Cocoa and Chocolate Market: Global Industry Analysis and Forecast 2026-2034

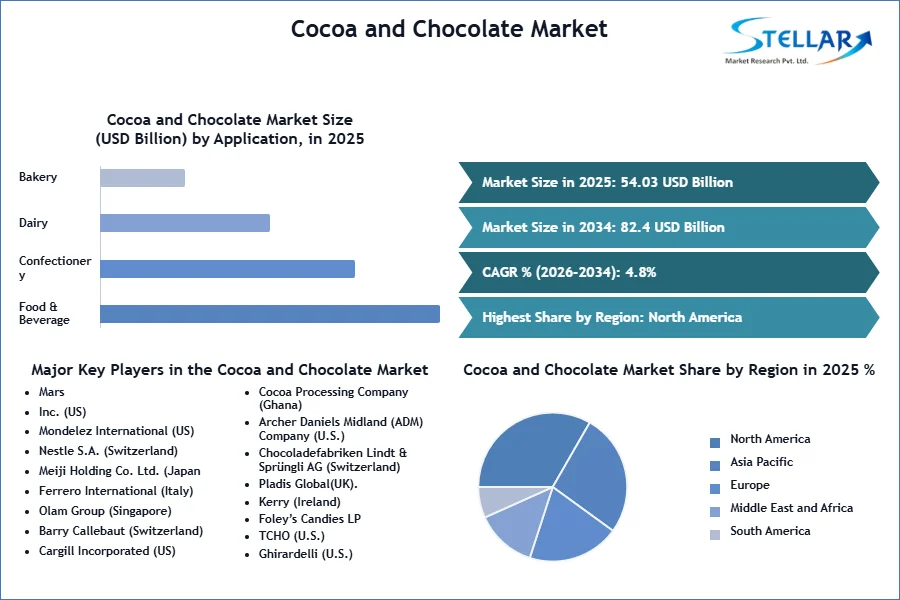

The Cocoa and Chocolate Market size was valued at USD 54.03 Billion in 2025 and the total Global Cocoa and Chocolate revenue is expected to grow at a CAGR of 4.8% from 2026 to 2034, reaching nearly USD 82.4 Billion by 2034.

Cocoa and Chocolate Market Overview

Cocoa is a dried and fully fermented fatty seed of the fruit of the cocoa tree. Cocoa Powder is made by removing some of the cocoa butter from the liquor. Chocolate is a solid food made by combining cocoa liquor with Cocoa butter and sugar. The proportion of the cocoa liquor is utilized for how dark the chocolate is.

The report from Stellar Market Research presents a thorough analysis of the Cocoa and Chocolate market, focusing on forecasting market growth trends and offering valuable insights into the supply chain dynamics. The Cocoa & Chocolate Market report has provided an overview of the market value structure, cost factor, and various driving factors and analyzes the industry atmosphere, then studies the global outline of industry size, demand, application, revenue, product, region, and segments. The report covers details of new recent developments, trade regulations, import-export analysis, production analysis, market share, the impact of domestic and localized market players, analyses of opportunities in terms of emerging revenue and changes in market regulations, strategic market growth analysis, market size, category market growths, product approvals, product launches, geographic developments, technological innovations in the market.

The increasing global population and higher disposable incomes in emerging markets are expected to boost the demand for luxury items such as premium chocolate.

According to SMR, Chocolates Exporters & Suppliers manual, there are 138 active Chocolates Exporters in the United States exporting to 59 Buyers.

According to SMR, Cocoa and chocolate contain significant amounts of magnesium, copper, potassium, and iron (14). Magnesium, copper, and potassium have a protective effect on the heart (15–17), while iron, found mainly in dark chocolate, helps prevent anemia in middle-aged men by contributing to 25% of the U.S. recommended dietary allowance.

According to SMR, In January 2025, the average cocoa contract prices in New York raise to USD per Tonne, marking a 6% decline compared to the previous crop year's average of USD 2675 per tonne.

