Light Beer Market Global Industry Analysis and Forecast (2026-2032)

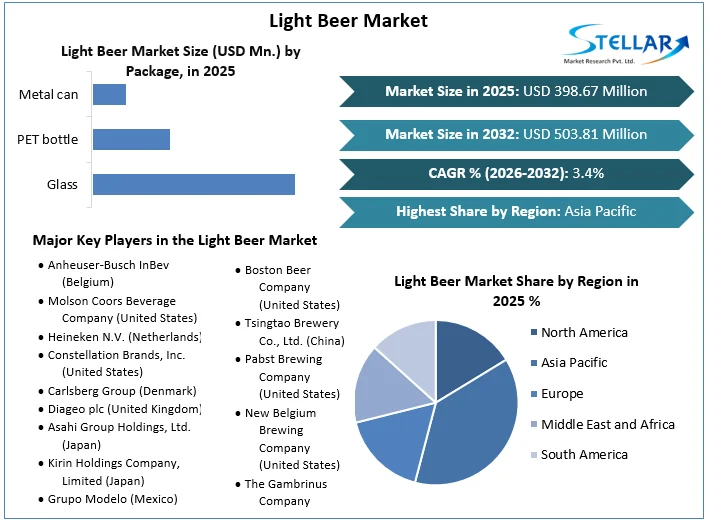

The Light Beer Market size was valued at USD 398.67 Mn. in 2025 and the total Global Light Beer revenue is expected to grow at a CAGR of 3.4 % from 2026 to 2032, reaching nearly USD 503.81 Mn. by 2032.

Light Beer Market Overview

Light beer is distinguished by its lower alcohol content or reduced calorie count compared to regular beers. Some popular light beer brands include Miller Lite, Bud Light, Coors Light, and Michelob Ultra. These brands have gained popularity among individuals. As one of the oldest known beverages, beer holds the distinction of being the world’s most widely consumed drink, ranking third in popularity after water and tea.

The popularity of craft brewing, with its emphasis on small-batch production and unique flavors, has further contributed to the growth of the beer market in these regions. The rise of craft brewing has had a significant impact on the light beer market. Craft breweries, with their focus on small-batch production and unique flavors, have brought diversity and innovation to the industry. This has not only created new opportunities for beer enthusiasts to explore different tastes but has also boost the growth of the overall market by attracting a wider consumer base. Due to its lighter profile, light beer appeal s to consumers seeking a beverage with fewer calories and less alcohol, while still retaining flavor and refreshment.

The global beer market encompasses over 10,000 breweries globally, with a concentration in the United States and Europe, which collectively account more than 50% of the global brewery count. According to a recent study by the SMR Research Corporation, conducted in 209 countries and territories, the across the world number of breweries has surged to over 19,000 as of 2023. This growth is primarily attributed to the rising prominence of craft breweries, which now represent 94% of all breweries globally. Significantly, the United States leads in craft brewery density, boasting 4,750 establishments, showcasing the significant contribution of craft brewing to the Light beer market's growth. The concentration of breweries in the United States and Europe is attributed to a combination of historical factors, cultural traditions, and market demand.

Light Beer Market Methodology

Stellar Market Research published a report that analyzes Light Beer Market trends to predict the market's growth. The report provides detailed insights into the five major elements (size, share, scope, growth, and potential of the industry). It offers valuable information to help businesses identify opportunities and potential risks within the market. This detailed report ensures an in-depth analysis of the subject matter. The report also provides insights on market overview, market segmentation, current and future growth analysis, competitive landscape, and other such premium insights within the forecast period.

The research objective of the report is to provide a report with an in-depth analysis of the Light Beer market by Package, Production, Distribution Channel, and region. It also offers comprehensive data on factors affecting the market and evaluates competition -mergers and expansions, product launches, and technological advancements within the market. Key players play a crucial role in driving innovation in diagnostics technology, underscoring the importance of targeted strategies to meet evolving consumer demands. Through quantitative research methods, the report offers statistical data on the effectiveness of Light Beer and its impact on market trends. Competitive intelligence analysis aids in comprehending market dynamics, competitor strategies, and customer perceptions, empowering market players to gain a competitive advantage in the global Light Beer Market.

To get more Insights: Request Free Sample Report

Light Beer Market Dynamics

Changing Consumer Preferences to drives the Light Beer Market Growth

Shifting consumer preferences towards healthier beverage choices have sparked remarkable growth in the light beer market globally. With an increasing focus on wellness and calorie-conscious lifestyles, consumers across the globe are turning to light beers for their lower calorie and alcohol content. This trend is particularly pronounced in developed markets where health consciousness is high. Light beers offer consumers the opportunity to enjoy their favorite beverage with reduced guilt, catering to their desire for balance and moderation.

The availability of a wide variety of flavors and effective marketing campaigns has significantly boosted the popularity of light beers among consumers globally. Breweries are actively expanding their light beer offerings to meet this growing demand, thereby driving the overall growth of the light beer market on a global scale. As consumers continue to prioritize health and wellness, the light beer segment is expected to maintain its upward trajectory in the global beverage market.

For Instance, According to SMR study Report in United Kingdom approximately 41% of adults consider calorie content, with 26% actively seeking lower-calorie options. This shift is reflected in market data, as sales of lower-calorie beers surged by more than 17% in 2024. Also, In United Kingdom 12% increase in sales of "light" or "low-carb" beers in the same year, echoing consumer preferences for reduced carbohydrate content. Younger demographics are particularly engaged in this trend, with a YouGov survey showing that 36% of adults aged 18-34 actively seek out beers with fewer carbs and calories. 31% of UK beer consumers prioritize low-calorie or light beer options, with 19% specifically looking for reduced carbohydrate content.

Raw Material Challenges Creates Barrier to Light Beer Market Growth

The growth of the Light Beer Market faces significant hurdles due to challenges associated with raw materials. Fluctuating prices of essential ingredients such as barley and hops, influenced by unpredictable weather conditions and global market dynamics, elevate production expenses. Consequently, this potentially led to increased consumer prices and diminished market competitiveness within the Light Beer Industry. Also, environmental adversities such as droughts and unsustainable agricultural practices disrupt the raw material supply chain. This, in turn, limits breweries' access to consistent, high-quality resources essential for production within the Light Beer Market.

In the production of light beer, specialized ingredients and processes are often required to achieve the desired lower calorie and alcohol content while maintaining flavor and quality. This adds complexity to the sourcing and procurement process, further exacerbating raw material challenges. The Light Beer Market faces significant challenges related to sourcing raw materials. Fluctuating prices of essential ingredients, environmental adversities, and the complexity of production processes all contribute to these challenges.

Innovation in Flavors creates lucrative growth opportunities for the Light Beer Market Growth

The evolving Light Beer Market, the chance to innovate with flavors stands out as a significant opportunity for breweries to boost growth. Through expanding their range of offerings with exciting flavor profiles, breweries provide to changing consumer tastes, broaden their customer base, and stay ahead in a competitive industry.

- For Instance, the trend of fruit-infused light beers, exemplified by brands like Corona Refresca and Michelob Ultra Infusions. These beverages, featuring flavors such as Passionfruit Lime and Pomegranate & Agave, appeal to a wider audience beyond traditional beer drinkers, offering a refreshing and tropical twist to the category. Craft breweries such as Dogfish Head Brewery also contribute to this trend by experimenting with unique ingredients like monk fruit in their Slightly Mighty IPA, appealing to health-conscious consumers seeking flavorful yet low-calorie options.

Embracing flavor innovation, breweries continuously engage consumers and drive interest in light beer. This strategy differentiates brands in a crowded market and taps into the growing demand for variety and excitement among consumers. Through ongoing exploration and creativity, breweries unlock endless possibilities for flavor innovation, strengthening their position in the Light Beer Market and helps to long-term growth.

Light Beer Market Related Regulations

The regulations for light beer vary by country and event, but there are some common rules that are often followed.

|

Aspect |

Regulations and Innovations |

|

Beer Mile Requirements |

- Beer must be canned or bottled |

|

- Minimum volume of 355mL (12 Oz) |

|

|

- Minimum alcohol content of 5% |

|

|

- Must be brewed from malted cereal grains and flavored with hops |

|

|

Beer Consumption |

- Must be consumed within the transition area before each lap |

|

Production Methods |

- Use of glucoamylase enzyme to metabolize residual carbohydrates |

|

- Pilot studies with genetically engineered yeast strains |

|

|

to enhance fermentability while maintaining flavor |

Light Beer Market Segment Analysis

Based On production, the Micro-brewery sub segment dominated the production segment of the global light beer market in the year 2025. The rise of craft beer culture has boosted the proliferation of microbreweries, which are often characterized by their emphasis on small-scale, artisanal production methods and a commitment to quality and innovation. These microbreweries have capitalized on consumer preferences for unique and flavorful brews, leveraging their flexibility to experiment with diverse ingredients and brewing techniques.

Also, the increasing demand for localized and niche products has played into the hands of microbreweries, allowing them to establish strong connections with local communities and build loyal customer bases. Their ability to adapt quickly to changing consumer trends and preferences has given them a competitive edge over larger breweries, enabling them to cater to a more discerning audience seeking authenticity and variety in their beer choices. As a result, microbreweries have successfully carved out a significant share of the global light beer market, driving growth and shaping industry trends in the process.

Light Beer Market Regional Analysis

Asia Pacific Region dominated the Light Beer Market in the year 2025. The region's burgeoning population, coupled with rapid urbanization and rising disposable incomes, has been responsible for a significant increase in beer consumption. As a result, major breweries and microbreweries alike have intensified their focus on the Asia Pacific market, recognizing its vast potential for growth.

The diverse cultural landscape of the Asia Pacific region has contributed to the popularity of light beer, with breweries tailoring their products to suit local tastes and preferences. From Japan's growing interest in craft beer to India's preference for milder flavors, breweries have adapted their offerings to resonate with diverse consumer segments across the region. Also, supportive regulatory environments and increasing investments in brewing infrastructure have facilitated the growth of the light beer market in Asia Pacific.

The impact of cultural diversity on beer consumption in the Asia Pacific region cannot be overstated. Breweries have recognized the need to tailor their products to suit local tastes and preferences, leading to the popularity of light beer. From Japan's growing interest in craft beer to India's preference for milder flavors, breweries have successfully resonated with diverse consumer segments, driving the growth of the light beer market in Asia Pacific.

Government initiatives aimed at promoting tourism and fostering economic development have provided a conducive environment for breweries to thrive, driving production and distribution efforts. Government initiatives aimed at promoting tourism and fostering economic development have provided a conducive environment for breweries to thrive, driving production and distribution efforts. These initiatives include tax incentives, streamlined regulations, and infrastructure investments that support the growth of the beer industry. By creating a favorable business climate, governments in the Asia Pacific region have attracted both domestic and international breweries, further fueling the expansion of the light beer market.

|

Light Beer Market Scope |

|

|

Market Size in 2025 |

USD 398.67 Mn |

|

Market Size in 2032 |

USD 503.81 Mn |

|

CAGR (2026-2032) |

3.4 % |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segments |

By Production Macro-brewery Micro-brewery Craft brewery Others |

|

By Package Glass PET bottle Metal can Other |

|

|

By Distribution Channel Hypermarkets & Supermarket On-trade Specialty Stores Convenience Store Other |

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Players in the Light Beer Market

- Anheuser-Busch InBev (Belgium)

- Molson Coors Beverage Company (United States)

- Heineken N.V. (Netherlands)

- Constellation Brands, Inc. (United States)

- Carlsberg Group (Denmark)

- Diageo plc (United Kingdom)

- Asahi Group Holdings, Ltd. (Japan)

- Kirin Holdings Company, Limited (Japan)

- Grupo Modelo (Mexico)

- Boston Beer Company (United States)

- Tsingtao Brewery Co., Ltd. (China)

- Pabst Brewing Company (United States)

- New Belgium Brewing Company (United States)

- The Gambrinus Company (United States)

- Stone Brewing (United States)

- Brooklyn Brewery (United States)

- Deschutes Brewery (United States)

- Sierra Nevada Brewing Co. (United States)

- Ballast Point Brewing Company (United States)

Frequently Asked Questions

Rhe rising health-conscious consumers drives the growth of Light Beer market. Light beers are perceived as a healthier alternative to regular beers due to their lower calorie and carbohydrate content. This trend is likely to continue as people become more focused on health and wellness.

Investors can capitalize on opportunities in the Light Beer market by focusing on companies that are leading in innovation trends such as Flavored light beers are becoming increasingly popular, particularly among younger consumers. This is due to the wider variety of flavors available and the perception that flavored light beers are more refreshing and less bitter than traditional light beers. Additionally, investing in companies with strong distribution channels and a growing online retail presence can offer the potential for growth as the market expands globally.

The Market size was valued at USD 398.67 Million in 2025 and the total Market revenue is expected to grow at a CAGR of 3.4 % from 2026 to 2032, reaching nearly USD 503.81 Million.

The segments covered in the market report are Production, Package, Distribution Channel, and region.

1. Research Methodology

1.1 Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Research Assumption

2. Light Beer Market Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026– 2032) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Global Light Beer Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Product Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. Product Launches and Innovations

4. Light Beer Market: Dynamics

4.1. Light Beer Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Light Beer Market Drivers

4.3. Light Beer Market Restraints

4.4. Light Beer Market Opportunities

4.5. Light Beer Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factor

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Value Chain Analysis and Supply Chain Analysis

4.10. Regulatory Landscape

4.10.1. Market Regulation by Region

4.10.1.1. North America

4.10.1.2. Europe

4.10.1.3. Asia Pacific

4.10.1.4. Middle East and Africa

4.10.1.5. South America

4.10.2. Impact of Regulations on Market Dynamics

5. Light Beer Market: Global Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Litres) (2025-2032)

5.1. Light Beer Market Size and Forecast, by Production (2025-2032)

5.1.1. Macro-brewery

5.1.2. Micro-brewery

5.1.3. Craft brewery

5.1.4. Others

5.2. Light Beer Market Size and Forecast, by Package (2025-2032)

5.2.1. Glass

5.2.2. PET bottle

5.2.3. Metal can

5.2.4. Other

5.3. Light Beer Market Size and Forecast, by Distribution Channel (2025-2032)

5.3.1. Hypermarkets & Supermarket

5.3.2. On-trade

5.3.3. Specialty Stores

5.3.4. Convenience Store

5.3.5. Other

5.4. Light Beer Market Size and Forecast, by Region (2025-2032)

5.4.1. North America

5.4.2. Europe

5.4.3. Asia Pacific

5.4.4. Middle East and Africa

5.4.5. South America

6. North America Light Beer Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Litres) (2025-2032)

6.1. North America Light Beer Market Size and Forecast, by Production (2025-2032)

6.1.1. Macro-brewery

6.1.2. Micro-brewery

6.1.3. Craft brewery

6.1.4. Others

6.2. North America Light Beer Market Size and Forecast, by Package (2025-2032)

6.2.1. Glass

6.2.2. PET bottle

6.2.3. Metal can

6.2.4. Other

6.3. North America Light Beer Market Size and Forecast, by Distribution Channel (2025-2032)

6.3.1. Hypermarkets & Supermarket

6.3.2. On-trade

6.3.3. Specialty Stores

6.3.4. Convenience Store

6.3.5. Other

6.4. North America Light Beer Market Size and Forecast, by Country (2025-2032)

6.4.1. United States

6.4.2. Canada

6.4.3. Mexico

7. Europe Light Beer Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Litres) (2025-2032)

7.1. Europe Light Beer Market Size and Forecast, by Production (2025-2032)

7.2. Europe Light Beer Market Size and Forecast, by Package (2025-2032)

7.3. Europe Light Beer Market Size and Forecast, by Distribution Channel (2025-2032)

7.4. Europe Light Beer Market Size and Forecast, by Country (2025-2032)

7.4.1. United Kingdom

7.4.2. France

7.4.3. Germany

7.4.4. Italy

7.4.5. Spain

7.4.6. Sweden

7.4.7. Austria

7.4.8. Rest of Europe

8. Asia Pacific Light Beer Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Litres) (2025-2032)

8.1. Asia Pacific Light Beer Market Size and Forecast, by Production (2025-2032)

8.2. Asia Pacific Light Beer Market Size and Forecast, by Package (2025-2032)

8.3. Asia Pacific Light Beer Market Size and Forecast, by Distribution Channel (2025-2032)

8.4. Asia Pacific Light Beer Market Size and Forecast, by Country (2025-2032)

8.4.1. China

8.4.2. S Korea

8.4.3. Japan

8.4.4. India

8.4.5. Australia

8.4.6. Indonesia

8.4.7. Malaysia

8.4.8. Vietnam

8.4.9. Taiwan

8.4.10. Rest of Asia Pacific

9. Middle East and Africa Light Beer Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Litres) (2025-2032)

9.1. Middle East and Africa Light Beer Market Size and Forecast, by Production (2025-2032)

9.2. Middle East and Africa Light Beer Market Size and Forecast, by Package (2025-2032)

9.3. Middle East and Africa Light Beer Market Size and Forecast, by Distribution Channel (2025-2032)

9.4. Middle East and Africa Light Beer Market Size and Forecast, by Country (2025-2032)

9.4.1. South Africa

9.4.2. GCC

9.4.3. Nigeria

9.4.4. Rest of ME&A

10. South America Light Beer Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Litres) (2025-2032)

10.1. South America Light Beer Market Size and Forecast, by Production (2025-2032)

10.2. South America Light Beer Market Size and Forecast, by Package (2025-2032)

10.3. South America Light Beer Market Size and Forecast, by Distribution Channel (2025-2032)

10.4. South America Light Beer Market Size and Forecast, by Country (2025-2032)

10.4.1. Brazil

10.4.2. Argentina

10.4.3. Rest Of South America

11. Company Profile: Key Players

11.1. Anheuser-Busch InBev (Belgium)

11.1.1. Company Overview

11.1.2. Product Portfolio

11.1.2.1. Product Name

11.1.2.2. Product Details (Price, Features, etc.)

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Molson Coors Beverage Company (United States)

11.3. Heineken N.V. (Netherlands)

11.4. Constellation Brands, Inc. (United States)

11.5. Carlsberg Group (Denmark)

11.6. Diageo plc (United Kingdom)

11.7. Asahi Group Holdings, Ltd. (Japan)

11.8. Kirin Holdings Company, Limited (Japan)

11.9. Grupo Modelo (Mexico)

11.10. Boston Beer Company (United States)

11.11. Tsingtao Brewery Co., Ltd. (China)

11.12. Pabst Brewing Company (United States)

11.13. New Belgium Brewing Company (United States)

11.14. The Gambrinus Company (United States)

11.15. Stone Brewing (United States)

11.16. Brooklyn Brewery (United States)

11.17. Deschutes Brewery (United States)

11.18. Sierra Nevada Brewing Co. (United States)

11.19. Ballast Point Brewing Company (United States)

12. Key Findings

13. Analyst Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook