US Radioactive Waste and Nuclear Waste Management Market: Spent Fuel Storage, Reactor Decommissioning, and Long-Term Waste Disposal Outlook (2026–2032)

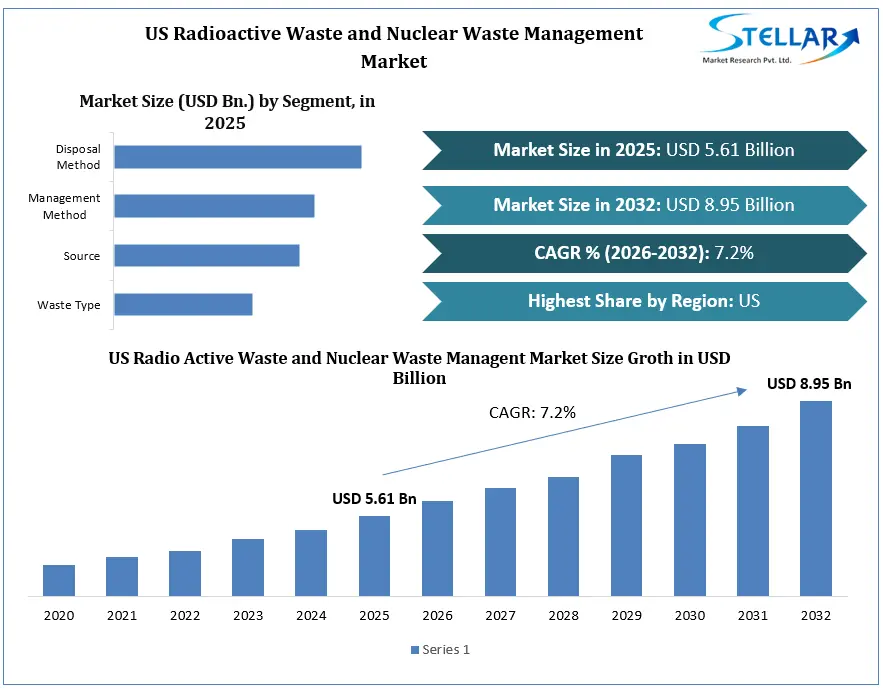

The US Radioactive Waste and Nuclear Waste Management Market was projected to grow from USD 5.61 Bn in 2025 to USD 8.95 Bn by 2032 at 7.2% CAGR, driven by a steady nuclear power base, increasing spent fuel from ongoing reactor operations, more decommissioning projects, and ongoing investment in safe storage, transport, and long-term disposal infrastructure.

US Radioactive Waste and Nuclear Waste Management Market Definition

The US radioactive and nuclear waste management market includes services and technologies used to handle waste produced by nuclear power plants, medical uses, industrial activities, and research. It includes the processes of collecting, treating, storing, moving, and safely disposing of radioactive materials. The main focus is on managing low, intermediate, and high-level waste in a controlled system to reduce risks to people and the environment.

It also covers the systems and infrastructure used for long-term management, such as temporary storage sites, deep underground disposal facilities, and treatment methods that stabilize waste for safer containment. The market operates under strict safety rules and regulations to prevent radiation exposure and contamination while supporting the continued use of nuclear energy across both power generation and non-power sectors.

To get more Insights: Request Free Sample Report

US Radioactive Waste and Nuclear Waste Management Market Dynamics

US Radioactive Waste and Nuclear Waste Management Market Drivers

Rising Nuclear Power Output and Waste Management Demands

Growing nuclear power use in the United States is producing more spent fuel and radioactive waste, which is increasing the demand for safe storage, transport, treatment, and long-term disposal options. At the same time, older reactors continue to operate and a steady stream of decommissioning work is underway, both of which keep adding waste and are pushing the need for reliable, compliance-focused handling services.

Companies such as Holtec International, EnergySolutions, Waste Control Specialists, NAC International, and Amentum support this demand through services spanning spent fuel storage systems, waste processing, transport, decommissioning support, and long-term management infrastructure. For instance, Holtec International provides dry cask storage systems along with containment technologies, while EnergySolutions focuses on decommissioning work and low-level waste processing across nuclear facilities in the US.

US Radioactive Waste and Nuclear Waste Management Market Opportunities

Advancement in waste treatment technologies

Advances in waste treatment technologies, such as vitrification, compaction, and advanced conditioning, are improving efficiency in the United States by reducing waste volumes and enhancing storage safety. These developments are helping utilities and service providers handle spent nuclear fuel along with low- and intermediate-level waste more effectively, while also meeting stricter safety and regulatory standards for long-term containment and disposal.

Ongoing Reactor Operations and Decommissioning Activities

Rising radioactive waste volumes from the steady operation of a large fleet of nuclear reactors in the United States, along with ongoing decommissioning projects, are generating consistent waste streams. This is driving continued demand for safe storage systems, transport services, waste processing, and long-term disposal infrastructure across the country.

US Radioactive Waste and Nuclear Waste Management Market Trends

Expansion of Dry Cask Storage and Interim Waste Facilities

Expansion of dry cask storage systems and on-site interim storage facilities is increasing across nuclear power plants in the United States. With permanent disposal capacity still limited, utilities are increasingly relying on secure long-term storage solutions to manage growing spent fuel inventories while staying compliant with regulatory requirements.

Growing Focus on Decommissioning and Site Restoration Activities

Rising decommissioning activity across aging nuclear reactors in the United States is increasing the need for structured waste handling, site cleanup, and long-term remediation services. This is driving stronger demand for specialized contractors that handle dismantling, waste sorting, transport, and safe disposal at retired and shut-down nuclear facilities.

US Radioactive Waste and Nuclear Waste Management Market Segmentation (2025)

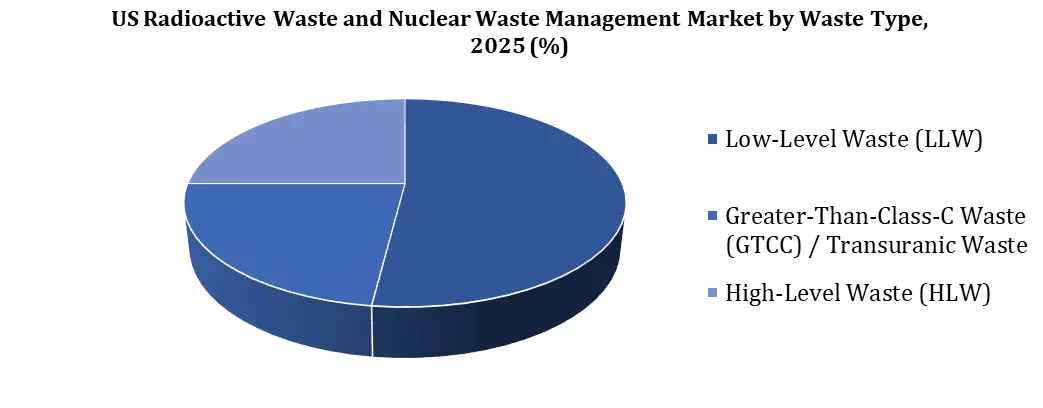

US Radioactive Waste and Nuclear Waste Management Market by Waste Type

Low-Level Waste (LLW) holds the largest market share at 52%, mainly due to the high volume of contaminated materials generated from nuclear power plants, hospitals, industrial operations, and research facilities. Greater-Than-Class-C Waste (GTCC) / Transuranic Waste is growing steadily as reactor maintenance, upgrades, and decommissioning activities increase the need for safe treatment and storage. High-Level Waste (HLW) is showing the fastest growth, supported by rising spent nuclear fuel volumes, expanding nuclear energy programs, and increasing investment in long-term disposal facilities and deep geological storage infrastructure.

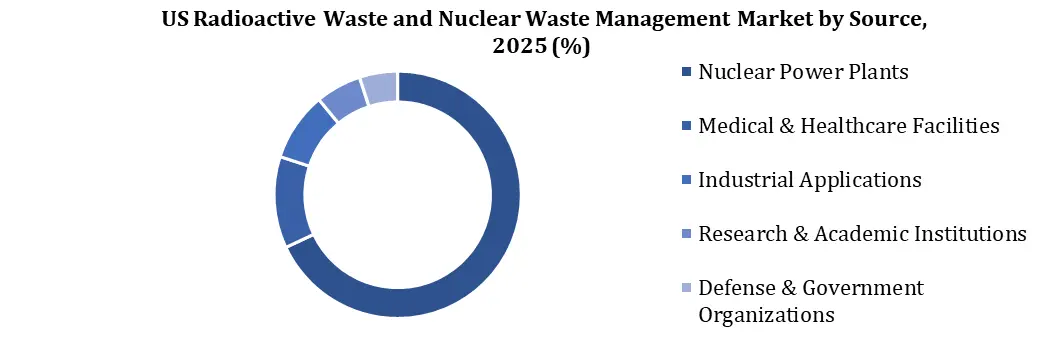

US Radioactive Waste and Nuclear Waste Management Market by Source

Nuclear Power Plants account for the largest market share at 68%, mainly due to the high volume of radioactive waste generated from reactor operations, spent fuel management, and plant decommissioning activities. Medical & Healthcare Facilities are showing strong growth with the rising use of radioisotopes in diagnostics and cancer treatment, while industrial applications continue to expand through wider use of radioactive materials in inspection, manufacturing, and testing. Research & Academic Institutions contribute through nuclear research, laboratory work, and isotope development, creating steady demand for specialized waste management services. Defense & Government Organizations also play a role through military reactor operations, nuclear defense activities, and the long-term handling of radioactive and legacy nuclear waste.

US Radioactive Waste and Nuclear Waste Management Market by Management Method

Storage holds the largest share of the market at 34%, supported by rising demand for interim and long-term storage facilities for spent nuclear fuel and other radioactive materials. Treatment & Processing is growing steadily as the industry focuses more on reducing waste volume, toxicity, and environmental impact before disposal. Recycling & Reprocessing is also expanding with increasing efforts to recover reusable nuclear materials and improve fuel utilization. Meanwhile, Transportation remains essential for the safe transfer of radioactive waste between reactors, processing facilities, and disposal sites under strict safety regulations.

US Radioactive Waste and Nuclear Waste Management Competitive Analysis 2025

The US Radioactive Waste and Nuclear Waste Management market is supported by companies that focus on spent fuel storage, decommissioning services, waste treatment, and radioactive material handling. Holtec International, EnergySolutions, and NAC International have a strong presence in this space, driven by growing demand for dry cask storage systems, interim storage facilities, and long-term spent fuel management across both operating and shut-down nuclear sites in the country.

Amentum, Bechtel Corporation, and BWX Technologies support market growth through reactor decommissioning, nuclear facility cleanup, waste conditioning, and transport services needed for aging nuclear infrastructure and government-led remediation projects. Waste Control Specialists (a subsidiary of Valhi Inc.) also plays an important role by operating licensed disposal facilities and providing low-level radioactive waste management services within the United States.

Jacobs Solutions Inc. and Fluor Corporation are actively engaged in nuclear site remediation, waste management engineering, and building infrastructure for long-term storage and disposal systems backed by federal cleanup programs. Perma-Fix Environmental Services also supports this space through radioactive waste treatment, processing, and environmental cleanup solutions across industrial, medical, and government nuclear waste streams.

US Radioactive Waste and Nuclear Waste Management Market Recent Developments

On June 2025, EnergySolutions successfully treated and permanently disposed of 1,000 gallons of mixed low-level radioactive waste from the Hanford Site under the U.S. Department of Energy’s Test Bed Initiative. The project included investment in waste treatment, transport, solidification, and disposal infrastructure at the Clive Disposal Facility in Utah, supporting future large-scale nuclear cleanup activities in the United States.

On March 2024, Amentum, along with BWXT Technical Services Group and Fluor Federal Services, received a USD 45 billion contract from the U.S. Department of Energy for radioactive waste cleanup and tank waste management at the Hanford Site in Washington, supporting long-term investment in US nuclear waste treatment and remediation infrastructure.

US Radioactive Waste and Nuclear Waste Management Regional Analysis

In the US Radioactive Waste and Nuclear Waste Management Market, the Southern United States holds a leading position due to the large number of nuclear reactors, waste processing facilities, and major government cleanup projects across states such as Texas, South Carolina, and Tennessee. The region benefits from well-established nuclear infrastructure, continuous spent fuel generation, and ongoing decommissioning activity. Companies including Holtec International, EnergySolutions, and Waste Control Specialists play an important role in supporting storage, disposal, transport, and waste treatment operations across the region.

The Western United States is the fastest-growing region in the market, driven by increasing investment in interim storage infrastructure, nuclear cleanup projects, and advanced waste treatment activities. States such as Utah and Washington are seeing higher levels of activity related to radioactive waste disposal and environmental remediation. Companies including Amentum, NAC International, and Perma-Fix Environmental Services are supporting this growth through spent fuel management, remediation services, and radioactive waste processing solutions.

|

US Radioactive Waste and Nuclear Waste Management Market |

|||

|

Report Coverage |

Details |

||

|

Base Year: |

2025 |

Forecast Period: |

2026-2032 |

|

Historical Data: |

2020 to 2025 |

Market Size in 2025: |

USD 5.61 Bn. |

|

Forecast Period 2026 to 2032 CAGR: |

7.2% |

Market Size in 2032: |

USD 8.95 Bn. |

|

Segments

|

By Waste Type |

|

|

|

By Source

|

|

||

|

By Management Method |

|

||

|

By Disposal Method |

|

||

Key Players Profiles Covered in the Report US Radioactive Waste and Nuclear Waste Management Market

- Holtec International

- EnergySolutions

- Amentum

- Bechtel Corporation

- BWX Technologies

- Waste Control Specialists

- NAC International

- Jacobs Solutions Inc.

- Fluor Corporation

- Perma-Fix Environmental Services

- Westinghouse Electric Company

- NorthStar Group Services

- US Ecology

- Curio

- Studsvik

- Others

Frequently Asked Questions

Deep geological disposal is gaining attention because it provides long-term isolation for high-level radioactive waste and spent nuclear fuel, reducing environmental and radiation risks over extended periods.

Hospitals, diagnostic centers, and cancer treatment facilities generate radioactive waste through nuclear medicine procedures, radiotherapy, and isotope-based diagnostics, supporting demand for safe waste handling and disposal solutions.

Recycling and reprocessing help recover usable nuclear materials from spent fuel, reduce waste volume, improve resource operation, and lower long-term storage requirements.

Emerging economies are expanding nuclear energy capacity to meet rising electricity demand, creating higher requirements for radioactive waste storage, treatment infrastructure, and regulatory waste management systems.

1. US Radioactive Waste and Nuclear Waste Management Market: Introduction

2. US Radioactive Waste and Nuclear Waste Management Market: Executive Summary

2.1. US Radioactive Waste and Nuclear Waste Management Market Size And Forecast (USD Billion)

2.2 Market Definition

2.3 Market Segmentation

2.4 Research Timelines

2.5 Assumptions

2.6 Limitation

3. US Radioactive Waste and Nuclear Waste Management Market: Research Methodology

3.1 Data Mining

3.2 Secondary Research

3.3 Primary Research

3.4 Subject Matter Expert Advice

3.5 Quality Check

3.6 Final Review

3.7 Data Triangulation

3.8 Top-Down Approach

3.9 Bottom-Up Approach

3.10 Research Flow

3.11 Data Sources

4. US Radioactive Waste and Nuclear Waste Management Market: Market Attractiveness Mapping

4. 1 US Radioactive Waste and Nuclear Waste Management Market Overview

4.2 Competitive Analysis: Funnel Diagram (Tier 1, Tier 2, Tier 3)

4.3 US Radioactive Waste and Nuclear Waste Management Market Absolute Market Opportunity

4.4 US Radioactive Waste and Nuclear Waste Management Market Attractiveness Analysis, By Waste Type

4.5 US Radioactive Waste and Nuclear Waste Management Market Attractiveness Analysis, By Source

4.6 US Radioactive Waste and Nuclear Waste Management Market Attractiveness Analysis, By Management Method

4.7 US Radioactive Waste and Nuclear Waste Management Market Attractiveness Analysis, By Disposal Method

4.8 Future Market Opportunities

5. US Radioactive Waste and Nuclear Waste Management Market: Market Outlook

5.1 US Radioactive Waste and Nuclear Waste Management Market Evolution

5.2 US Radioactive Waste and Nuclear Waste Management Adoption Analysis

5.3 Market Trends

5.4 Market Dynamics

5.4.1 Market Drivers

5.4.2 Market Restraints

5.4.3 Market Trends

5.4.4 Market Opportunity

5.5 Porter’s Five Forces Analysis

5.5.1 Threat Of New Entrants

5.5.2 Bargaining Power Of Suppliers

5.5.3 Bargaining Power Of Buyers

5.5.4 Threat Of Substitute Products

5.5.5 Competitive Rivalry Of Existing Competitors

5.6 PESTEL Analysis

5.7 Value Chain Analysis

5.8 System Configuration and Installation Analysis

5.9 Pricing Analysis

5.10 Analysis Opportunity Outlook & Adoption Analysis

5.11 Geopolitical Impact Assessment

5.12 Regulatory Framework and Policy Impact Assessment

5.13 Technology Landscape

6. US Radioactive Waste and Nuclear Waste Management Market: By Waste Type, 2026-2032 (USD Billion)

6.1 Low-Level Waste (LLW)

6.2 Greater-Than-Class-C Waste (GTCC) / Transuranic Waste

6.3 High-Level Waste (HLW)

7. US Radioactive Waste and Nuclear Waste Management Market: By Source, 2026-2032 (USD Billion)

7.1 Nuclear Power Plants

7.2 Medical & Healthcare Facilities

7.3 Industrial Applications

7.4 Research & Academic Institutions

7.5 Defense & Government Organizations

8. US Radioactive Waste and Nuclear Waste Management Market: By Management Method, 2026-2032 (USD Billion)

8.1 Storage

8.2 Treatment & Processing

8.3 Recycling & Reprocessing

8.4 Transportation

9. US Radioactive Waste and Nuclear Waste Management Market: By Disposal Method, 2026-2032 (USD Billion)

9.1 Near-Surface Disposal

9.2 Deep Geological Disposal

9.3 Borehole Disposal

9.4 Landfill Disposal Others

10. US Radioactive Waste and Nuclear Waste Management Competitive Matrix

11. US Radioactive Waste and Nuclear Waste Management Market: Company Benchmarking

12. Merger & Acquisition

13. US Radioactive Waste and Nuclear Waste Management Market: Company Profiles

14. Risk Assessment and Scenario Analysis

15. Strategic Opportunity

16. Investments & Funding Analysis

17. Strategic Roadmap

19. Analyst Recommendations