Prefabricated Homes Market Size, Share and Global Forecast 2026-2032

The Global Prefabricated Homes Market is undergoing a structural paradigm shift, evolving from a niche alternative to a primary solution for the global housing crisis. Prefabricated Homes Market was valued at USD 39.2 Billion in 2025, and the total revenue is expected to grow at a CAGR of 7.1 % from 2026 to 2032, reaching USD 63.36 Billion by 2032.

The Prefabricated Homes Market is no longer defined by 'mobile homes' but by Industrialized Construction (IC). Leading developers are moving away from unique, one-off projects toward a Productized Catalog model. This shift, driven by a USD 40 trillion global infrastructure gap, leverages an "automotive-style" production logic to mitigate chronic labor shortages. By adopting productized design catalogs, the industry is achieving unprecedented scalability, moving beyond the "mobile home" stigma toward high-value, sustainable modular solutions.

Key Market Highlights (2025)

- Productivity & Velocity Inflection: The transition to off-site manufacturing enables 20% to 50% faster delivery schedules compared to "stick-built" projects. This compression of the construction lifecycle significantly enhances capital turnover for developers.

- Cost Optimization at Scale: Implementing standardized, repeatable design modules allows firms to amortize R&D costs, leading to a potential 20% reduction in total construction expenditure when executed through mass-production protocols.

- ESG & Waste Mitigation: Controlled factory environments virtually eliminate on-site material inefficiencies, reducing construction waste by up to 90%. This aligns with tightening global green building mandates and institutional ESG requirements.

- From Project to Product: Leading market players are pivoting toward a "Productized Catalog" model. By treating a home as a manufactured product rather than a one-off project, companies can integrate BIM (Building Information Modeling) and AI-driven design to ensure zero-tolerance precision.

Our insights are powered by a proprietary database of 600+ global Prefabricated entities across 30 countries. The analysis reveals that market outperformance is strictly correlated with robust building systems and high value-chain control. Scalability is achieved through strategic, focused integration, transforming construction from fragmented projects into a high-margin Productized Catalog model.

The Efficiency Frontier – Comparative Performance Benchmarks of Prefabricated vs. Traditional Stick-Built Construction

|

Metric |

Traditional Build |

Prefabricated Build |

% Improvement |

|

Construction Time |

12–18 Months |

6–9 Months |

30% – 50% Faster |

|

On-Site Labor |

100% |

20% – 40% |

60% Reduction |

|

Material Waste |

10% – 15% |

< 2% |

90% Less Waste |

To get more Insights: Request Free Sample Report

Top Market Trend: The Surge in Net-Zero Industrialized Housing

The most transformative trend in the Prefabricated Homes Market is the integration of Net-Zero Energy (NZE) standards within factory-controlled production lines. No longer a niche luxury, carbon-neutral prefab is now a mainstream requirement driven by global ESG mandates and the USD 25 billion shift toward "Green Building" financing.

- The Catalyst: Governments (such as the UK, Canada, and India) are offering subsidies for homes that produce as much energy as they consume.

- The Technology: Manufacturers are embedding solar-active facades, BIM-optimized insulation, and IoT-managed energy systems directly into the modules during the factory phase.

- The Impact: This reduces operational energy costs for homeowners by 60% to 100%, while the factory setting ensures a 35% reduction in embodied carbon compared to onsite builds.

By 2032, the 'Net-Zero' home is expected to be the industry standard. MMR research indicates that prefabricated homes with high energy-efficiency certifications command a 15% valuation premium in the resale market. For developers, this trend is the key to unlocking lower-cost Green Loans and securing fast-track planning approvals in urban centers.

Prefabricated Homes Market Dynamics:

Rapid Urbanization is Driving the Shift to Prefabricated Construction:

The global USD 40 trillion infrastructure gap and chronic housing shortfalls drive the market toward a projected USD 63.36 Billion valuation by 2032. Rapid urbanization necessitates the 7.1% CAGR, as modular solutions offer a 50% acceleration in build cycles and a 20% reduction in direct construction costs over traditional "stick-built" methods.

High Capital Intensity to Hamper Market Growth:

Widespread adoption is hampered by high upfront capital requirements, often exceeding USD 55 million for tier-1 manufacturing facilities. Additionally, fragmented building codes across 50+ countries create a 0.7% drag on potential CAGR, while a persistent quality stigma held by 48% of surveyed consumers prevails despite the precision of factory-controlled Industrialized Construction (IC).

The Surge in ESG-Compliant Assets:

The Net-Zero housing presents an opportunity, expanding at an outsized 12.8% CAGR over the forecast period. With governments offering subsidies for Green Building protocols, modular projects that achieve a 90% reduction in material waste are capturing the attention of institutional investors, particularly in the APAC region, which held market worth USD 40.54 Billion in 2025.

Prefabricated Homes Market: Segment Analysis

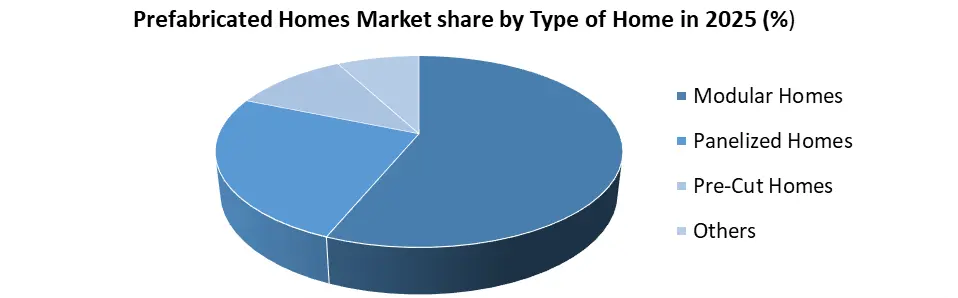

Type of Home is segmented by Modular Homes, Panelized Homes, Pre-Cut Homes, and Others. The modular homes held the largest type in 2025, known for their high degree of factory completion and rapid on-site assembly. These structures account for a significant revenue share of over 50%, as they allow for nearly 90% of the build to occur in a controlled environment, ensuring precision and quality. Panelized homes are gaining popularity due to their superior design flexibility and ease of transportation, particularly for multi-story urban projects. Pre-cut homes (such as kit homes and log cabins) are a significant contributor, driven by the DIY housing segment and the demand for rustic, customizable retreats.

Regional Analysis: Geographic Stratification and Strategic Growth Vectors (2025)

The global landscape is currently defined by a multi-speed adoption of Industrialized Construction (IC), where each region leverages prefabrication to solve localized structural challenges. Asia-Pacific stands as the primary volume driver, utilizing massive volumetric scaling and "Housing for All" mandates to counter rapid urbanization in India and China, while Japan maintains its leadership in high-tech, earthquake-resistant modularity. In North America, the focus has shifted toward high-tech off-site manufacturing and automation to bridge a multi-million-unit housing shortfall and mitigate a severe deficit in skilled trades. Europe leads in the qualitative frontier, where stringent net-zero mandates and circular-economy policies have institutionalized timber-frame (CLT) and energy-efficient building envelopes as the new residential standard. Meanwhile, the Middle East and Africa are utilizing rapid-deploy modular systems to fulfill the ambitious timelines of "Giga-projects" in the GCC, and South America is increasingly adopting standardized panelized kits to address the urgent demand for affordable, disaster-resilient social housing.

Competitive Landscape: Structural Fragmentation and Value Chain Archetypes

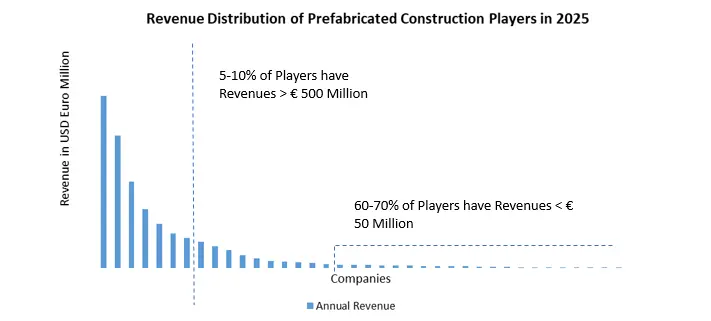

The global Prefabricated Homes Market is characterized by extreme structural fragmentation, with a long tail of over 500 small-to-mid-sized players generating annual revenues below USD 58 million. According to MMR database of 600+ industry entities, only 5% to 10% of market participants have achieved true industrial scale.

Success in this landscape is increasingly dictated by Value Chain Control. Competitive outperformance is concentrated among Integrated Modular Developers who manage the end-to-end lifecycle from architectural design and factory manufacturing to on-site assembly. These vertically integrated players realize significantly higher margins, with an average EBITDA of 15% to 20%, compared to pure-play manufacturers who often operate at a lower 5% EBITDA due to their reliance on third-party contractors and volatile material procurement cycles.

The industry pivots from "project-based" to "product-led" models, the competitive frontier is shifting toward firms that invest in Proprietary Building Systems. Leading players are consolidating their market position by scaling across specific geographies rather than spreading resources too thin, ensuring stable factory utilization and achieving the automotive-style efficiencies required to dominate the next decade of industrialized construction.

Prefabricated Homes Market Scope

|

Prefabricated Homes Market |

|||

|

This Report Covers |

Details |

||

|

Base Year: |

2025 |

Forecast Period: |

2026-2032 |

|

Historical Data: |

2020 to 2025 |

Market Size in 2025: |

USD 39.2 Bn |

|

Forecast Period 2026 to 2032 CAGR: |

7.1% |

Market Size in 2032: |

USD 63.36 Bn |

|

Prefabricated Homes Market Segments Covered: |

By Type of Home |

Modular Homes Panelized Homes Pre-Cut Homes Others |

|

|

By Installation Type |

Permanent Relocatable |

||

|

By Construction Material |

Wood Steel Concrete Others |

||

|

By Application |

Residential Commercial Industrial |

||

Prefabricated Homes Market, by region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Russia and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, and Rest of APAC)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, Rest of MEA)

Prefabricated Homes industry key Players

North America

- Clayton Homes (Berkshire Hathaway)

- Skyline Champion Corporation

- Cavco Industries, Inc.

- Boxabl Inc.

- Plant Prefab, Inc.

- Blu Homes

- Guerdon Modular Buildings

- Onx Homes

- Method Homes LLC

- ATCO Structures

Asia-Pacific

- Sekisui House, Ltd.

- Daiwa House Industry Co., Ltd.

- Panasonic Homes Co., Ltd.

- Asahi Kasei Corporation

- Toyota Housing Corporation

- Ichijo Co., Ltd.

- CIMC Modular Building Systems (MBS)

- Fleetwood Australia

- Larsen & Toubro (L&T) Construction

- EPACK Prefab

Europe & Middle East

- Skanska AB (BoKlok)

- Bouygues Construction

- Laing O'Rourke

- Modulaire Group (Algeco)

- Huf Haus GmbH & Co. KG

- Red Sea International Company

- WeberHaus GmbH & Co. KG

- Kleusberg GmbH & Co. KG

- Speed House Group of Companies

- Tempohousing

Frequently Asked Questions

In 2025, the Asia-Pacific region dominated the Prefabricated Homes market. This dominance is driven by massive infrastructure investments in China and India, alongside Japan’s long-standing leadership in modular manufacturing.

The Prefabricated Homes market was valued at USD 39.2 Billion in 2025 and is expected to grow at a 7.1% CAGR, reaching USD 63.36 Billion by 2032.

The report covers Type of Home, Installation Type, Construction Material, Application and Region.

Major challenges include high upfront capital, logistical transport complexities, fragmented building codes, and persistent negative public perceptions of quality.

1. Prefabricated Homes Market Introduction

1.1. Study Assumption and Market Definition

1.2. Scope of the Study

1.3. Executive Summary

2. Global Prefabricated Homes Market: Competitive Landscape

2.1. SMR Competition Matrix

2.2. Key Players Benchmarking

2.2.1. Company Name

2.2.2. Headquarter

2.2.3. Business Portfolio

2.2.4. Revenue (2024)

2.2.5. End-User Segment

2.2.6. Market Share (%) 2025

2.2.7. Growth Rate (%)

2.2.8. Factory Automation & Technology Adoption

2.2.9. Delivery Time

2.2.10. Design Customization Capability

2.2.11. Green Building Certifications

2.2.12. After-Sales Services & Warranty

2.2.13. Geographical Presence

2.3. Market Structure

2.3.1. Market Leaders

2.3.2. Market Followers

2.3.3. Emerging Players

2.4. Mergers and Acquisitions Details

3. Prefabricated Homes Market: Dynamics

3.1. Prefabricated Homes Market Trends

3.2. Prefabricated Homes Market Dynamics

3.2.1. Drivers

3.2.2. Restraints

3.2.3. Opportunities

3.2.4. Challenges

3.3. PORTER’s Five Forces Analysis

3.4. PESTLE Analysis

3.5. Regulatory Landscape by Region

3.6. Key Opinion Leader Analysis for the Global Industry

3.7. Analysis of Government Schemes and Initiatives for Industry

4. Pricing Trend Analysis by Region

4.1. Country-wise Price Trends by House Type (2020–2024)

4.2. Raw Material Cost Trends (Steel, Concrete, Wood, Others)

4.3. Competitive Pricing Strategies by Regional Players

4.4. Cost Comparison: Prefabricated vs. Traditional Construction Methods

5. Regional Construction Trends & House Demand Analysis

5.1. Year-over-Year Growth in Residential Construction Volume (2025)

5.2. Russia: Federal District-wise Construction Demand

5.3. India: Smart Cities and Affordable Housing Push

5.4. U.S.: Suburban vs. Urban Prefab Adoption

5.5. Regional Analysis of House Shortage and Prefab Uptake

5.6. Infrastructure and Logistics Readiness for Prefab Deployment

5.7. Impact of Urbanization and Migration on Prefab Demand

6. Consumer Behavior Analysis – Prefabricated House Market

6.1. Buying Preferences

6.1.1. Shift Toward Affordable and Rapid-Deployment Housing Solutions

6.1.2. Rising Demand for Customizable and Aesthetic Modular Homes

6.2. Usage Patterns

6.2.1. Growth in Use for Second Homes, Vacation Homes, and Rental Properties

6.2.2. Adoption by Remote Workers Seeking Rural or Suburban Living

6.3. Demographic Insights

6.3.1. Buyer Trends by Age, Income Group, and Household Size

6.3.2. Millennial and Gen Z Preferences for Sustainable and Smart Homes

6.3.3. Urban vs. Rural Demand Patterns and Land Ownership Impact

6.3.4. First-Time Home Buyers vs. Institutional Buyers (Developers, NGOs, Governments)

6.4. Digital Influence

6.4.1. Role of Online Configurators, Virtual Tours, and Digital Customization Tools

6.4.2. Use of Social Media and YouTube in Influencing Design and Builder Choices

6.4.3. Increasing Use of Mobile Apps for Home Planning and Financing

6.4.4. Impact of Online Reviews and Influencer Content on Purchase Decisions

7. Technological Innovations

7.1. 3D Printing and Robotic Assembly in Prefab Construction

7.2. Integration of Smart Home Technology in Modular Homes

7.3. Development of Weatherproof and Fire-Resistant Materials

7.4. Off-site Automation and BIM Integration in Prefab Projects

7.5. Lightweight Structural Systems for Faster Deployment

7.6. Use of IoT in Monitoring Structural Health of Prefab Units

8. Sustainability & Environmental Impact

8.1. Use of Recycled and Low-Carbon Materials in Prefabricated Houses

8.2. Circular Economy Approaches in Prefab Design and Construction

8.3. Energy-Efficient Manufacturing and Assembly Processes

8.4. Eco-Certification (LEED, BREEAM, EDGE) and Green Labeling

8.5. Waste Reduction and Resource Optimization in Factory Settings

9. Supply Chain Analysis

9.1. Overview of the Prefabricated House Supply Chain

9.2. Key Raw Material Suppliers and Component Manufacturers

9.3. Logistics and Transportation Challenges in Module Delivery

9.4. On-Site Assembly Teams and Installation Service Providers

9.5. Builder Partnerships, Franchise Networks, and Developer Strategies

9.6. Risk Factors Including Supply Delays, Skilled Labor Shortages, and Energy Costs

10. Import-Export & Trade Flow Analysis (2024)

10.1. Top Importing Countries for Prefabricated House Units

10.2. Top Exporting Countries of Prefabricated House Units

10.3. Trade Barriers and Tariffs Impacting Global Shipments

10.4. Regional Trade Agreements Supporting Prefabricated House Flow

10.5. Localization vs. Cross-Border Module Supply Trends

11. Regulatory Framework by Region

11.1. Building Codes and Zoning Regulations for Prefabricated Structures

11.2. Fire Safety and Energy Efficiency Standards for Prefabricated Houses

11.3. Legal Recognition of Modular and Manufactured Homes

11.4. Environmental Compliance Related to Waste, Emissions, and Water Use

11.5. Government Incentives for Affordable and Green Prefabricated Housing

12. Prefabricated Homes Market: Global Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Units) (2025-2032)

12.1. Prefabricated Homes Market Size and Forecast, By Type of Home (2025-2032)

12.1.1. Modular Homes

12.1.2. Panelized Homes

12.1.3. Pre-Cut Homes

12.1.4. Others

12.2. Prefabricated Homes Market Size and Forecast, By Installation Type (2025-2032)

12.2.1. Permanent

12.2.2. Relocatable

12.3. Prefabricated Homes Market Size and Forecast, By Construction Material (2025-2032)

12.3.1. Wood

12.3.2. Steel

12.3.3. Concrete

12.3.4. Others

12.4. Prefabricated Homes Market Size and Forecast, By Application (2025-2032)

12.4.1. Residential

12.4.2. Commercial

12.4.3. Industrial

12.5. Prefabricated Homes Market Size and Forecast, By Region (2025-2032)

12.5.1. North America

12.5.2. Europe

12.5.3. Asia Pacific

12.5.4. Middle East and Africa

12.5.5. South America

13. North America Prefabricated Homes Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Units) (2025-2032)

13.1. North America Prefabricated Homes Market Size and Forecast, By Type of Home (2025-2032)

13.2. North America Prefabricated Homes Market Size and Forecast, By Installation Type (2025-2032)

13.3. North America Prefabricated Homes Market Size and Forecast, By Construction Material (2025-2032)

13.4. North America Prefabricated Homes Market Size and Forecast, By Application (2025-2032)

13.5. North America Prefabricated Homes Market Size and Forecast, by Country (2025-2032)

13.5.1. United States

13.5.2. Canada

13.5.3. Mexico

14. Europe Prefabricated Homes Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Units) (2025-2032)

14.1. Europe Prefabricated Homes Market Size and Forecast, By Type of Home (2025-2032)

14.2. Europe Prefabricated Homes Market Size and Forecast, By Installation Type (2025-2032)

14.3. Europe Prefabricated Homes Market Size and Forecast, By Construction Material (2025-2032)

14.4. Europe Prefabricated Homes Market Size and Forecast, By Application (2025-2032)

14.5. Europe Prefabricated Homes Market Size and Forecast, by Country (2025-2032)

14.5.1. United Kingdom

14.5.1.1. United Kingdom Prefabricated Homes Market Size and Forecast, By Type of Home (2025-2032)

14.5.1.2. United Kingdom Prefabricated Homes Market Size and Forecast, By Installation Type (2025-2032)

14.5.1.3. United Kingdom Prefabricated Homes Market Size and Forecast, By Construction Material (2025-2032)

14.5.1.4. United Kingdom Prefabricated Homes Market Size and Forecast, By Application (2025-2032)

14.5.2. France

14.5.3. Germany

14.5.4. Italy

14.5.5. Spain

14.5.6. Sweden

14.5.7. Russia

14.5.8. Rest of Europe

15. Asia Pacific Prefabricated Homes Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Units) (2025-2032)

15.1. Asia Pacific Prefabricated Homes Market Size and Forecast, By Type of Home (2025-2032)

15.2. Asia Pacific Prefabricated Homes Market Size and Forecast, By Installation Type (2025-2032)

15.3. Asia Pacific Prefabricated Homes Market Size and Forecast, By Construction Material (2025-2032)

15.4. Asia Pacific Prefabricated Homes Market Size and Forecast, By Application (2025-2032)

15.5. Asia Pacific Prefabricated Homes Market Size and Forecast, by Country (2025-2032)

15.5.1. China

15.5.2. S Korea

15.5.3. Japan

15.5.4. India

15.5.5. Australia

15.5.6. Indonesia

15.5.7. Malaysia

15.5.8. Philippines

15.5.9. Thailand

15.5.10. Vietnam

15.5.11. Rest of Asia Pacific

16. Middle East and Africa Prefabricated Homes Market Size and Forecast (by Value in USD Million and Volume in Units) (2025-2032)

16.1. Middle East and Africa Prefabricated Homes Market Size and Forecast, By Type of Home (2025-2032)

16.2. Middle East and Africa Prefabricated Homes Market Size and Forecast, By Installation Type (2025-2032)

16.3. Middle East and Africa Prefabricated Homes Market Size and Forecast, By Construction Material (2025-2032)

16.4. Middle East and Africa Prefabricated Homes Market Size and Forecast, By Application (2025-2032)

16.5. Middle East and Africa Prefabricated Homes Market Size and Forecast, by Country (2025-2032)

16.5.1. South Africa

16.5.2. GCC

16.5.3. Egypt

16.5.4. Nigeria

16.5.5. Rest of ME&A

17. South America Prefabricated Homes Market Size and Forecast by Segmentation (by Value in USD Million and Volume in Units) (2025-2032)

17.1. South America Prefabricated Homes Market Size and Forecast, By Type of Home (2025-2032)

17.2. South America Prefabricated Homes Market Size and Forecast, By Installation Type (2025-2032)

17.3. South America Prefabricated Homes Market Size and Forecast, By Construction Material (2025-2032)

17.4. South America Prefabricated Homes Market Size and Forecast, By Application (2025-2032)

17.5. South America Prefabricated Homes Market Size and Forecast, by Country (2025-2032)

17.5.1. Brazil

17.5.2. Argentina

17.5.3. Colombia

17.5.4. Chile

17.5.5. Rest Of South America

18. Company Profile: Key Players

18.1. Clayton Homes (Berkshire Hathaway)

18.1.1. Company Overview

18.1.2. Business Portfolio

18.1.3. Financial Overview

18.1.4. SWOT Analysis

18.1.5. Strategic Analysis

18.1.6. Recent Developments

18.1.7. BYD Auto

18.2. Skyline Champion Corporation

18.3. Cavco Industries, Inc.

18.4. Boxabl Inc.

18.5. Plant Prefab, Inc.

18.6. Blu Homes

18.7. Guerdon Modular Buildings

18.8. Onx Homes

18.9. Method Homes LLC

18.10. ATCO Structures

18.11. Sekisui House, Ltd.

18.12. Daiwa House Industry Co., Ltd.

18.13. Panasonic Homes Co., Ltd.

18.14. Asahi Kasei Corporation

18.15. Toyota Housing Corporation

18.16. Ichijo Co., Ltd.

18.17. CIMC Modular Building Systems (MBS)

18.18. Fleetwood Australia

18.19. Larsen & Toubro (L&T) Construction

18.20. EPACK Prefab

18.21. Skanska AB (BoKlok)

18.22. Bouygues Construction

18.23. Laing O'Rourke

18.24. Modulaire Group (Algeco)

18.25. Huf Haus GmbH & Co. KG

18.26. Red Sea International Company

18.27. WeberHaus GmbH & Co. KG

18.28. Kleusberg GmbH & Co. KG

18.29. Speed House Group of Companies

18.30. Tempohousing

18.31. Others

19. Key Findings

20. Analyst Recommendations

21. Prefabricated Homes Market: Research Methodology