Hydrolyzed Vegetable Protein Market - Global Industry Analysis and Forecast 2026-2034

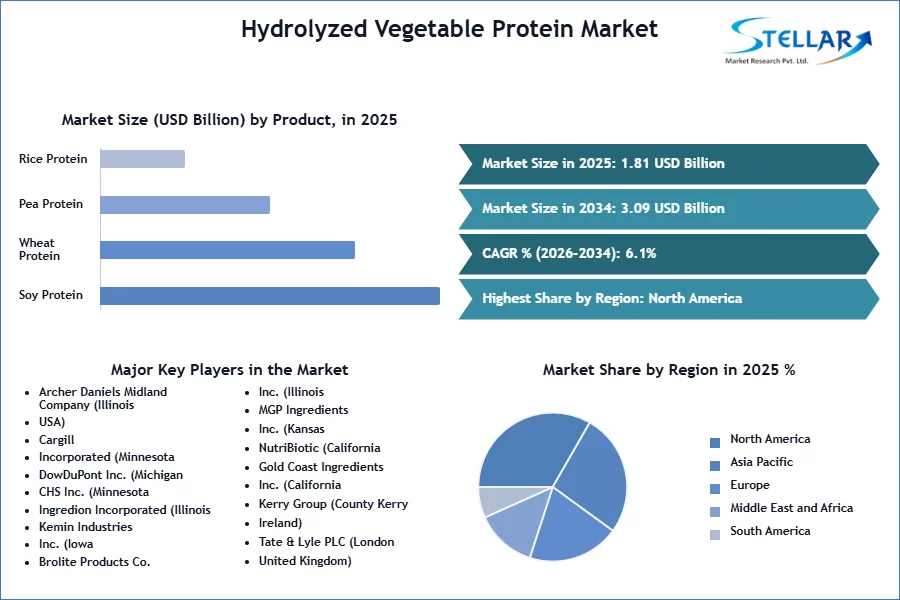

The Hydrolyzed Vegetable Protein Market size was valued at USD 1.81 Bn. in 2025 and the total Hydrolyzed Vegetable Protein revenue is expected to grow at a CAGR of 6.1% from 2026 to 2034, reaching nearly USD 3.09 Bn.

Hydrolyzed Vegetable Protein Market Overview:

Hydrolyzed vegetable protein (HVP) is gaining recognition as a global culinary sensation. HVP is derived from the breakdown of protein-rich substances through processes like acid, alkaline, or enzymatic hydrolysis. However, its true essence lies in its remarkable versatility as a flavor enhancer, particularly known for its ability to evoke or intensify savory tastes. In the realm of vegetarian and vegan cuisine, HVP is emerging as a prominent player. Being sourced from plants, it seamlessly aligns with dietary preferences advocating for vegetarian and vegan choices. This attribute makes HVP a preferred option for those adhering to such dietary guidelines. Hydrolyzed vegetable proteins (HVPs) and yeast extracts serve as indispensable flavor enhancers across a diverse array of processed foods.

These additives are pivotal in elevating the taste profiles of soups, chili, sauces, gravies, stews, and various meat products like hot dogs. Their versatility extends to dips, snacks like potato chips and pretzels, as well as seasonings, marinades, and side dishes. HVPs are crafted from a spectrum of protein sources, ensuring a rich reservoir of savory flavor systems. Their utility spans IP-certified and non-GMO variants, catering to discerning consumer preferences. Low-sodium HVPs further accentuate their appeal, aligning with health-conscious consumption trends in Hydrolyzed Vegetable Protein Market. Their role in enhancing mouthfeel extends beyond conventional applications, finding resonance in plant protein beverages, cold drinks, and cold foods.

Yeast extracts emerge as stalwarts in flavor modulation. Baker’s and brewer’s yeast extracts, alongside bespoke solutions, underpin a great approach to crafting product-specific flavor profiles. This versatility positions them as indispensable bases for seasonings and soups, infusing depth into snack seasonings and tastemakers. The distinct flavor profiles imparted by these additives underscore their indispensability. Offering notes of meatiness, smokiness, and umami, they seamlessly integrate into beef and chicken soups, elevating culinary experiences. Their role as a natural alternative to sodium glutamate, in Chinese cuisine and beyond, underscores their appeal in addressing evolving dietary preferences.

The application transcends conventional boundaries, permeating into instant soups, ready-to-eat snacks like extruded varieties and noodles, as well as spice mixes and meaty flavor enhancers. As a versatile sauce component and a replacement for mono-sodium glutamate, HVPs emerge as pivotal in the culinary landscape which drives Hydrolyzed Vegetable Protein Market.

To get more Insights: Request Free Sample Report

Hydrolyzed Vegetable Protein Market Dynamics:

A Nutritional Powerhouse and Culinary Marvel is Driving the growth of Hydrolyzed Vegetable Protein Market

Hydrolyzed Vegetable Protein (HVP) is celebrated for its nutritional prowess, boasting a high protein content and essential amino acids vital for bodily functions like tissue repair and muscle building. Its low-fat, low-carb profile makes it a favored choice for those seeking protein-rich diets without excess calories. In the culinary realm, HVP reigns supreme as a versatile flavor enhancer, elevating dishes ranging from soups and sauces to snacks and meat products. Its ability to enrich umami and savory notes caters to evolving palates, while its plant-based nature aligns seamlessly with the surging demand for vegetarian and vegan options. Safety regulations govern the production of HVP, ensuring stringent quality control measures to uphold consumer trust. Regular inspections and adherence to hygienic standards guarantee the product's purity and safety.

Environmental consciousness further bolsters HVP's appeal, with its plant-derived origin contributing to a lower carbon footprint and sustainable food production practices. Additionally, HVP's health benefits extend beyond its protein content; its role as a flavor enhancer can reduce the need for added salt, promoting lower sodium intake. Selecting the right HVP product is paramount, and ETprotein emerges as a leader in the field. Their commitment to quality shines through their range of non-GMO Hydrolyzed Vegetable Protein products. Employing advanced technology, ETprotein ensures optimal protein hydrolysis, resulting in a product rich in amino acids and devoid of unwanted by-products. With rigorous quality control measures in place, HVP stands as a benchmark for excellence, meeting the highest industry standards and delighting food manufacturers and consumers in Hydrolyzed Vegetable Protein Market demand.

Plant-Based Palates HVP's Crucial Role in Catering to Changing Consumer Tastes

The current landscape of the food industry presents a compelling opportunity for Hydrolyzed Vegetable Protein (HVP) powders to shine as indispensable flavor enhancers. As one of the most favored and cost-effective ingredients, HVP plays a crucial role in imparting a distinctive umami note to savory prepared foods. Its inclusion in product recipes significantly influences taste profiles, making it a cornerstone ingredient for food companies worldwide. In recent times, there has been a notable shift in consumer preferences towards plant-based and vegetarian options. This shift has created a pressing need for food companies to innovate and offer tasteful variants derived from plant or vegetable sources. Consumers are increasingly seeking products that align with their dietary choices and values, prompting food companies to explore new avenues and develop distinctive offerings Hydrolyzed Vegetable Protein Market propels the demand.

In the evolving consumer landscape, forward-thinking companies have seized the opportunity to leverage their expertise and cutting-edge technology to meet these needs. By harnessing deep product understanding and innovative processes, these companies have developed a unique range of Reaction Flavors that offer non-vegetarian profiles such as Chicken and Beef entirely derived from vegetarian protein sources like Maize, Soya, or Wheat. This innovative approach opens doors to a wealth of opportunities for food companies. With the novel Reaction Flavors in their product formulations, food companies can create character-specific food products that resonate with consumers seeking delicious yet vegetarian-friendly options.

This not only satisfies consumer demand for Hydrolyzed Vegetable Protein Market but also allows companies to differentiate themselves in a competitive market landscape. Furthermore, the versatility and sustainability of these Reaction Flavors align perfectly with modern consumer values. By utilizing vegetarian protein sources, companies not only meet the demand for plant-based alternatives but also contribute to environmentally conscious food production practices, thereby enhancing their brand image and appeal among consumers. The emergence of these innovative Reaction Flavors presents a unique opportunity for food companies to meet the evolving needs of consumers while driving growth and innovation in the industry.

Hydrolyzed Vegetable Protein Market Segment Analysis:

Based on Product Type, the market is divided into Soy Protein, Wheat Protein, Pea Protein, Rice Protein, Chia Protein, Flax Protein, and Corn Protein. Soy Protein witnessed the highest market share in 2025 and continued its dominance during the forecast period. Soy protein is widely available and has been a staple in the food industry for decades. Its versatility allows it to be used in various forms, including whole soybeans, soy flour, soy protein concentrate, and soy protein isolate. Soy protein is considered a complete protein, meaning it contains all nine essential amino acids required by the human body. This nutritional profile makes it highly desirable for food manufacturers looking to fortify their products with protein. Soy protein possesses excellent functional properties, including emulsification, gelation, and water absorption.

These properties make it suitable for a wide range of food applications, from meat analogs to dairy alternatives to baked goods. While soy allergies do exist, they are less common compared to allergies to other plant-based proteins like wheat or peanuts. Soy protein can cater to a broader consumer base, including those with specific dietary restrictions or preferences. Soybeans are relatively sustainable to cultivate, requiring less land and water compared to some other protein sources like animal-derived proteins. This aligns with the growing consumer demand for environmentally friendly and sustainable food options in Hydrolyzed Vegetable Protein Market trend.

Hydrolyzed Vegetable Protein Market Regional Insight:

North America witnessed the highest Hydrolyzed Vegetable Protein market share in 2025 and continued its dominance during the forecast period. North America boasts a thriving food industry characterized by a diverse range of products catering to varying consumer preferences. The region's food manufacturers recognized the significance of HVP as a cost-effective and favored ingredient, integrating it into a multitude of savory prepared foods to enhance flavor profiles. Moreover, consumer demand in North America aligned closely with the trends favoring plant-based and vegetarian options.

As consumers increasingly sought products that resonated with their dietary choices and values, the demand for HVP soared, further propelling the market share of North America. Additionally, the region's food companies exhibited a penchant for innovation, continually seeking ways to meet evolving consumer needs. By leveraging advanced technologies and deep product understanding, North American companies developed novel formulations incorporating HVP, thereby solidifying their market dominance.

Hydrolyzed Vegetable Protein Market Competitive Landscape:

On 15 March, 2022, Kerry, renowned as the taste and nutrition company globally, has officially unveiled its newly upgraded facility located in Rome, Georgia. A significant investment totaling €125 million ($137 million) has been dedicated to crafting one of the most cutting-edge food manufacturing facilities in the United States. This initiative stands as Kerry's most substantial capital expenditure to date and ranks among the largest investments in Georgia's history. This state-of-the-art facility, now employing 250 individuals, offers integrated taste and nutrition solutions tailored to meet the escalating consumer demand within the poultry, seafood, and alternative protein markets across the US and Canada.

Spanning an impressive 316,000 square feet, the facility showcases leading-edge food technologies and systems, ensuring the highest standards of food safety are maintained. In line with Kerry's commitment to sustainability, as outlined in their "Beyond the Horizon" strategy, the company has implemented a range of sustainability initiatives throughout the facility. These initiatives encompass the utilization of 100% renewable electricity, achieving zero waste to landfill, adopting bulk receiving of materials, promoting local sourcing wherever feasible, and leveraging energy-efficient equipment extensively.

|

Hydrolyzed Vegetable Protein Market Scope |

|

|

Market Size in 2025 |

USD 1.81 Billion |

|

Market Size in 2034 |

USD 3.09 Billion |

|

CAGR (2026-2034) |

6.1% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Segments |

By Form Chunks Slice Flakes Granules |

|

By Product Type Soy Protein Wheat Protein Pea Protein Rice Protein Chia Protein Flax Protein Corn Protein |

|

|

By Distribution Channel Online Channels Offline Channels |

|

|

By End User Food and Beverages Cosmetics and Personal Care Pharmaceuticals Others |

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Russia, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Players in the Hydrolyzed Vegetable Protein Market

North America:

- Archer Daniels Midland Company (Illinois, USA)

- Cargill, Incorporated (Minnesota, USA)

- DowDuPont Inc. (Michigan, USA)

- CHS Inc. (Minnesota, USA)

- Ingredion Incorporated (Illinois, USA)

- Kemin Industries, Inc. (Iowa, USA)

- Brolite Products Co., Inc. (Illinois, USA)

- MGP Ingredients, Inc. (Kansas, USA)

- NutriBiotic (California, USA)

- Brolite Products Co., Inc. (Illinois, USA)

- MGP Ingredients, Inc. (Kansas, USA)

- NutriBiotic (California, USA)

- Gold Coast Ingredients, Inc. (California, USA)

Europe:

- Kerry Group (County Kerry, Ireland)

- Tate & Lyle PLC (London, United Kingdom)

- Roquette Frères (Lestrem, France)

- Givaudan SA (Vernier, Switzerland)

- Diana Group (Vannes, France)

- Meelunie B.V. (Amsterdam, Netherlands)

- Fuerst Day Lawson Ltd. (London, United Kingdom)

Asia-Pacific

- Ajinomoto Co., Inc. (Tokyo, Japan)

- Sonic Biochem Extraction Pvt. Ltd. (Ahmedabad, India)

- Niran (Thailand) Co., Ltd. (Bangkok, Thailand)

Frequently Asked Questions

The growth of the Hydrolyzed Vegetable Protein market is primarily driven by factors such as the rising popularity of plant-based diets, increasing consumer awareness about the health benefits of vegetable proteins, and the expanding food and beverage industry's focus on clean label and natural ingredients.

Key opportunities in the Hydrolyzed Vegetable Protein market include expanding applications in various food and beverage products such as snacks, ready-to-eat meals, and sports nutrition, as well as the potential for innovation in product formulations to meet the diverse preferences of consumers, including texture, flavor, and functionality enhancements. Additionally, the growing demand for clean labels and natural ingredients presents opportunities for market players to capitalize on the increasing consumer preference for healthier and sustainable food options.

The Hydrolyzed Vegetable Protein Market size was valued at USD 1.71 Billion in 2024 and the total Global Hydrolyzed Vegetable Protein revenue is expected to grow at a CAGR of 6.1% from 2025 to 2032, reaching nearly USD 2.74 Billion by 2032.

The segments covered in the market report are Form, Product Type, Distribution Channel, End User, and region.

1. Research Methodology

1.1 Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Research Assumption

2. Hydrolyzed Vegetable Protein Market: Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026– 2034) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Global Hydrolyzed Vegetable Protein Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Product Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. Product Launches and Innovations

4. Hydrolyzed Vegetable Protein Market: Dynamics

4.1. Hydrolyzed Vegetable Protein Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Hydrolyzed Vegetable Protein Market Drivers

4.3. Hydrolyzed Vegetable Protein Market Restraints

4.4. Hydrolyzed Vegetable Protein Market Opportunities

4.5. Hydrolyzed Vegetable Protein Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factor

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Value Chain Analysis and Supply Chain Analysis

4.10. Regulatory Landscape by Region

4.10.1. North America

4.10.2. Europe

4.10.3. Asia Pacific

4.10.4. Middle East and Africa

4.10.5. South America

5. Hydrolyzed Vegetable Protein Market: Global Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Metric Tons) (2026-2034)

5.1. Hydrolyzed Vegetable Protein Market Size and Forecast, by Form (2026-2034)

5.1.1. Chunks

5.1.2. Slice

5.1.3. Flakes

5.1.4. Granules

5.2. Hydrolyzed Vegetable Protein Market Size and Forecast, by Product Type (2026-2034)

5.2.1. Soy Protein

5.2.2. Wheat Protein

5.2.3. Pea Protein

5.2.4. Rice Protein

5.2.5. Chia Protein

5.2.6. Flax Protein

5.2.7. Corn Protein

5.3. Hydrolyzed Vegetable Protein Market Size and Forecast, by Distribution Channel (2026-2034)

5.3.1. Online Channels

5.3.2. Offline Channels

5.4. Hydrolyzed Vegetable Protein Market Size and Forecast, by End User (2026-2034)

5.4.1. Food and Beverages

5.4.2. Cosmetics and Personal Care

5.4.3. Pharmaceuticals

5.4.4. Others

5.5. Hydrolyzed Vegetable Protein Market Size and Forecast, by Region (2026-2034)

5.5.1. North America

5.5.2. Europe

5.5.3. Asia Pacific

5.5.4. Middle East and Africa

5.5.5. South America

6. North America Hydrolyzed Vegetable Protein Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Metric Tons) (2026-2034)

6.1. North America Hydrolyzed Vegetable Protein Market Size and Forecast, by Form (2026-2034)

6.1.1. Chunks

6.1.2. Slice

6.1.3. Flakes

6.1.4. Granules

6.2. North America Hydrolyzed Vegetable Protein Market Size and Forecast, by Product Type (2026-2034)

6.2.1. Soy Protein

6.2.2. Wheat Protein

6.2.3. Pea Protein

6.2.4. Rice Protein

6.2.5. Chia Protein

6.2.6. Flax Protein

6.2.7. Corn Protein

6.3. North America Hydrolyzed Vegetable Protein Market Size and Forecast, by Distribution Channel (2026-2034)

6.3.1. Online Channels

6.3.2. Offline Channels

6.4. North America Hydrolyzed Vegetable Protein Market Size and Forecast, by End User (2026-2034)

6.4.1. Food and Beverages

6.4.2. Cosmetics and Personal Care

6.4.3. Pharmaceuticals

6.4.4. Others

6.5. North America Hydrolyzed Vegetable Protein Market Size and Forecast, by Country (2026-2034)

6.5.1. United States

6.5.2. Canada

6.5.3. Mexico

7. Europe Hydrolyzed Vegetable Protein Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Metric Tons) (2026-2034)

7.1. Europe Hydrolyzed Vegetable Protein Market Size and Forecast, by Form (2026-2034)

7.2. Europe Hydrolyzed Vegetable Protein Market Size and Forecast, by Product Type (2026-2034)

7.3. Europe Hydrolyzed Vegetable Protein Market Size and Forecast, by Distribution Channel (2026-2034)

7.4. Europe Hydrolyzed Vegetable Protein Market Size and Forecast, by End User (2026-2034)

7.5. Europe Hydrolyzed Vegetable Protein Market Size and Forecast, by Country (2026-2034)

7.5.1. United Kingdom

7.5.2. France

7.5.3. Germany

7.5.4. Italy

7.5.5. Spain

7.5.6. Sweden

7.5.7. Austria

7.5.8. Rest of Europe

8. Asia Pacific Hydrolyzed Vegetable Protein Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Metric Tons) (2026-2034)

8.1. Asia Pacific Hydrolyzed Vegetable Protein Market Size and Forecast, by Form (2026-2034)

8.2. Asia Pacific Hydrolyzed Vegetable Protein Market Size and Forecast, by Product Type (2026-2034)

8.3. Asia Pacific Hydrolyzed Vegetable Protein Market Size and Forecast, by Distribution Channel (2026-2034)

8.4. Asia Pacific Hydrolyzed Vegetable Protein Market Size and Forecast, by End User (2026-2034)

8.5. Asia Pacific Hydrolyzed Vegetable Protein Market Size and Forecast, by Country (2026-2034)

8.5.1. China

8.5.2. S Korea

8.5.3. Japan

8.5.4. India

8.5.5. Australia

8.5.6. ASEAN

8.5.7. Rest of Asia Pacific

9. Middle East and Africa Hydrolyzed Vegetable Protein Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Metric Tons) (2026-2034)

9.1. Middle East and Africa Hydrolyzed Vegetable Protein Market Size and Forecast, by Form (2026-2034)

9.2. Middle East and Africa Hydrolyzed Vegetable Protein Market Size and Forecast, by Product Type (2026-2034)

9.3. Middle East and Africa Hydrolyzed Vegetable Protein Market Size and Forecast, by Distribution Channel (2026-2034)

9.4. Middle East and Africa Hydrolyzed Vegetable Protein Market Size and Forecast, by End User (2026-2034)

9.5. Middle East and Africa Hydrolyzed Vegetable Protein Market Size and Forecast, by Country (2026-2034)

9.5.1. South Africa

9.5.2. GCC

9.5.3. Egypt

9.5.4. Nigeria

9.5.5. Rest of ME&A

10. South America Hydrolyzed Vegetable Protein Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Metric Tons) (2026-2034)

10.1. South America Hydrolyzed Vegetable Protein Market Size and Forecast, by Form (2026-2034)

10.2. South America Hydrolyzed Vegetable Protein Market Size and Forecast, by Product Type (2026-2034)

10.3. South America Hydrolyzed Vegetable Protein Market Size and Forecast, by Distribution Channel (2026-2034)

10.4. South America Hydrolyzed Vegetable Protein Market Size and Forecast, by End User (2026-2034)

10.5. South America Hydrolyzed Vegetable Protein Market Size and Forecast, by Country (2026-2034)

10.5.1. Brazil

10.5.2. Argentina

10.5.3. Rest Of South America

11. Company Profile: Key Players

11.1. Archer Daniels Midland Company (Illinois, USA)

11.1.1. Company Overview

11.1.2. Product Portfolio

11.1.2.1. Product Name

11.1.2.2. Product Details (Price, Features, etc.)

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Cargill, Incorporated (Minnesota, USA)

11.3. DowDuPont Inc. (Michigan, USA)

11.4. CHS Inc. (Minnesota, USA)

11.5. Ingredion Incorporated (Illinois, USA)

11.6. Kemin Industries, Inc. (Iowa, USA)

11.7. Brolite Products Co., Inc. (Illinois, USA)

11.8. MGP Ingredients, Inc. (Kansas, USA)

11.9. NutriBiotic (California, USA)

11.10. Brolite Products Co., Inc. (Illinois, USA)

11.11. MGP Ingredients, Inc. (Kansas, USA)

11.12. NutriBiotic (California, USA)

11.13. Gold Coast Ingredients, Inc. (California, USA)

11.14. Kerry Group (County Kerry, Ireland)

11.15. Tate & Lyle PLC (London, United Kingdom)

11.16. Roquette Frères (Lestrem, France)

11.17. Givaudan SA (Vernier, Switzerland)

11.18. Diana Group (Vannes, France)

11.19. Meelunie B.V. (Amsterdam, Netherlands)

11.20. Fuerst Day Lawson Ltd. (London, United Kingdom)

11.21. Ajinomoto Co., Inc. (Tokyo, Japan)

11.22. Sonic Biochem Extraction Pvt. Ltd. (Ahmedabad, India)

11.23. Niran (Thailand) Co., Ltd. (Bangkok, Thailand)

12. Key Findings

13. Analyst Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook