Premium Apparel Market Industry Analysis and Forecast (2026-2032)

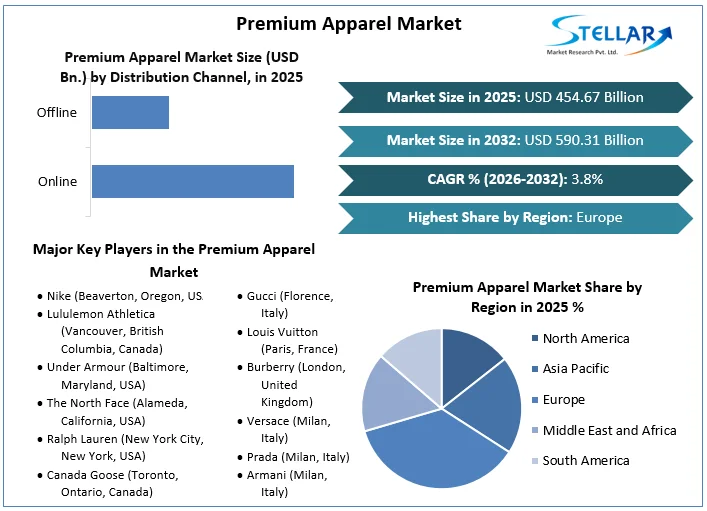

The Premium Apparel size was valued at USD 454.67 Billion in 2025 and the total Global Premium Apparel revenue is expected to grow at a CAGR of 3.8% from 2026 to 2032, reaching nearly USD 590.31 Billion by 2032.

Premium Apparel Market Overview:

Premium apparel is high-quality clothing that typically embodies superior craftsmanship, luxury materials, and exclusive designs. These garments are often associated with established luxury brands or emerging designers who prioritize quality, innovation, and unique fashion experiences. Premium apparel caters to discerning consumers willing to invest in clothing that reflects their style, status, and appreciation for fine craftsmanship. It covers a wide range of products, including haute couture, ready-to-wear collections, and accessories, all characterized by their exceptional quality, attention to detail, and elevated aesthetic appeal. Premium apparel serves as a symbol of status and luxury, offering consumers superior quality, craftsmanship, and unique fashion expression. It provides a luxurious shopping experience and can be viewed as both an investment and a means of personal style expression.

The globalization of fashion, combined with rising disposable incomes and evolving consumer preferences worldwide, fuels the growth of the Global Premium Apparel Market, expanding its reach and market potential across diverse regions and demographics. The increasing adoption of online retail channels and social media platforms on a global scale provides premium apparel brands with unparalleled opportunities to connect with consumers, showcase their products, and expand their market presence beyond traditional retail boundaries.

To get more Insights: Request Free Sample Report

Premium Apparel Market Dynamics:

Digital Transformation Shaping the Democratization of Luxury in the Premium Apparel Market

The advent of the internet and the subsequent rise of social media platforms have dramatically reshaped the landscape of the Premium Apparel Market. Initially cautious about the digital realm, premium apparel brands have gradually recognized its potential for consumer engagement and brand building. However, their entry into social media was delayed compared to other sectors. The digital platforms have become essential tools for reaching a broader audience and fostering aspirational lifestyles. This shift has led to the democratization of luxury, making premium apparel more accessible to a wider demographic, including younger consumers.

Social media platforms serve as channels for consumers to engage with brands, aspire to luxury lifestyles, and express affinity through virtual interactions. Premium apparel brands leverage their originality, creativity, and luxury brand presentation to create immersive experiences that transcend products, forging emotional connections with consumers. This emotional branding reinforces consumers' social status and sense of identity, aligning with their desire for authenticity and aspiration. Thus, the Premium Apparel Market thrives in an era where digital engagement and emotional resonance play pivotal roles in shaping consumer preferences and brand perceptions.

The Democratization Dilemma Impact on Premium Apparel Brands

The evolving purchasing habits of young luxury consumers, who increasingly mix traditional luxury fashion brands with high-street fashion labels, poses a significant challenge for the Premium Apparel Market. This trend blurs the distinction between premium and mass-market offerings, impacting the perceived value and exclusivity of premium apparel products. For instance, a young consumer pair a high-end designer jacket with jeans from a fast-fashion retailer, indicating a shift towards a more eclectic and value-conscious approach to fashion. This mixing and matching dilutes the aspirational appeal of premium apparel items and challenges the traditional notions of luxury.

Moreover, the abundance of information available on the internet presents another restraining factor for premium apparel brands. The digital age has democratized access to fashion information, challenging the perception of scarcity and exclusivity that luxury brands have traditionally relied upon. As consumers have access to a wealth of product information, reviews, and pricing comparisons online, the aura of mystery and allure surrounding premium apparel diminishes. Luxury brands carefully manage their online presence to maintain an air of exclusivity while engaging with consumers transparently and authentically. Overexposure on social media platforms can erode the perceived value of premium apparel items, as consumers become familiarised to seeing luxury products in everyday contexts. Therefore, premium apparel brands need to strike a delicate balance between leveraging social media for brand awareness and maintaining an aura of exclusivity to preserve their desirability and aspirational appeal.

Celebrity Endorsements and Brand Culture Lessons for Premium Apparel Companies

The robust growth of the luxury industry, as evidenced by its increased market share despite challenges such as the global pandemic, presents a significant opportunity for the Premium Apparel Market. As consumers become increasingly affluent and discerning, there is a growing desire for sophisticated and design-oriented commodities, driving demand for premium apparel brands. This trend is particularly pronounced in emerging markets like China, where sales of personal luxury goods have experienced substantial year-on-year growth. Luxury goods, characterized by their high price points and aspirational appeal, serve as symbols of identity and social expression for consumers, elevating the status of premium apparel brands in the eyes of the public.

Moreover, the marketing strategies employed by luxury brands, leveraging celebrity endorsements, brand culture, and exclusive promotions, play a crucial role in driving their success. By understanding the causes and history of luxury goods and analyzing the marketing strategies of leading luxury brands, premium apparel companies can gain valuable insights into consumer behavior and preferences. This knowledge can inform their own marketing strategies, allowing them to effectively position themselves in the market and capitalize on the growing demand for luxury apparel. Additionally, evaluating the strengths and weaknesses of luxury brand marketing practices can help premium apparel brands critically assess their approaches and refine their strategies to better resonate with consumers and drive growth in a competitive market landscape.

Premium Apparel Market Segment Analysis:

Based on Category: the market is divided into Clothing, Footwear, and Accessories. Clothing The Premium Apparel Market is dominated by clothing due to several key factors. The clothing segment dominated the market in 2025 and continues its dominance during the forecast period serving as a fundamental aspect of self-expression and identity for consumers, making it a cornerstone of the fashion industry. Premium apparel brands capitalize on this by offering high-quality garments that not only fulfill functional needs but also reflect the wearer's individual style, status, and taste.

This emphasis on craftsmanship, design, and exclusivity distinguishes premium clothing from mass-market alternatives, attracting discerning consumers who seek superior quality and unique fashion experiences. It covers a wide range of product categories and styles, catering to diverse consumer preferences and occasions. From haute couture gowns to tailored suits, casual wear, and accessories, premium clothing brands offer a comprehensive selection of garments to suit various lifestyles, occasions, and aesthetic preferences. This versatility allows premium apparel brands to appeal to a broader audience and capture a larger share of the market. The enduring appeal of clothing as a form of personal expression and social status ensures its dominance in the premium apparel market. Unlike other categories such as footwear or accessories, clothing has a universal appeal and relevance across different cultures, age groups, and demographics. As such, premium clothing brands command significant influence and visibility in the fashion industry, setting trends, shaping consumer preferences, and driving consumer behaviour.

Premium Apparel Market Regional Analysis:

Europe region dominated the market in the year 2025 and is expected to continue its dominance during the forecast period. In 2025, the Premium Apparel Market in Europe asserted its dominance, emerging as the leading region in terms of market share and growth. This trend is expected to persist throughout the forecast period, underpinned by several key factors. One significant factor contributing to Europe's dominance in the premium apparel market is its rich fashion heritage and culture. European countries, particularly France, Italy, and the United Kingdom, are renowned for their long-standing tradition of craftsmanship, luxury fashion houses, and iconic designer brands. Consumers worldwide perceive European fashion as synonymous with sophistication, elegance, and superior quality, driving demand for premium apparel products originating from this region. Moreover, Europe's diverse consumer base and affluent population further bolster its position as a dominant market for premium apparel. With a large segment of consumers willing to invest in high-quality clothing that reflects their personal style and status, Europe offers a lucrative market opportunity for premium apparel brands. Additionally, the region's robust retail infrastructure, including luxury boutiques, department stores, and online platforms, facilitates the accessibility and distribution of premium apparel products to consumers across Europe and beyond.

Table: Key differences in buying models between USA and EU

|

Europe |

USA |

|

OEM/ODM |

CMT |

|

Factory source RMs |

Nominated RMs |

|

Smaller Order Quantities |

Large Order Quantities |

|

Cost and speed-driven |

Cost-driven |

|

Faster fashion |

Slower fashion |

|

Development agents |

Sourcing agents |

|

Direct business |

Wholesale and private label |

|

One-stop shops |

Specialist product manufacturers |

Competitive Analysis

In the premium apparel market, Nike, Adidas, and Under Armour dominate sportswear, while Lululemon Athletica is known for yoga wear. The North Face and Canada Goose excel in outdoor apparel, while Ralph Lauren offers classic American fashion. In the luxury segment, European brands like Gucci, Louis Vuitton, and Burberry are renowned for their iconic designs, while Italian brands like Versace, Prada, and Armani epitomize luxury fashion. Hugo Boss and Tommy Hilfiger cater to contemporary lifestyles, while Chanel, Fendi, and Saint Laurent represent timeless elegance. Moncler specializes in luxury outerwear, offering high-end winter apparel.

|

Premium Apparel Market Scope |

|

|

Market Size in 2025 |

USD 454.67 Billion |

|

Market Size in 2032 |

USD 590.31 Billion |

|

CAGR (2026-2032) |

3.8% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segments |

By Category

|

|

By Distribution Channel

|

|

|

By End User

|

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Russia, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Premium Apparel Market Key Players:

North America:

- Nike (Beaverton, Oregon, USA)

- Lululemon Athletica (Vancouver, British Columbia, Canada)

- Under Armour (Baltimore, Maryland, USA)

- The North Face (Alameda, California, USA)

- Ralph Lauren (New York City, New York, USA)

- Canada Goose (Toronto, Ontario, Canada)

- Patagonia (Ventura, California, USA)

Europe:

- Adidas (Herzogenaurach, Germany)

- Gucci (Florence, Italy)

- Louis Vuitton (Paris, France)

- Burberry (London, United Kingdom)

- Versace (Milan, Italy)

- Prada (Milan, Italy)

- Armani (Milan, Italy)

- Hugo Boss (Metzingen, Germany)

- Tommy Hilfiger (Amsterdam, Netherlands)

- Chanel (Paris, France)

- Moncler (Milan, Italy)

- Fendi (Rome, Italy)

- Saint Laurent (Paris, France)

Frequently Asked Questions

The major restraints for the premium apparel market growth include economic fluctuations impacting consumer spending, evolving consumer preferences towards more casual wear, and intense competition leading to price sensitivity and margin pressures.

Europe is expected to lead the global Premium Apparel Market during the forecast period.

The Premium Apparel Market size was valued at USD 454.67 Billion in 2025 and the total revenue is expected to grow at a CAGR of 3.8% from 2026 to 2032, reaching nearly USD 590.31 Billion by 2032.

The Premium Apparel report covers Category, Distribution Channel, End User, and Region.

1. Premium Apparel Market: Research Methodology

1.1. Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Assumptions

2. Premium Apparel Market: Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026– 2032) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Premium Apparel Market: Competitive Landscape

3.1. Stellar Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Product Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. Product Launches and Innovation

4. Premium Apparel Market: Dynamics

4.1. Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Market Drivers

4.3. Market Restraints

4.4. Market Opportunities

4.5. Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factors

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Value Chain Analysis

4.10. Regulatory Landscape by Region

4.10.1. North America

4.10.2. Europe

4.10.3. Asia Pacific

4.10.4. Middle East and Africa

4.10.5. South America

5. Premium Apparel Market Size and Forecast by Segments (by Value USD Million)

5.1. Premium Apparel Market Size and Forecast, By Category (2025-2032)

5.1.1. Clothing

5.1.2. Footwear

5.1.3. Accessories

5.2. Premium Apparel Market Size and Forecast, By Distribution Channel (2025-2032)

5.2.1. Online

5.2.2. Offline

5.3. Premium Apparel Market Size and Forecast, By End-User (2025-2032)

5.3.1. Men

5.3.2. Women

5.3.3. Children

5.4. Premium Apparel Market Size and Forecast, by Region (2025-2032)

5.4.1. North America

5.4.2. Europe

5.4.3. Asia Pacific

5.4.4. Middle East and Africa

5.4.5. South America

6. North America Premium Apparel Market Size and Forecast (by Value USD Million)

6.1. North America Premium Apparel Market Size and Forecast, By Category (2025-2032)

6.1.1. Clothing

6.1.2. Footwear

6.1.3. Accessories

6.2. North America Premium Apparel Market Size and Forecast, By Distribution Channel (2025-2032)

6.2.1. Online

6.2.2. Offline

6.3. North America Premium Apparel Market Size and Forecast, By End-User (2025-2032)

6.3.1. Men

6.3.2. Women

6.3.3. Children

6.4. North America Premium Apparel Market Size and Forecast, by Country (2025-2032)

6.4.1. United States

6.4.2. Canada

6.4.3. Mexico

7. Europe Premium Apparel Market Size and Forecast (by Value USD Million)

7.1. Europe Premium Apparel Market Size and Forecast, By Category (2025-2032)

7.2. Europe Premium Apparel Market Size and Forecast, By Distribution Channel (2025-2032)

7.3. Europe Premium Apparel Market Size and Forecast, By End-User (2025-2032)

7.4. Europe Premium Apparel Market Size and Forecast, by Country (2025-2032)

7.4.1. UK

7.4.2. France

7.4.3. Germany

7.4.4. Italy

7.4.5. Spain

7.4.6. Sweden

7.4.7. Austria

7.4.8. Rest of Europe

8. Asia Pacific Premium Apparel Market Size and Forecast (by Value USD Million)

8.1. Asia Pacific Premium Apparel Market Size and Forecast, By Category (2025-2032)

8.2. Asia Pacific Premium Apparel Market Size and Forecast, By Distribution Channel (2025-2032)

8.3. Asia Pacific Premium Apparel Market Size and Forecast, By End-User (2025-2032)

8.4. Asia Pacific Premium Apparel Market Size and Forecast, by Country (2025-2032)

8.4.1. China

8.4.2. S Korea

8.4.3. Japan

8.4.4. India

8.4.5. Australia

8.4.6. Indonesia

8.4.7. Malaysia

8.4.8. Vietnam

8.4.9. Taiwan

8.4.10. Bangladesh

8.4.11. Pakistan

8.4.12. Rest of Asia Pacific

9. Middle East and Africa Premium Apparel Market Size and Forecast (by Value USD Million)

9.1. Middle East and Africa Premium Apparel Market Size and Forecast, By Category (2025-2032)

9.2. Middle East and Africa Premium Apparel Market Size and Forecast, By Distribution Channel (2025-2032)

9.3. Middle East and Africa Premium Apparel Market Size and Forecast, By End-User (2025-2032)

9.4. Middle East and Africa Premium Apparel Market Size and Forecast, by Country (2025-2032)

9.4.1. South Africa

9.4.2. GCC

9.4.3. Egypt

9.4.4. Nigeria

9.4.5. Rest of ME&A

10. South America Premium Apparel Market Size and Forecast (by Value USD Million)

10.1. South America Premium Apparel Market Size and Forecast, By Category (2025-2032)

10.2. South America Premium Apparel Market Size and Forecast, By Distribution Channel (2025-2032)

10.3. South America Premium Apparel Market Size and Forecast, By End-User (2025-2032)

10.4. South America Premium Apparel Market Size and Forecast, by Country (2025-2032)

10.4.1. Brazil

10.4.2. Argentina

10.4.3. Rest of South America

11. Company Profile: Key players

11.1. Nike (Beaverton, Oregon, USA)

11.1.1. Company Overview

11.1.2. Product Portfolio

11.1.2.1. Product Name

11.1.2.2. Product Details (Price, Features, etc.)

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Lululemon Athletica (Vancouver, British Columbia, Canada)

11.3. Under Armour (Baltimore, Maryland, USA)

11.4. The North Face (Alameda, California, USA)

11.5. Ralph Lauren (New York City, New York, USA)

11.6. Canada Goose (Toronto, Ontario, Canada)

11.7. Patagonia (Ventura, California, USA)

11.8. Adidas (Herzogenaurach, Germany)

11.9. Gucci (Florence, Italy)

11.10. Louis Vuitton (Paris, France)

11.11. Burberry (London, United Kingdom)

11.12. Versace (Milan, Italy)

11.13. Prada (Milan, Italy)

11.14. Armani (Milan, Italy)

11.15. Hugo Boss (Metzingen, Germany)

11.16. Tommy Hilfiger (Amsterdam, Netherlands)

11.17. Chanel (Paris, France)

11.18. Moncler (Milan, Italy)

11.19. Fendi (Rome, Italy)

11.20. Saint Laurent (Paris, France)

12. Key Findings

13. Industry Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook