Japan Delta Robots Market Size, Share, Growth Trends, Industry Analysis, Key Players, Investment Opportunities and Forecast 2026–2034

The Japan Delta Robots Market was valued at USD 112.4 Million in 2025 and is projected to reach USD 322.8 Million by 2034, expanding at a CAGR of 12.4% during the forecast period.

Market growth is being supported by Japan’s strong industrial automation ecosystem, increasing deployment of robotics across electronics manufacturing, food processing facilities, pharmaceutical production plants, and logistics centres. Rising labor shortages caused by demographic changes, together with growing investments in smart factories and next-generation manufacturing technologies, continue to accelerate adoption of Delta robot systems across the country.

Japan Delta Robots Market Overview

Japan has long been recognized as one of the world's leading robotics markets, with automation playing a central role in industrial operations. Delta robots have become increasingly important in high-speed manufacturing environments where precision, repeatability, and productivity are critical requirements.

These robots are extensively utilized in packaging, sorting, assembly, material handling, and pick-and-place applications across a broad range of industries. Their lightweight structure, rapid cycle speeds, and compact footprint make them particularly suitable for modern production lines requiring continuous high-volume operations.

The expansion of smart manufacturing initiatives, increasing adoption of Industry 4.0 technologies, and continuous investment in advanced factory automation are creating favorable conditions for market growth. In addition, developments in artificial intelligence, machine vision systems, and intelligent motion control technologies are enhancing robot performance and enabling wider deployment across complex industrial applications.

To get more Insights: Request Free Sample Report

Japan Delta Robots Market Dynamics

Market Drivers

Growing Factory Automation Across Manufacturing Industries

Japan's manufacturing sector continues to invest heavily in automation technologies to improve production efficiency and maintain global competitiveness. Delta robots are increasingly integrated into production lines due to their ability to perform repetitive operations with high accuracy and speed.

Rising Labor Shortages Supporting Robotic Adoption

Japan's aging workforce and declining working-age population have intensified labor shortages across manufacturing, logistics, and food processing industries. Companies are increasingly turning to robotic automation to address workforce constraints and maintain operational productivity.

Expansion of Electronics and Semiconductor Manufacturing

Japan remains a major hub for electronics and semiconductor production. Delta robots are widely used for component handling, assembly, inspection, and packaging processes, supporting growing demand from these industries.

Market Opportunities

Increasing Adoption of AI-Based Vision Systems

The integration of artificial intelligence with machine vision technologies is creating new opportunities for Delta robot manufacturers. Advanced vision-guided systems enable robots to perform complex inspection, sorting, and assembly tasks with greater precision.

Growth in Pharmaceutical Manufacturing Automation

Japan's pharmaceutical industry continues to modernize production facilities through automation investments. Delta robots are increasingly utilized for packaging, labeling, quality inspection, and medical device assembly applications.

Development of Flexible Production Systems

Manufacturers are increasingly seeking production systems capable of handling multiple product variations while maintaining efficiency. Delta robots provide flexibility and rapid reconfiguration capabilities that support evolving manufacturing requirements.

Market Challenges

High Capital Investment Requirements

The implementation of Delta robot systems often requires significant upfront expenditure involving robotics hardware, software integration, machine vision equipment, and production line modifications.

Integration Complexity

Integrating robotic systems into existing production environments may require process redesign, technical expertise, and employee training, which can increase deployment timelines and costs.

Shortage of Robotics Specialists

Although Japan is a global leader in robotics, demand for qualified automation engineers, software developers, and maintenance specialists continues to exceed supply in several industrial sectors.

Japan Delta Robots Market Trends

Expansion of Vision-Guided Robotics

Manufacturers are increasingly adopting machine vision-enabled Delta robots to improve product inspection, object recognition, sorting accuracy, and packaging efficiency.

Growth of Smart Factory Deployments

Smart manufacturing initiatives are driving greater use of connected robotic systems capable of exchanging real-time operational data and supporting predictive maintenance programs.

AI-Driven Predictive Maintenance

Artificial intelligence is being used to monitor robot performance, identify potential equipment failures, reduce downtime, and improve operational reliability.

Japan Delta Robots Market Segmentation, 2025

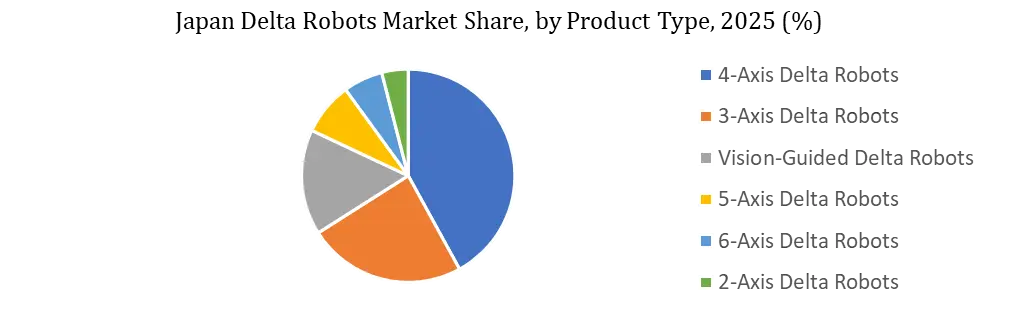

By Product Type

The 4-Axis Delta Robots segment accounted for approximately 42% of the market in 2025. The segment's strong position is supported by widespread adoption across electronics manufacturing, food processing, packaging, and pharmaceutical industries. The Vision-Guided Delta Robots segment continues to record strong growth due to increasing demand for intelligent automation solutions. Meanwhile, 3-Axis Delta Robots remain widely utilized for traditional pick-and-place applications.

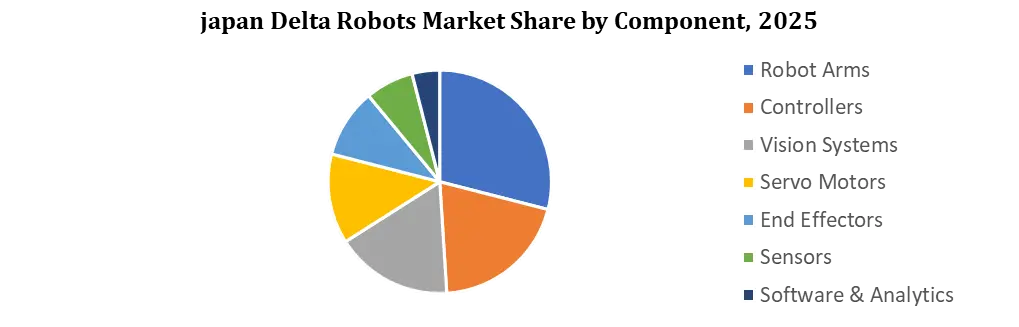

By Component

By Component: Robot Arms led the U.S. Delta Robots Market with approximately 29% market share, driven by their critical role in high-speed and precision automation. Controllers accounted for 20%, supported by increasing adoption of smart manufacturing technologies, while Vision Systems held 17% due to growing demand for AI-enabled inspection and sorting applications. Servo Motors represented 13% of the market, followed by End Effectors at 10%, reflecting their importance in precise material handling. The remaining 11% consisted of sensors, safety systems, communication modules, and other supporting components.

By Payload Capacity

The 1–3 Kg payload capacity segment dominated the market with approximately 38% share, driven by its widespread adoption in packaging, food processing, pharmaceuticals, and electronics assembly applications where high-speed handling of lightweight to medium-weight products is required. The Up to 1 Kg segment accounted for around 29% of the market, supported by increasing use in precision tasks such as small-component assembly, sorting, and inspection operations. The 3–8 Kg segment represented approximately 24% share, benefiting from growing demand for handling heavier products in industrial manufacturing, logistics, and material handling applications. Meanwhile, the Above 8 Kg segment held nearly 9% of the market, primarily serving specialized applications that require higher payload capacities, including automotive components, bulk packaging, and heavy-duty industrial operations.

By Application

Packaging & Pick-and-Place dominated the market with approximately 40% share in 2025, driven by the increasing adoption of high-speed automation in food & beverage, pharmaceuticals, consumer goods, and e-commerce packaging operations. Sorting accounted for around 22% of the market, supported by growing demand for automated product identification, classification, and distribution in logistics and warehouse facilities. Assembly represented approximately 19% share, benefiting from the widespread use of delta robots in electronics, automotive, and precision manufacturing processes requiring speed and accuracy. Material Handling held nearly 11% of the market, driven by the need for efficient movement of products and components across production lines. Meanwhile, Palletizing & Inspection accounted for approximately 8% share, supported by increasing deployment of robotic systems for quality control, packaging verification, and end-of-line palletizing operations.

Japan Delta Robots Market Share Analysis, 2025

The Japanese Delta robots market is characterized by the presence of globally recognized robotics manufacturers and automation technology providers. Domestic companies maintain a strong competitive position due to extensive technological expertise, established customer relationships, and continuous investment in research and development. Leading companies including Yaskawa Electric Corporation, FANUC Corporation, OMRON Corporation, Mitsubishi Electric Corporation, and ABB Ltd. continue to strengthen their market positions through product innovation, AI-enabled robotic systems, and advanced automation solutions.

Recent Market Developments

March 2025

FANUC Corporation introduced new high-speed Delta robot systems designed for semiconductor manufacturing and electronics assembly applications.

July 2025

Yaskawa Electric Corporation expanded its intelligent robotics portfolio with enhanced machine vision integration capabilities.

January 2026

OMRON Corporation launched next-generation AI-enabled Delta robotic systems targeting smart factory environments.

April 2026

Mitsubishi Electric Corporation announced upgrades to its motion control technologies aimed at improving robotic precision and operational efficiency.

|

Japan Delta Robots Market |

|||

|

Report Coverage |

Details |

||

|

Base Year: |

2025 |

Forecast Period: |

2026-2034 |

|

Historical Data: |

2020 to 2025 |

Market Size in 2025: |

USD 112.4 Mn. |

|

Forecast Period 2026 to 2034 CAGR: |

12.4% |

Market Size in 2034: |

USD 322.8 Mn. |

|

Segments

|

By Product Type |

|

|

|

By Payload Capacity

|

|

||

|

By Component |

|

||

|

|

By Application

|

|

|

|

|

By End User |

|

|

Japan Delta Robots Market Key Players

- FANUC Corporation

- Yaskawa Electric Corporation

- OMRON Corporation

- Mitsubishi Electric Corporation

- ABB Ltd.

- KUKA AG

- Epson Robots

- Kawasaki Robotics

- Bosch Rexroth Corporation

- Denso Corporation

Frequently Asked Questions

The 1–3 Kg payload capacity segment holds the largest market share due to its extensive use in packaging, pick-and-place, sorting, and assembly applications.

Packaging & Pick-and-Place is the dominant application segment, accounting for the largest share of the market owing to rising adoption of automated packaging and material handling systems.

Key end-user industries include food & beverage, pharmaceuticals, electronics & semiconductors, consumer goods, logistics & warehousing, and automotive manufacturing.

Major trends include the integration of artificial intelligence (AI), machine vision systems, Industry 4.0 technologies, collaborative robotics, and increasing demand for flexible and high-speed automation solutions.

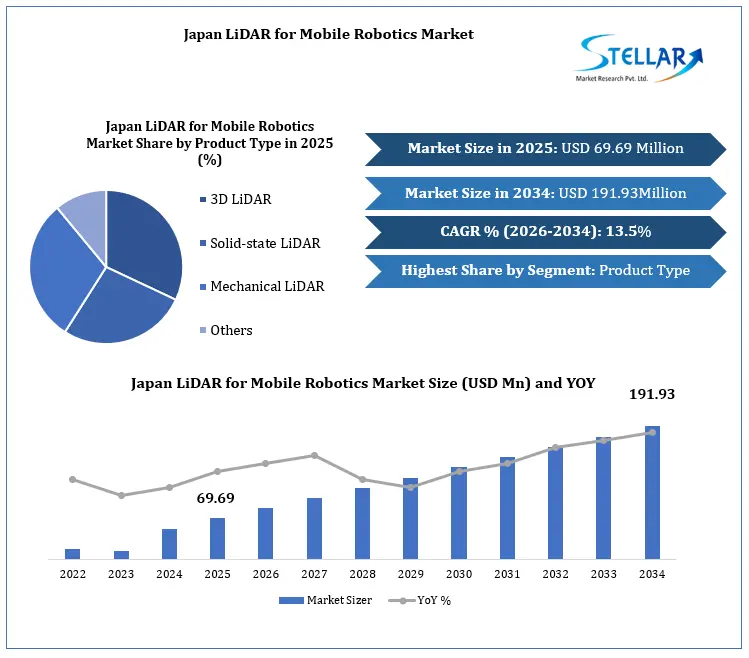

1. Japan LiDAR for Mobile Robotics Market: Executive Summary

1.1 Japan LiDAR for Mobile Robotics Market Size and Forecast (USD Million)

1.2 Market Definition

1.3 Market Segmentation

1.4 Research Timelines

1.5 Assumptions

1.6 Limitations

2. Japan LiDAR for Mobile Robotics Market: Research Methodology

2.1 Data Mining

2.2 Secondary Research

2.3 Primary Research

2.4 Subject Matter Expert Advice

2.5 Quality Check

2.6 Final Review

2.7 Data Triangulation

2.8 Top-Down Approach

2.9 Bottom-Up Approach

2.10 Research Flow

2.11 Data Sources

3. Japan LiDAR for Mobile Robotics Market: Market Attractiveness Mapping

3.1 Japan LiDAR for Mobile Robotics Market Overview

3.2 Competitive Analysis: Funnel Diagram (Tier 1, Tier 2, Tier 3)

3.3 Japan LiDAR for Mobile Robotics Market Absolute Market Opportunity

3.4 Japan LiDAR for Mobile Robotics Market Attractiveness Analysis, By Product Type

3.5 Japan LiDAR for Mobile Robotics Market Attractiveness Analysis, By Component

3.6 Japan LiDAR for Mobile Robotics Market Attractiveness Analysis, By Application

3.7 Japan LiDAR for Mobile Robotics Market Attractiveness Analysis, By Sensor Type

3.8 Future Market Opportunities

4. Japan LiDAR for Mobile Robotics Market: Market Outlook

4.1 Japan LiDAR for Mobile Robotics Market Evolution

4.2 Japan LiDAR for Mobile Robotics Market Outlook

4.3 Market Drivers

4.4 Market Restraints

4.5 Market Trends

4.6 Market Opportunities

4.7 Porter’s Five Forces Analysis

4.7.1 Threat of New Entrants

4.7.2 Bargaining Power of Suppliers

4.7.3 Bargaining Power of Buyers

4.7.4 Threat of Substitute Products

4.7.5 Competitive Rivalry of Existing Competitors

4.8 Value Chain Analysis

4.9 Pricing and Cost Structure Analysis

4.10 Robotics Infrastructure Development in Japan

4.11 Warehouse & Industrial Automation Ecosystem Analysis

4.12 Geopolitical Impact Analysis

4.13 Regulatory Standards & Policy Landscape

4.14 Sustainability & Energy Efficiency Analysis

4.15 Technology Analysis

5. Japan LiDAR for Mobile Robotics Market: By Product Type (2026-2034)

5.1 3D LiDAR

5.2 Solid-State LiDAR

5.3 Mechanical LiDAR

6. Japan LiDAR for Mobile Robotics Market: By Component (2026-2034)

6.1 Laser Scanners

6.2 Inertial Measurement Units (IMUs)

6.3 GPS/GNSS Receivers

6.4 Cameras

6.5 Processors

6.6 Controllers

6.7 Others

7. Japan LiDAR for Mobile Robotics Market: By Application (2026-2034)

7.1 Warehousing & Logistics

7.2 Industrial Manufacturing

7.3 Healthcare & Hospital Automation

7.4 Retail & Commercial Spaces

7.5 Others

8. Japan LiDAR for Mobile Robotics Market: By Sensor Type (2026-2034)

8.1 1D LiDAR Sensors

8.2 2D LiDAR Sensors

8.3 3D LiDAR Sensors

9. SMR Competitive Matrix

10. Japan LiDAR for Mobile Robotics Market: Company Benchmarking

11. Japan LiDAR for Mobile Robotics Market: Company Profiles

11.1 Company Overview

11.2 Business Portfolio

11.3 Financial Overview

11.4 Industry Focus

11.5 Strategic Analysis

11.6 SWOT Analysis

11.7 Recent Developments

11.8 Key Players

1. Hokuyo Automatic Co., Ltd.

2. Sony Semiconductor Solutions Corporation

3. Panasonic Advanced Technology Co., Ltd.

4. OMRON Corporation

5. KEYENCE Corporation

6. Mitsubishi Electric Corporation

7. DENSO Corporation

8. Yamaha Motor Co., Ltd.

9. NEC Corporation

10. Fujitsu Limited

11. Others

12. Risk Assessment and Scenario Analysis

13. Strategic Opportunities

14. Investment & Funding Analysis

15. Strategic Roadmap

15.1 Short-Term Roadmap (2026–2027)

15.2 Mid-Term Roadmap (2028–2030)

15.3 Long-Term Roadmap (2031–2034)

16. Analyst Recommendations

16.1 Recommendations for LiDAR Manufacturers

16.2 Recommendations for Mobile Robotics Companies

16.3 Recommendations for Investors

16.4 Recommendations for New Entrants

16.5 Recommendations for System Integrators and Consulting Firms