Ocean Wind Farm Market Global Industry Analysis and Forecast (2026-2032)

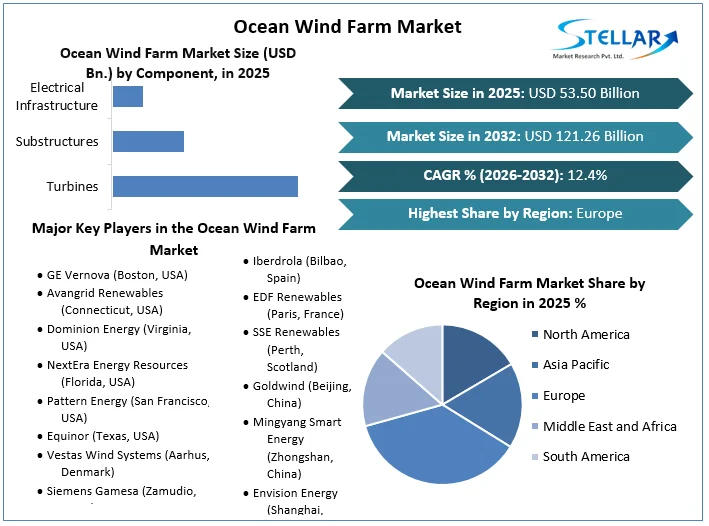

Global Ocean Wind Farm Market size was valued at USD 53.50 Bn. in 2025 and is expected to reach USD 121.26 Bn. by 2032, at a CAGR of 12.4%.

Ocean Wind Farm Market Overview

Ocean wind farms are large renewable energy projects located in ocean waters, usually on the continental shelf, and are known as offshore wind farms. They have several wind turbines mounted on platforms so that use wind energy to generate electricity. These farms offer many advantages over onshore wind farms, including stronger and more consistent winds, and more energy. They aid in reducing land use conflicts and minimize visual and noise impacts on local communities.

The Ocean Wind Farm is a major initiative in the United States renewable energy strategy, promoting to generation of 30 GW of offshore wind power. This ambitious project needs the construction of over 2,000 wind turbines and foundations, the installation of 6,800 miles of cable, and the deployment of enormous specialized vessels. In the first year following the Inflation Reduction Act, the offshore wind industry invested $2.7 billion in 2023 in critical infrastructure, such as ports, vessels, supply chains, and transmission enhancements.

This investment highlights the industry's commitment to developing a robust and efficient offshore wind energy supply chain, making the Ocean Wind Farm an essential component in America's clean energy future. Increasing demand for renewable energy, advances in offshore wind technologies, and capital investments in the public and private sectors are driving the large-scale Ocean Wind Farm Market growth, particularly in Europe, Asia Pacific, and North America. Key players emphasize increasing turbine efficiency and the development of floating wind turbines for deep-water production.

To get more Insights: Request Free Sample Report

Ocean Wind Farm Market Trend

Increasing development and adoption of floating wind farms

The increasing development and adoption of floating wind farms represent a transformative trend in the ocean wind farm market. These innovative structures, such as tension-leg platforms, semi-submersibles, barges, and spar buoys, are designed to harness wind energy in deeper waters where traditional fixed-bottom installations are impractical. Tension-leg platforms, for instance, offer advantages like lighter weight, a smaller mooring footprint, and enhanced stability once installed. Semi-submersibles and barges, anchored with spread mooring systems, provide versatility across different conditions but require careful engineering to achieve stability. Spar buoys, featuring vertical cylindrical structures with ballast for stability, are simpler to construct but demand deep-water installations or harbor facilities.

The transition to floating wind turbines is driven by the need to access wind resources far from shore, beyond fixed onshore capacity systems and by technological advances in the United States. This trend significantly reduces costs, making it competitive with conventional energy Led by several government agencies, the program aims to meet and achieve climate goals jobs and stimulate economic growth in wind generation, installation and operations.

- Equinor, a global leader in floating offshore wind development, exemplifies the industry's push toward industrial-scale deployment. Their experience in the North Sea and other regions positions them uniquely to advance floating wind technology, contributing to new markets and opportunities globally. Similarly, TechnipFMC plays a crucial role by leveraging its expertise in subsea technologies and dynamic systems, essential for the installation and operation of floating wind farms in challenging offshore environments.

Ocean Wind Farm Market Dynamics

Increasing global commitment to decarbonization and the transition towards renewable energy sources Market Growth

The commitment to reducing greenhouse gas emissions and mitigating climate change, and switching to renewable energy sources. Governments, businesses and international organizations have ambitious targets for reducing carbon emissions, focusing on increasing the use of renewable energy. Offshore wind energy, particularly floating wind, is a very important component in this transition, offering feasible solutions for traditional deep water applications of wind resources fixed installations are not possible, which contribute to Ocean Wind Farm Market growth. Supporting government policies and incentives aim to encourage offshore wind development such as financing mechanisms including tax incentives, subsidies, and competitive auctions designed to reduce costs and attract investment.

For instance, the European Union's Green Deal initiative aims to achieve 300 GW of offshore wind capacity by 2050, demonstrating a strong commitment to renewable energy expansion. Similarly, the U.S. Department of Energy's Floating Offshore Wind Shot initiative seeks to reduce the cost of floating offshore wind energy by more than 70% by 2035, making it competitive with conventional energy sources.

Innovations in offshore wind turbine design, layout and installation techniques allow wind farms to be deployed in deeper and more complex marine environments, especially floating wind technology has expanded the geographic wind of offshore operations, to enable wind turbines from offshore Stress-leg platforms, to partially submerge, boost Ocean Wind Farm Market growth. Structures such as platforms, barges and spar buoys are designed for stability, offering many advantages in terms of versatility and cost-effectiveness, contributing to the overall efficiency and scalability of floating wind farms.

Ocean Wind Farm Market Restraint

High initial capital costs associated with the development of offshore wind projects

The high initial cost associated with developing wind projects is a major restriction in the offshore wind farm market due to the capital investment required at various stages from planning to implementation. These costs include site surveys, design and technology, which are necessary to ensure the feasibility and safety of the project which negatively affects offshore wind farms. The construction phase uses specialized vessels, advanced turbine technology and sturdy foundations that withstand the harsh elements of the sea. Turbine installation and grid connections require multiple processes, such as the sea bottom lines and ground stations, increasing costs, which hamper Ocean Wind Farm Market growth.

Financing these projects is challenging because they require significant expenditure over a long period before any revenue is generated. This financial burden is compounded by risks associated with long development times, regulatory uncertainties, and possible changes in government policies and incentives. Difficulties in obtaining licenses and navigating regulatory approvals for the industry delay projects and increase costs, especially in areas without installed offshore wind infrastructure.

Ocean Wind Farm Market Segment Analysis

Based on Component, the market is segmented into Turbines, Substructures, Electrical Infrastructure and Others. Turbines held the largest Ocean Wind Farm Market share in 2025 and are expected to have the highest CAGR during the forecast period. As an integral part of the wind farm, turbines are important in converting the kinetic energy of the wind into electricity, making it an integral part of the overall system operation and operation Turbines transmit wind energy carried by wind along the lines the child is used. This mechanical action rotates the rotor connected to the generator either directly or through the gearbox which increases the speed of rotation, thus producing electricity.

Technological advances, economic impact, adaptability, and key roles in energy production. Modern turbines have seen significant technological advances, such as larger blade designs and enhanced materials, which have improved efficiency and manufacturability. These advances enable turbines to generate more power more reliably and at lower cost and influence the Ocean Wind Farm Market growth. The unique conditions of the offshore environment, with strong, constant wind speeds compared to onshore locations, make turbines particularly efficient and efficient for energy generation work Floating offshore wind has increased the popularity of turbines by enabling them to be used in deep-water wind turbines in wind turbines in the ocean locations to expand the potential areas and increases the overall power output.

Based on Water Depth, the market is categorized into Shallow Water (up to 30 meters), Transitional Water (30 to 60) and Deep Water (over 60 meters). Shallow Water (up to 30 meters) is expected to dominate the Ocean Wind Farm Market during the forecast period. Wind turbines in shallow water are less expensive to operate and maintain than in deep water because they can easily take advantage of simpler and cheaper construction methods for installation since cranes and equipment other heavier ones work well in shallow water. Due to its proximity to the coast and ease of maintenance of the equipment, turbine maintenance is straightforward and inexpensive.

Technological advances in shallow-water wind turbines also play an important role. These wind turbines have been developed for a long time and have been refined, and incorporate well-established processes and practices that ensure efficiency and reliability. This maturity means that many of the technical challenges associated with wind turbines have been overcome along the coast have already been addressed and adjustments have been made in shallow water.

The materials and availability further confirm the popularity of shallow-water wind turbines. Locations close to the coast make it easier to connect turbines to existing power grids, reducing the need for extensive and expensive underwater transmission lines and complex power systems. Thus this closer coastline not only reduces initial costs but also simplifies ongoing business processes, making energy transfer more efficient and less susceptible to loss or technical issues.

Ocean Wind Farm Market Regional Insights

Europe held the largest Ocean Wind Farm Market share and is expected to have the highest CAGR during the forecast period. The continental characteristics of extensive offshore areas and shallow waters in areas such as the North Sea and the Baltic Sea provide favorable conditions for the construction of offshore wind farms. These areas provide consistent and robust wind systems and improve the efficiency and reliability of wind power generation. Countries such as Denmark, Germany and the Netherlands host manufacturers of air conditioners, foundations and other critical components.

This established technological base not only ensures the continued delivery of high-quality equipment but also facilitates innovation and efficiency improvements. The presence of leading companies such as Orsted, Siemens Gamesa and Vestas emphasizes the sector’s leadership, as these companies drive technological breakthroughs and raise productivity. Europe’s growing strength in collaborative research and development production has led to technological advances such as floating turbines and next-generation wind turbines.

The leading countries in terms of the number of offshore wind farms in February 2023 are the United Kingdom, China, Germany, the Netherlands and Denmark. The UK boasts the highest number, followed by China, which has rapidly expanded offshore wind. Germany, the Netherlands and Denmark also have significant numbers of offshore wind farms, contributing to global renewable energy growth and the transition to sustainable energy sources.

The regulatory environment in Europe is also particularly favorable for the development of offshore wind. Across the continent, governments have simplified permitting processes and established clear guidelines and targets for renewable energy integration. This regulatory clarity reduces uncertainty for investors and operators, making it easier to run the business smoothly and drive the Ocean Wind Farm Market growth. The European power grid is well developed and increasingly interconnected, enabling efficient transmission of electricity from offshore wind farms to onshore wind pipeline Infrastructure such as the North Sea. The Wind Power Station, which aims to create an integrated offshore grid, is an example of a forward-thinking approach to wind connectivity and energy distribution in Europe.

Top Five Upcoming Offshore Wind Farm Power Projects in Europe in 2024

|

Project Name |

Country |

Capacity (MW) |

Project Company |

|

Sylen Offshore Wind Power Plant |

Sweden |

8,675 |

SVEA/IG |

|

Med Wind Offshore Wind Power Plant |

Italy |

2,800 |

Renexia |

|

Eystrasalt Offshore Wind Power Plant |

Sweden |

3,900 |

Skyborn Renewables |

|

Erik Segersall Offshore Wind Power Plant |

Sweden |

6,000 |

Deep Wind Offshore |

|

IJmuiden Ver Wind Power Plant Zone |

Netherlands |

6,000 |

RVO |

Ocean Wind Farm Market Scope

|

Ocean Wind Farm Market |

|

|

Market Size in 2025 |

USD 53.50 Bn. |

|

Market Size in 2032 |

USD 121.26 Bn. |

|

CAGR (2026-2032) |

12.4% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Ocean Wind Farm Market Segments |

By Component Turbines Substructures Electrical Infrastructure Others |

|

By Water Depth Shallow Water (up to 30 meters) Transitional Water (30 to 60 Deep Water (over 60 meters) |

|

|

Regional Scope |

North America (United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Russia, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa ( South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Ocean Wind Farm Market Key players

North America

- GE Vernova (Boston, USA)

- Avangrid Renewables (Connecticut, USA)

- Dominion Energy (Virginia, USA)

- NextEra Energy Resources (Florida, USA)

- Pattern Energy (San Francisco, USA)

- Equinor (Texas, USA)

Europe

- Vestas Wind Systems (Aarhus, Denmark)

- Siemens Gamesa (Zamudio, Spain)

- Nordex SE (Hamburg, Germany)

- Iberdrola (Bilbao, Spain)

- EDF Renewables (Paris, France)

- SSE Renewables (Perth, Scotland)

Asia Pacific

- Goldwind (Beijing, China)

- Mingyang Smart Energy (Zhongshan, China)

- Envision Energy (Shanghai, China)

- Windey (Hangzhou, China)

- Hitachi Ltd. (Tokyo, Japan)

- MHI Vestas Offshore Wind (Tokyo, Japan)

- Doosan Heavy Industries & Construction (Changwon, South Korea)

Middle East and Africa (MEA)

- Nordex Group (South Africa)

- Enercon GmbH (South Africa)

South America

- GE Renewable Energy ( Brazil)

- ACCIONA Windpower (Brazil)

Frequently Asked Questions

Europe is expected to dominate the Ocean Wind Farm Market during the forecast period.

The Ocean Wind Farm Market size is expected to reach USD 121.26 Billion by 2032.

The major top players in the Global Ocean Wind Farm Market are GE Vernova (Boston, USA),Avangrid Renewables (Connecticut, USA),Dominion Energy (Virginia, USA),NextEra Energy Resources (Florida, USA),Pattern Energy (San Francisco, USA),Equinor (Texas, USA), Vestas Wind Systems (Aarhus, Denmark)and others.

Increasing demand for renewable energy, advances in offshore wind technologies and capital investments in the public and private sectors are expected to drive market growth during the forecast period.

