Advanced Metering Infrastructure Market- Global Industry Analysis and Forecast 2026-2034 Trends, Statistics, Dynamics, and Region

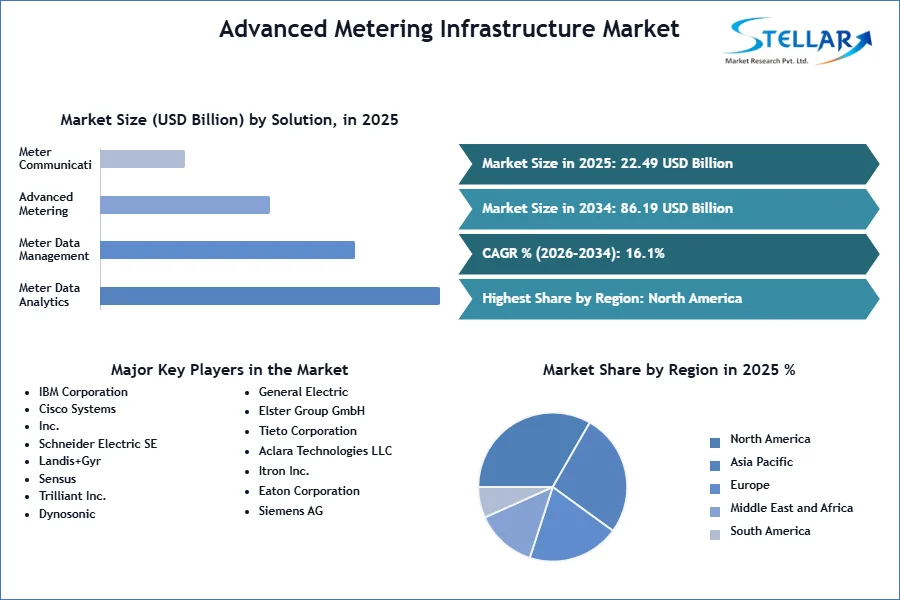

Advanced Metering Infrastructure Market was valued at USD 22.49 billion in 2025. Global Advanced Metering Infrastructure Market size is estimated to grow at a CAGR of 16.1 % over the forecast period.

Advanced Metering Infrastructure Market Definition:

Advanced metering infrastructure (AMI) helps private, and public utilities manage energy demand by identifying peak load times. In addition, smart metering infrastructure assists users in managing their energy consumption as well as their Time-Of-Use (TOU) tariff. Electrical system operators can use an IT-enabled interface provided by Advanced Metering Infrastructure. Smart meters, meter connection infrastructure, and data management are all part of this system.

The Advanced Metering Infrastructure market analyses and forecasts the market size, in terms of value, for the market. Further, the Advanced Metering Infrastructure Market is segmented by Device, Deployment Mode, Solution, Service, Application, and Region. Based on Device, the Advanced Metering Infrastructure market is segmented under Smart Electric, Water, and Gas. Based on the Service, the market is segmented into Residential, Commercial, and Industrial. The market sizing and forecasts have been done for each segment based on value (in USD Billion).

To get more Insights: Request Free Sample Report

Advanced Metering Infrastructure Market Dynamics:

Market Drivers:

Increased adoption of the Internet of Things (IoT): Increased Internet of Things penetration is driving the worldwide advanced metering infrastructure market forward (IoT). Also, because of the growing demand for low-bandwidth, low-cost, and delay-insensitive metering, the demand for AMI communications networks is expected to skyrocket in the near future. The network and communications modules of the meter must be as low-cost as possible. The key communication technologies driving AMI adoption in the early days are narrow-band power-line communication (PLC) and RF-Mesh. As communication technology advances, other technologies such as broadband PLC and low-power wide-area networks (LPWAN) are gaining momentum in the industry.

Two-way smart meters are in high demand.

The primary goal of deploying advanced metering infrastructure solutions is to manage and monitor energy resources and their use. AMR (advanced meter reading) technology now available only allows us to monitor and has limitations. In order to establish a successful AMI solution, AMI-integrated meters are used.

These are two-way smart meters, which not only monitor but also allow us to transfer information from both ends, making real-time data transmission and automatic data collecting possible throughout the grid. Meter data management and meter communication infrastructure would also be critical for smart meters to reach their full potential.

Growth of electricity infrastructure driving the market:

Growth, modernization, and decentralization of electricity infrastructure for increased resilience, as well as planned investments from organizations like the World Economic Forum, which has set aside USD 7.6 trillion for smart grids over the next 25 years, are expected to alter several market dynamics in the global scenario.

Government agencies are building smart grids and deploying smart meters:

Regulatory mandates and legislative directives are being issued by a number of governments and organizations throughout the world addressing the building of smart grids and the deployment of smart meters. For example, by 2021, European Union countries want to replace 80% of old electricity meters with smart metering infrastructure. In addition, the Tokyo Electric Power Company (TEPCO) wants to install 27 million smart meters in Japan and develop an integrated energy management platform that connects to smart devices in households and businesses. During the forecast period, this factor is likely to drive the worldwide advanced metering infrastructure market.

Market Restraint:

Interoperability standards are in scarce supply: Smart meter adoption is being studied, and several smart meter manufacturers have been working to produce a uniform design that would comply with regulatory standards around the world in order to maximize their market revenue potential. Inadequate financial incentives for utilities, as well as interoperability and a consistent interface, are limiting the market growth.

Market Opportunity:

Rising demand in international economies: Transport restrictions were imposed as a result in lower industrial productivity and disrupted supply chains, which had a significant influence on global economic growth and market growth. When the economy that produces the items grows, so makes the demand for consumer goods. An economy with strong overall growth and stable growth prospects is frequently accompanied by comparable increases in demand for goods and services.

Market Challenge:

High start-up costs: Another issue that could limit the growth of this market is the high cost of installation associated with smart meters. Also, these meters must be maintained at regular intervals, and the expenses associated with meter maintenance are extremely high, which is another factor that could limit the growth of the advanced metering infrastructure market.

Advanced Metering Infrastructure Market Trends:

Meters or modules with communication capabilities (unidirectional or bidirectional) built within or attached to the meter are included in smart metering solutions. Smart meters have become more popular as a result of the major worry of increased energy usage, as they enable two-way communication between the meter and the utility's central system.

Smart meters are increasingly being used for a variety of services, including gas, electricity, and water, due to their two-way communication feature, which allows both the utility supplier and the consumer to monitor utility usage in real-time and encourages the supplier to start/read/cutoff supply remotely. Smart metering also allows for the installation of a Home Energy Management System (HEMS) or a Building Energy Management System (BEMS), which allows for the viewing of electric power usage in individual homes or entire buildings.

Asian countries are preparing to move forward with the use of smart meters. For example, the Indian government declared in February 2020 that the smart meter national program would install 10 lakh smart meters across the country (SMNP). The European Union has also calculated that replacing 80% of present electricity meters with smart meters would reduce regional carbon emissions by 9% by 2020 and reduce annual household energy use by a similar proportion, which is pushing smart meter adoption.

Advanced Metering Infrastructure Market key Developments:

- March 2021- Calaveras County Water District and Mueller Systems joined in March 2021 to develop an advanced metering infrastructure (AMI) network. With 13,000 AMI endpoints, it would cover 1,000 square miles. The project involves replacing the bulk of the district's meters and equipping all of them with communication capabilities. In six service regions throughout the county, the Calaveras County Water District serves over 13,000 municipal, residential, and business customers.

- June 2020- Piedmont Electric teamed up with Landis+Gyr (LAND.SW) to modernize its advanced metering system and supply grid management and member engagement technology. The company replaced its existing power line carrier AMI system with Landis+Gyr's Gridstream Connect platform with an RF mesh network and 35,000 advanced meters to enable secure communication with advanced meters, load control, and distribution automation devices while improving reliability and support for flexible billing options like prepaying metering services.

Advanced Metering Infrastructure Market Segment Analysis:

Based on Device, in 2025, the electricity segment held the largest share accounting for 36.5%, while the water segment would have the highest CAGR of 15.2% through the forecast period. Smart meters are a game-changing technology for the utility industry. These technologically sophisticated meters provide more information about energy usage. Smart meters have been employed all around the world to build sophisticated metering infrastructure initiatives.

Based on Solution, in 2025, the software sector held the largest market share and is expected to increase at a CAGR of 12.2% through the forecast period. Meter Data Management stores a large number of meter data repositories for a limited time, including customer billing, credit management, outage management, and meter asset management.

Advanced Metering Infrastructure Market Regional Insights:

The North American region held the largest market share accounting for 38.2% in 2025. The North American market is also developing as the population of the United States and Canada grows, as well as the number of water Services. Owing to the rise in the adoption of smart meters in developing countries such as India and Indonesia, Asia-Pacific is the fastest-growing area for the worldwide advanced metering infrastructure market. For example, the Indian government declared in February 2020 that the smart meter national program would install 10 lakh smart meters across the country (SMNP).

Europe holds the second-largest share in the Advanced Metering Infrastructure market. The European Union has the world's largest working population, requiring a long-term infrastructure. Regulatory mandates and legislative directives are being issued by government entities across Europe addressing the development of smart grids and the deployment of smart meters. By 2023, the European Union mandates that 84% of all traditional power meters be replaced with modernized metering infrastructure.

Advanced Metering Infrastructure Market Key Players Insights:

The market is characterized by the existence of a number of well-known firms. These companies control a large portion of the market, have a wide product portfolio, and have a global presence. In addition, the market comprises small to mid-sized competitors that sell a limited variety of items, some of which are self-publishing organizations.

The market's major companies have a significant impact because most of them have extensive global networks through which they can reach their massive client bases. To drive revenue growth and strengthen their positions in the global market, key players in the market, particularly in North America and Europe, are focusing on strategic initiatives such as acquisitions, new collection launches, and partnerships.

The objective of the report is to present a comprehensive analysis of the Global Advanced Metering Infrastructure Market to the stakeholders in the industry. The report provides trends that are most dominant in the Global Advanced Metering Infrastructure Market and how these trends will influence new business investments and market development throughout the forecast period. The report also aids in the comprehension of the Global Advanced Metering Infrastructure Market dynamics and competitive structure of the market by analyzing market leaders, market followers, and regional players.

The qualitative and quantitative data provided in the Global Advanced Metering Infrastructure Market report is to help understand which market segments, regions are expected to grow at higher rates, factors affecting the market, and key opportunity areas, which will drive the industry and market growth through the forecast period. The report also includes the competitive landscape of key players in the industry along with their recent developments in the Global Advanced Metering Infrastructure Market. The report studies factors such as company size, market share, market growth, revenue, production volume, and profits of the key players in the Global Advanced Metering Infrastructure Market.

The report provides Porter's Five Force Model, which helps in designing the business strategies in the market. The report helps in identifying how many rivals exist, who they are, and how their product quality is in the Global Advanced Metering Infrastructure Market. The report also analyses if the Global Advanced Metering Infrastructure Market is easy for a new player to gain a foothold in the market, do they enter or exit the market regularly, if the market is dominated by a few players, etc.

The report also includes a PESTEL Analysis, which aids in the development of company strategies. Political variables help in figuring out how much a government can influence the Global Advanced Metering Infrastructure Market. Economic variables aid in the analysis of economic performance drivers that have an impact on the Global Advanced Metering Infrastructure Market. Understanding the impact of the surrounding environment and the influence of environmental concerns on the Global Advanced Metering Infrastructure Market is aided by legal factors.

Advanced Metering Infrastructure Market Scope:

|

Advanced Metering Infrastructure Market |

|

|

Market Size in 2025 |

USD 22.49 Bn. |

|

Market Size in 2034 |

USD 86.19 Bn. |

|

CAGR (2026-2034) |

16.1% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Segment Scope |

By Device

|

|

By Solution

|

|

|

By Deployment Mode3

|

|

|

By Service

|

|

|

|

By Application

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Advanced Metering Infrastructure Market Key Players:

- IBM Corporation

- Cisco Systems, Inc.

- Schneider Electric SE

- Landis+Gyr

- Sensus

- Trilliant Inc.

- Dynosonic

- General Electric

- Elster Group GmbH

- Tieto Corporation

- Aclara Technologies LLC

- Itron Inc.

- Eaton Corporation

- Siemens AG

- General Electric

Frequently Asked Questions

North America region is expected to hold the highest share in the Advanced Metering Infrastructure Market.

The market size of the Advanced Metering Infrastructure Market by 2034 is expected to reach USD 86.19 Billion.

The forecast period for the Advanced Metering Infrastructure Market is 2026-2034.

The market size of the Advanced Metering Infrastructure Market in 2025 was valued at USD 22.49 Billion.

1. Research Methodology

1.1 Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Research Assumption

2. Advanced Metering Infrastructure Market Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026 – 2034) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Advanced Metering Infrastructure Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Business Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. Developments and Innovations

4. Advanced Metering Infrastructure Market: Dynamics

4.1. Advanced Metering Infrastructure Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Advanced Metering Infrastructure Market Drivers

4.3. Advanced Metering Infrastructure Market Restraints

4.4. Advanced Metering Infrastructure Market Opportunities

4.5. Advanced Metering Infrastructure Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factors

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Regulatory Landscape

4.9.1. Market Regulation by Region

4.9.1.1. North America

4.9.1.2. Europe

4.9.1.3. Asia Pacific

4.9.1.4. Middle East and Africa

4.9.1.5. South America

4.9.2. Government Schemes and Initiatives

5. Advanced Metering Infrastructure Market: Global Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

5.1. Advanced Metering Infrastructure Market Size and Forecast, by Device (2026-2034)

5.1.1. Electric

5.1.2. Water

5.1.3. Gas

5.2. Advanced Metering Infrastructure Market Size and Forecast, by Solution (2026-2034)

5.2.1. Meter Data Analytics

5.2.2. Meter Data Management

5.2.3. Advanced Metering Infrastructure Security

5.2.4. Meter Communication Infrastructure

5.3. Advanced Metering Infrastructure Market Size and Forecast, by Deployment Mode (2026-2034)

5.3.1. Cloud

5.3.2. On-premises

5.4. Advanced Metering Infrastructure Market Size and Forecast, by Service (2026-2034)

5.4.1. System Integration

5.4.2. Meter Deployment

5.4.3. Program Management and Consulting

5.5. Advanced Metering Infrastructure Market Size and Forecast, by Application (2026-2034)

5.5.1. Residential

5.5.2. Commercial

5.5.3. Industrial

5.6. Advanced Metering Infrastructure Market Size and Forecast, by Region (2026-2034)

5.6.1. North America

5.6.2. Europe

5.6.3. Asia Pacific

5.6.4. Middle East and Africa

5.6.5. South America

6. North America Advanced Metering Infrastructure Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

6.1. North America Advanced Metering Infrastructure Market Size and Forecast, by Device (2026-2034)

6.1.1. Electric

6.1.2. Water

6.1.3. Gas

6.2. North America Advanced Metering Infrastructure Market Size and Forecast, by Solution (2026-2034)

6.2.1. Meter Data Analytics

6.2.2. Meter Data Management

6.2.3. Advanced Metering Infrastructure Security

6.2.4. Meter Communication Infrastructure

6.3. North America Advanced Metering Infrastructure Market Size and Forecast, by Deployment Mode (2026-2034)

6.3.1. Cloud

6.3.2. On-premises

6.4. North America Advanced Metering Infrastructure Market Size and Forecast, by Service (2026-2034)

6.4.1. System Integration

6.4.2. Meter Deployment

6.4.3. Program Management and Consulting

6.5. North America Advanced Metering Infrastructure Market Size and Forecast, by Application (2026-2034)

6.5.1. Residential

6.5.2. Commercial

6.5.3. Industrial

6.6. North America Advanced Metering Infrastructure Market Size and Forecast, by Country (2026-2034)

6.6.1. United States

6.6.2. Canada

6.6.3. Mexico

7. Europe Advanced Metering Infrastructure Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

7.1. Europe Advanced Metering Infrastructure Market Size and Forecast, by Device (2026-2034)

7.2. Europe Advanced Metering Infrastructure Market Size and Forecast, by Solution (2026-2034)

7.3. Europe Advanced Metering Infrastructure Market Size and Forecast, by Deployment Mode (2026-2034)

7.4. Europe Advanced Metering Infrastructure Market Size and Forecast, by Service (2026-2034)

7.5. Europe Advanced Metering Infrastructure Market Size and Forecast, by Application (2026-2034)

7.6. Europe Advanced Metering Infrastructure Market Size and Forecast, by Country (2026-2034)

7.6.1. United Kingdom

7.6.2. France

7.6.3. Germany

7.6.4. Italy

7.6.5. Spain

7.6.6. Sweden

7.6.7. Austria

7.6.8. Rest of Europe

8. Asia Pacific Advanced Metering Infrastructure Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

8.1. Asia Pacific Advanced Metering Infrastructure Market Size and Forecast, by Device (2026-2034)

8.2. Asia Pacific Advanced Metering Infrastructure Market Size and Forecast, by Solution (2026-2034)

8.3. Asia Pacific Advanced Metering Infrastructure Market Size and Forecast, by Deployment Mode (2026-2034)

8.4. Asia Pacific Advanced Metering Infrastructure Market Size and Forecast, by Service (2026-2034)

8.5. Asia Pacific Advanced Metering Infrastructure Market Size and Forecast, by Application (2026-2034)

8.6. Asia Pacific Advanced Metering Infrastructure Market Size and Forecast, by Country (2026-2034)

8.6.1. China

8.6.2. S Korea

8.6.3. Japan

8.6.4. India

8.6.5. Australia

8.6.6. Indonesia

8.6.7. Malaysia

8.6.8. Vietnam

8.6.9. Taiwan

8.6.10. Rest of Asia Pacific

9. Middle East and Africa Advanced Metering Infrastructure Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

9.1. Middle East and Africa Advanced Metering Infrastructure Market Size and Forecast, by Device (2026-2034)

9.2. Middle East and Africa Advanced Metering Infrastructure Market Size and Forecast, by Solution (2026-2034)

9.3. Middle East and Africa Advanced Metering Infrastructure Market Size and Forecast, by Deployment Mode (2026-2034)

9.4. Middle East and Africa Advanced Metering Infrastructure Market Size and Forecast, by Service (2026-2034)

9.5. Middle East and Africa Advanced Metering Infrastructure Market Size and Forecast, by Application (2026-2034)

9.6. Middle East and Africa Advanced Metering Infrastructure Market Size and Forecast, by Country (2026-2034)

9.6.1. South Africa

9.6.2. GCC

9.6.3. Nigeria

9.6.4. Rest of ME&A

10. South America Advanced Metering Infrastructure Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2034)

10.1. South America Advanced Metering Infrastructure Market Size and Forecast, by Device (2026-2034)

10.2. South America Advanced Metering Infrastructure Market Size and Forecast, by Solution (2026-2034)

10.3. South America Advanced Metering Infrastructure Market Size and Forecast, by Deployment Mode (2026-2034)

10.4. South America Advanced Metering Infrastructure Market Size and Forecast, by Service (2026-2034)

10.5. South America Advanced Metering Infrastructure Market Size and Forecast, by Application (2026-2034)

10.6. South America Advanced Metering Infrastructure Market Size and Forecast, by Country (2026-2034)

10.6.1. Brazil

10.6.2. Argentina

10.6.3. Rest Of South America

11. Company Profile: Key Players

11.1. IBM Corporation

11.1.1. Company Overview

11.1.2. Business Portfolio

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Cisco Systems, Inc.

11.3. Schneider Electric SE

11.4. Landis+Gyr

11.5. Sensus

11.6. Trilliant Inc.

11.7. Dynosonic

11.8. General Electric

11.9. Elster Group GmbH

11.10. Tieto Corporation

11.11. Aclara Technologies LLC

11.12. Itron Inc.

11.13. Eaton Corporation

11.14. Siemens AG

11.15. General Electric

12. Key Findings

13. Analyst Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook