Tomato Processing Market Industry Analysis and Forecast (2026-2032)

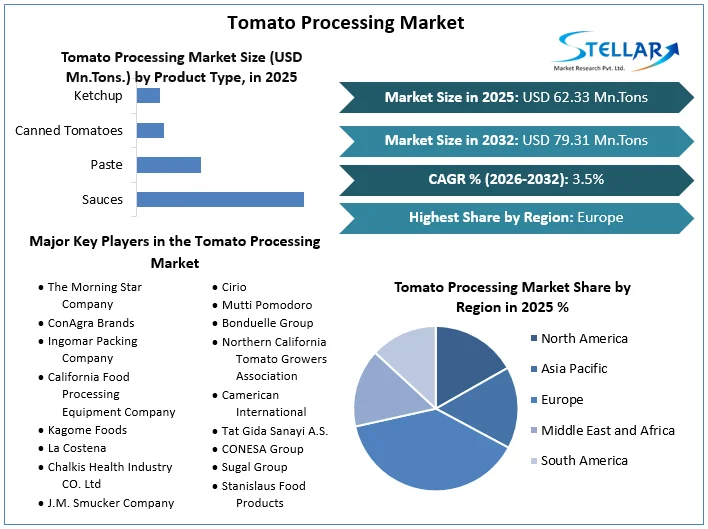

The Tomato Processing Market size was USD 62.33 Mn. Tons in 2025 and the total Global Tomato Processing market is expected to grow at a CAGR of 3.5% from 2026 to 2032, reaching nearly USD 79.31 Mn. Tons by 2032.

Tomato Processing Market Overview

The process of converting fresh tomatoes into value added product by canning, pureeing, drying, and other techniques is known as Tomato Processing. The procedure ensure that tomatoes have a longer shelf life while maintaining their flavour and nutritional value. The food and beverage sector uses processed tomato products extensively for sauces, ketchups, soups, pastes, and other tomato based products. Processed tomatoes are the main ingredient for all these products.

Tomatoes are a highly popular vegetable known for their nutritional and health benefits. Their high initial moisture content makes them susceptible to postharvest deterioration, necessitating preservation techniques. 80% of global tomato production is processed into value-added products such as ketchup, powders, sauces, and juices.

The demand for tomato processing usually arises from a need to preserve the product for home use (inclusion in stews, soups, curries etc.) out of season or to add value for extra income. Traditionally, the most important methods used are concentration (to a paste or purée) and drying either fruit pieces or to a powder. These remain the most suitable processes for many people to use and form the bulk of this brief.

To get more Insights: Request Free Sample Report

Tomato Processing Market Dynamics

Increasing Demand for Convenience Food and Growing Food Industry

The demand for easy food items, such as processed tomato products like sauces, pastes, and canned tomatoes, has increased because of busy lifestyle and urbanization, which is propelling the growth of the tomato processing market. The need for processed tomato products including soups, sauces, pizzas, and ready meals is being driven by the growing food sector, especially in growing economies. These is further fuelling the tomato processing market. The problem of fresh tomato perishability and seasonal availability are addressed by processed tomato products. They contribute to the market growth by providing consumers with an extended shelf life and allowing them to enjoy all year around in all seasons.

Raw Material Cost and Health Concerns

Processing companies profit margins are impacted by the fluctuation in the prices of raw material. Tomato yield is impacted by weather related events like droughts or pests, which cause supply disruptions and price volatility. Even though tomatoes are nutrient dense, processed tomato products face scrutiny because of concerns about additives, preservatives, or high level of sugar or salt. Consumer’s preference towards healthier options decreases the demand for processed tomato products.

Quality Control and Market Competition

It is difficult to maintain consistent quality throughout the processing steps, particularly when dealing with the inherent variances in tomato yields. Strong quality control procedures are needed to guarantee consistency in flavour, texture, and colour throughout batches. There are many companies fighting for market share in the very competitive tomato processing sector. For processors to be competitive in the market, they need to set themselves apart from the competition with elements like price, quality, innovation, and branding. Tomato processors have to adhere to quality standards, labelling laws, and regulations pertaining to food safety. Operations become more complex when one has to stay on top of changing legislation and ensure compliance in multiple markets.

Product Innovation and Export Opportunities

Processors have the chance to adapt to changing consumer tastes and market trends by innovating and broadening their product offerings. These entail the creation of fresh tomato-based goods, like flavoured salsas, dips, sauces, and prepared meals, in addition to healthier or more upscale versions that satisfy particular dietary requirements. Tomato processors have options to sell their products to other markets as a result of the globalisation of the food sector.

By entering new export markets, companies lessen their reliance on changes in domestic demand and diversify their sources of income. It is possible to develop synergies and open up new business prospects by working together with other food industry participants like growers, merchants, or foodservice providers. Collaborations bring mutual growth and success by providing access to new product development knowledge, distribution channels, and resources.

Tomato Processing Market Segment Analysis

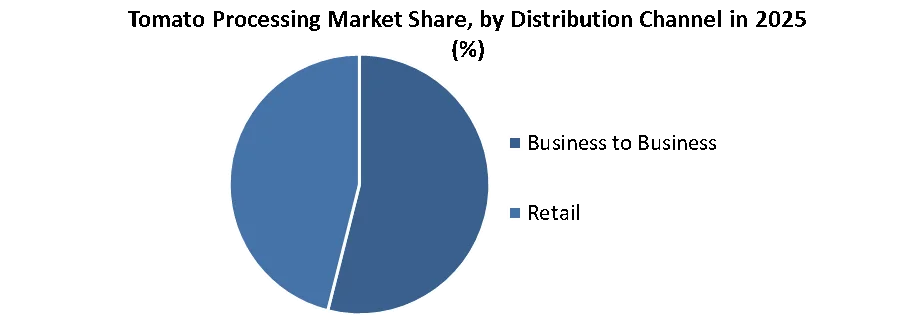

Based on Distribution Channel, market is divided into Business to Business channel and Retail channel. Retail channel has the highest market share in the segment. A major factor driving the market is the growing number of convenience-conscious consumers who are interested in packaged and processed tomato products such purees, ketchups, and sauces. Because they offer a wide range of products, supermarkets and hypermarkets are important retail locations that successfully meet this need. Additionally, because private labelling allows retailers to sell high-quality goods at reasonable costs, it has helped the retail industry.

In response to growing consumer concerns about nutrition and wellbeing, many merchants are diversifying their product offerings to include more natural, healthier options. In addition, the growing influence of e-commerce has forced conventional merchants to change by merging their online and offline sales channels to provide customers with an Omni channel experience. Retail is being promoted as a preferred channel by technological innovations like contactless payments and QR codes, which further simplify the shopping experience. Geographically, more consumers have access to processed tomato products as retail networks spread into suburban and rural areas.

Business to Business (B2B) channel has the second highest market share in the segment. Business to Business processed tomato suppliers operate in a various regions worldwide. In this channel suppliers explore new markets, which involves understanding local preferences, adopting products to cultural tastes, navigating regulatory requirements, and establish distribution networks to reach their customers. In Business to Business channel most of the customers are food restaurants, and companies who produce value added products from the processed tomatoes.

Tomato Processing Market Regional Analysis

Europe dominates the market with compound annual growth rate (CAGR) of 3.7%. The tomato processing business in Europe is driven by multiple market factors that support its steady growth. The area's vibrant culinary scene, which favours tomato-based goods like sauces, pastes, and ketchups, is one of the primary drivers. Demand is fuelled by the popularity of Mediterranean food, which is renowned for its tasty and nutritious components, which include tomatoes. Furthermore, the trend for organic and GMO-free tomato products is growing among health-conscious European customers.

Manufacturers have responded by implementing cleaner processing techniques and sustainable farming methods. Technological developments in agriculture and processing are another factor, increasing yields and decreasing waste to boost industry efficiency. Europe's strict laws governing food safety further guarantee excellent standards, winning over customers' confidence and increasing revenue. Furthermore, the growth of e-commerce has extended market penetration, enabling producers to serve a wider range of customers. The European Union's trade agreements make cross-border distribution simpler and increase product accessibility.

Asia Pacific is the largest producer of tomatoes in the world. These factor is propelling the growth of the tomato processing market in the region. Governments across Asia Pacific are supporting the tomato processing industry through different policies an incentives, which is creating a favourable environment for the market players. High production of tomatoes, sufficient manpower, and supportive government policies offers good opportunities to the market players and fuels the growth of tomato processing market in the region.

Tomato Processing Market Competitive Landscape

- Dec 2023, KURNOOL: The tomato processing unit being established in Pathikonda and managed by a local farmer producer organisation (FPO) would be a boon to local tomato farmers.

- In May 2023, Pacific Coast Producers received $890,000 in state funds for climate investment to cut emissions at its Woodland tomato processing plant, which is projected to increase efficiency.

- In February 2022, Olam International announced the news to sell off the northern 15-acre tomato processing portion of the company but keep the remaining 10 acres of the processing facility property for its granulated garlic business.

|

Tomato Processing Market Scope |

|

|

Market Size in 2025 |

USD 62.33 Million Tons |

|

Market Size in 2032 |

USD 79.31 Million Tons |

|

CAGR (2026-2032) |

3.5% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segments |

By Distribution Channel Business to Business Retail |

|

By Product Type Sauces Paste Canned Tomatoes Ketchup Others |

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Players in the Tomato Processing Market

- The Morning Star Company

- ConAgra Brands

- Ingomar Packing Company

- California Food Processing Equipment Company

- Kagome Foods

- La Costena

- Chalkis Health Industry CO. Ltd

- J.M. Smucker Company

- Kraft Heinz Company

- Cirio

- Mutti Pomodoro

- Bonduelle Group

- Northern California Tomato Growers Association

- Camerican International

- Tat Gida Sanayi A.S.

- CONESA Group

- Sugal Group

- Stanislaus Food Products

- Los Gatos Tomato Products

- Olam International

Frequently Asked Questions

Global tomato processing market is expected to grow at CAGR of 3.5% during 2026-2032.

The growing demand for processed tomato products that are generally characterized by a relatively longer shelf life and ease of storage is primarily driving the global tomato processing market.

Based on the product type, the market has been divided into sauces, paste, canned tomatoes, ketchup, juice, and others.

On a regional level, the market has been classified into North America, Asia Pacific, Europe, Latin America, and Middle East and Africa.

1. Tomato Processing Market: Research Methodology

1.1. Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Assumptions

2. Tomato Processing Market: Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026 – 2032) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Tomato Processing Market: Competitive Landscape

3.1. Stellar Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Business Segment

3.2.5. End-user Segment

3.2.6. Y-O-Y%

3.2.7. Revenue (2025)

3.2.8. Profit Margin

3.2.9. Market Share

3.2.10. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. Product Launches and Innovation

4. Tomato Processing Market: Dynamics

4.1. Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Market Drivers

4.3. Market Restraints

4.4. Market Opportunities

4.5. Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factors

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Regulatory Landscape by Region

4.9.1. North America

4.9.2. Europe

4.9.3. Asia Pacific

4.9.4. Middle East and Africa

4.9.5. South America

5. Tomato Processing Market Size and Forecast by Segments (by Value USD Million)

5.1. Tomato Processing Market Size and Forecast, By Distribution Channel (2025-2032)

5.1.1. Business to Business

5.1.2. Retail

5.2. Tomato Processing Market Size and Forecast, By Product Type (2025-2032)

5.2.1. Sauces

5.2.2. Paste

5.2.3. Canned Tomatoes

5.2.4. Ketchup

5.2.5. Others

5.3. Tomato Processing Market Size and Forecast, by Region (2025-2032)

5.3.1. North America

5.3.2. Europe

5.3.3. Asia Pacific

5.3.4. Middle East and Africa

5.3.5. South America

6. North America Tomato Processing Market Size and Forecast (by Value USD Million)

6.1. North America Tomato Processing Market Size and Forecast, By Distribution Channel (2025-2032)

6.1.1. Business to Business

6.1.2. Retail

6.2. North America Tomato Processing Market Size and Forecast, By Product Type (2025-2032)

6.2.1. Sauces

6.2.2. Paste

6.2.3. Canned Tomatoes

6.2.4. Ketchup

6.2.5. Others

6.3. North America Tomato Processing Market Size and Forecast, by Country (2025-2032)

6.3.1. United States

6.3.2. Canada

6.3.3. Mexico

7. Europe Tomato Processing Market Size and Forecast (by Value USD Million)

7.1. Europe Tomato Processing Market Size and Forecast, By Distribution Channel (2025-2032)

7.2. Europe Tomato Processing Market Size and Forecast, By Product Type (2025-2032)

7.3. Europe Tomato Processing Market Size and Forecast, by Country (2025-2032)

7.3.1. UK

7.3.2. France

7.3.3. Germany

7.3.4. Italy

7.3.5. Spain

7.3.6. Sweden

7.3.7. Austria

7.3.8. Rest of Europe

8. Asia Pacific Tomato Processing Market Size and Forecast (by Value USD Million)

8.1. Asia Pacific Tomato Processing Market Size and Forecast, By Distribution Channel (2025-2032)

8.2. Asia Pacific Tomato Processing Market Size and Forecast, By Product Type (2025-2032)

8.3. Asia Pacific Tomato Processing Market Size and Forecast, by Country (2025-2032)

8.3.1. China

8.3.2. S Korea

8.3.3. Japan

8.3.4. India

8.3.5. Australia

8.3.6. Indonesia

8.3.7. Malaysia

8.3.8. Vietnam

8.3.9. Taiwan

8.3.10. Bangladesh

8.3.11. Pakistan

8.3.12. Rest of Asia Pacific

9. Middle East and Africa Tomato Processing Market Size and Forecast (by Value USD Million)

9.1. Middle East and Africa Tomato Processing Market Size and Forecast, By Distribution Channel (2025-2032)

9.2. Middle East and Africa Tomato Processing Market Size and Forecast, By Product Type (2025-2032)

9.3. Middle East and Africa Tomato Processing Market Size and Forecast, by Country (2025-2032)

9.3.1. South Africa

9.3.2. GCC

9.3.3. Egypt

9.3.4. Nigeria

9.3.5. Rest of ME&A

10. South America Tomato Processing Market Size and Forecast (by Value USD Million)

10.1. South America Tomato Processing Market Size and Forecast, By Distribution Channel (2025-2032)

10.2. South America Tomato Processing Market Size and Forecast, By Product Type (2025-2032)

10.3. South America Tomato Processing Market Size and Forecast, by Country (2025-2032)

10.3.1. Brazil

10.3.2. Argentina

10.3.3. Rest of South America

11. Company Profile: Key players

11.1. The Morning Star Company

11.1.1. Company Overview

11.1.2. Business Portfolio

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. ConAgra Brands

11.3. Ingomar Packing Company

11.4. California Food Processing Equipment Company

11.5. Kagome Foods

11.6. La Costena

11.7. Chalkis Health Industry CO. Ltd

11.8. J.M. Smucker Company

11.9. Kraft Heinz Company

11.10. Cirio

11.11. Mutti Pomodoro

11.12. Bonduelle Group

11.13. Northern California Tomato Growers Association

11.14. Camerican International

11.15. Tat Gida Sanayi A.S.

11.16. CONESA Group

11.17. Sugal Group

11.18. Stanislaus Food Products

11.19. Los Gatos Tomato Products

11.20. Olam International

12. Key Findings

13. Industry Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook