Generic Drug Market: Regulatory Reform, Supply Security, and Market Access Dynamics (2026-2032)

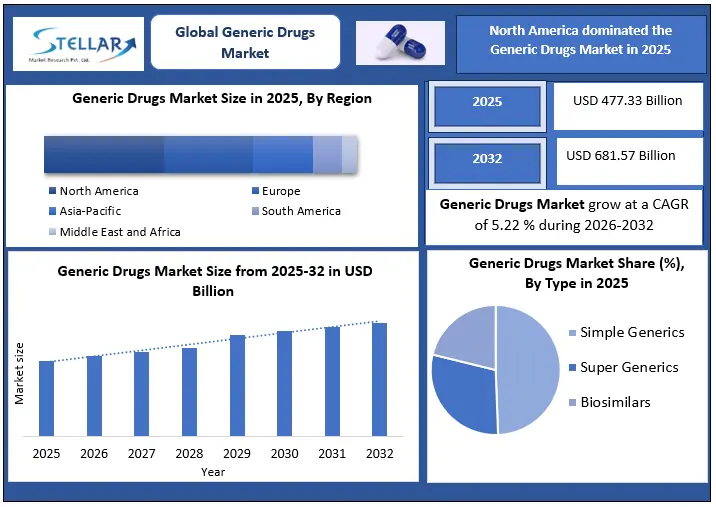

Generic Drug Market size was valued at USD 477.33 Bn. in 2025 and the total Global Generic Drug Market revenue is expected to grow at a CAGR of 5.22% from 2026 to 2032, reaching nearly USD 681.57 Bn. in 2032.

Generic Drug Market Overview:

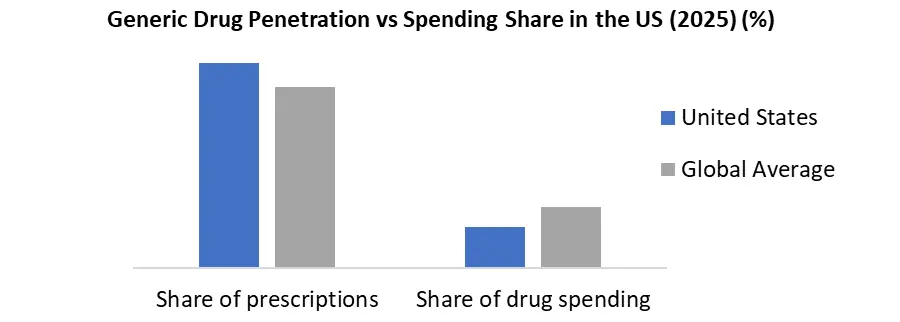

The Global Generic Drugs market plays a central role in ensuring access to essential medicines while containing healthcare expenditure across both developed and emerging economies. Generic medicines dominate prescription volumes worldwide, particularly in public healthcare systems where affordability and scale are critical. Generic Drug Market size was valued at USD 477.33 Bn. in 2025 and the total Global Generic Drug Market revenue is expected to grow at a CAGR of 5.22% from 2026 to 2032, reaching nearly USD 681.57 Bn. in 2032. In the United States, generics account for 90% of all prescriptions dispensed, yet represent only 18.6% of total drug spending, highlighting the structural cost efficiency embedded in the generic drug model. Government utilization data further confirms that over 78% of all drugs dispensed in the US are generic, underscoring their entrenched position in routine clinical practice.

Consumption data from Medicare reinforces this dominance. For drugs with available generic alternatives, the generic utilization rate reaches 94.4% under Medicare Part D, with over 1 billion generic prescription fills annually. In 2022 alone, 43.2 million Medicare Part D enrollees, representing 81.4% of total enrollees, filled at least one generic prescription. These figures demonstrate that generic medicines are no longer substitutes at the margin but form the backbone of pharmaceutical consumption, particularly for chronic disease management.

From a supply perspective, regulatory throughput remains a key indicator of market vitality. In FY 2024, the US FDA approved 694 Abbreviated New Drug Applications (ANDAs), reflecting sustained momentum in generic market entry. Importantly, 70 of these approvals were first-time generics, introducing competition into previously single-source markets and accelerating price erosion. The FDA also received 740 ANDA submissions, indicating a steady pipeline of future approvals and continued manufacturer interest despite pricing pressure.

To know about the Research Methodology :- Request Free Sample Report

Generic Drug Market Dynamics

Demand-Side and Economic Drivers

The primary driver of the generic drugs market remains cost containment. Price erosion following generic entry is both rapid and predictable. Evidence indicates that generic prices typically fall to around 32% of branded prices within three years of entry. Competitive intensity further amplifies this effect. Markets with two to three generic competitors experience approximately 50% price reductions, while markets with more than three competitors see price declines of 80–90% relative to originator products.

The economic impact of generics and biosimilars is measurable at the system level. Biosimilars alone have generated USD 56 billion in cumulative savings since 2015, including USD 20 billion in savings in 2024. In the first half of 2024, over 500,000 non-LIS Medicare enrollees saved USD 979 million, with an average saving of USD 1,800 per enrollee upon reaching the catastrophic coverage phase. These savings reinforce payer support for accelerated substitution and formulary preference for generics and biosimilars.

Regulatory Performance and Pipeline Health

Regulatory efficiency under the Generic Drug User Fee Amendments (GDUFA) framework continues to shape supply-side dynamics. In FY 2024, 122 ANDAs achieved first-cycle approval, representing 17% of total approvals, signalling improving submission quality and regulatory alignment. Approval timelines remain relatively stable, with median approval times of 25–29 months and mean approval times of 40–43 months, providing manufacturers with predictable development and commercialization planning horizons.

Complex generics are an increasingly important growth lever. In FY 2024, the FDA received 138 complex product applications, reflecting a strategic shift toward higher-barrier products such as injectables, drug-device combinations, and complex formulations. To support this evolution, the FDA issued 206 new Product-Specific Guidances (PSGs) during the year, including 109 related to complex products, bringing the cumulative total to 2,223 PSGs. This expanding guidance base materially lowers regulatory uncertainty and supports investment in technically challenging generics.

Generic Drug Market Regional Insights

North America remains the most consumption-intensive generic drugs market, driven by high prescription volumes and strong payer-led substitution. Regulatory engagement is extensive. In FY 2024, the FDA processed 85 Product Development Meeting requests, granting 99% within 14 days.

Followed by Europe which is characterized by high generic penetration but structurally lower pricing due to tender-based procurement and country-specific reimbursement systems. While volumes remain strong, profitability is constrained, pushing manufacturers to rationalize portfolios and focus on scale efficiencies and biosimilars. Asia-Pacific functions as both a manufacturing hub and a growing consumption market. India and China remain central to global supply, particularly for APIs and oral solid dosage forms. Export-oriented manufacturing dominates, supported by regulatory approvals in the US and Europe.

Generic Drug Market Segment Analysis

By type, simple generics account for the largest share of prescription volumes in 2025, while super generics and biosimilars contribute disproportionately to value growth due to higher development complexity and reduced competition. By brand, pure generics dominate public healthcare channels, whereas branded generics remain relevant in emerging markets, supported by physician prescribing behavior and private-sector demand.

Oral formulations remain the dominant route of administration due to scale manufacturing and lower regulatory complexity. However, injectables and biosimilars are gaining share, driven by oncology, hospital demand, and biologic patent expires. Therapeutically, cardiovascular, CNS, oncology, and respiratory segments represent the largest demand pools, closely aligned with aging populations and chronic disease prevalence.

Generic Drug Market Competitive Landscape

The global generic drugs market is moderately consolidated, with competition centered on scale, regulatory execution, and portfolio breadth. Leading players such as Teva Pharmaceutical Industries, Viatris, Sandoz Group, Sun Pharmaceutical Industries, Fresenius Kabi, Dr. Reddy’s Laboratories and Cipla operate across multiple geographies and dosage forms.

Regulatory compliance remains a key competitive differentiator. In FY 2024, the FDA conducted 773 inspections, including 570 foreign inspections, reflecting the globalized manufacturing footprint of the industry. A total of 462 Form 483 observations were issued, with a median of five days from inspection start to 483 issuance, underscoring the intensity of quality oversight. Median timelines from 483 issuance to warning letters and import alerts stood at 187 days and 159 days, respectively, reinforcing the operational and reputational risks associated with non-compliance.

Policy and Regulatory Framework – Key Recent Developments

- India scaled domestic API capacity through fiscal intervention, committing ?6,940 crore under the PLI scheme for bulk drugs, with 34 projects commissioned and ?4,253.92 crore in realized investments as of 2024, strengthening backward integration and export resilience.

- Generic penetration remains structurally high in the US, with generics accounting for 91% of prescriptions but only ~18% of drug spending, reinforcing continued payer and policy support for accelerated generic entry.

- US FDA approvals remain strong under GDUFA III, with 694 ANDAs approved in FY 2024, including 70 first-time generics, supported by expanded product-specific guidance for complex generics.

- China’s Volume-Based Procurement now covers 435 drugs, driving 50–70% average price reductions and reshaping domestic generic pricing benchmarks across essential therapy areas.

- Supply security has emerged as a policy priority across developed markets, reflected in initiatives such as FDA’s Advanced Manufacturing Technologies designation and EU-level discussions on regionalized drug production.

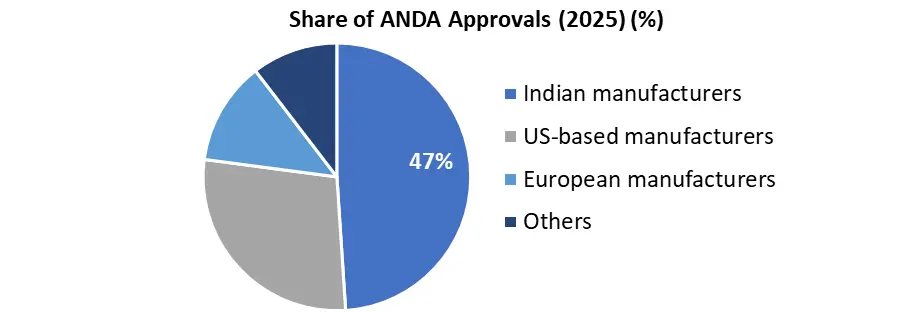

- India continues to anchor global generic supply, accounting for ~20% of global generic volumes, including 40% of generics consumed in the US, underscoring its strategic role in global healthcare affordability.

|

Global Generic Drugs Market |

|||

|

Report Coverage |

Details |

||

|

Base Year: |

2025 |

Forecast Period: |

2026-2032 |

|

Historical Data: |

2020 to 2025 |

Market Size in 2025: |

USD 477.33 Billion |

|

Forecast Period 2026 to 2032 CAGR: |

5.22 % |

Market Size in 2032: |

USD 681.57 Billion |

|

Generic Drugs Market Segment Analysis |

By Type |

Simple Generics Super Generics Biosimilars |

|

|

By Brand |

Pure Generic Drugs Branded Generic Drugs |

||

|

By Route of Administration |

Oral Injection Cutaneous Others |

||

|

By Application |

Central Nervous System (CNS) Cardiovascular Dermatology Oncology Respiratory Others |

||

|

|

By Distribution Channel |

Hospitals Pharmacies Private Clinics Drug Stores Others |

|

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Russia, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Thailand, Vietnam, Philippines, and Rest of APAC)

Middle East and Africa (South Africa, GCC, Nigeria, Egypt, Turkey, and Rest of ME&A)

South America (Brazil, Argentina, Colombia, Chile, Peru, and the Rest of South America)

Generic Drug Market Key Players/Competitors Analysis

- Teva Pharmaceutical Industries Ltd.

- Viatris

- Sandoz Group AG

- Sun Pharmaceutical Industries Ltd.

- Fresenius Kabi

- Dr. Reddy’s Laboratories Ltd

- Cipla Ltd.

- Aurobindo Pharma Ltd.

- Lupin Ltd.

- Apotex Inc.

- Hikma Pharmaceuticals plc

- Stada Arzneimittel AG

- Alvogen

- Amneal Pharmaceuticals LLC

- Glenmark Pharmaceuticals Ltd.

- Torrent Pharmaceuticals Ltd.

- Nichii-Iko Pharmaceutical Co., Ltd.

- Krka d.d.

- Eurofarma Laboratórios S.A.

- Medochemie Ltd.

- Panacea Biotec

- Pharmaniaga Berhad

- Hovid Berhad

- Duopharma Biotech Berhad

- Sawai Pharmaceutical Co., Ltd.

Frequently Asked Questions

There are 2 major types of brand modes in Generic Drug Market, namely; Pure Generics and Branded Generics.

Include Teva Pharmaceutical Industries Ltd., Novartis AG (Sandoz International), Viatris, Sun Pharma, Fresenius Kabi, Aurobindo Pharma, Mylan N.V., Pfizer Inc., Sanofi, Novel Understanding.

North America holds the largest market share in Generic Drug Market.

5.22% CAGR is the growth rate of the Generic Drug Market.

1. Global Generic Drugs Market: Research Methodology

2. Global Generic Drugs Market Introduction

2.1. Market Size (2025) & Forecast (2026-2032)

2.2. Market Size (USD) and Market Share (%) - By Segments, Regions and Country

2.3. Executive Summary

3. Global Generic Drugs Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Competitive Landscape

3.3. Key Players Benchmarking

3.3.1. Company Name

3.3.2. Product Portfolio

3.3.3. Market Share (%)

3.3.4. Revenue (2025)

3.3.5. R&D Investment

3.3.6. Revenue Growth Rate (%)

3.3.7. Geographical Presence

3.4. Market Structure

3.4.1. Market Leaders

3.4.2. Market Followers

3.4.3. Emerging Players

3.5. Mergers and Acquisitions Details

3.6. Recent Developments

3.7. Market Positioning & Share Analysis

3.7.1. Company Revenue, Generic Drugs Revenue, and Market Share (%)

3.7.2. SMR Competitive Positioning

3.8. Strategic Developments & Partnerships

4. Generic Drugs Market: Dynamics

4.1. Generic Drugs Market Trends

4.2. Generic Drugs Market Dynamics

4.2.1. Drivers

4.2.2. Restraints

4.2.3. Challenges

4.2.4. Opportunities

4.3. PORTER’s Five Forces Analysis

4.4. PESTLE Analysis

5. Global Generic Drugs Demand Analysis

5.1. Historical and current Demand volume by formulation type (2020-2025)

5.2. Consumption value split by therapeutic class

5.3. Per-capita generic drug consumption by key countries

5.4. Branded vs unbranded generics penetration across mature and emerging markets

5.5. Demand outlook under patent expiry and pricing pressure scenarios

6. Global Generic Drugs Production Analysis (2025)

6.1. Global production volume and capacity by dosage form

6.2. Production split by geography (India, China, US, EU, RoW)

6.3. API vs finished dosage formulation production balance

6.4. Capacity utilization trends and brownfield vs greenfield expansion

6.5. Key production hubs and manufacturing concentration analysis

7. Consumer & Patient Demographics

7.1. Age-wise consumption trends and chronic disease linkage

7.2. Income and insurance coverage impact on generic uptake

7.3. Urban vs rural prescription behavior

7.4. Physician substitution behavior and pharmacist-led switching

7.5. Public healthcare vs private channel consumption split

8. Generic Drugs Import–Export & Trade Flow Analysis (2025)

8.1. Global generic drug trade value and volume flows

8.2. Major exporting countries and key destination markets

8.3. API trade dependency and exposure risks

8.4. Trade barriers, tariffs, and regulatory bottlenecks

8.5. Supply security and reshoring impact assessment

9. Generic Drugs Market Supply Chain & Distribution Structure

9.1. End-to-end supply chain mapping from API to patient

9.2. Contract manufacturing and outsourcing penetration

9.3. Wholesaler, distributor, and pharmacy channel dynamics

9.4. Supply disruptions, shortages, and resilience strategies

9.5. Cold-chain and injectable-specific supply challenges

10. Generic Drugs Market Patent Landscape & Exclusivity Analysis

10.1. Key patent expiries shaping the generics opportunity pipeline

10.2. Paragraph IV filings and litigation trends

10.3. First-to-file exclusivity impact on pricing

10.4. Biosimilar vs small-molecule patent complexity

10.5. Geographic variation in patent enforcement strength

11. Generic Drugs Market Technology & Manufacturing Advancements

11.1. Process optimization and cost-reduction technologies

11.2. Continuous manufacturing and automation adoption

11.3. Complex generics and drug-device combinations

11.4. Quality compliance, data integrity, and digital QA systems

11.5. Technology as a competitive differentiator

12. Generic Drugs Market Investment & Strategic Activity

12.1. Capacity expansion and capex trends by region

12.2. M&A, divestments, and portfolio rationalization

12.3. Private equity participation in generics platforms

12.4. API backward integration strategies

12.5. ROI risk assessment under pricing erosion

13. Generic Drugs Market Policy & Regulatory Framework

13.1. Generic approval pathways by major regulators

13.2. Pricing controls, tender systems, and reimbursement models

13.3. GMP compliance trends and regulatory warning patterns

13.4. Localization policies and domestic manufacturing incentives

13.5. Regulatory risk mapping by geography

14. Epidemiology-Driven Demand Assessment

14.1. Disease prevalence trends driving generic demand

14.2. Chronic vs acute therapy demand mapping

14.3. Aging population impact on prescription volumes

14.4. Epidemiology-based forecasting assumptions

14.5. Sensitivity analysis linking disease burden to market size

15. Global Generic Drugs Market: Size and Forecast by Segmentation (By Value USD Billion and Volume 000’Units) (2025-2032)

15.1. Global Generic Drugs Market Size and Forecast, By Type

15.1.1. Simple Generics

15.1.2. Super Generics

15.1.3. Biosimilars

15.2. Global Generic Drugs Market Size and Forecast, By Brand

15.2.1. Pure Generic Drugs

15.2.2. Branded Generic Drugs

15.3. Global Generic Drugs Market Size and Forecast, By Route of Administration

15.3.1. Oral

15.3.2. Injection

15.3.3. Cutaneous

15.3.4. Others

15.4. Global Generic Drugs Market Size and Forecast, By Application

15.4.1. Central Nervous System (CNS)

15.4.2. Cardiovascular

15.4.3. Dermatology

15.4.4. Oncology

15.4.5. Respiratory

15.4.6. Others

15.5. Global Generic Drugs Market Size and Forecast, By Distribution Channel

15.5.1. Hospitals

15.5.2. Pharmacies

15.5.3. Private Clinics

15.5.4. Drug Stores

15.5.5. Others

15.6. Global Generic Drugs Market Size and Forecast, By Region

15.6.1. North America

15.6.2. Europe

15.6.3. Asia Pacific

15.6.4. Middle East and Africa

15.6.5. South America

16. North America Generic Drugs Market Size and Forecast By Segmentation (By Value USD Billion and Volume 000’Units) (2025-2032)

16.1. North America Market Size and Forecast, By Type

16.2. North America Market Size and Forecast, By Brand

16.3. North America Market Size and Forecast, By Route of Administration

16.4. North America Market Size and Forecast, By Application

16.5. North America Market Size and Forecast, By Distribution Channel

16.6. North America Market Size and Forecast, By Country

16.6.1. United States

16.6.2. Canada

16.6.3. Mexico

17. Europe Generic Drugs Market Size and Forecast By Segmentation (By Value USD Billion and Volume 000’Units) (2025-2032)

17.1. Europe Market Size and Forecast, By Type

17.2. Europe Market Size and Forecast, By Brand

17.3. Europe Market Size and Forecast, By Route of Administration

17.4. Europe Market Size and Forecast, By Application

17.5. Europe Market Size and Forecast, By Distribution Channel

17.6. Europe Market Size and Forecast, By Country

17.6.1. United Kingdom

17.6.2. France

17.6.3. Germany

17.6.4. Italy

17.6.5. Spain

17.6.6. Sweden

17.6.7. Russia

17.6.8. Rest of Europe

18. Asia Pacific Generic Drugs Market Size and Forecast by Segmentation (By Value USD Billion and Volume 000’Units) (2025-2032)

18.1. Asia Pacific Market Size and Forecast, By Type

18.2. Asia Pacific Market Size and Forecast, By Brand

18.3. Asia Pacific Market Size and Forecast, By Route of Administration

18.4. Asia Pacific Market Size and Forecast, By Application

18.5. Asia Pacific Market Size and Forecast, By Distribution Channel

18.6. Asia Pacific Market Size and Forecast, By Country

18.6.1. China

18.6.2. Japan

18.6.3. South Korea

18.6.4. India

18.6.5. Australia

18.6.6. Malaysia

18.6.7. Thailand

18.6.8. Vietnam

18.6.9. Indonesia

18.6.10. Philippines

18.6.11. Rest of Asia Pacific

19. Middle East and Africa Generic Drugs Market Size and Forecast By Segmentation (By Value USD Billion and Volume 000’Units) (2025-2032)

19.1. Middle East and Africa Market Size and Forecast, By Type

19.2. Middle East and Africa Market Size and Forecast, By Brand

19.3. Middle East and Africa Market Size and Forecast, By Route of Administration

19.4. Middle East and Africa Market Size and Forecast, By Application

19.5. Middle East and Africa Market Size and Forecast, By Distribution Channel

19.6. Middle East and Africa Market Size and Forecast, By Country

19.6.1. South Africa

19.6.2. GCC

19.6.3. Nigeria

19.6.4. Egypt

19.6.5. Turkey

19.6.6. Rest of ME&A

20. South America Generic Drugs Market Size and Forecast By Segmentation (By Value USD Billion and Volume 000’Units) (2025-2032)

20.1. South America Market Size and Forecast, By Type

20.2. South America Market Size and Forecast, By Brand

20.3. South America Market Size and Forecast, By Finish

20.4. South America Market Size and Forecast, By Application

20.5. South America Market Size and Forecast, By Distribution Channel

20.6. South America Market Size and Forecast, By Country

20.6.1. Brazil

20.6.2. Argentina

20.6.3. Colombia

20.6.4. Chile

20.6.5. Rest Of South America

21. Company Profile: Key Players

21.1. Teva Pharmaceutical Industries Ltd.

21.1.1. Company Overview

21.1.2. Business Portfolio

21.1.3. Financial Overview

21.1.4. SWOT Analysis

21.1.5. Strategic Analysis

21.1.6. Recent Developments

21.2. Viatris

21.3. Sandoz Group AG

21.4. Sun Pharmaceutical Industries Ltd.

21.5. Fresenius Kabi

21.6. Dr. Reddy’s Laboratories Ltd

21.7. Cipla Ltd.

21.8. Aurobindo Pharma Ltd.

21.9. Lupin Ltd.

21.10. Apotex Inc.

21.11. Hikma Pharmaceuticals plc

21.12. Stada Arzneimittel AG

21.13. Alvogen

21.14. Amneal Pharmaceuticals LLC

21.15. Glenmark Pharmaceuticals Ltd.

21.16. Torrent Pharmaceuticals Ltd.

21.17. Nichii-Iko Pharmaceutical Co., Ltd.

21.18. Krka d.d.

21.19. Eurofarma Laboratórios S.A.

21.20. Medochemie Ltd.

21.21. Panacea Biotec

21.22. Pharmaniaga Berhad

21.23. Hovid Berhad

21.24. Duopharma Biotech Berhad

21.25. Sawai Pharmaceutical Co., Ltd.

22. Key Findings

23. Industry Recommendations