Europe has been a significant market in the Cocoa and Chocolate markets. Europe Known for its rich chocolate culture and premium brands. Countries like Switzerland and Belgium excel in quality and craftsmanship. The popularity of dark chocolate is influenced by health and wellness trends, as consumer preferences are shaped by sustainability initiatives. The European cocoa market is highly diverse, as European buyers source cocoa beans of various qualities and origins to meet the demand of the cocoa and chocolate industries.

To get more Insights: Request Free Sample Report

Cocoa and Chocolate Market Dynamics

Growing Consumer Demands for chocolate Products

Chocolate manufacturers are continuously working to fulfill the constantly changing demands of customers through the introduction of innovative and tempting products. It includes creating innovative flavors, textures, and formats, as well as incorporating efficient ingredients such as nuts, fruits, and spices. Also, there is a growing trend towards smaller portion sizes and individually wrapped chocolates, which cater to on-the-go consumption and promote portion control.

A major cause for the growing demand for chocolates is the rising disposable income of customers in Asia Pacific's developing countries. The availability of local chocolate brands has led to an increase in chocolate sales in South Korea, Japan, India, and China because people's taste preferences are changing and they are becoming more loyal to local brands. However, international brands such as Ghirardelli, Mars, Ferrero, and Hershey's have also seen growth in these countries. Chocolate is a popular gift, especially during holidays like Easter, and Christmas. Seasonal demand drives up overall consumption and is expected to drive a cocoa and chocolate market.

A growing interest in research on the various health benefits of cocoa, especially dark chocolate. It has the potential to improve heart health and include antioxidants, and mood-boosting properties, contributing to its growing popularity. Demand for chocolates with a higher cocoa content has been driven growth of the Cocoa and chocolate Market.An increasing prevalence of lactose intolerance among the population has encouraged consumers to shift to non-animal-based food ingredients such as cocoa products.

For instance, In October 2025, Barry Callebaut announced a novel method of farming, fermentation, & cocoa bean roasting to form 2nd generation chocolate. The formulation of the Cocoa Cultivation & Craft (CCC) principle to redesign chocolate development with 60-80% higher cocoa content and 50% less sugar than a standard consumed chocolate.

High Production Costs & Supply Chain Disruptions

The Cocoa and Chocolate Market is expected to continue growing, but some factors restrain its market growth. Cocoa production is susceptible to climate change, diseases, and pests, which can affect crop yields. Also, Companies in the supply chain face ethical challenges such as child labor and poor working conditions in cocoa-producing regions. The cost of producing chocolate is directly impacted by changes in cocoa bean prices, which is one of the key variables Businesses struggle to maintain low prices for customers. Worries about the sustainability and moral source of cocoa beans are hamper the supply of high-quality ingredients. Despite these difficulties, the cocoa and chocolate industry continues to grow and prosper, providing various delicious options to satisfy our demands for sweets. Rising costs are passed on to consumers in the form of higher chocolate prices, which lead to decreased demand.

According to SMR, 36% of Europeans prefer chocolates with health benefits, while 38% require chocolates with reduced sugar content.

Food and beverage manufacturers have faced difficulties in sourcing raw materials due to supply chain disruptions such as trade wars, tariffs, and evolving regulations, leading to increased production costs and affecting profitability. Adverse weather conditions and logistical disruptions have caused a shortage of cocoa beans, resulting in price increases that impact both chocolate producers and consumers. Cocoa farming has significant environmental impacts, including deforestation, soil degradation, and biodiversity loss.

Changing Consumer Preference towards Healthy Chocolates

A new trend within the Cocoa & Chocolate market is the growing preference for sustainable and eco-friendly products. Another significant trend in the Cocoa & Chocolate market is the rising incorporation of technology to enhance product quality and efficiency. There is a growing demand for healthy chocolate options, with an inclination towards dark chocolate, a rich source of polyphenols. Companies such as Hero Nutritional and Barry Callebaut are introducing chocolate products with added health benefits, driven by the changing preferences of consumers. As chocolates are perishable products, any decrease in demand for a particular product results in large inventories with limited time for disposal. Therefore, companies need to align their new product releases with the evolving tastes and preferences of consumers. Small craft chocolate makers are leveraging their tree-to-bar model to insulate themselves from global commodity price fluctuations and highlight organic farming and fair trade practices to meet evolving consumer demands.

Cocoa and Chocolate Market Segment Analysis

Based on the Type, the Cocoa Butter Type segment held the largest market share of about 49.5% in the Cocoa and Chocolate Market in 2025. According to the SMR analysis, the segment is expected to grow during the forecast period and maintain its dominance till 2032. Cocoa butter is a versatile ingredient used in various applications within the chocolate and confectionery industry. Cocoa butter is a key component in high-quality chocolate production. It contributes to the flavor profile, texture, and overall sensory experience of chocolate products. Chocolate makers often choose cocoa butter for its excellent melting properties and ability to work well with other ingredients, ensuring accurate tempering and molding for consistent quality and creating smooth appearance. Cocoa Butter Type segment has extensive application in the cosmetics industry. The all-natural trend in the skin care products market is set to boost the demand for cocoa butter. The increasing demand for chocolate among consumers triggers the demand for cocoa butter as it provides the chocolate with its melt-in-the-mouth texture.

The increasing demand for high-quality chocolate is driving up the demand for authentic cocoa butter, which is expected to continue rising in the future.

According to SMR, the global largest supplier of Cocoa is Africa, which accounts for 73% of the global production of Cocoa. Ivory Coast and Ghana are the major countries producing Cocoa.

Cocoa and Chocolate Market Regional Analysis

North America has dominated the Cocoa and Chocolate Market, which held the largest market share accounting for 45.6% in 2025, the region is expected to grow during the forecast period and maintain its dominance by 2034. North America consistently ranks as one of the top-selling regions in the global cocoa and chocolate market, driven by its large and affluent consumer base, strong retail distribution networks, and a culture deeply rooted in chocolate consumption. North America has dominated because of the increasing demand for chocolate-based confectioneries and the rising adoption of chocolate ingredients to infuse food products such as indulgent snacks, chocolate-flavored ice creams, and cocoa bars, among others. Also, increasing awareness of the health benefits of cocoa and chocolate consumption is expected to drive the uptake of cocoa products and thus drive the Cocoa and chocolate market's growth.

The rising demand for chocolate in North America enhances the growth of cocoa simultaneously as it is the key raw material used in the production of chocolate. The U.S. accounted for the highest chocolate consumption and production in the North American region. In Canada, chocolate is becoming more expensive given to the rising cost of raw materials.

Asia Pacific represents a mature market for the Cocoa and Chocolate industry, holding a market share of XX% and experiencing significant growth during its forecast period. In Asia Pacific, the rising growth of population, urbanization, and shifting demographics have the potential to impact the consumption trends of chocolate. The rise of emerging markets, particularly in countries like China and India, where the middle-class population is expanding, offers substantial prospects for market development. Investment in cocoa research and cultivation in the Asia Pacific region coupled with new product launches such as the development of organic and natural cocoa products to support the Cocoa and Chocolate market growth.

Cocoa and Chocolate Market Competitive Landscape

Prominent market players are making collaborative efforts by partnering with other companies to stay ahead of the competition. Many companies are also investing in new product launches to develop their product portfolio. Mergers and acquisitions are also among the key strategies used by players to expand their product portfolios. Some major global key players in Cocoa and Chocolate Market include Barry Callebaut, Cargill, Olam, ECOM Cocoa and Chocolate Market Agro-industrial Corporation, Cocoa Processing, Touton, Niche Cocoa, BD Associates Ghana, PLOT Enterprise Ghana, Nestlé, Mondelez International, and Meiji Holdings, etc. These companies play a crucial role in shaping the cocoa and chocolate market through innovation, global reach, and brand recognition.

- In March 2022 - Barry Callebaut announced the development of its factory in Campbell field, Melbourne, Australia. The new factory expands the company's geographical footprint in Asia Pacific by creating safe, high-quality products. The facility can serve the whole food sector in Australia, from global and local food manufacturers to artisanal and professional chocolate users.

- Barry Callebaut promotes the sale of sustainable HORIZONTES cocoa and chocolate products, improving the incomes of cocoa producers and communities.

- In November 2022, As per a Business Standard article, Ghana and Ivory Coast, the top cocoa producers globally, hiked cocoa prices for chocolate makers. Smaller manufacturers may respond to this by lowering their prices, that is going to drop Ghana's and Ivory Coast's market shares.

- In November 2022, the Niche Cocoa Industry announced an expansion of its manufacturing facility in the U.S. located in Franklin, Wisconsin. The development will also improve the company's direct presence in the U.S. by strengthening its global market presence.

- In May 2022, Blommer Chocolate partnered with DouxMatok (Israel/USA), a food tech company to launch chocolate and confectionery products.

- In March 2022, Hershey Company launched a crunch cookie chocolate spread in India for the consumer's breakfast

- In March 2021, Barry Callebaut opened its third factory in India. The new chocolate factory consists of an R&D lab and assembly lines capable of manufacturing various needs of customers - international food manufacturers, local confectioneries, and semi-industrial bakers and patisseries.

- In March 2021, Cargill partnered with Nestlé to extend the Nestlé Cocoa Plan (NCP) to benefit its network of cocoa farmers in Sulawesi, Indonesia. Activities include three key NCP pillars: better farming, better lives, and better cocoa.

|

Cocoa and Chocolate Market Scope |

|

|

Market Size in 2025 |

USD 54.03 Bn. |

|

Market Size in 2034 |

USD 82.4 Bn. |

|

CAGR (2026-2034) |

4.8 % |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Segments |

By Type Cocca Ingredients

Chocolate

|

|

By Application

|

|

|

By Nature

|

|

|

By Distribution Channel

|

|

|

Regional Scope |

North America(United States), Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Player in the Cocoa and Chocolate Market

- Mars, Inc. (US)

- Mondelez International (US)

- Nestle S.A. (Switzerland)

- Meiji Holding Co. Ltd. (Japan

- Ferrero International (Italy)

- Olam Group (Singapore)

- Barry Callebaut (Switzerland)

- Cargill Incorporated (US)

- Cocoa Processing Company (Ghana)

- Archer Daniels Midland (ADM) Company (U.S.)

- Chocoladefabriken Lindt & Sprüngli AG (Switzerland)

- Pladis Global(UK).

- Kerry (Ireland)

- Foley’s Candies LP

- TCHO (U.S.)

- Ghirardelli (U.S.)

- Alpezzi Chocolate (Mexico)

- Valrhona (France)

- Guittard (U.S.)

- Irca (Belgium)

- Hershey (U.S.)

Frequently Asked Questions

North America is expected to hold the highest share of the Cocoa and Chocolate Market.

The Cocoa and Chocolate Market size was valued at USD 54.03 billion in 2025 reaching nearly USD 82.4 billion in 2034.

The rising demand from the dietary supplements chocolates industry improved knowledge of healthcare well-being growing preference for clean label products are the opportunities in the global Cocco and Chocolates Market.

The segments covered in the Cocoa and Chocolate Market report are based on Type, Application, Nature, and Distribution Channel.

1. Cocoa and Chocolate Market: Research Methodology

1.1. Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Assumptions

2. Cocoa and Chocolate Market: Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026 – 2034) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Cocoa and Chocolate Market: Competitive Landscape

3.1. Stellar Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Product Segment

3.2.4. Total Production (2025)

3.2.5. End-user Segment

3.2.6. Y-O-Y%

3.2.7. Revenue (2025)

3.2.8. Profit Margin

3.2.9. Market Share

3.2.10. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. Product Launches and Innovation

4. Cocoa and Chocolate Market: Dynamics

4.1. Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Market Drivers

4.3. Market Restraints

4.4. Market Opportunities

4.5. Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factors

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Value Chain Analysis and Supply Chain Analysis

4.10. Trade Analysis

4.11. Regulatory Landscape

4.11.1. Market Regulation by Region

4.11.1.1. North America

4.11.1.2. Europe

4.11.1.3. Asia Pacific

4.11.1.4. Middle East and Africa

4.11.1.5. South America

4.11.2. Impact of Regulations on Market Dynamics

4.11.3. Government Schemes and Initiatives

5. Cocoa and Chocolate Market Size and Forecast by Segments (by Value USD Billion and Volume in Tonnes)

5.1. Cocoa and Chocolate Market Size and Forecast, By Type (2026-2034)

5.1.1. Cocoa Ingredients

5.1.1.1. Cocoa Butter

5.1.1.2. Cocoa Liquor

5.1.1.3. Cocoa Powder

5.1.2. Chocolate

5.1.2.1. Dark

5.1.2.2. Milk

5.1.2.3. White

5.1.2.4. Filled

5.2. Cocoa and Chocolate Market Size and Forecast, By Application (2026-2034)

5.2.1. Food & Beverage

5.2.2. Confectionery

5.2.3. Dairy

5.2.4. Bakery

5.2.5. Cosmetics

5.2.6. Pharmaceuticals

5.2.7. Others

5.3. Cocoa and Chocolate Market Size and Forecast, By Nature (2026-2034)

5.3.1. Organic

5.3.2. Conventional

5.4. Cocoa and Chocolate Market Size and Forecast, By Distribution Channel (2026-2034)

5.4.1. Online

5.4.2. Offline

5.5. Cocoa and Chocolate Market Size and Forecast, by Region (2026-2034)

5.5.1. North America

5.5.2. Europe

5.5.3. Asia Pacific

5.5.4. Middle East and Africa

5.5.5. South America

6. North America Cocoa and Chocolate Market Size and Forecast (by Value USD Billion and Volume in Tonnes)

6.1. North America Cocoa and Chocolate Market Size and Forecast, By Type (2026-2034)

6.1.1. Cocoa Ingredients

6.1.1.1. Cocoa Butter

6.1.1.2. Cocoa Liquor

6.1.1.3. Cocoa Powder

6.1.2. Chocolate

6.1.2.1. Dark

6.1.2.2. Milk

6.1.2.3. White

6.1.2.4. Filled

6.2. North America Cocoa and Chocolate Market Size and Forecast, By Application (2026-2034)

6.2.1. Food & Beverage

6.2.2. Confectionery

6.2.3. Dairy

6.2.4. Bakery

6.2.5. Cosmetics

6.2.6. Pharmaceuticals

6.2.7. Others

6.3. North America Cocoa and Chocolate Market Size and Forecast, By Nature (2026-2034)

6.3.1. Organic

6.3.2. Conventional

6.4. North America Cocoa and Chocolate Market Size and Forecast, By Distribution Channel (2026-2034)

6.4.1. Online

6.4.2. Offline

6.5. North America Cocoa and Chocolate Market Size and Forecast, by Country (2026-2034)

6.5.1. United States

6.5.2. Canada

6.5.3. Mexico

7. Europe Cocoa and Chocolate Market Size and Forecast (by Value USD Billion and Volume in Tonnes)

7.1. Europe Cocoa and Chocolate Market Size and Forecast, By Type (2026-2034)

7.2. Europe Cocoa and Chocolate Market Size and Forecast, By Application (2026-2034)

7.3. Europe Cocoa and Chocolate Market Size and Forecast, By Nature (2026-2034)

7.4. Europe Cocoa and Chocolate Market Size and Forecast, By Distribution Channel (2026-2034)

7.5. Europe Cocoa and Chocolate Market Size and Forecast, by Country (2026-2034)

7.5.1. UK

7.5.2. France

7.5.3. Germany

7.5.4. Italy

7.5.5. Spain

7.5.6. Sweden

7.5.7. Austria

7.5.8. Rest of Europe

8. Asia Pacific Cocoa and Chocolate Market Size and Forecast (by Value USD Billion and Volume in Tonnes)

8.1. Asia Pacific Cocoa and Chocolate Market Size and Forecast, By Type (2026-2034)

8.2. Asia Pacific Cocoa and Chocolate Market Size and Forecast, By Application (2026-2034)

8.3. Asia Pacific Cocoa and Chocolate Market Size and Forecast, By Nature (2026-2034)

8.4. Asia Pacific Cocoa and Chocolate Market Size and Forecast, By Distribution Channel (2026-2034)

8.5. Asia Pacific Cocoa and Chocolate Market Size and Forecast, by Country (2026-2034)

8.5.1. China

8.5.2. S Korea

8.5.3. Japan

8.5.4. India

8.5.5. Australia

8.5.6. Indonesia

8.5.7. Malaysia

8.5.8. Vietnam

8.5.9. Taiwan

8.5.10. Bangladesh

8.5.11. Pakistan

8.5.12. Rest of Asia Pacific

9. Middle East and Africa Cocoa and Chocolate Market Size and Forecast (by Value USD Billion and Volume in Tonnes)

9.1. Middle East and Africa Cocoa and Chocolate Market Size and Forecast, By Type (2026-2034)

9.2. Middle East and Africa Cocoa and Chocolate Market Size and Forecast, By Application (2026-2034)

9.3. Middle East and Africa Cocoa and Chocolate Market Size and Forecast, By Nature (2026-2034)

9.4. Middle East and Africa Cocoa and Chocolate Market Size and Forecast, By Distribution Channel (2026-2034)

9.5. Middle East and Africa Cocoa and Chocolate Market Size and Forecast, by Country (2026-2034)

9.5.1. South Africa

9.5.2. GCC

9.5.3. Egypt

9.5.4. Nigeria

9.5.5. Rest of ME&A

10. South America Cocoa and Chocolate Market Size and Forecast (by Value USD Billion and Volume in Tonnes)

10.1. South America Cocoa and Chocolate Market Size and Forecast, By Type (2026-2034)

10.2. South America Cocoa and Chocolate Market Size and Forecast, By Application (2026-2034)

10.3. South America Cocoa and Chocolate Market Size and Forecast, By Nature (2026-2034)

10.4. South America Cocoa and Chocolate Market Size and Forecast, By Distribution Channel (2026-2034)

10.5. South America Cocoa and Chocolate Market Size and Forecast, by Country (2026-2034)

10.5.1. Brazil

10.5.2. Argentina

10.5.3. Rest of South America

11. Company Profile: Key players

11.1. Mars, Inc. (US)

11.1.1. Company Overview

11.1.2. Product Segment

11.1.2.1. Product Name

11.1.2.2. Product Details (Price, Features, etc.)

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Mondelez International (US)

11.3. Nestle S.A. (Switzerland)

11.4. Meiji Holding Co. Ltd. (Japan

11.5. Ferrero International (Italy)

11.6. Olam Group (Singapore)

11.7. Barry Callebaut (Switzerland)

11.8. Cargill Incorporated (US)

11.9. Cocoa Processing Company (Ghana)

11.10. Archer Daniels Midland (ADM) Company (U.S.)

11.11. Chocoladefabriken Lindt & Sprüngli AG (Switzerland)

11.12. Pladis Global(UK).

11.13. Kerry (Ireland)

11.14. Foley’s Candies LP

11.15. TCHO (U.S.)

11.16. Ghirardelli (U.S.)

11.17. Alpezzi Chocolate (Mexico)

11.18. Valrhona (France)

11.19. Guittard (U.S.)

11.20. Irca (Belgium)

11.21. Hershey (U.S.)

12. Key Findings

13. Industry Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook