Dry White Wine Market Global Industry Analysis and Forecast (2026-2032)

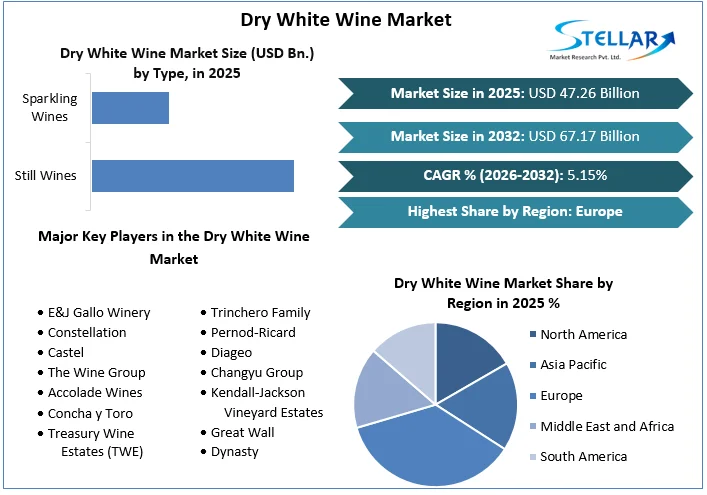

The Global Dry White Wine Market size reached US$ 47.26 Billion in 2025 and expects the market to reach US$ 67.17 Billion by 2032, exhibiting a growth rate (CAGR) of 5.15% during 2026-2032.

Dry White Wine Market Overview:

Dry white wine is a type of wine that has very little residual sugar, which means it's not sweet. The term "dry" in the context of wine refers to the absence of sweetness, as opposed to wines that are sweet or off-dry (slightly sweet). Dry white wines are typically made from white grape varieties and are popular for their crispness, acidity, and versatility in pairing with various types of foods.

The Dry White Wine Industry is expected to be driven by the huge demand for dry white wine made from grapes in Western countries. During the anticipated period, the market's expansion will be driven by the rising use of dry white wine for cooking. White wine may be produced through the fermentation of grape pulp in white wine brews. Wine may have a lower risk of cardiovascular disease because the polyphenols in wine assist blood vessels produce more nitric oxide, according to one theory. Antioxidants found in dry white wine help strengthen the immune system. Because alcohol kills the "good" bacteria in the body, drinking too much wine can trigger a yeast infection.

The increasing consumption of wine in the U.S. and European countries like France, Italy, Germany, the UK, and Spain shows how popular wine is in Western countries. Online retailers sell Italian dry white wines like Abbazia di Novacella 2020 Kerner and Alto Adige Italy for $19.99. Two excellent wines that are favorites of many home cooks are Still wines and Chardonnay. The outlook for the dry white wine industry is shown here.

To get more Insights: Request Free Sample Report

Dry White Wine Market Dynamics:

Increasing dry white wine production in the new market of developing countries

Consumers' tastes and preferences have been shifting towards lighter, crisper, and drier wines. Dry white wines tend to be less sweet and offer a broader range of flavors, appealing to a growing segment of wine drinkers who prefer less sweetness in their beverages.

Dry white wines are often perceived as healthier due to their lower sugar content than sweeter wines. This health-conscious trend has contributed to the demand for drier wine varieties. Wineries and wine distributors have been actively marketing and educating consumers about the nuances of different wine styles, including the characteristics of dry white wines. This has helped create awareness and demand for such wines.

The characteristics of grapes used to make wine are influenced by the climate and terroir (soil, topography, climate) of the region where they are grown. Some regions are known for producing high-quality dry white wines, attracting consumers looking for specific flavor profiles.

Dry White Wine Market Restraints:

Excessive Intake of White Wine Resulting in Liver Ailment and Other Issues

Numerous alcoholic and non-alcoholic beverages compete with wine in the market. The demand for dry white wine may change due to changes in consumer trends and preferences. The laws governing the manufacture, sale, labeling, and promotion of alcoholic beverages can differ significantly between different nations and areas. Wine growers and distributors may face difficulties adhering to these regulations.

The availability of raw commodities, such as grapes, as well as packaging materials, might be impacted by supply chain interruptions. Wine production and distribution may be hampered by unforeseen circumstances such as bad weather, disease outbreaks, or transportation problems.

Regions that cultivate grapes may be affected by climate patterns, which may impact the quality and quantity of grape harvests. Extreme weather conditions, including heat waves or unexpected frosts, can harm grapevines and have an impact on wine output.

Dry White Wine Market Opportunities:

Dry white wines and other beverages with reduced alcohol and calorie content are becoming more and more popular

As customers become more health concerned. Wineries that can make wines with an emphasis on health benefits and clarity in labeling may draw customers who are concerned about their health.

Wines made utilizing sustainable and organic methods are becoming more and more popular as customers' knowledge of the environment grows. Wineries that use environmentally friendly production techniques and highlight their dedication to sustainability may stand out in the marketplace.

The wine sector has also benefited from the rise of online commerce. Wineries that make an investment in e-commerce systems that are easy to use and allow direct-to-consumer sales can reach a wider audience outside of their local markets.

Dry White Wine Market Challenges:

Getting products to consumers can be challenging

The wine industry is subject to various regulations, both domestically and internationally. Navigating these regulations, such as labeling requirements and import/export restrictions, can be complex and time-consuming. Counterfeit wine can damage a brand's reputation and erode consumer trust. Ensuring the authenticity of products is a significant concern for high-end wine producers.

Getting products to consumers can be challenging due to distribution logistics and retailer partnerships. Building relationships with distributors, retailers, and restaurants is crucial for expanding market reach.

Dry White Wine Market Trends:

Modern Trade Shows a Strong Preference for Semi-Sweet Flavors in White Wine Sales.

Throughout the whole projected period, modern trade stores will be the primary sales channel for white wine in the global market. If they capture more than a third of global revenues, producers will move the majority of their goods to modern commerce channels. Due to white wines' adaptability in meeting all winetasting criteria, consumers should be prepared to see more of them in innovative food and beverage products. White wine producers still struggle with issues like challenging storage temperatures and a lack of health benefits associated with its consumption, therefore it's expected that the global market for this beverage won't grow particularly quickly.

Western countries are in great demand

Market growth is anticipated over the projected period due to rising demand for dry white wine in both established and developing nations. The industry is also growing due to the abundance of raw resources, well-trained labor forces, technological advancements, booming R&D activities, and product developments. As a result of global technological improvements, the dry white wine market is anticipated to provide a wide range of opportunities. Dry white wine producers are having trouble making ends meet due to rising production expenses, which directly affects the wine's elegance.

Dry White Wine Market Regional Insights:

The market under study is made up of the following regions: North America, Europe, South America, Asia Pacific, the Middle East, and Africa. The world's largest wine market was found to be in Europe, with a 31.7% sales share in 2025.

Europe today holds a dominant position in the organic wine market as a result of the region's strong and established winemaking industry. Due to the region's expanding organic wine consumer base.

North America is also anticipated to experience growth during the projected period. The United States and Canada were important markets for dry white wine. In the US, regions like California, Oregon, and Washington were known for producing high-quality white wines, such as Chardonnay and Still wines. The increasing popularity of food and wine pairings, along with a growing interest in wine culture, contributed to the demand for dry white wines in North America.

The Asia Pacific region, particularly China and Japan, was experiencing a rise in wine consumption, including dry white wines. As economies were growing and middle-class populations were expanding, there was an increasing interest in Western wines, often seen as symbols of sophistication and luxury. Australia and New Zealand were notable exporters of dry white wines to this region.

Dry White Wine Market Segment Analysis:

By Type: The Dry White Wine Market can be divided into Still Wines and Sparkling Wines based on type. In 2025, the segment that accounted for the highest share of the dry white wine market was sparkling wines. The popularity of sparkling wines, which have high quantities of carbon dioxide and are made fizzy and enjoyable by a natural fermentation process, is what is fueling this increase. Sparkling wines are made from both red and white grapes, and when drank in moderation, they may be good for cardiovascular health. The sparkling wine market is expanding as a result of sparkling Reisling's increasing popularity. Additionally, it is anticipated that the market of sparkling wines would expand at the quickest CAGR of 4.3% from 2026 to 2032.

Based on the Application, the Dry White Wine Market may be further divided into households and commercials. In 2025, the Dry White Wine market's highest market share belonged to the Households segment. Due to its acidity in dishes like risotto in Western countries, dry white wine is increasingly being used in cooking, which has led to this growth. For those with yeast infections, dry white wine is not advised. The consumption of dry white wine as a meal complement is rising, which is helping this market segment grow. Additionally, due to the rapidly expanding use of dry white wine in commercial settings, the Commercial category is anticipated to rise at the quickest CAGR of 4.5% during the projection period of 2025–2032.

Dry White Wine Market Competitive Landscape:

The major companies are currently focusing on putting strategies into practice, such as adopting new technology, product developments, collaborations, mergers & acquisitions, joint ventures, alliances, and partnerships, to increase their market positions in the international organic wine sector.

In 2025, Tamburlaine Organic Wines acquired Cumulus Winery, a renowned premium winemaking facility known for its expertise in producing wines from oranges. Tamburlaine disclosed the acquisition to promote Oranges' reputation for producing organic wines. These purchases are made with the intention of growing the company's market share and revenue.

|

Dry White Wine Market Scope |

|

|

Market Size in 2025 |

USD 47.26 billion. |

|

Market Size in 2032 |

USD 67.17 billion. |

|

CAGR (2026-2032) |

5.15% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segment Scope |

By Type:

|

|

By Application

|

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Dry White Wine Market Key Players:

- E&J Gallo Winery

- Constellation

- Castel

- The Wine Group

- Accolade Wines

- Concha y Toro

- Treasury Wine Estates (TWE)

- Trinchero Family

- Pernod-Ricard

- Diageo

- Changyu Group

- Kendall-Jackson Vineyard Estates

- Great Wall

- Dynasty

Frequently Asked Questions

The major players in the dry white wine market include E&J Gallo, Constellation Brands, The Wine Group, Treasury Wine Estates, and Brown-Forman.

There are several opportunities in the dry white wine market, including increasing demand for premium wines, growing interest in organic and sustainable wines, and the rise of online wine sales.

Regions such as Asia Pacific, Europe, and North America are expected to see significant growth in the dry white wine market due to increasing consumer demand and expanding distribution channels.

The global dry white wine market is experiencing steady growth, with demand increasing due to rising affluence and changing consumer preferences.

1. Global Dry White Wine Market: Research Methodology

2. Global Dry White Wine Market: Executive Summary

3. Global Dry White Wine Market: Competitive Landscape

3.1. Stellar Competition Matrix

3.2. Competitive Landscape

3.3. Key Players Benchmarking

3.4. Market Structure

3.4.1. Market Leaders

3.4.2. Market Followers

3.4.3. Emerging Players

3.5. Consolidation of the Market

4. Global Dry White Wine Market: Dynamics

4.1. Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Market Drivers by Region

4.2.1. North America

4.2.2. Europe

4.2.3. Asia Pacific

4.2.4. Middle East and Africa

4.2.5. South America

4.3. Market Restraints

4.4. Market Opportunities

4.5. Market Challenges

4.6. PORTER’s Five Forces Analysis

4.7. PESTLE Analysis

4.8. Value Chain Analysis

4.9. Regulatory Landscape by Region

4.9.1. North America

4.9.2. Europe

4.9.3. Asia Pacific

4.9.4. Middle East and Africa

4.9.5. South America

5. Global Dry White Wine Market Size and Forecast by Segments (by Value USD and Volume Units)

5.1. Global Dry White Wine Market Size and Forecast, by Type (2025-2032)

5.1.1. Still wines

5.1.2. Sparkling wines

5.2. Global Dry White Wine Market Size and Forecast, by Application(2025-2032)

5.2.1. Household

5.2.2. Commercials

5.3. Global Dry White Wine Market Size and Forecast, by Region (2025-2032)

5.3.1. North America

5.3.2. Europe

5.3.3. Asia Pacific

5.3.4. Middle East and Africa

5.3.5. South America

6. North America Global Dry White Wine Market Size and Forecast (by Value USD and Volume Units)

6.1. North America Global Dry White Wine Market Size and Forecast, by Type (2025-2032)

6.1.1. Still wines

6.1.2. Sparkling wines

6.2. North America Global Dry White Wine Market Size and Forecast, by Application(2025-2032)

6.2.1. Household

6.2.2. Commercials

6.3. North America Global Dry White Wine Market Size and Forecast, by Country (2025-2032)

6.3.1. United States

6.3.2. Canada

6.3.3. Mexico

7. Europe Global Dry White Wine Market Size and Forecast (by Value USD and Volume Units)

7.1. Europe Global Dry White Wine Market Size and Forecast, by Type (2025-2032)

7.1.1. Still wines

7.1.2. Sparkling wines

7.2. Europe Global Dry White Wine Market Size and Forecast, by Application(2025-2032)

7.2.1. Household

7.2.2. Commercials

7.3. Europe Global Dry White Wine Market Size and Forecast, by Country (2025-2032)

7.3.1. UK

7.3.2. France

7.3.3. Germany

7.3.4. Italy

7.3.5. Spain

7.3.6. Sweden

7.3.7. Austria

7.3.8. Rest of Europe

8. Asia Pacific Global Dry White Wine Market Size and Forecast (by Value USD and Volume Units)

8.1. Asia Pacific Global Dry White Wine Market Size and Forecast, by Type (2025-2032)

8.1.1. Still wines

8.1.2. Sparkling wines

8.2. Asia Pacific Global Dry White Wine Market Size and Forecast, by Application(2025-2032)

8.2.1. Household

8.2.2. Commercials

8.3. Asia Pacific Global Dry White Wine Market Size and Forecast, by Country (2025-2032)

8.3.1. China

8.3.2. S Korea

8.3.3. Japan

8.3.4. India

8.3.5. Australia

8.3.6. Indonesia

8.3.7. Malaysia

8.3.8. Vietnam

8.3.9. Taiwan

8.3.10. Bangladesh

8.3.11. Pakistan

8.3.12. Rest of Asia Pacific

9. Middle East and Africa Global Dry White Wine Market Size and Forecast (by Value USD and Volume Units)

9.1. Middle East and Africa Global Dry White Wine Market Size and Forecast, by Type (2025-2032)

9.1.1. Still wines

9.1.2. Sparkling wines

9.2. Middle East and Africa Global Dry White Wine Market Size and Forecast, by Application(2025-2032)

9.2.1. Household

9.2.2. Commercials

9.3. Middle East and Africa Global Dry White Wine Market Size and Forecast, by Country (2025-2032)

9.3.1. South Africa

9.3.2. GCC

9.3.3. Egypt

9.3.4. Nigeria

9.3.5. Rest of ME&A

10. South America Global Dry White Wine Market Size and Forecast (by Value USD and Volume Units)

10.1. South America Global Dry White Wine Market Size and Forecast, by Type (2025-2032)

10.1.1. Still wines

10.1.2. Sparkling wines

10.2. South America Global Dry White Wine Market Size and Forecast, by Application(2025-2032)

10.2.1. Household

10.2.2. Commercials

10.3. South America Global Dry White Wine Market Size and Forecast, by Country (2025-2032)

10.3.1. Brazil

10.3.2. Argentina

10.3.3. Rest of South America

11. Company Profile: Key players

11.1.1. E&J Gallo Winery

11.1.1. Company Overview

11.1.2. Financial Overview

11.1.3. Business Portfolio

11.1.4. SWOT Analysis

11.1.5 Business Strategy

11.1.6. Recent Developments

11.2. Constellation

11.3. Castel

11.4. The Wine Group

11.5. Accolade Wines

11.6. Concha y Toro

11.7. Treasury Wine Estates (TWE)

11.8. Trinchero Family

11.9. Pernod-Ricard

11.10. Diageo

11.11. Changyu Group

11.12. Kendall-Jackson Vineyard Estates

11.13. Great Wall

11.14. Dynasty

12. Key Findings

13. Industry Recommendation