Potable Alcohol Market Global Industry Analysis and Forecast (2026-2032)

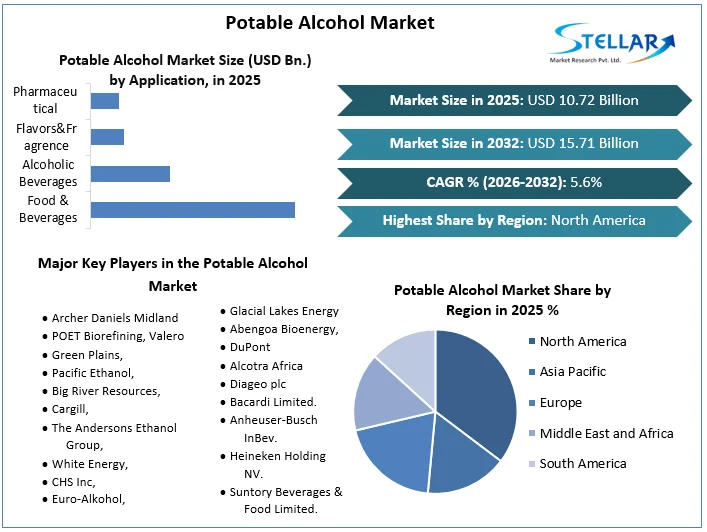

The Potable Alcohol Market size was valued at USD 10.72 Bn. in 2025 and the total Global Potable Alcohol Market revenue is expected to grow at a CAGR of 5.6 % from 2026 to 2032, reaching nearly USD 15.71 Bn. by 2032.

Potable Alcohol Market Overview:

Potable Alcohol is a highly purified product with very neutral odour and taste. This natural product is produced by fermentation of the sugars, using yeast. The sugars are derived from molasses and/or grain. After the fermentation process, the ethanol is purified by a multiple distillation and rectification process.

The growth of the global alcohol market is closely related to the rising disposable income of consumers, particularly in rising economies. As individuals and households experience greater economic prosperity, they tend to allocate a portion of their income to discretionary spending, including indulging in alcoholic beverages. This trend is often accompanied by an aspirational desire to consume premium and imported brands, further boosting the market for higher-priced alcoholic products. Emerging middle-class populations in countries like China and India have become key growth drivers, attracting the attention of global alcohol producers who aim to tap into these blooming markets by customizing their products to local preferences and purchasing power

The growing demand for convenience and rising health consciousness among consumers are the major factors driving the demand for Potable Alcohol. Nowadays, low-calorie drinks with natural ingredients appeal the most to consumers, thus, manufacturers are focusing on launching products with natural ingredients to capture a wider market share.

To get more Insights: Request Free Sample Report

Potable Alcohol Market Dynamics:

The Potable Alcohol Drinks market in Worldwide is experiencing significant growth and development due to changing customer preferences, emerging trends, local special circumstances, and underlying macroeconomic factors.

The Potable Alcohol market in Worldwide is influenced by various macroeconomic factors. Economic growth, rising disposable incomes, and urbanization are key drivers of market expansion. As economies grow, consumers have more purchasing power and are willing to spend on premium alcoholic beverages. Additionally, the increasing urban population, particularly in emerging markets, has led to a rise in the number of bars, restaurants, and entertainment venues, creating a favourable environment for the growth of the market. Furthermore, demographic shifts, such as changing age structures and evolving lifestyles, are shaping the market dynamics.

Millennials, for example, have different preferences and consumption habits compared to previous generations. They are more likely to experiment with new Flavors and brands, seek authentic experiences, and prioritize social and environmental values. As this generation becomes a significant consumer group, companies in the Potable Alcoholic Drinks market are adapting their strategies to cater to their needs and preferences

Various policies and regulations to control the quality of spirits in the market. These policies often mandate the use of ENA of a specific standard in the production of alcoholic beverages. As a result, leading manufacturers are procuring ENA that meets the required specifications, which, in turn, is supporting the growth of the market.

One of the key trends in the Potable Alcohol market in Worldwide is the rise of e-commerce. Online platforms have made it easier for consumers to explore and purchase a wide range of alcoholic beverages from the comfort of their homes. This has opened up new distribution channels for both established brands and small-scale producers, enabling them to reach a larger customer base. Additionally, social media and digital marketing have played a significant role in promoting and creating awareness about new products, driving consumer engagement and loyalty. Another trend in the market is the increasing focus on sustainability and environmental responsibility.

Consumers are becoming more conscious of the environmental impact of their choices and are seeking brands that prioritize sustainability. This has led to a rise in the demand for organic and biodynamic wines, as well as eco-friendly packaging solutions. Companies that embrace sustainable practices and communicate their efforts effectively are likely to gain a competitive edge in the market.

The huge availability of substitute products is one of the major challenges in the global Potable alcohol market

Increasing health concern among consumers leads to a decline in alcohol consumption which give rise to Potable alcohol products in the market

Potable Alcohol Market Segment Analysis:

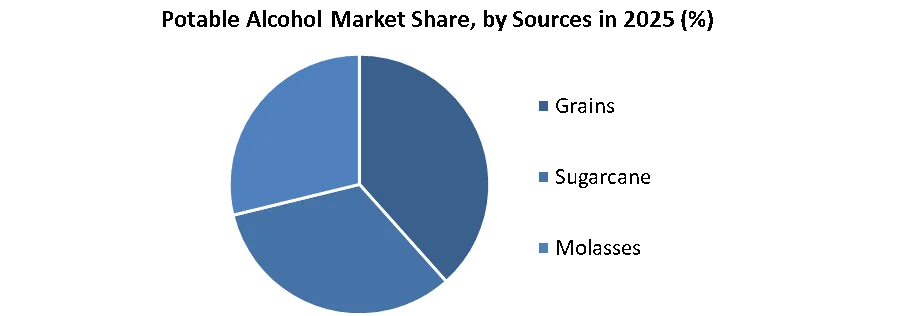

By Source, Sugarcane: Potable alcohol made with a sugar cane base source. This type of alcohol, commonly known as rum, is derived from the fermentation and distillation of sugarcane juice

Neutral sugarcane is used as a base ingredient for rum, vodka and many more different liqueurs with in the food industry it has been utilized in the production of vinegar, as well as put as a solvent for flavouring. Sugarcane also been used as a preservative for a variety of products Organic sugarcane alcohol is most popular and universal carrier solvent for fine fragrance concentrates because of its miscibility tolerance.

Grains: Potable alcohol, also known as drinkable alcohol or consumable alcohol, refers to any type of alcoholic beverage that is safe for human consumption. It is produced through the fermentation and distillation of various ingredients, including grains. When it comes to potable alcohol made with grains, it typically refers to spirits such as whiskey, vodka, gin, and rum. These types of alcoholic beverages are produced by fermenting grains like barley, corn, rye, or wheat and then distilling the resulting mixture. During the fermentation process, grains give yeast the carbohydrates it needs to produce alcohol.

Molasses: Molasses is a major ingredient in the production of potable alcohol, a form of alcoholic beverage. The process begins with the fermentation of molasses, where yeast converts the sugars present in molasses into alcohol through a natural chemical reaction. This fermented mixture is then distilled to remove impurities and increase its alcohol content. The resulting product is a clear and potent alcoholic beverage.

Potable Alcohol Market Regional insights:

North America: The North American region which includes countries like the US, Canada, and Mexico has a highest share contributed to the potable alcohol market. Consumer preferences for alcoholic beverages are evolving in this region owing to the ever-changing consumer preferences over time. Consumers are often ready to pay more for high-quality, artisanal products, which has led to increased demand for specialty and craft alcoholic beverages.

In United states and Canada there is a rich tradition of alcohol consumption with beer, spirits and wine being popular choice among consumers however, there has been a shifting towards premiumization and craft offerings, driven by consumer’s desire for quality and unique experience

Europe: The European region which consists of key countries like France, the UK, Germany, Italy, and Spain plays a pivot role in the development of the potable alcohol market. France is renowned for its wine culture, and wine consumption has historically been an integral part of French society. The country is one of the world's leading wine producers, and its reputation for quality wines has led to a consistent domestic and international demand for French wines. France is a major exporter of wine and spirits, wherein wines are highly regarded globally, and the export market has been a significant driver of growth for the French wine industry. Exports have contributed to the overall expansion of the potable alcohol market.

Potable Alcohol Market Competitive Landscape:

- 4 March 2024 – As the global leader in premium drinks, Diageo marks its ongoing ambition to shape the future of how people around the world interact with its extensive portfolio of iconic brands through an inaugural experience with Apple Vision Pro. Tequila Don Julio, Mexico’s original luxury tequila, will be the first Diageo brand to leverage this immersive new storytelling platform, as the company adapts this emerging technology to create new experiences for tequila enthusiasts.

- 09.02.24 Carlsberg celebrates the Year of the Dragon with limited edition packaging Lunar New Year, also called Chinese New Year, is a major celebration across Asia and other parts of the world. This year, Carlsberg delighted to showcase the extraordinary collaboration that has resulted in the creation of our special edition Lunar New Year Carlsberg Pilsners.

- LEXINGTON, KY – Thursday, April 11th 2024 – Keeneland Race Course and Maker’s Mark Kentucky Bourbon today announced a new chapter in their longstanding partnership with the launch of “Greats of the Gate,” a 10-year commemorative bottle series celebrating Thoroughbred racing’s most iconic horses – featuring a different horse each year.

Potable Alcohol Market Scope

|

Potable Alcohol Market |

|

|

Market Size in 2025 |

USD 10.72 Bn. |

|

Market Size in 2032 |

USD 15.71 Bn. |

|

CAGR (2026-2032) |

5.6 % |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segments |

By Sources

|

|

By Application

|

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Russia, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Player in the Potable Alcohol Market

- Archer Daniels Midland

- POET Biorefining, Valero

- Green Plains,

- Pacific Ethanol,

- Big River Resources,

- Cargill,

- The Andersons Ethanol Group,

- White Energy,

- CHS Inc,

- Euro-Alkohol,

- Glacial Lakes Energy

- Abengoa Bioenergy,

- DuPont

- Alcotra Africa

- Diageo plc

- Bacardi Limited.

- Anheuser-Busch InBev.

- Heineken Holding NV.

- Suntory Beverages & Food Limited.

- Pernord Richard SA

Frequently Asked Questions

Potable Alcohol segments are Based on By Sources, By Application and By Region.

The Potable Alcohol market in Worldwide is influenced by various macroeconomic factors. Economic growth, rising disposable incomes, and urbanization are key drivers of market expansion. As economies grow, consumers have more purchasing power and are willing to spend on premium alcoholic beverages.

Archer Daniels Midland, POET Biorefining, Valero Green Plains, Pacific Ethanol, Big River Resources, and many more.

Potable Alcohol Market revenue is expected to grow at a CAGR of 5.6 % from 2026 to 2032.

1. Potable Alcohol Market: Research Methodology

1.1. Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Assumptions

2. Potable Alcohol Market: Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026– 2032) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Potable Alcohol Market: Competitive Landscape

3.1. Stellar Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Product Segment

3.2.4. Total Production (2025)

3.2.5. End-user Segment

3.2.6. Y-O-Y%

3.2.7. Revenue (2025)

3.2.8. Profit Margin

3.2.9. Market Share

3.2.10. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. Product Launches and Innovation

4. Potable Alcohol Market: Dynamics

4.1. Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Market Drivers

4.3. Market Restraints

4.4. Market Opportunities

4.5. Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factors

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Value Chain Analysis

4.10. Regulatory Landscape by Region

4.10.1. North America

4.10.2. Europe

4.10.3. Asia Pacific

4.10.4. Middle East and Africa

4.10.5. South America

5. Potable Alcohol Market Size and Forecast by Segments (by Value USD Million)

5.1. Potable Alcohol Market Size and Forecast, By Sources (2025-2032)

5.1.1. Grains

5.1.2. Sugarcane

5.1.3. Molasses

5.2. Potable Alcohol Market Size and Forecast, By Application (2025-2032)

5.2.1. Food & Beverages

5.2.2. Alcoholic Beverages

5.2.3. Flavors&Fragrence

5.2.4. Pharmaceutical

5.2.5. Others

5.3. Potable Alcohol Market Size and Forecast, by Region (2025-2032)

5.3.1. North America

5.3.2. Europe

5.3.3. Asia Pacific

5.3.4. Middle East and Africa

5.3.5. South America

6. North America Potable Alcohol Market Size and Forecast (by Value USD Million)

6.1. North America Potable Alcohol Market Size and Forecast, By Sources (2025-2032)

6.1.1. Grains

6.1.2. Sugarcane

6.1.3. Molasses

6.2. North America Potable Alcohol Market Size and Forecast, By Application (2025-2032)

6.2.1. Food & Beverages

6.2.2. Alcoholic Beverages

6.2.3. Flavors&Fragrence

6.2.4. Pharmaceutical

6.2.5. Others

6.3. North America Potable Alcohol Market Size and Forecast, by Country (2025-2032)

6.3.1. United States

6.3.2. Canada

6.3.3. Mexico

7. Europe Potable Alcohol Market Size and Forecast (by Value USD Million)

7.1. Europe Potable Alcohol Market Size and Forecast, By Sources (2025-2032)

7.2. Europe Potable Alcohol Market Size and Forecast, By Application (2025-2032)

7.3. Europe Potable Alcohol Market Size and Forecast, by Country (2025-2032)

7.3.1. UK

7.3.2. France

7.3.3. Germany

7.3.4. Italy

7.3.5. Spain

7.3.6. Sweden

7.3.7. Austria

7.3.8. Rest of Europe

8. Asia Pacific Potable Alcohol Market Size and Forecast (by Value USD Million)

8.1. Asia Pacific Potable Alcohol Market Size and Forecast, By Sources (2025-2032)

8.2. Asia Pacific Potable Alcohol Market Size and Forecast, By Application (2025-2032)

8.3. Asia Pacific Potable Alcohol Market Size and Forecast, by Country (2025-2032)

8.3.1. China

8.3.2. S Korea

8.3.3. Japan

8.3.4. India

8.3.5. Australia

8.3.6. Indonesia

8.3.7. Malaysia

8.3.8. Vietnam

8.3.9. Taiwan

8.3.10. Bangladesh

8.3.11. Pakistan

8.3.12. Rest of Asia Pacific

9. Middle East and Africa Potable Alcohol Market Size and Forecast (by Value USD Million)

9.1. Middle East and Africa Potable Alcohol Market Size and Forecast, By Sources (2025-2032)

9.2. Middle East and Africa Potable Alcohol Market Size and Forecast, By Application (2025-2032)

9.3. Middle East and Africa Potable Alcohol Market Size and Forecast, by Country (2025-2032)

9.3.1. South Africa

9.3.2. GCC

9.3.3. Egypt

9.3.4. Nigeria

9.3.5. Rest of ME&A

10. South America Potable Alcohol Market Size and Forecast (by Value USD Million)

10.1. South America Potable Alcohol Market Size and Forecast, By Sources (2025-2032)

10.2. South America Potable Alcohol Market Size and Forecast, By Application (2025-2032)

10.3. South America Potable Alcohol Market Size and Forecast, by Country (2025-2032)

10.3.1. Brazil

10.3.2. Argentina

10.3.3. Rest of South America

11. Company Profile: Key players

11.1. Archer Daniels Midland

11.1.1. Company Overview

11.1.2. Product Portfolio

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. POET Biorefining, Valero

11.3. Green Plains,

11.4. Pacific Ethanol,

11.5. Big River Resources,

11.6. Cargill,

11.7. The Andersons Ethanol Group,

11.8. White Energy,

11.9. CHS Inc,

11.10. Euro-Alkohol,

11.11. Glacial Lakes Energy

11.12. Abengoa Bioenergy,

11.13. DuPont

11.14. Alcotra Africa

11.15. Diageo plc

11.16. Bacardi Limited.

11.17. Anheuser-Busch InBev.

11.18. Heineken Holding NV.

11.19. Suntory Beverages & Food Limited.

11.20. Pernord Richard SA

12. Key Findings

13. Industry Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook