Marine Battery Market Global Industry Analysis and Forecast (2026-2032) By Ship Type, Battery Function, Nominal Capacity, Propulsion Type, Ship Power, Battery Design, Battery Type, Sales Channel, Energy Density, and Application

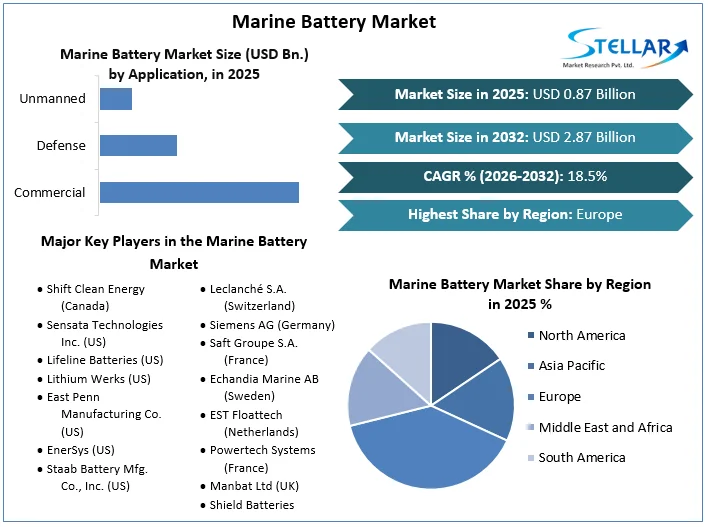

Global Marine Battery Market size was valued at USD 0.87 Bn. in 2025 and is expected to reach USD 2.87 Bn. by 2032, at a CAGR of 18.5%.

Marine Battery Market Overview

Marine batteries are specialized power storage devices engineered for marine applications such as boats and yachts. Designed to endure harsh aquatic conditions, including moisture, salinity, and constant motion, these batteries come in two primary types: starting batteries and deep-cycle batteries. Starting batteries provide a high current for short periods to start engines, while deep-cycle batteries offer consistent, long-term energy output for onboard appliances and systems. Marine batteries replace traditional lead-acid automotive batteries, featuring robust constructions with maintenance-free plate designs that minimize corrosion and fluid loss. They are crucial for ensuring safety and comfort during maritime activities, capable of withstanding brutal operating conditions such as vibration and high temperatures which increases their demand in the Marine Battery Market.

The growth of the marine battery market is driven by several factors, including the increase in global commercial trade and the rise of hybrid and fully electric marine vessels. Demand for advanced marine batteries with higher specific energy density and low operational costs is growing, essential for sustainable marine transportation and offering quick, hazard-proof rechargeable systems. Additionally, the increasing demand for marine freight transportation vessels and advancements in lithium-ion battery technology over lead-acid batteries, coupled with rising automation in marine transportation and growth in water sports and leisure activities, fuels the Marine Battery Market expansion.

However, the market faces challenges such as the limited range and capacity of fully electric ships and the maintenance and protection of batteries. Fully electric ships typically travel only about 80 kilometres on a single charge, presenting a significant limitation. Nonetheless, hybrid propulsion technology and alternative fuels like fuel cells present substantial potential for Marine Battery Market players, with smaller vessels such as ferries and cruise ships being particularly suited for hybrid propulsion.

Technological advancements in marine battery technology are pivotal, with the increasing adoption of alternative propulsion and power sources by commercial passenger vessels, leisure boat operators, ferry operators, and submarines. The push for cleaner sea transportation is driven by international regulations aimed at reducing harmful emissions from conventional fuel consumption. Future trends in the Marine Battery Market include the utilization of renewable energy sources in charging Marine Batteries; continuous developments in the hybrid power system, and prospects for sodium-ion batteries since sodium is more available all over the world compared to lithium-ion batteries.

Market leaders within the Marine Battery Market are diversifying to address requirements for new designs and technologies that promote the green marine industry. It is due to the market necessity for leisure boating and advances in eco-friendly technologies to cope with maritime emissions and global warming. In general, the advances in the development of materials, the growing tendency toward utilizing environmentally-friendly energy sources, as well as the governmental initiatives that promote diminishing the number of emissions, all create a favorable background for the further growth of interest in marine batteries.

To get more Insights: Request Free Sample Report

Marine Battery Market Trend

Implementation of IMO 2020 Sulphur Regulation to Boost Market Growth

Starting from January 2020, the International Maritime Organisation (IMO) has implemented a regulation on limiting the emission of sulfur oxide from ships, particularly in the Baltic Sea, North Sea, North America, and the US Caribbean Sea ECA. This regulation calls for a lowering of sulfur content in ship fuel from 3. 5% to 0. 5%, hitting the ship operators with the prospect of having to fit them with exhaust cleaning systems (scrubbers), or buy the very low sulfur fuel oil (VLSFO) or LNG-based fuel. This initiative responds to issues of environment and health that various governments and environmental organizations have expressed and is expected to drive the Marine Battery Market growth.

The regulation on sulfur emissions is deemed to have a huge impact on the demand for other Marine SC technologies such as marine batteries and hybrid or electric propulsion systems. These have vast Marine Battery Market prospects through the ability to cut emissions, fuel, and overall operational expenses. A study carried out by Drewry Shipping Consultants Ltd revealed that the cost of installing a scrubber on a ship falls between, USD 2 million to USD 6 million. VLCCs rely on about 60-70 metric tonnes of fuel daily; the cost variation is around USD 238. $ 5 per metric ton between HSFO and VLSFO. By July 2019, only 4% of vessels were equipped with scrubbers.

Battery-driven propulsion engines present a cost-effective alternative, potentially saving shipowners from high fuel costs and scrubber installations. Hybrid setups reduce annual fuel costs by 3–5%, while fully electric systems achieve savings of 80–100%. Additionally, electric propulsion systems lower maintenance costs by up to 50%. The implementation of the IMO 2020 Sulphur Regulation is set to propel the growth of the Marine Battery Market, encouraging the adoption of cleaner and more efficient marine propulsion technologies.

Marine Battery Market Dynamics

Driver: Growing Demand for Electric and Hybrid Vessels

The marine battery market has seen significant developments, driven by the increasing demand for electric and hybrid passenger vessels. A notable example is the introduction of 48V high-energy Li-ion marine batteries by Electric Fuel at the METSTRADE 2021 event. In Denmark, Siemens reported that out of 52 operational ferries, 39 could is converted to battery-driven/electric propulsion, aligning with Denmark's goal to become fossil-fuel-free by 2050. This electrification could cut operating and maintenance costs by USD 12 million annually and reduce fuel consumption from 19,000 tonnes to zero in the Marine Battery Market. However, the conversion requires an additional investment of approximately USD 1.4 million per ferry for batteries, port mooring system connections, and charging station infrastructure.

In January 2023, it defined Leclanché SA as the battery technology supplier for two hybrids for Stena RoRo and Brittany Ferries. Both battery systems have a storage capacity of 11. 3 MWh. Getting more specific, the RoPax, or roll-on/roll-off passenger, ships are the largest hybrid vessels globally. For instance, North America with American Marine Battery Market demand, and Europe with Norwegian Marine Battery Market demand have a big call for hybrid and fully electric vessels since governments are encouraging environmentally friendly water transportation. The purchasing costs of electric vessels are still less than diesel ones due to lower operation costs, and as a result, global demand for marine batteries is likely to increase.

Impact of Maritime Trade on Market Growth

Maritime trade, which accounts for about 90% of global trade according to the Maritime Supply Chain Optimization study, is a crucial driver for the marine battery market. The Asymmetric threat of COVID-19, the trade conflict between the US and China, and shifts in global political realignment continue to alter sea-borne trade adversely thereby forcing governments of the world towards seeking to diversify supply chain networks as well as harness new marine energy conversion systems. This change is expected to raise the demand for a multitude of vessels and the modernization of the existing fleet in the period between 2025 and 2032, as it will enhance the specifications related to marine batteries.

Rising Maritime Tourism and Infrastructure Needs

The demand for maritime tourism and the need for improved marine infrastructure and connectivity are significant growth drivers. These factors are expected to generate substantial revenues for countries relying on marine and coastal tourism. Governments are optimizing seaborne economy policies to promote eco-friendly marine tourism and enhance connectivity to various ports, which is projected to drive the Marine Battery Market growth from 2025 to 2032.

Increase in Marine Freight Transportation Vessels

Marine transportation is cheaper, especially for the transport of freights, and has in equal measure experienced more growth. International seaborne trade, for 2024 statistics, amounted to 10%. 7 billion tons, according to the United Nations Conference on Trade and Development (UNCTAD). According to the observation of the OECD, today sixty percent of all freight is moved through maritime ways, and by 2032 this figure will increase to seventy percent. This is a result of traffic congestion which is in trade lanes and especially in the Indian and Pacific Oceans.

There is also an upsurge of maritime freight transportation hence the need for vessels with enhanced marine batteries. Also, the world’s merchant fleet of vessels with 100 gross tonnes and over was about 99,800 vessels. All these vessels employ a marine battery for lighting, start-stop of the engine, and other purposes like accessories. Such a high demand for freight vessels with high–end battery systems will foster the marine battery market.

The marine battery market is driven by the growing demand for electric and hybrid vessels, the impact of maritime trade, rising maritime tourism, improved infrastructure needs, and increased demand for marine freight transportation. Significant examples include the introduction of new marine battery technologies, Denmark's push towards fossil-fuel-free operations, and the increasing number of hybrid vessels in Norway. The overall trend points towards a modernization of marine fleets and a shift towards more sustainable and cost-effective maritime operations, driving the demand for marine batteries.

Opportunity: Hybrid propulsion technology, currently suitable for small vessels like ferries and cruise ships, presents a significant opportunity for larger ships due to advancements in marine electric-propulsion technology and alternative fuels such as fuel cells in the Marine Battery Market.

- Case Study: Ferguson Marine (UK): The shipbuilder created the USD 14 million diesel-electric hybrid ferry, the Catriona, for CalMac, operating on Clyde and Hebridean routes. Catriona’s system combines diesel power with electric battery power, demonstrating the practical application of hybrid technology in marine transport.

- Research Insights: According to "A Smarter Journey," a report by Siemens and Bellona (Norway) published in June 2018, approximately 70% of Norway's 180-strong ferry fleet is converted to battery or hybrid propulsion, with 84% potential for all-electric conversion and 43% for hybrid technology.

- Innovative Partnership: In June 2019, Leclanché SA partnered with Comau (Italy), a leader in industrial automation, to build the world’s first automated manufacturing lines for lithium-ion battery modules for transport applications. This collaboration aims to produce energy storage solutions for e-transport and e-marine applications on an industrial scale, positioning Leclanché SA as a key provider in the electric and hybrid mass transport market.

These developments highlight the growing potential and Marine Battery Market opportunities for hybrid propulsion technology in the marine industry, driven by technological advancements and strategic partnerships.

Challenges: One significant challenge facing the marine battery market is the inadequate charging infrastructure at ports. Large ships, which need substantial power to operate their systems and store energy, face more difficulties compared to smaller vessels. These large ships often require multiple heavy-duty cables to ensure a consistent power supply. Connecting 15-20 of these cables is neither efficient nor practical, especially for vessels docked for short periods.

Moreover, the current electrical power from onshore grids does not meet the specific needs of ships regarding voltage, frequency, and earthing. To address these challenges, additional infrastructure both onshore and onboard is necessary. For instance, electric vessels require high-voltage superchargers to maintain quick turnaround times. However, these superchargers exert significant demands on local power grids, which are often unable to provide the necessary power within the required timeframe. Consequently, the initial deployment of fully electric ferries requires substantial storage capacity to facilitate faster turnaround times. The transition to electric ferries, such as those being developed by companies like Siemens and Wärtsilä, underscores the urgent need for improved charging infrastructure and power grid adaptations in the Marine Battery Market.

Marine Battery Market Segment Analysis

Based on Ship Type: The Marine Battery market, segmented by ship type into Commercial, Defense, and Unmanned vessels, is expected to see the Commercial segment lead in market share and growth during the forecast period. Thus, this growth is mainly propelled by global tourism, where there is a need for better quality of marine batteries with high energy density, small dimensions, high performance, and long endurance. The commercial segment of the industry thrives from gradual changes in maritime policies and regulations like the saga of the International Maritime Organisation’s IMO 2020 where real and serious measures to reduce emissions are encouraged through the use of electricity in engines or electric propulsion engines.

Also, increasing utilization of marine services in such sectors as deep-sea mining, energy, and infrastructural, oil and gas has a positive implication for the commercial segment. The Marine Battery market also has some other segments which include the starting battery segment, dual-purpose battery segment, and deep cycle battery segments This segment is expected to have substantial technological innovations in the future to support the growth of this segment and hence, is emerging as the fastest growing segment in the Marine Battery market.

Based on Battery Type: Among all the product types, Fuel Cells are supposed to take the largest CAGR of the Marine Battery market in the future period. They have the possibility of becoming a type of zero-emission propulsion solution, particularly, for the medium- and heavy-duty marine sectors. Hydrogen fuel cell technology is already proving its effectiveness, with early implementations powering smaller vessels and port handling equipment. Major industry players like Ballard Power Systems (Canada) are leading in fuel cell production and innovation.

Out of these subcategories, the Lithium-Ion Batteries segment is expected to show high growth as there is increasing adoption of electric propulsion systems in commercial ships. This trend is especially prevalent with IMO 2020 regulations and the expansion of lithium-ion batteries in various segments of the maritime market. These batteries have a definite advantage of being environmentally friendly, efficient, and reliable causing a remarkable proportion of the batteries’ market. This segmentation highlights the diverse landscape of marine batteries, with each type offering unique advantages and facing specific Marine Battery Market dynamics.

Based on Energy Density: The marine battery market is segmented by energy density into three categories: Region-wise classification includes < 100 WH/kg, 100-500 WH/kg, and > 500 WH/kg out of which > 500 WH/Kg segment is expected to have good Marine Battery Market demand throughout the forecast period as it consists of Lithium-ion, Sodium ion, LFP solid state, and other high-performance batteries. These batteries are incorporated into systems whose power is above fifty-kilowatt hours, which are used mainly for propulsion. The first segment is that of high energy density battery technologies where once again, lithium-ion batteries deliver the highest energy density often over 500 WH/kg.

This characteristic makes them a preferred choice for high-capacity, as well as high-performance marine applications. Spear Power Systems was bought by Sensata Technologies, Inc. in August 2021 Spear Power Systems is a company that designs and produces next-generation scalable lithium-ion battery storage systems for the most demanding land, marine, and airborne applications. Sensata’sstry of acquiring Spear Power Systems strengthens its electrification offer as well as moves further into new clean energy segments.

Based on the Sales Channel: The Marine Battery market has OEM and Aftermarket as the distribution channels. Thus, during the intended forecast period, the OEM segment will have the highest market share. Setting from the cargo and freight operators and the global naval forces, manufacturing industries have expanded their fleets. More and more inland and seagoing ships’ masters use hybrid and entirely electric-power systems to decrease their expenses and harm the environment.

Failure to invest systematically in, and expansion of existing fleets by the key players in the global shipping industry. Integrated Propulsion Systems with Special Reference to Hybrid and Electrics with More Emphasis on Sustainability and Reduced Impacts on the Environment hence Cutting down Operational Costs. In conclusion, the change in the demand of the OEM segment for more ecological and efficient propulsion systems also has a positive influence on the expansion of the Marine Battery market.

Based on the Nominal Capacity: According to the assessment made for 2025, the segment of batteries with a capability of more than 250 Ah dominated the Marine Battery Market due to the large demand for large marine batteries used in electrically propelled commercial ships. This increase is due to the recent increase in the governmental and international regulation on carbon and hazardous emissions that is resulting in propulsion systems in marine vessels such as passenger ships and ferries. Spread across the different regions and countries, the less than 100 Ah segment is predicted to become the second biggest during the forecast period.

This is primarily due to the high demand for these batteries in leisure boats and the growing shift from traditional fuel-based propulsion systems to marine batteries. The 100-250 Ah segment is also projected to experience significant growth in the Marine Battery Market. This increase is driven by the need for enhanced maritime connectivity and the rising demand for maritime passenger ships and ferries globally.

Marine Battery Market Regional Insights

Europe is expected to dominate the Marine Battery Market size of marine batteries during the anticipated timeframe. This is due to key players including OEMs and component makers who are incorporating significant capital expenditure on R & D to improve on efficiency and durability of marine batteries. Leading market players include the likes of Corvus Energy based in Norway, Leclanché S. based in Switzerland, Siemens AG based in Germany, and Saft SA based in France. Consequently, Europe dominated the market share by having an amount of USD 0. 42 billion in 2023 because of the numerous commercial marine vessel operators, sound supply chain, and increasing interest in electric boats. Wartsila and Akasol AG are diversifying their product portfolios and designing sophisticated electric propulsion systems; so are Swedish-based Enchandia AB and Leclanché SA headquartered in Switzerland.

Latin America had the highest CAGR in 2021 primarily because Brazil’s naval budget for modern naval vessels is rising. This is expected to remain the same in the forecast period hence putting Latin America as a region of high growth in the Marine Battery Market.

The two regions that are also experiencing fairly good market growth include the Middle East and Africa especially because more and more countries in the region are investing in their defense.

North America is expected to exhibit significant growth contributed by government departments like NOAA opting for electric propulsion as well as improved use of battery-powered marine vessels for commercial, governmental, and leisure use.

Asia Pacific is anticipated to grow at a moderate pace, with market drivers including prominent marine battery manufacturers such as Toshiba Corporation, Exide Industries Ltd., Korea Special Battery, and Furukawa Battery Solutions.

Overall, the rest of the world, including Latin America and the Middle East & Africa, will see moderate growth due to the rising number of commercial marine vessels.

Marine Battery Market Scope

|

Marine Battery Market |

|

|

Market Size in 2025 |

USD 0.87 Bn. |

|

Market Size in 2032 |

USD 2.87 Bn. |

|

CAGR (2026-2032) |

18.5% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Marine Battery Market Segments |

By Ship Type Commercial Defense Unmanned |

|

By Battery Function Starting Batteries Deep-Cycle Batteries Dual Purpose Batteries |

|

|

|

By Nominal Capacity < 100 AH 100 – 250 AH > 250 AH |

|

|

By Propulsion Type Conventional Hybrid Fully Electric |

|

|

By Ship Power < 75 kW 75-150 kW 150-745 kW 745-7,560 kW > 7,560 kW |

|

|

By Battery Design Solid State Liquid/Gel Based |

|

|

By Battery Type Lithium Lead-acid Nickel Cadmium Sodium-ion Fuel-Cell Flooded Gel |

|

|

By Sales Channel OEM Aftermarket |

|

|

By Energy Density < 100 WH/Kg 100-500 WH/Kg > 500 WH/Kg |

|

|

By Application Commercial Defense Unmanned |

|

Regional Scope |

North America (United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Russia, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa ( South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Marine Battery Market Key players

North America

- Shift Clean Energy (Canada)

- Sensata Technologies Inc. (US)

- Lifeline Batteries (US)

- Lithium Werks (US)

- East Penn Manufacturing Co. (US)

- EnerSys (US)

- Staab Battery Mfg. Co., Inc. (US)

Europe

- Corvus Energy (Norway)

- Leclanché S.A. (Switzerland)

- Siemens AG (Germany)

- Saft Groupe S.A. (France)

- Echandia Marine AB (Sweden)

- EST Floattech (Netherlands)

- Powertech Systems (France)

- Manbat Ltd (UK)

- Shield Batteries Limited (UK)

- Systems Sunlight SA (Greece)

- Akasol AG (Germany)

- Johnson Controls International (Ireland)

- Wärtsilä Oyj Abp (Finland)

Asia Pacific

- Furukawa Battery Solutions Co. Ltd. (Japan)

- Kokam Co. Ltd. (South Korea)

- EverExceed Industrial Co. Ltd. (China)

- Exide Industries Ltd. (India)

- G.S. Yuasa Corporation (Japan)

- HBL Power Systems Ltd. (India)

- Korea Special Battery (South Korea)

- Zibo Torch Energy (China)

- Toshiba Corporation (Japan)

Frequently Asked Questions

Europe is expected to dominate the Marine Battery Market during the forecast period.

The Marine Battery Market size is expected to reach USD 2.87 Billion by 2032.

The major top players in the Global Marine Battery Market are GE Vernova (Boston, USA), Avangrid Renewables (Connecticut, USA), Dominion Energy (Virginia, USA), NextEra Energy Resources (Florida, USA), Pattern Energy (San Francisco, USA), Equinor (Texas, USA), Vestas Wind Systems (Aarhus, Denmark) and others.

In comparison with other segments, differences in growth rates are highlighted, market dynamics, and application areas. The marine battery market is compared to automotive, stationary, and consumer electronics battery markets.

1. Marine Battery Market: Research Methodology

2. Marine Battery Market Introduction

2.1. Study Assumption and Market Definition

2.2. Scope of the Study

2.3. Executive Summary

3. Global Marine Battery Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Competitive Landscape

3.3. Key Players Benchmarking

3.3.1. Company Name

3.3.2. Product Segment

3.3.3. End-user Segment

3.3.4. Revenue (2025)

3.3.5. Company Headquarter

3.4. Leading Marine Battery Market Companies, by Market Capitalization

3.5. Market Structure

3.5.1. Market Leaders

3.5.2. Market Followers

3.5.3. Emerging Players

3.6. Mergers and Acquisitions Details

4. Marine Battery Market: Dynamics

4.1. Marine Battery Market Trends

4.2. Marine Battery Market Dynamics

4.2.1.1. Drivers

4.2.1.2. Restraints

4.2.1.3. Opportunities

4.2.1.4. Challenges

4.3. PORTER’s Five Forces Analysis

4.4. PESTLE Analysis

4.5. Water Depth Roadmap

4.6. Regulatory Landscape by Region

4.6.1. North America

4.6.2. Europe

4.6.3. Asia Pacific

4.6.4. Middle East and Africa

4.6.5. South America

5. Marine Battery Market: Global Market Size and Forecast (Value in USD Million) (2025-2032)

5.1. Marine Battery Market Size and Forecast, By Ship Type (2025-2032)

5.1.1. Commercial

5.1.2. Defense

5.1.3. Unmanned

5.2. Marine Battery Market Size and Forecast, By Battery Function (2025-2032)

5.2.1. Starting Batteries

5.2.2. Deep-Cycle Batteries

5.2.3. Dual Purpose Batteries

5.3. Marine Battery Market Size and Forecast, By Nominal Capacity (2025-2032)

5.3.1. < 100 AH

5.3.2. 100 – 250 AH

5.3.3. > 250 AH

5.4. Marine Battery Market Size and Forecast, By Propulsion Type (2025-2032)

5.4.1. Conventional

5.4.2. Hybrid

5.4.3. Fully Electric

5.5. Marine Battery Market Size and Forecast, By Ship Power (2025-2032)

5.5.1. < 75 kW

5.5.2. 75-150 kW

5.5.3. 150-745 kW

5.5.4. 745-7,560 kW

5.5.5. > 7,560 kW

5.6. Marine Battery Market Size and Forecast, By Battery Design (2025-2032)

5.6.1. Solid State

5.6.2. Liquid/Gel Based

5.7. Marine Battery Market Size and Forecast, By Battery Type (2025-2032)

5.7.1. Lithium

5.7.2. Lead-acid

5.7.3. Nickel Cadmium

5.7.4. Sodium-ion

5.7.5. Fuel-Cell

5.7.6. Flooded

5.7.7. Gel

5.8. Marine Battery Market Size and Forecast, By Sales Channel (2025-2032)

5.8.1. OEM

5.8.2. Aftermarket

5.9. Marine Battery Market Size and Forecast, By Energy Density (2025-2032)

5.9.1. < 100 WH/Kg

5.9.2. 100-500 WH/Kg

5.9.3. > 500 WH/Kg

5.10. Marine Battery Market Size and Forecast, By Application (2025-2032)

5.10.1. Commercial

5.10.2. Defense

5.10.3. Unmanned

5.11. Marine Battery Market Size and Forecast, by Region (2025-2032)

5.11.1. North America

5.11.2. Europe

5.11.3. Asia Pacific

5.11.4. Middle East and Africa

5.11.5. South America

6. North America Marine Battery Market Size and Forecast by Segmentation (Value in USD Million) (2025-2032)

6.1. North America Marine Battery Market Size and Forecast, By Ship Type (2025-2032)

6.1.1. Commercial

6.1.2. Defense

6.1.3. Unmanned

6.2. North America North America Marine Battery Market Size and Forecast, By Battery Function (2025-2032)

6.2.1. Starting Batteries

6.2.2. Deep-Cycle Batteries

6.2.3. Dual Purpose Batteries

6.3. North America Marine Battery Market Size and Forecast, By Nominal Capacity (2025-2032)

6.3.1. < 100 AH

6.3.2. 100 – 250 AH

6.3.3. > 250 AH

6.4. North America Marine Battery Market Size and Forecast, By Propulsion Type (2025-2032)

6.4.1. Conventional

6.4.2. Hybrid

6.4.3. Fully Electric

6.5. North America Marine Battery Market Size and Forecast, By Ship Power (2025-2032)

6.5.1. < 75 kW

6.5.2. 75-150 kW

6.5.3. 150-745 kW

6.5.4. 745-7,560 kW

6.5.5. > 7,560 kW

6.6. North America Marine Battery Market Size and Forecast, By Battery Design (2025-2032)

6.6.1. Solid State

6.6.2. Liquid/Gel Based

6.7. North America Marine Battery Market Size and Forecast, By Battery Type (2025-2032)

6.7.1. Lithium

6.7.2. Lead-acid

6.7.3. Nickel Cadmium

6.7.4. Sodium-ion

6.7.5. Fuel-Cell

6.7.6. Flooded

6.7.7. Gel

6.8. North America Marine Battery Market Size and Forecast, By Sales Channel (2025-2032)

6.8.1. OEM

6.8.2. Aftermarket

6.9. North America Marine Battery Market Size and Forecast, By Energy Density (2025-2032)

6.9.1. < 100 WH/Kg

6.9.2. 100-500 WH/Kg

6.9.3. > 500 WH/Kg

6.10. North America Marine Battery Market Size and Forecast, By Application (2025-2032)

6.10.1. Commercial

6.10.2. Defense

6.10.3. Unmanned

6.11. North America Marine Battery Market Size and Forecast, by Country (2025-2032)

6.11.1. United States

6.11.2. Canada

6.11.3. Mexico

7. Europe Marine Battery Market Size and Forecast by Segmentation (Value in USD Million) (2025-2032)

7.1. Europe Marine Battery Market Size and Forecast, By Ship Type (2025-2032)

7.2. Europe Marine Battery Market Size and Forecast, By Battery Function (2025-2032)

7.3. Europe Marine Battery Market Size and Forecast, By Nominal Capacity (2025-2032)

7.4. Europe Marine Battery Market Size and Forecast, By Propulsion Type (2025-2032)

7.5. Europe Marine Battery Market Size and Forecast, By Ship Power (2025-2032)

7.6. Europe Marine Battery Market Size and Forecast, By Battery Design (2025-2032)

7.7. Europe Marine Battery Market Size and Forecast, By Battery Type (2025-2032)

7.8. Europe Marine Battery Market Size and Forecast, By Sales Channel (2025-2032)

7.9. Europe Marine Battery Market Size and Forecast, By Energy Density (2025-2032)

7.10. Europe Marine Battery Market Size and Forecast, By Application (2025-2032)

7.11. Europe Marine Battery Market Size and Forecast, by Country (2025-2032)

7.11.1. United Kingdom

7.11.2. France

7.11.3. Germany

7.11.4. Italy

7.11.5. Spain

7.11.6. Sweden

7.11.7. Russia

7.11.8. Rest of Europe

8. Asia Pacific Marine Battery Market Size and Forecast by Segmentation (Value in USD Million) (2025-2032)

8.1. Asia Pacific Marine Battery Market Size and Forecast, By Ship Type (2025-2032)

8.2. Asia Pacific Marine Battery Market Size and Forecast, By Battery Function (2025-2032)

8.3. Asia Pacific Marine Battery Market Size and Forecast, By Nominal Capacity (2025-2032)

8.4. Asia Pacific Marine Battery Market Size and Forecast, By Propulsion Type (2025-2032)

8.5. Asia Pacific Marine Battery Market Size and Forecast, By Ship Power (2025-2032)

8.6. Asia Pacific Marine Battery Market Size and Forecast, By Battery Design (2025-2032)

8.7. Asia Pacific Marine Battery Market Size and Forecast, By Battery Type (2025-2032)

8.8. Asia Pacific Marine Battery Market Size and Forecast, By Sales Channel (2025-2032)

8.9. Asia Pacific Marine Battery Market Size and Forecast, By Energy Density (2025-2032)

8.10. Asia Pacific Marine Battery Market Size and Forecast, By Application (2025-2032)

8.11. Asia Pacific Marine Battery Market Size and Forecast, by Country (2025-2032)

8.11.1. China

8.11.2. S Korea

8.11.3. Japan

8.11.4. India

8.11.5. Australia

8.11.6. ASEAN

8.11.7. Rest of Asia Pacific

9. Middle East and Africa Marine Battery Market Size and Forecast by Segmentation (Value in USD Million) (2025-2032)

9.1. Middle East and Africa Marine Battery Market Size and Forecast, By Ship Type (2025-2032)

9.2. Middle East and Africa Marine Battery Market Size and Forecast, By Battery Function (2025-2032)

9.3. Middle East and Africa Marine Battery Market Size and Forecast, By Nominal Capacity (2025-2032)

9.4. Middle East and Africa Marine Battery Market Size and Forecast, By Propulsion Type (2025-2032)

9.5. Middle East and Africa Marine Battery Market Size and Forecast, By Ship Power (2025-2032)

9.6. Middle East and Africa Marine Battery Market Size and Forecast, By Battery Design (2025-2032)

9.7. Middle East and Africa Marine Battery Market Size and Forecast, By Battery Type (2025-2032)

9.8. Middle East and Africa Marine Battery Market Size and Forecast, By Sales Channel (2025-2032)

9.9. Middle East and Africa Marine Battery Market Size and Forecast, By Energy Density (2025-2032)

9.10. Middle East and Africa Marine Battery Market Size and Forecast, By Application (2025-2032)

9.11. Middle East and Africa Marine Battery Market Size and Forecast, by Country (2025-2032)

9.11.1. South Africa

9.11.2. GCC

9.11.3. Nigeria

9.11.4. Rest of ME&A

10. South America Marine Battery Market Size and Forecast by Segmentation (Value in USD Million) (2025-2032)

10.1. South America Marine Battery Market Size and Forecast, By Ship Type (2025-2032)

10.2. South America Marine Battery Market Size and Forecast, By Nominal Capacity (2025-2032)

10.3. South America Marine Battery Market Size and Forecast, By Propulsion Type (2025-2032)

10.4. South America Marine Battery Market Size and Forecast, By Ship Power (2025-2032)

10.5. South America Marine Battery Market Size and Forecast, By Battery Design (2025-2032)

10.6. South America Marine Battery Market Size and Forecast, By Battery Type (2025-2032)

10.7. South America Marine Battery Market Size and Forecast, By Sales Channel (2025-2032)

10.8. South America Marine Battery Market Size and Forecast, By Energy Density (2025-2032)

10.9. South America Marine Battery Market Size and Forecast, By Application (2025-2032)

10.10. South America Marine Battery Market Size and Forecast, By Battery Function (2025-2032)

10.11. South America Marine Battery Market Size and Forecast, by Country (2025-2032)

10.11.1. Brazil

10.11.2. Argentina

10.11.3. Rest Of South America

11. Company Profile: Key Players

11.1. Corvus Energy (Norway)

11.1.1. Company Overview

11.1.2. Business Portfolio

11.1.3. Financial Overview

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Leclanché S.A. (Switzerland)

11.3. Siemens AG (Germany)

11.4. Saft Groupe S.A. (France)

11.5. Shift Clean Energy (Canada)

11.6. Echandia Marine AB (Sweden)

11.7. EST Floattech (Netherlands)

11.8. Sensata Technologies Inc. (US)

11.9. Powertech Systems (France)

11.10. Lifeline Batteries (US)

11.11. Furukawa Battery Solutions Co. Ltd. (Japan)

11.12. Lithium Werks (US)

11.13. Kokam Co. Ltd. (South Korea)

11.14. East Penn Manufacturing Co. (US)

11.15. EnerSys (US)

11.16. EverExceed Industrial Co. Ltd. (China)

11.17. Exide Industries Ltd. (India)

11.18. G.S. Yuasa Corporation (Japan)

11.19. HBL Power Systems Ltd. (India)

11.20. Korea Special Battery (South Korea)

11.21. Manbat Ltd (UK)

11.22. Shield Batteries Limited (UK)

11.23. Staab Battery Mfg. Co., Inc. (US)

11.24. Systems Sunlight SA (Greece)

11.25. Zibo Torch Energy (China)

11.26. Akasol AG (Germany)

11.27. Johnson Controls International (Ireland)

11.28. Toshiba Corporation (Japan)

11.29. Wärtsilä Oyj Abp (Finland)

12. Key Findings

13. Industry Recommendations