Cheilectomy Market Global Industry Analysis and Forecast (2026-2032)

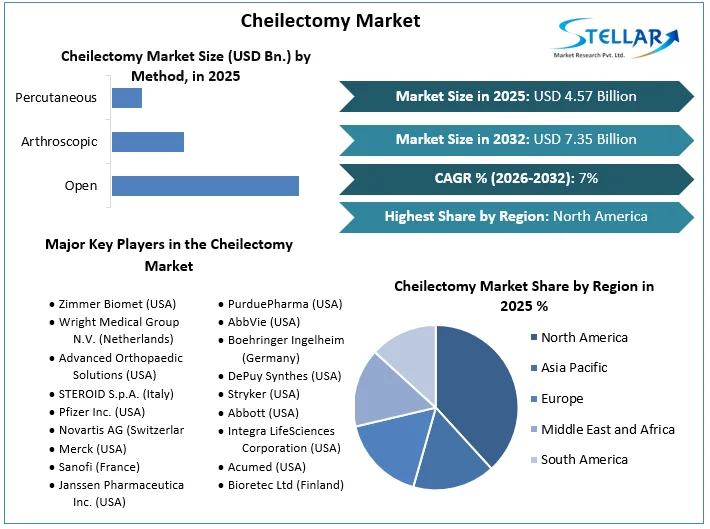

The Cheilectomy Market size was valued at USD 4.57 Bn. in 2025 and the total Cheilectomy Market size is expected to grow at a CAGR of 7% from 2026 to 2032, reaching nearly USD 7.35 Bn. by 2032.

Cheilectomy Market Overview

Cheilectomy is a surgical process used to treat hallux rigidus, a condition considered arthritis at the base of the big toe. The market dynamics of cheilectomy are influenced by rising incidence rates of hallux rigidus, as the population ages and lifestyles evolve. Advances in medical technology, such as less invasive procedures and sophisticated imaging methods, have led to decreased recovery time, enhanced patient satisfaction, and broader promotion of surgery. Improved awareness of cheilectomy and successful treatment devices drives market growth. Competency among medical device manufacturers, healthcare installations, and healthcare centers is a hallmark of the cheilectomy market.

Subsidies and coverage by private and public healthcare insurance define the market scope of cheilectomy. Patient factors and postoperative outcomes play a role in market dynamics, with surgeons and healthcare providers focusing on improving their methods. Hospitals, medical facilities, medical device manufacturers, and research organizations contribute to the development of more effective and resource-saving treatment methods. The global influence of market demography in cheilectomy is because of the imbalance in society caused by the aging population and migration to urban areas.

To get more Insights: Request Free Sample Report

Cheilectomy Market Dynamics:

The Cheilectomy market has experienced significant growth in recent years because of the increasing prevalence of osteoarthritis and other joint-related conditions. Cheilectomy, a surgical procedure for treating hallux rigidus, has become a popular choice for patients seeking relief from foot pain and limited joint mobility. The market growth is driven by the decreasing number of hallux rigidus cases, which are primarily because of infantilization and sedentary lifestyles.

Improvements in surgical methods, such as minimally invasive surgeries, precise technology, and better imaging machines, have improved the chances of success in the cheilectomy market. Also, increased awareness about foot conditions and aggressive patient education have contributed to the market's growth. The rise in global healthcare expenditures has also improved the performance of the Cheilectomy device industry, with patients spending on richly constructed and multi-functional treatments for a foot.

- Future developments in Cheilectomy procedures are expected as a result of ongoing research and development initiatives. The future course of the cheilectomy industry is expected to be shaped by the incorporation of technology like robotics and artificial intelligence into surgical procedures, which have an opportunity to improve surgical results and patient experiences.

The Cheilectomy Market faces several restraints influencing its dynamics. The Cheilectomy Market is inclined by regulatory inspection, technological advancements, competition from other treatments, reimbursement policies, economic conditions, demographic shifts, and healthcare spending trends. Clinical efficacy, security, and patient outcomes impact adoption rates, while educational initiatives increase awareness. Healthcare legislation and supply chain disruptions are two other factors that lead to market difficulties. By being aware of these limitations, stakeholders successfully traverse the market and make informed decisions, ensuring the success of cheilectomy treatments.

The aging population, particularly in industrialized regions, has led to a rise in foot challenges such as hallux rigidus. Cheilectomy is a viable orthopedic treatment that helps with the sales feat, as older adults are looking for ways to continue playing an active role in society. Even while the operations have made significant progress, the market of cheilectomy still faces several challenges, including difficulties with funding and a shortage of accessible healthcare in some developing countries. However, these challenges present opportunities for market players to advance and develop strategies that help in resolving issues and growing their market share.

Cheilectomy Market Segment Analysis:

Based on Method, The Arthroscopy segment is dominated in 2025, the pronounced "ahr-THROS-kuh-pee," is a technique used to identify and manage joint issues. A buttonhole-sized incision is made, and a tiny tube connected to a fiber-optic video camera is inserted by the surgeon. A high-definition video display receives the picture inside your joint. With arthroscopy, the doctor looks inside your joint without creating a big hole. During arthroscopy, surgeons even treat some forms of joint injury by inserting pencil-thin surgical tools through extra tiny incisions.

Based on End-user, Hospitals & clinics are partnered to demonstrate the importance of the hospital pharmacy in the Cheilectomy market. The growing initiatives aimed at improving access to healthcare energy the growing prevalence of Cheilectomy, the aging population, the growth of healthcare infrastructure, and the growing demand for Cheilectomy in hospitals. This, in turn, boosts the growth of the global market in Hospitals & clinics -based therapies for Cheilectomy during the forecast period.

Cheilectomy Market Regional Insight:

The North American Cheilectomy Market had a XX% market share in 2025. Because of their highly developed healthcare systems and rising rates of hallux rigidus, the Americas are the market leaders for cheilectomy procedures. Also, rising healthcare costs and the presence of major competitors in the regions support the market's growth in the Americas. The growing female population and aging population also contribute to the growth of the regional market. In the North American area, the market of Cheilectomy in the United States had the most market share, while the market in Canada was growing at the fastest rate.

Europe has the second-largest market of cheilectomy procedures. Osteoarthritis is a prevalent ailment that results in hallux rigidus. As a result, the disease's rising prevalence in the area drives market growth. The most prevalent orthopaedic disease among older adults in the UK according to Arthritis Research in the osteoarthritis XX% of people from the region were expected to have sought treatment for osteoarthritis.

Cheilectomy Market Competitive Landscape:

- May 21, 2024. Sanofi, Formation Bio, and OpenAI are collaborating to build AI-powered software to accelerate drug development and bring new medicines to patients more efficiently. The three teams bring together data, software, and tuning models to develop custom, purpose-built solutions across the drug development lifecycle. This represents the first collaboration of its kind within the pharma and life sciences industries. Sanofi is leveraging this partnership to provide access to proprietary data to develop AI models as it continues on its path to becoming the first biopharma company powered by AI at scale.

- In 2022, Stryker announced the acquisition of Trice Medical, a leading provider of minimally invasive orthopedic diagnostics, specifically for sports medicine. The acquisition allows Stryker to increase its product offerings and enhance its position in the growing market.

- March 11, 2024, Integra LifeSciences Launches MicroMatrix® Flex To Provide Convenient Access To Hard-To-Reach Areas In Complex Cases MicroMatrix® Flex is now available commercially in the U.S. MicroMatrix Flex is a dual-syringe system enabling the convenient mixing and precise delivery of MicroMatrix® paste to provide convenient access to hard-to-reach spaces and to help prepare an even wound surface in challenging wound areas.

|

Cheilectomy Market Scope |

|

|

Market Size in 2025 |

USD 4.57 Bn. |

|

Market Size in 2032 |

USD 7.35 Bn. |

|

CAGR (2026-2032) |

7 % |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segments |

By Method Open Arthroscopic Percutaneous |

|

By Anesthesia General anesthesia Local anesthesia Regional anesthesia |

|

|

By Medication Prescription pain relievers OCT Others |

|

|

By End-user Hospitals & clinics Academic institutes Retail pharmacies Others |

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Russia, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Player in the Cheilectomy Market

- Zimmer Biomet (USA)

- Wright Medical Group N.V. (Netherlands)

- Advanced Orthopaedic Solutions (USA)

- STEROID S.p.A. (Italy)

- Pfizer Inc. (USA)

- Novartis AG (Switzerland)

- Merck (USA)

- Sanofi (France)

- Janssen Pharmaceuticals Inc. (USA)

- PurduePharma (USA)

- AbbVie (USA)

- Boehringer Ingelheim (Germany)

- DePuy Synthes (USA)

- Stryker (USA)

- Abbott (USA)

- Integra LifeSciences Corporation (USA)

- Acumed (USA)

- Bioretec Ltd (Finland)

Frequently Asked Questions

North America is expected to lead the Cheilectomy Market during the forecast period.

An analysis of profit trends and projections for companies in the Cheilectomy Market is included, offering insights into factors driving profitability, cost management strategies, and financial performance metrics.

The Cheilectomy Market size was valued at USD 4.57 Billion in 2025 and the total Cheilectomy Market size is expected to grow at a CAGR of 7% from 2026 to 2032, reaching nearly USD 7.35 Billion by 2032.

The segments covered in the market report are by Method, by Anesthesia, by Medication, and by End-user.

1. Research Methodology

1.1 Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Research Assumption

2. Cheilectomy Market Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026 – 2032) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Global Cheilectomy Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Business Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

4. Cheilectomy Market: Dynamics

4.1. Cheilectomy Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Cheilectomy Market Drivers

4.3. Cheilectomy Market Restraints

4.4. Cheilectomy Market Opportunities

4.5. Cheilectomy Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factor

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Regulatory Landscape by Region

4.9.1. North America

4.9.2. Europe

4.9.3. Asia Pacific

4.9.4. Middle East and Africa

4.9.5. South America

5. Cheilectomy Market: Global Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

5.1. Cheilectomy Market Size and Forecast, by Method (2025-2032)

5.1.1. Open

5.1.2. Arthroscopic

5.1.3. Percutaneous

5.2. Cheilectomy Market Size and Forecast, by Anesthesia (2025-2032)

5.2.1. General anesthesia

5.2.2. Local anesthesia

5.2.3. Regional anesthesia

5.3. Cheilectomy Market Size and Forecast, by Medication (2025-2032)

5.3.1. Prescription pain relievers

5.3.2. OCT

5.3.3. Others

5.4. Cheilectomy Market Size and Forecast, by End User (2025-2032)

5.4.1. Hospitals & clinics

5.4.2. Academic Institutes

5.4.3. Retail pharmacies

5.4.4. Others

5.5. Cheilectomy Market Size and Forecast, by Region (2025-2032)

5.5.1. North America

5.5.2. Europe

5.5.3. Asia Pacific

5.5.4. Middle East and Africa

5.5.5. South America

6. North America Cheilectomy Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

6.1. North America Cheilectomy Market Size and Forecast, by Method (2025-2032)

6.1.1. Open

6.1.2. Arthroscopic

6.1.3. Percutaneous

6.2. North America Cheilectomy Market Size and Forecast, by Anesthesia (2025-2032)

6.2.1. General anesthesia

6.2.2. Local anesthesia

6.2.3. Regional anesthesia

6.3. North America Cheilectomy Market Size and Forecast, by Medication (2025-2032)

6.3.1. Prescription pain relievers

6.3.2. OCT

6.3.3. Others

6.4. North America Cheilectomy Market Size and Forecast, by End User (2025-2032)

6.4.1. Hospitals & clinics

6.4.2. Academic institutes

6.4.3. Retail pharmacies

6.4.4. Others

6.5. North America Cheilectomy Market Size and Forecast, by Country (2025-2032)

6.5.1. United States

6.5.2. Canada

6.5.3. Mexico

7. Europe Cheilectomy Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

7.1. Europe Cheilectomy Market Size and Forecast, by Method (2025-2032)

7.2. Europe Cheilectomy Market Size and Forecast, by Anesthesia (2025-2032)

7.3. Europe Cheilectomy Market Size and Forecast, by Medication (2025-2032)

7.4. Europe Cheilectomy Market Size and Forecast, by End User (2025-2032)

7.5. Europe Cheilectomy Market Size and Forecast, by Country (2025-2032)

7.5.1. United Kingdom

7.5.2. France

7.5.3. Germany

7.5.4. Italy

7.5.5. Spain

7.5.6. Sweden

7.5.7. Russia

7.5.8. Rest of Europe

8. Asia Pacific Cheilectomy Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

8.1. Asia Pacific Cheilectomy Market Size and Forecast, by Method (2025-2032)

8.2. Asia Pacific Cheilectomy Market Size and Forecast, by Anesthesia (2025-2032)

8.3. Asia Pacific Cheilectomy Market Size and Forecast, by Medication (2025-2032)

8.4. Asia Pacific Cheilectomy Market Size and Forecast, by End User (2025-2032)

8.5. Asia Pacific Cheilectomy Market Size and Forecast, by Country (2025-2032)

8.5.1. China

8.5.2. S Korea

8.5.3. Japan

8.5.4. India

8.5.5. Australia

8.5.6. ASEAN

8.5.7. Rest of Asia Pacific

9. Middle East and Africa Cheilectomy Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

9.1. Middle East and Africa Cheilectomy Market Size and Forecast, by Method (2025-2032)

9.2. Middle East and Africa Cheilectomy Market Size and Forecast, by Anesthesia (2025-2032)

9.3. Middle East and Africa Cheilectomy Market Size and Forecast, by Medication (2025-2032)

9.4. Middle East and Africa Cheilectomy Market Size and Forecast, by End User (2025-2032)

9.5. Middle East and Africa Cheilectomy Market Size and Forecast, by Country (2025-2032)

9.5.1. South Africa

9.5.2. GCC

9.5.3. Egypt

9.5.4. Rest of ME&A

10. South America Cheilectomy Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

10.1. South America Cheilectomy Market Size and Forecast, by Method (2025-2032)

10.2. South America Cheilectomy Market Size and Forecast, by Anesthesia (2025-2032)

10.3. South America Cheilectomy Market Size and Forecast, by Medication (2025-2032)

10.4. South America Cheilectomy Market Size and Forecast, by End User (2025-2032)

10.5. South America Cheilectomy Market Size and Forecast, by Country (2025-2032)

10.5.1. Brazil

10.5.2. Argentina

10.5.3. Rest Of South America

11. Company Profile: Key Players

11.1. Zimmer Biomet (USA)

11.1.1. Company Overview

11.1.2. Business Portfolio

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Wright Medical Group N.V. (Netherlands)

11.3. Advanced Orthopaedic Solutions (USA)

11.4. STEROID S.p.A. (Italy)

11.5. Pfizer Inc. (USA)

11.6. Novartis AG (Switzerland)

11.7. Merck (USA)

11.8. Sanofi (France)

11.9. Janssen Pharmaceuticals Inc. (USA)

11.10. PurduePharma (USA)

11.11. AbbVie (USA)

11.12. Boehringer Ingelheim (Germany)

11.13. DePuy Synthes (USA)

11.14. Stryker (USA)

11.15. Abbott (USA)

11.16. Integra LifeSciences Corporation (USA)

11.17. Acumed (USA)

11.18. Bioretec Ltd (Finland)

11.19. XX.inc

12. Key Findings

13. Analyst Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook