Spirits Market Industry Analysis and Forecast 2026 to 2034.

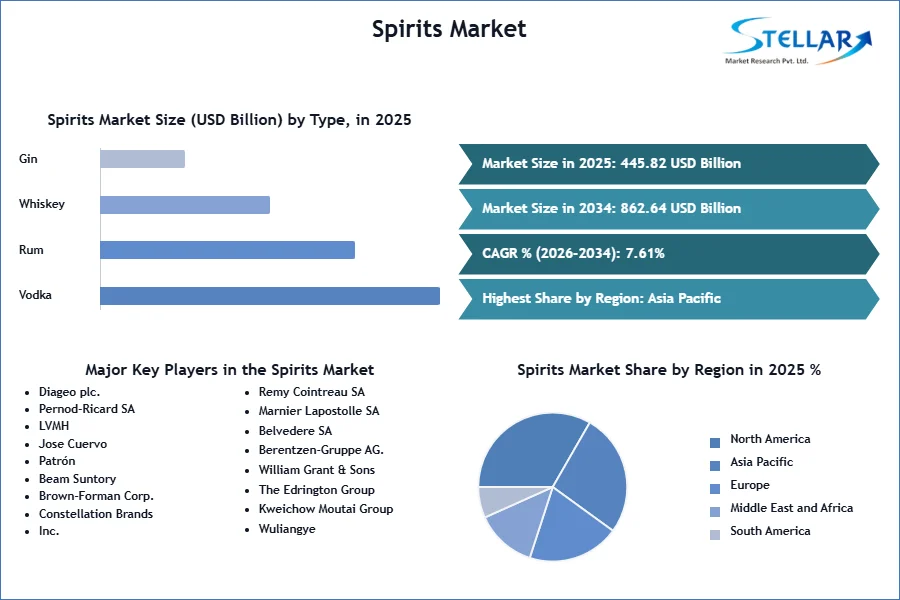

The Spirits Market size was valued at USD 445.82 Bn. in 2025 and the total Global Spirits revenue is expected to grow at a CAGR of 7.61% from 2026 to 2034., reaching nearly USD 862.64 Bn. by 2034.

Spirits Market Overview

Spirits are typically volatile liquids with specific chemical properties, often utilized in various laboratory and industrial applications. The spirits market report presents key findings, unveiling notable trends and insights. Premiumization emerges as a driving force, with consumers increasingly opting for high-quality, premium-priced spirits, driving growth for upscale brands and craft distilleries. Emerging markets, characterized by expanding populations and rising incomes, offer a fertile ground for spirits consumption, creating a substantial consumer base. Evolving preferences towards flavored spirits, ready-to-drink cocktails, and low/no-alcohol alternatives provide diverse tastes and health-conscious trends, influencing market dynamics.

The Asia Pacific region, led by powerhouse economies like China and India, showcases significant growth potential, with Southeast Asia and South America emerging as key markets. Investment opportunities abound in premium and craft distilleries, tapping into the premiumization trend. Online marketplaces facilitating spirits sales and delivery are poised to benefit from the growing e-commerce wave. RTD cocktail brands offering innovative and convenient options are positioned for growth, alongside functional beverage companies developing health-oriented alternatives. Growth into emerging markets presents significant potential for companies with robust regional strategies and brand recognition, offering opportunities for capitalizing on shifting consumer trends and driving overall growth in the spirits market.

To get more Insights: Request Free Sample Report

Spirits Market Dynamics

The Influence of Premiumization on Spirits Consumption

Consumers are increasingly willing to pay a premium for high-quality spirits, driving the trend of premiumization. The trend is driven by a growing appreciation for craft and artisanal products, as well as a desire for unique and exotic flavor experiences. Distillers are responding by introducing premium and super-premium offerings, including aged spirits, limited editions, and luxury brands. SMR research indicates that over 45% of consumers purchased premium and luxury spirits occasionally from 2026 to 2034. showcasing a trend of trading up for premium brands. The surge in demand has driven the growth of craft distilleries, which offer unique flavors and appeal to enthusiasts.

Distilleries are also innovating with limited-edition releases, cask-finished expressions, and aged spirits to meet the demands of the premium market. Premiumization has exceeded being a simple trend and has become deeply ingrained in the Indian consumer psyche, representing a lifestyle choice centered on embracing high-quality products and services across various categories. The shift in consumer preferences is reflected in the steady rise in sales of spirits retailing above ?2,000 per bottle.

Despite a challenging economic environment, consumers are increasingly inclined towards premium beverage products, driven by a desire for differentiation and quality. Notably, the high-income demographic, which often consumes premium beverages, has shown resilience to inflation and economic downturns. According to SMR analysis, in 2025, 33% of Americans spent $50 or more on a bottle of alcohol, a notable increase from 24% in 2025. The trend of premiumization has been particularly pronounced in the Spirits segment, where celebrity endorsements and strong brand reputations have cultivated significant customer loyalty.

The spirits sales reached a record $37.6 billion in 2025, representing a 5.1% year-over-year growth. Significantly, more than 60% of this revenue came from sales of high-end and super-premium spirits. The increasing willingness of consumers to spend on premium beverages underscores the importance of quality and differentiation in product offerings. The robust growth in spirits sales, particularly in the high-end and super-premium segments, highlights the strength of customer loyalty and the potential for premiumization to drive revenue growth.

Competition from Alternative Beverages

The spirits market faces increasing competition from alternative beverage categories such as non-alcoholic spirits, ready-to-drink (RTD) cocktails, and low-alcohol or alcohol-free options. These alternatives provide to the health-conscious consumers seeking non-alcoholic and lower-calorie options, posing a threat to traditional spirits sales. The impact of competition from alternative beverages on the spirits market is multifaceted. It challenges traditional spirits producers to innovate and diversify their product offerings to provide evolving consumer preferences. Additionally, it leads to changes in marketing strategies, pricing models, and distribution channels to remain competitive in a rapidly changing market landscape. Understanding and addressing this challenge is crucial for spirits manufacturers to maintain market relevance and sustain growth among increasing competition from alternative beverage categories.

Spirits Market Segment Analysis

By Product Type, The Vodka segment held the largest market share in the Global Spirits Market in 2025. According to SMR analysis, the segment is further expected to grow at a CAGR of XX% during the forecast period. Vodka is a versatile and widely consumed spirit known for its neutrality in flavor, making it a popular choice for cocktails and mixed drinks. It holds a significant share of the spirits market, driven by its versatility and appeal to a broad consumer base. Vodka's popularity extends across various demographics and occasions, contributing to its consistent market presence. Smirnoff, the world's leading vodka brand, achieved remarkable sales of 28.1 million 9L cases in 2025.

While originating in Moscow, Smirnoff is currently produced in various countries, including the U.S., Canada, and Italy. Diageo plc (NYSE: DEO) boasts ownership of other renowned vodka brands like Cîroc and Ketel One. In the fiscal year ending 30th June 2023, Diageo reported a significant 10.7% increase in net sales, reaching $21.93 billion, driven by the success of its premium-plus brands. The data underscores Diageo's dominance in the spirits market and its ability to drive growth through its portfolio of popular vodka brands. Vodka's substantial market share reflects its widespread consumer acceptance and versatility in both traditional and emerging markets. Its popularity drives competition among vodka producers, leading to innovation in flavors, packaging, and marketing strategies to differentiate brands and capture market share.

Spirits Market Regional Insights

In the Asia Pacific region, the spirits market is showing significant growth with a projected CAGR of around XX% during the forecast period. Premiumization is a key trend, mirroring global patterns, as consumers favor high-quality domestic and imported spirits. Evolving preferences include a surge in demand for flavored spirits, craft offerings, and ethnic varieties. Rising disposable incomes, strengthened by improving economies, drive increased spending on alcoholic beverages. Additionally, the growing culture of social gatherings, particularly in Southeast Asian countries, further contributes to market growth. In the Asia Pacific region, the cost of service varies by country but generally remains lower than in North America and Europe. Raw material costs are influenced by the type of spirit and are expected to be impacted by import duties in certain countries.

Government regulations primarily focus on maintaining production standards and struggle with simulating to uphold quality and consumer safety. Additionally, some countries impose specific taxes and regulations on alcohol sales to further regulate the industry. China holds a dominant position in the Asia-Pacific spirits market. Emerging markets with substantial growth prospects include India, Japan, and Southeast Asian countries such as Thailand, Malaysia, and Singapore. These regions present lucrative opportunities for market growth and investment, driven by evolving consumer preferences, rising disposable incomes, and a growing culture of social gatherings.

Spirits Market Competitive Landscape

Diageo plc (UK) leads globally with iconic brands like Johnnie Walker, Smirnoff, and Baileys, prioritizing premiumization and growing into emerging markets. Pernod Ricard (France) boasts a formidable portfolio including Absolut Vodka, Chivas Regal Scotch, and Havana Club rum, actively pursuing acquisitions and partnerships for market dominance. Beam Suntory Inc. (US & Japan), formed from a merger, owns Jim Beam bourbon, Maker's Mark whiskey, and Sauza tequila, leveraging combined strengths for effective competition. William Grant & Sons Ltd. (UK) specializes in premium spirits like Glenfiddich Scotch and Hendrick's gin, focusing on innovation and family heritage.

Encouraging premiumization, limited editions, and super-premium offerings meet the rising demand for top-tier spirits. RTD cocktails and flavored spirits fulfill consumer preferences for convenience and diverse flavors. Increasing market reach, new launches target fresh customer segments and potentially penetrate new geographic markets. Strengthening brand image, innovative marketing, and product differentiation strategies enhance brand perception amid competitive landscapes.

- In March 2023, Pernod Ricard unveiled its intention to acquire a controlling interest in Skrewball, a rapidly expanding super-premium flavored whiskey brand. Screwball is renowned as the pioneer of peanut butter-flavored whiskey, delivering a smooth, nutty taste sensation. This strategic partnership aligns with Pernod Ricard's enduring commitment to consumer-centric strategies and premiumization initiatives while enriching its diverse portfolio of renowned wine and spirits brands with a complementary addition.

- In March 2023, Bacardi unveiled Bacardi Caribbean Spiced Rum, a meticulously crafted spiced-aged offering. This refined concoction blends aged rum with an infusion of spices, pineapple, coconut water, and coconut blossoms, resulting in a uniquely flavorful and indulgent libation.

- In June 2022, Brown-Forman Corporation and The Coca-Cola Company forged a global partnership, unveiling their upcoming launch of a ready-to-drink mixed cocktail featuring Jack Daniels and Coke. Anticipated to debut in Mexico by late 2022.

|

Spirits Market Scope |

|

|

Market Size in 2025 |

USD 445.82 Bn. |

|

Market Size in 2034 |

USD 862.64 Bn. |

|

CAGR (2026-2034) |

7.61% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Segments |

By Product Type Vodka Rum Whiskey Gin Tequila Other Spirits |

|

By Application Household Commercial |

|

|

By Distribution Channel Direct Sales Channels Indirect Sales Channels |

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Player in the Spirits Market

- Diageo plc.

- Pernod-Ricard SA

- LVMH

- Jose Cuervo

- Patrón

- Beam Suntory

- Brown-Forman Corp.

- Constellation Brands, Inc.

- Remy Cointreau SA

- Marnier Lapostolle SA

- Belvedere SA

- Berentzen-Gruppe AG.

- William Grant & Sons

- The Edrington Group

- Kweichow Moutai Group

- Wuliangye

- Yanghe Brewery

- Daohuaxiang

- Luzhou Laojiao

- The Miller Brewing Company (U.S.)

- XXX

Frequently Asked Questions

Investment opportunities include investing in premium and craft distilleries, online marketplaces facilitating spirits sales, RTD cocktail brands, functional beverage companies, and expansion into emerging markets.

Challenges include regulatory hurdles, supply chain disruptions, changing consumer preferences, and competition from alternative beverages.

The Market size was valued at USD 445.82 Billion in 2025 and the total Market revenue is expected to grow at a CAGR of 7.61% from 2026 to 2034, reaching nearly USD 862.64 billion.

The segments covered in the market report are by Type, Application, and End User.

1. Spirits Market: Research Methodology

1.1. Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Assumptions

2. Spirits Market: Executive Summary

2.1. Market Overview

2.2. Market Size (2024) and Forecast (2025 – 2032) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Spirits Market: Competitive Landscape

3.1. Stellar Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Product Segment

3.2.4. Total Production (2024)

3.2.5. End-user Segment

3.2.6. Y-O-Y%

3.2.7. Revenue (2023)

3.2.8. Profit Margin

3.2.9. Market Share

3.2.10. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. Product Launches and Innovation

4. Spirits Market: Dynamics

4.1. Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Market Drivers

4.3. Market Restraints

4.4. Market Opportunities

4.5. Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factors

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Value Chain Analysis

4.10. Trade Analysis

4.10.1. Import Scenario

4.10.2. Export Scenario

4.11. Regulatory Landscape

4.11.1. Market Regulation by Region

4.11.1.1. North America

4.11.1.2. Europe

4.11.1.3. Asia Pacific

4.11.1.4. Middle East and Africa

4.11.1.5. South America

4.11.2. Impact of Regulations on Market Dynamics

4.11.3. Government Schemes and Initiatives

5. Spirits Market Size and Forecast by Segments (by Value USD Million and Volume in Litre)

5.1. Spirits Market Size and Forecast, By Product Type (2024-2032)

5.1.1. Vodka

5.1.2. Rum

5.1.3. Whiskey

5.1.4. Gin

5.1.5. Tequila

5.1.6. Other Spirits

5.2. Spirits Market Size and Forecast, By Application (2024-2032)

5.2.1. Household

5.2.2. Commercial

5.3. Spirits Market Size and Forecast, By Distribution Channel (2024-2032)

5.3.1. Direct Sales Channel

5.3.2. Indirect Sales Channel

5.4. Spirits Market Size and Forecast, by Region (2024-2032)

5.4.1. North America

5.4.2. Europe

5.4.3. Asia Pacific

5.4.4. Middle East and Africa

5.4.5. South America

6. North America Spirits Market Size and Forecast (by Value USD Million and Volume in Litre)

6.1. North America Spirits Market Size and Forecast, By Product Type (2024-2032)

6.1.1. Vodka

6.1.2. Rum

6.1.3. Whiskey

6.1.4. Gin

6.1.5. Tequila

6.1.6. Other Spirits

6.2. North America Spirits Market Size and Forecast, By Application (2024-2032)

6.2.1. Household

6.2.2. Commercial

6.3. North America Spirits Market Size and Forecast, By Distribution Channel (2024-2032)

6.3.1. Direct Sales Channel

6.3.2. Indirect Sales Channel

6.4. North America Spirits Market Size and Forecast, by Country (2024-2032)

6.4.1. United States

6.4.2. Canada

6.4.3. Mexico

7. Europe Spirits Market Size and Forecast (by Value USD Million and Volume in Litre)

7.1. Europe Spirits Market Size and Forecast, By Product Type (2024-2032)

7.2. Europe Spirits Market Size and Forecast, By Application (2024-2032)

7.3. Europe Spirits Market Size and Forecast, By Distribution Channel (2024-2032)

7.4. Europe Spirits Market Size and Forecast, by Country (2024-2032)

7.4.1. UK

7.4.2. France

7.4.3. Germany

7.4.4. Italy

7.4.5. Spain

7.4.6. Sweden

7.4.7. Austria

7.4.8. Rest of Europe

8. Asia Pacific Spirits Market Size and Forecast (by Value USD Million and Volume in Litre)

8.1. Asia Pacific Spirits Market Size and Forecast, By Product Type (2024-2032)

8.2. Asia Pacific Spirits Market Size and Forecast, By Application (2024-2032)

8.3. Asia Pacific Spirits Market Size and Forecast, By Distribution Channel (2024-2032)

8.4. Asia Pacific Spirits Market Size and Forecast, by Country (2024-2032)

8.4.1. China

8.4.2. S Korea

8.4.3. Japan

8.4.4. India

8.4.5. Australia

8.4.6. Indonesia

8.4.7. Malaysia

8.4.8. Vietnam

8.4.9. Taiwan

8.4.10. Bangladesh

8.4.11. Pakistan

8.4.12. Rest of Asia Pacific

9. Middle East and Africa Spirits Market Size and Forecast (by Value USD Million and Volume in Litre)

9.1. Middle East and Africa Spirits Market Size and Forecast, By Product Type (2024-2032)

9.2. Middle East and Africa Spirits Market Size and Forecast, By Application (2024-2032)

9.3. Middle East and Africa Spirits Market Size and Forecast, By Distribution Channel (2024-2032)

9.4. Middle East and Africa Spirits Market Size and Forecast, by Country (2024-2032)

9.4.1. South Africa

9.4.2. GCC

9.4.3. Egypt

9.4.4. Nigeria

9.4.5. Rest of ME&A

10. South America Spirits Market Size and Forecast (by Value USD Million and Volume in Litre)

10.1. South America Spirits Market Size and Forecast, By Product Type (2024-2032)

10.2. South America Spirits Market Size and Forecast, By Application (2024-2032)

10.3. South America Spirits Market Size and Forecast, By Distribution Channel (2024-2032)

10.4. South America Spirits Market Size and Forecast, by Country (2024-2032)

10.4.1. Brazil

10.4.2. Argentina

10.4.3. Rest of South America

11. Company Profile: Key players

11.1. Diageo plc.

11.1.1. Company Overview

11.1.2. Product Portfolio

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Pernod-Ricard SA

11.3. LVMH

11.4. Jose Cuervo

11.5. Patrón

11.6. Beam Suntory

11.7. Brown-Forman Corp.

11.8. Constellation Brands, Inc.

11.9. Remy Cointreau SA

11.10. Marnier Lapostolle SA

11.11. Belvedere SA

11.12. Berentzen-Gruppe AG.

11.13. William Grant & Sons

11.14. The Edrington Group

11.15. Kweichow Moutai Group

11.16. Wuliangye

11.17. Yanghe Brewery

11.18. Daohuaxiang

11.19. Luzhou Laojiao

11.20. The Miller Brewing Company (U.S.)

11.21. XXX

12. Key Findings

13. Industry Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook