Hyper Scale Data Center Market Size by Power Capacity, Data Center Type, Component, End User, Region, Country-level Analysis, Competitive Landscape, and Future Outlook (2026–2032)

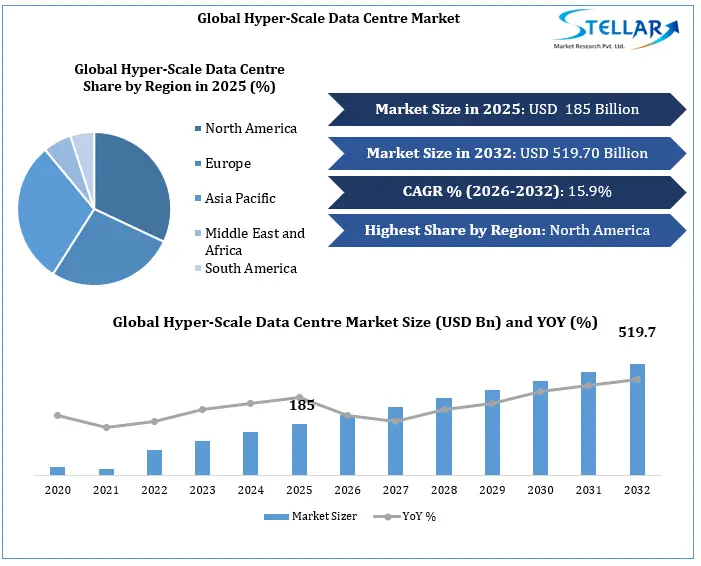

Global Hyper-Scale Data Centre Market was valued at USD 185.0 billion in 2025 and is forecast to reach USD 519.70 billion by 2032, growing at a 15.9% CAGR. AI infrastructure, cloud region expansion, GPU clusters, liquid cooling, and power infrastructure upgrades are driving hyper-scale capacity investment.

Global Hyper-Scale Data Centre Market Overview

The Global Hyper Scale Data Center Market is shifting from simple capacity expansion for cloud services to bigger, energy-hungry, AI-optimized campuses. Providers of cloud services, web-based enterprises, colocation service providers, and other investors are opting for facilities with the capability to offer MW-scale capacity, GPU computing farms, large server rooms, fast network links, fiber connectivity, liquid-cooling technology, backup power supply, and automated operations.

Highest growth rates are seen in places with cloud service adoption, data sovereignty considerations, availability of energy sources, and colocation leasing facilities. The highest revenue by far is generated in North America because of its major AI facility deployments and cloud providers' capital expenditure. The fastest-growing region is Asia Pacific, consisting of India, China, Japan, Southeast Asia, and Australia. Growth in Europe is being driven by data sovereignty requirements, renewable energy access, and policies for establishing AI Gigafactories.

To get more Insights: Request Free Sample Report

Global Hyper-Scale Data Centre Market Definition & Scope

Hyper scale data centers are large and scalable digital infrastructure facilities that support cloud computing, AI workloads, data storage, digital platforms, high-performance computing, and internet-scale applications. These facilities bring together cloud infrastructure, AI computing capacity, MW-scale power, high-density racks, servers, storage, networking, power systems, cooling systems, automation, and campus-level infrastructure to handle large volumes of digital workloads.

The Global Hyper Scale Data Center Market tracks spending on hyper scale infrastructure. This includes investment in facility construction, IT equipment, power systems, cooling systems, networking equipment, DCIM software, automation, security systems, engineering, fit-out, and managed infrastructure services. The market value covers the deployment, expansion, modernization, and lifecycle support of hyper scale cloud, AI-ready, and colocation campuses.

Global Hyper-Scale Data Centre Market Growth Drivers

GPU cluster deployment is expanding hyper scale campus size.

Hyper scale operators are building larger campuses to host GPU clusters for AI training and inference workloads. This directly increases spending on servers, storage, networking, power distribution, liquid cooling, and high-density white-space infrastructure.

Power availability has become a site-selection driver:

Data center location decisions now depend heavily on access to large MW capacity, substations, grid connection, transmission lines, and renewable power contracts. Markets with faster power approvals are attracting more hyper scale investment.

Cloud providers are adding regional availability zones:

AWS, Microsoft, Google Cloud, Oracle, Alibaba Cloud, and other providers are expanding cloud regions and availability zones to improve latency, resilience, and regulatory compliance. This creates steady demand for new hyper scale data center campuses.

AI workloads are increasing cost per MW:

AI-ready facilities cost more per MW than traditional cloud data centers because they require high-density racks, advanced cooling, high-speed networking, backup power, and stronger electrical systems. This increases total market value even when capacity growth is constrained.

Global Hyper-Scale Data Centre Market Opportunities

Direct-to-chip liquid cooling creates a new infrastructure upgrade cycle:

AI racks are pushing operators toward direct-to-chip cooling, coolant distribution units, rear-door heat exchangers, and liquid-compatible rack designs. This creates a strong opportunity for cooling vendors, engineering firms, and campus retrofit providers.

Behind-the-meter power can unlock large AI campuses:

Hyper scale operators are exploring dedicated substations, on-site generation, battery storage, fuel cells, and direct renewable energy arrangements. These models can reduce grid dependency and speed up AI campus development.

Secondary data center markets are becoming hyper scale destinations:

Power-constrained hubs such as Northern Virginia, Dublin, Frankfurt, and Singapore are pushing new investment toward secondary markets with better land, power, tax incentives, and permitting flexibility.

AI inference demand supports distributed hyper scale capacity:

AI inference workloads need capacity closer to users, enterprises, and regional cloud zones. This creates demand for smaller hyper scale nodes, regional colocation campuses, and cloud availability zone expansion.

Global Hyper-Scale Data Centre Market Trends

Hyper scale campuses are moving toward 100 MW–300 MW development blocks:

Many operators are designing campuses in scalable power blocks instead of single-building projects. The 100 MW–300 MW range is becoming the core development model because it balances capacity scale with grid and permitting feasibility.

Above-500 MW AI campuses are emerging but remain selective:

Gigawatt-scale AI campuses are gaining attention, but only a few markets can support them. These projects require exceptional access to land, power, transmission, cooling, and long-term financing.

White-space design is being rebuilt around AI rack density:

Traditional rack layouts are being redesigned for GPU clusters, high-speed interconnects, heavier racks, liquid cooling loops, and higher floor loading requirements. This changes how operators plan halls, power distribution, and cooling zones.

Power contracts are becoming as important as tenant contracts:

A hyper scale project is no longer bankable only because it has a cloud or AI tenant. Investors also want proof of secured MW capacity, grid connection timelines, energy pricing, and renewable power availability.

Global Hyper-Scale Data Centre Market Challenges

Converting announced AI capacity into delivered MW

Many hyper scale announcements are large, but actual delivery depends on power, permits, equipment, construction labour, and commissioning. The key challenge is turning planned AI campuses into operational capacity.

Balancing AI rack density with facility reliability

Higher rack density increases stress on power distribution, cooling loops, backup systems, and monitoring tools. Operators must support AI loads without compromising uptime and redundancy.

Managing stranded capacity risk

Some campuses may have available building space but not enough power or cooling capacity to use it fully. This creates stranded white-space risk and lowers asset productivity.

Securing long-term power at predictable cost

AI-ready hyper scale data centers consume large amounts of electricity. Volatile power prices and uncertain grid tariffs can affect long-term project economics.

Reducing PUE while supporting higher compute density

Operators must improve energy efficiency even as AI workloads increase heat and power demand. Maintaining low power usage effectiveness becomes harder in high-density GPU environments.

Global Hyper-Scale Data Centre Market Segmentation Analysis

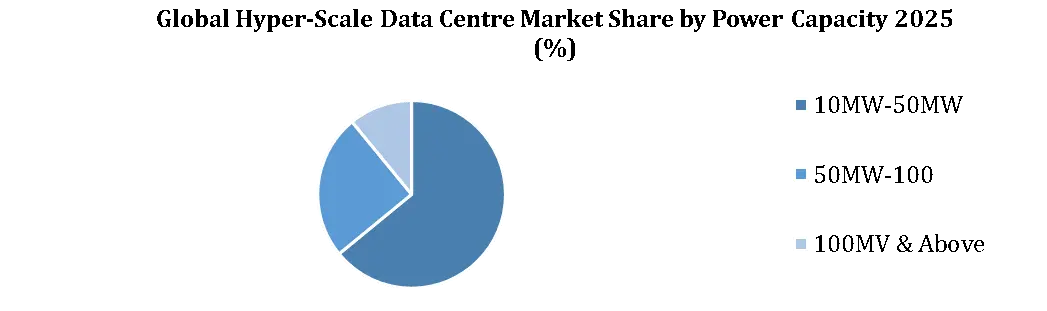

Hyper-Scale Data Centre Market Size by power capacity

The market includes 10 MW to 50 MW, 50 MW to 100 MW, and above 100 MW. The 50 MW to 100 MW segment leads with a 38% share because it supports large hyper scale facilities, cloud region expansion, wholesale colocation demand, and AI-ready builds without requiring extreme grid commitments. The 10 MW to 50 MW segment serves regional hyper scale sites and enterprise-scale facilities, while the above-100 MW segment is growing through large AI campuses and multi-building GPU cluster developments.

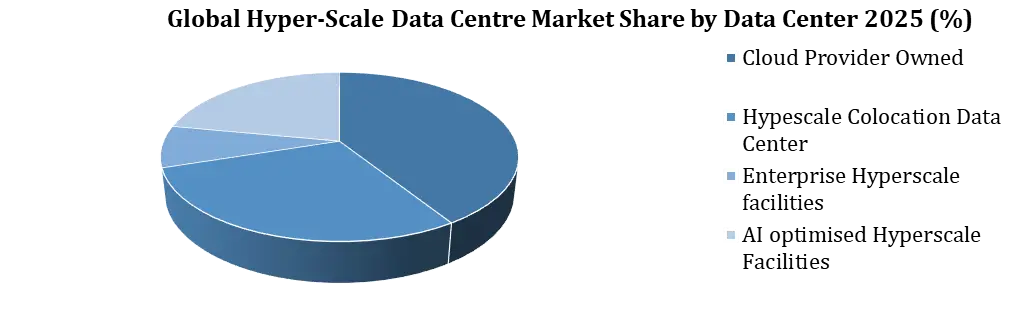

Global Hyper-Scale Data Centre Market Size by Data Center Type

The market includes cloud provider-owned hyper scale data centers, hyper scale colocation data centers, enterprise hyper scale facilities, and AI-optimized hyper scale facilities. Cloud provider-owned hyper scale data centers lead with a 41% share because major cloud operators build large campuses to support cloud regions, availability zones, AI services, storage demand, and sovereign cloud workloads. Hyper scale colocation facilities are expanding through large MW leasing, while AI-optimized facilities are gaining demand as GPU cluster adoption increases.

Global Hyper-Scale Data Centre Market Size by Component

The market includes servers and storage, networking equipment, power systems, cooling systems, DCIM and monitoring software, and services. Servers and storage lead with a 39% share because AI-ready facilities need large volumes of GPU servers, high-performance computer systems, storage platforms, and rack-scale infrastructure. Networking, power, and cooling systems remain important as rack density rises, while DCIM, monitoring software, and services improve uptime and operating efficiency.

Global Hyper-Scale Data Centre Market Size by End User

The market includes cloud service providers, colocation providers, large internet and content companies, BFSI and enterprise technology buyers, and government and public sector agencies. Cloud service providers lead with a 45% share because they drive major investments in cloud regions, availability zones, AI infrastructure, data localization, and enterprise workload migration. Colocation providers support outsourced capacity demand, while internet companies, enterprises, and public agencies add demand for AI, storage, and secure cloud infrastructure.

Global Hyper-Scale Data Centre Market Regional Analysis

North America leads the Global Hyper Scale Data Center Market with 42% share in 2025. The region benefits from heavy cloud provider capex, large AI infrastructure programs, GPU cluster deployment, hyper scale colocation leasing, strong fiber connectivity, and mature power procurement models. The U.S. remains the core market because AWS, Microsoft, Google, Meta, Oracle, and major colocation operators continue to build large cloud and AI-ready campuses.

Asia Pacific is the second-largest and fastest-expanding region. Growth is supported by cloud region expansion in India, China, Japan, Singapore, Australia, South Korea, and Southeast Asia. Data localization, digital economy growth, enterprise cloud migration, AI adoption, and government-backed digital infrastructure programs are increasing demand for hyper scale campuses, colocation facilities, power systems, cooling infrastructure, and server capacity.

Europe holds a strong position because of data sovereignty, regulated enterprise demand, renewable energy access, and rising AI infrastructure investment. Key markets such as Germany, the UK, France, the Netherlands, Ireland, Spain, and the Nordics are attracting hyper scale and colocation investment. However, grid constraints, permitting rules, land availability, and sustainability scrutiny are slowing capacity delivery in some mature hubs.

Middle East & Africa is still a smaller market but is gaining momentum. Gulf countries such as the UAE and Saudi Arabia are investing in sovereign cloud, AI infrastructure, digital government platforms, smart cities, and renewable-backed data center capacity. Africa is growing from a lower base, with demand supported by cloud adoption, internet penetration, fintech growth, and regional colocation development. South America is an emerging hyper scale data center region led by Brazil, Chile, Colombia, and Argentina. Growth is supported by cloud adoption, subsea cable connectivity, digital banking, e-commerce, content delivery, and regional AI inference demand. The region remains smaller than North America, Europe, and Asia Pacific, but improving connectivity and rising enterprise cloud demand are creating steady opportunities for hyper scale and colocation expansion.

Global Hyper-Scale Data Centre Market Competitive Analysis

The Global Hyper Scale Data Center Market is highly competitive, with cloud and internet-scale operators leading the market. Major players such as Amazon Web Services, Microsoft, Google Cloud, Meta, Oracle, Alibaba Cloud, ten cent Cloud, China Telecom, China Mobile, and China Unicom create strong demand for cloud regions, availability zones, AI-ready campuses, GPU clusters, storage capacity, network switching, and high-density data center infrastructure.

Hyper scale colocation providers such as Equinix, Digital Realty, NTT Global Data Centers, Vantage Data Centers, QTS, CyrusOne, STACK Infrastructure, Global Switch, and Iron Mountain Data Centers are becoming key capacity partners for cloud and AI customers. Their role is moving beyond traditional colocation toward large MW campuses, powered shells, build-to-suit facilities, pre-leased AI-ready halls, renewable-backed campuses, and regional expansion platforms.

Infrastructure suppliers such as Schneider Electric, Vertiv, Eaton, ABB, Siemens, Legrand, Johnson Controls, Carrier, Trane Technologies, STULZ, Dell Technologies, Hewlett Packard Enterprise, Lenovo, Cisco, Arista Networks, NVIDIA, and Supermicro support the market with power systems, cooling equipment, racks, DCIM, servers, storage, GPUs, AI systems, and high-speed networking. Their competitiveness depends on how quickly they can support high-density racks, liquid cooling, resilient power design, and scalable AI infrastructure deployment.

Global Hyper-Scale Data Centre Market Recent Development

January 2025, OpenAI announced the Stargate Project with SoftBank, Oracle, and MGX to invest up to USD 500 billion over four years in new AI infrastructure in the United States. The initial plan included immediate deployment of USD 100 billion for AI infrastructure. The development shows how dedicated AI infrastructure programs are becoming a direct source of hyper scale data center construction, power systems, GPU servers, and high-density networking demand.

September 2025, OpenAI, Oracle, and SoftBank expanded the Stargate AI infrastructure program with five new U.S. data center sites. The combined capacity from the five new sites, the Abilene flagship site, and ongoing CoreWeave projects brought Stargate to nearly 7 GW of planned capacity and more than USD 400 billion of investment over three years. The development shows how AI partnerships are shifting hyper scale demand toward dedicated AI campuses with very high power, cooling, server, and networking requirements.

October 2025, Google announced its first AI hub in India, including a purpose-built data center campus in Visakhapatnam. The hub includes gigawatt-scale compute capacity and is supported by partners such as AdaniConneX and Airtel. The development shows how hyper scale operators are expanding into high-growth digital markets to meet AI demand, data localization needs, and cloud availability requirements.

October 2025, Meta entered a USD 27 billion financing agreement with Blue Owl Capital for its Hyperion data center project in Louisiana. The project supports Meta’s AI infrastructure expansion and is expected to provide more than 2 GW of compute capacity. The development shows how hyper scale AI campuses are increasingly using private-capital structures to fund very large data center programs.

November 2025, Google announced a USD 40 billion investment in Texas through 2027 to build cloud and AI infrastructure, including three new data centers. The investment strengthens U.S. hyper scale capacity and connects AI workload growth with land, energy access, and regional cloud expansion. The development shows how major cloud providers are using large state-level investment programs to secure scalable data center capacity.

On May 2026, I Squared Capital acquired 10 U.S. data center facilities from Cogent Fiber for USD 225 million and committed an additional USD 1 billion for upgrades, expansion, and further acquisitions. The assets provide 53 MW of power capacity and colocation space across nine U.S. markets. The development shows how infrastructure investors are targeting AI inference and distributed data center capacity, not only large centralized AI training campuses.

Global Hyper Scale Data Center Market Regulatory framework

The regulatory framework for the Global Hyper Scale Data Center Market is becoming stricter as governments focus on energy reporting, grid connection, sustainability, data sovereignty, and facility security. The EU has one of the clearest frameworks, as data centers with installed IT power demand above 500 kW must report annual energy and sustainability indicators such as power usage effectiveness, water usage effectiveness, energy reuse, and renewable energy use. In the U.S., there is no single federal data center law, but the Department of Energy has highlighted rapid data center load growth, making utility approvals, grid planning, power procurement, and energy efficiency more important for hyper scale campus development. These requirements directly affect hyper scale operators because new data center campuses must secure power access, manage cooling demand, prove energy efficiency, source renewable power, and maintain operational transparency.

In Asia Pacific, regulation is moving toward controlled data center growth, green power use, and national digital infrastructure development. Singapore’s Green Data Centre Roadmap supports sustainable data center expansion through energy efficiency and green energy adoption, while India’s draft Data Centre Policy promotes data center parks and minimum standards for build, IT, non-IT, and security infrastructure. For hyper scale operators, market attractiveness now depends on more than cloud demand; it also depends on clear land approvals, grid connection timelines, renewable energy access, water-efficient cooling options, security compliance, and data localization support. As a result, regions with strong digital policy, reliable power planning, faster permitting, and sustainability-focused infrastructure rules are better positioned to attract cloud regions, AI-ready campuses, and hyper scale colocation investment.

|

Global Hyper-Scale Data Centre Market |

|||

|

Report Coverage |

Details |

||

|

Base Year: |

2025 |

Forecast Period: |

2026-2032 |

|

Historical Data: |

2020 to 2025 |

Market Size in 2025: |

USD 185 Bn. |

|

Forecast Period 2026 to 2032 CAGR: |

15.9% |

Market Size in 2032: |

USD 519.7 Bn. |

|

Segments

|

By Power Capacity |

|

|

|

By Data Center type

|

|

||

|

By Component |

|

||

|

By End User |

|

||

Key Players Covered in the Hyper Scale Data Center Market Report

- Amazon Web Services

- Microsoft Azure

- Google Cloud

- Meta

- Oracle Cloud Infrastructure

- Equinix

- Digital Realty

- NTT Global Data Centers

- Vantage Data Centers

- QTS Data Centers

- CyrusOne

- STACK Infrastructure

- Schneider Electric

- Vertiv

- Eaton

- Dell Technologies

- Hewlett Packard Enterprise

- NVIDIA

- Cisco

- Arista Networks

Frequently Asked Questions

The Global Hyper Scale Data Center Market is estimated at USD 185.0 billion in 2025.

The market is expected to reach USD 520.0 billion by 2032, growing at a CAGR of 15.9% from 2025 to 2032.

The 50 MW to 100 MW segment leads the market with 38% share because it fits large hyper scale facilities, cloud region expansion, wholesale colocation demand, and AI-ready builds.

Key players include Amazon Web Services, Microsoft Azure, Google Cloud, Meta, Oracle Cloud Infrastructure, Equinix, Digital Realty, NTT Global Data Centers, Vantage Data Centers, QTS Data Centers, Schneider Electric, Vertiv, Dell Technologies, NVIDIA, Cisco, and Arista Networks.

1. Global Hyper Scale Data Center Market Introduction

2. Global Hyper Scale Data Center Market Executive Summary

2.1. Global Hyper Scale Data Center Market Size and Forecast (USD Billion)

2.2 Market Definition

2.3 Market Segmentation

2.4 Research Timelines

2.5 Assumptions

2.6 Limitation

3.1 Data Mining

3.2 Secondary Research

3.3 Primary Research

3.4 Subject Matter Expert Advice

3.5 Quality Check

3.6 Final Review

3.7 Data Triangulation

3.8 Top-Down Approach

3.9 Bottom-Up Approach

3.10 Research Flow

3.11 Data Sources

4. 1 Global Hyper Scale Data Center Market Overview

4.2 Competitive Analysis: Funnel Diagram (Tier 1, Tier 2, Tier 3)

4.3 Global Hyper Scale Data Center Market Absolute Market Opportunity

4.4 Global Hyper Scale Data Center Market Attractiveness Analysis, By Region

4.5 Global Hyper Scale Data Center Market Attractiveness Analysis, By Power Capacity

4.6 Global Hyper Scale Data Center Market Attractiveness Analysis, By Data Center Type

4.7 Global Hyper Scale Data Center Market Attractiveness Analysis, By Component

4.8 Global Hyper Scale Data Center Market Attractiveness Analysis, By End User

4.10 Future Market Opportunities

5.1 Global Hyper Scale Data Center Market Evolution

5.2 Global Hyper Scale Data Center Adoption Analysis

5.3 Market Trends

5.4 Market Dynamics

5.4.1 Market Drivers

5.4.2 Market Restraints

5.4.3 Market Trends

5.4.4 Market Opportunity

5.5 Porter’s Five Forces Analysis

5.5.1 Threat of New Entrants

5.5.2 Bargaining Power of Suppliers

5.5.3 Bargaining Power of Buyers

5.5.4 Threat of Substitute Products

5.5.5 Competitive Rivalry of Existing Competitors

5.6 PESTEL Analysis

5.7 Value Chain Analysis

5.8 System Configuration and Installation Analysis

5.9 Pricing Analysis

5.10 Analysis Opportunity Outlook & Adoption Analysis

5.11 Geopolitical Impact Assessment

5.12 Regulatory Framework and Policy Impact Assessment

5.13 Technology Landscape

6. Global Hyper Scale Data Center Market Size By Power Capacity, 2026-2032 (USD Billion)

6.1 10 MW- 50MW

6.2 50MW- 100MW

6.3 100MW & Above

7. Global Hyper Scale Data Center Market Size By Component, 2026-2032 (USD Billion)

7.1 Servers and Storage

7.2 Networking Equipment

7.3 Power Systems

7.4 Cooling Systems

7.5 DCIM and Monitoring Software

7.6 Services

8. Global Hyper Scale Data Center Market Size By Data Center Type, 2026-2032 (USD Billion)

8.1 Cloud Provider-Owned Hyper Scale Data Centers

8.2 Hyper scale Colocation Data Centers

8.3 Enterprise Hyper Scale Facilities

8.4 AI-Optimized Hyper Scale Facilities

9. Global Hyper Scale Data Center Market Size By End User, 2026-2032 (USD Billion)

9.1 Cloud Service Providers

9.2 Colocation Providers

9.3 Large Internet and Content Companies

9.4 BFSI and Enterprise Technology Buyers

9.5 Government and Public Sector Agencies

10. Global Hyper Scale Data Center Market Size Geography, 2026-2032 (USD Billion)

10.1 North America Global Hyper Scale Data Center Market

10.2 Europe Global Hyper Scale Data Center Market

10.3 Asia Pacific Global Hyper Scale Data Center Market

10.4 South America Global Hyper Scale Data Center Market

10.5 Middle East and Africa Global Hyper Scale Data Center Market

11. Global Hyper Scale Data Center Competitive Matrix

12. Global Hyper Scale Data Center Market: Company Benchmarking

13. Merger & Acquisition

14. Global Hyper Scale Data Center Market: Company Profiles

1. Amazon Web Services

2. Microsoft Azure

3. Google Cloud

4. Meta

5. Oracle Cloud Infrastructure

6. Equinix

7. Digital Realty

8. NTT Global Data Centers

9. Vantage Data Centers

10. QTS Data Centers

11. CyrusOne

12. STACK Infrastructure

13. Schneider Electric

14. Vertiv

15. Eaton

16. Dell Technologies

17. Hewlett Packard Enterprise

18. NVIDIA

19. Cisco

20. Arista Networks

21. Others

15. Risk Assessment and Scenario Analysis

16. Strategic Opportunity

17. Investments & Funding Analysis

18. Strategic Roadmap

19. Analyst Recommendations