Market Share Analysis, By Country, 2025-2032 (Value US$ MN)

4.7.4.1.Brazil

4.7.4.2.Argentina

4.7.4.3.Rest Of South America

4.8. Middle East and Africa Automotive Fuel Cell Market Segmentation Analysis, 2025-2032 (Value US$ MN)

4.8.1.Middle East and Africa Market Share Analysis, By Power Capacity, 2025-2032 (Value US$ MN)

4.8.2.Middle East and Africa Market Share Analysis, By Vehicle Type, 2025-2032 (Value US$ MN)

4.8.3.Middle East and Africa Market Share Analysis, By Operating Miles, 2025-2032 (Value US$ MN)

4.8.4.Middle East and Africa Market Share Analysis, By Country, 2025-2032 (Value US$ MN)

4.8.4.1.South Africa

4.8.4.2.GCC

4.8.4.3.Egypt

4.8.4.4.Nigeria

4.8.4.5.Rest Of ME&A

Chapter 5 Stellar Competition Matrix

5.1.Global Stellar Competition Matrix

5.2.North America Stellar Competition Matrix

5.3.Europe Stellar Competition Matrix

5.4.Asia Pacific Stellar Competition Matrix

5.5.South America Stellar Competition Matrix

5.6.Middle East and Africa Stellar Competition Matrix

5.7.Key Players Benchmarking

5.7.1.Key Players Benchmarking By Power Capacity, Pricing, Market Share, Investments, Expansion Plans, Physical Presence and Presence in the Market.

5.8.Mergers and Acquisitions in Operating Miles

5.8.1.M&A by Region, Value and Strategic Intent

Chapter 6 Company Profiles

6.1.Key Players

6.1.1.Ballard Power Systems (Canada)

6.1.1.1.Company Overview

6.1.1.2.Source Portfolio

6.1.1.3.Financial Overview

6.1.1.4.Business Strategy

6.1.1.5.Key Developments

6.1.2.Toyota Motor Corporation (Japan)

6.1.3.Hyundai Group (South Korea)

6.1.4.Hyster Yale (US)

6.1.5.Cummins (US)

6.1.6.Toshiba India Pvt. Ltd. (India)

6.1.7.ITM Power (UK)

6.1.8.PLUG POWER INC. (USA)

6.1.9.Ceres Power Holdings plc (UK)

6.1.10.Nedstack Fuel Cell Technology BV (Netherlands)

6.1.11.NUVERA FUEL CELLS, LLC (USA)

6.1.12.American Honda Motor Co., Inc. (USA)

6.1.13.Hyundai Motor Company (South Korea)

6.1.14.Daimler AG (Germany)

6.1.15.Nissan (Japan)

6.1.16.TW Horizon Fuel Cell Technologies (Singapore)

6.1.17.Altergy (USA)

6.1.18.Intelligent Energy Limited (UK)

6.1.19.K- Pas Instronic Engineers India Private Limited (India)

6.1.20.Fuji Electric Co. (Japan)

6.2. Key Findings

6.3. Recommendations