1. Ocean Wind Farm Market: Research Methodology

2. Ocean Wind Farm Market Introduction

2.1. Study Assumption and Market Definition

2.2. Scope of the Study

2.3. Executive Summary

3. Global Ocean Wind Farm Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Competitive Landscape

3.3. Key Players Benchmarking

3.3.1. Company Name

3.3.2. Product Segment

3.3.3. End-user Segment

3.3.4. Revenue (2025)

3.3.5. Company Headquarter

3.4. Leading Ocean Wind Farm Market Companies, by Market Capitalization

3.5. Market Structure

3.5.1. Market Leaders

3.5.2. Market Followers

3.5.3. Emerging Players

3.6. Mergers and Acquisitions Details

4. Ocean Wind Farm Market: Dynamics

4.1. Ocean Wind Farm Market Trends

4.2. Ocean Wind Farm Market Dynamics

4.2.1.1. Drivers

4.2.1.2. Restraints

4.2.1.3. Opportunities

4.2.1.4. Challenges

4.3. PORTER’s Five Forces Analysis

4.4. PESTLE Analysis

4.5. Water Depth Roadmap

4.6. Regulatory Landscape by Region

4.6.1. North America

4.6.2. Europe

4.6.3. Asia Pacific

4.6.4. Middle East and Africa

4.6.5. South America

5. Ocean Wind Farm Market: Global Market Size and Forecast (Value in USD Million) (2025-2032)

5.1. Ocean Wind Farm Market Size and Forecast, By Component (2025-2032)

5.1.1. Turbines

5.1.2. Substructures

5.1.3. Electrical Infrastructure

5.1.4. Others

5.2. Ocean Wind Farm Market Size and Forecast, By Water Depth (2025-2032)

5.2.1. Shallow Water (up to 30 meters)

5.2.2. Transitional Water (30 to 60

5.2.3. Deep Water (over 60 meters)

5.3. Ocean Wind Farm Market Size and Forecast, by Region (2025-2032)

5.3.1. North America

5.3.2. Europe

5.3.3. Asia Pacific

5.3.4. Middle East and Africa

5.3.5. South America

6. North America Ocean Wind Farm Market Size and Forecast by Segmentation (Value in USD Million) (2025-2032)

6.1. North America Ocean Wind Farm Market Size and Forecast, By Component (2025-2032)

6.1.1. Turbines

6.1.2. Substructures

6.1.3. Electrical Infrastructure

6.1.4. Others

6.2. North America Ocean Wind Farm Market Size and Forecast, By Water Depth (2025-2032)

6.2.1. Shallow Water (up to 30 meters)

6.2.2. Transitional Water (30 to 60

6.2.3. Deep Water (over 60 meters)

6.3. North America Ocean Wind Farm Market Size and Forecast, by Country (2025-2032)

6.3.1. United States

6.3.2. Canada

6.3.3. Mexico

7. Europe Ocean Wind Farm Market Size and Forecast by Segmentation (Value in USD Million) (2025-2032)

7.1. Europe Ocean Wind Farm Market Size and Forecast, By Component (2025-2032)

7.2. Europe Ocean Wind Farm Market Size and Forecast, By Water Depth (2025-2032)

7.3. Europe Ocean Wind Farm Market Size and Forecast, by Country (2025-2032)

7.3.1. United Kingdom

7.3.2. France

7.3.3. Germany

7.3.4. Italy

7.3.5. Spain

7.3.6. Sweden

7.3.7. Russia

7.3.8. Rest of Europe

8. Asia Pacific Ocean Wind Farm Market Size and Forecast by Segmentation (Value in USD Million) (2025-2032)

8.1. Asia Pacific Ocean Wind Farm Market Size and Forecast, By Component (2025-2032)

8.2. Asia Pacific Ocean Wind Farm Market Size and Forecast, By Water Depth (2025-2032)

8.3. Asia Pacific Ocean Wind Farm Market Size and Forecast, by Country (2025-2032)

8.3.1. China

8.3.2. S Korea

8.3.3. Japan

8.3.4. India

8.3.5. Australia

8.3.6. ASEAN

8.3.7. Rest of Asia Pacific

9. Middle East and Africa Ocean Wind Farm Market Size and Forecast by Segmentation (Value in USD Million) (2025-2032)

9.1. Middle East and Africa Ocean Wind Farm Market Size and Forecast, By Component (2025-2032)

9.2. Middle East and Africa Ocean Wind Farm Market Size and Forecast, By Water Depth (2025-2032)

9.3. Middle East and Africa Ocean Wind Farm Market Size and Forecast, by Country (2025-2032)

9.3.1. South Africa

9.3.2. GCC

9.3.3. Nigeria

9.3.4. Rest of ME&A

10. South America Ocean Wind Farm Market Size and Forecast by Segmentation (Value in USD Million) (2025-2032)

10.1. South America Ocean Wind Farm Market Size and Forecast, By Component (2025-2032)

10.2. South America Ocean Wind Farm Market Size and Forecast, By Water Depth (2025-2032)

10.3. South America Ocean Wind Farm Market Size and Forecast, by Country (2025-2032)

10.3.1. Brazil

10.3.2. Argentina

10.3.3. Rest Of South America

11. Company Profile: Key Players

11.1. Hormel Foods Corporation (Austin, Minnesota, USA)

11.1.1. Company Overview

11.1.2. Business Portfolio

11.1.3. Financial Overview

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. GE Vernova (Boston, USA)

11.3. Avangrid Renewables (Connecticut, USA)

11.4. Dominion Energy (Virginia, USA)

11.5. NextEra Energy Resources (Florida, USA)

11.6. Pattern Energy (San Francisco, USA)

11.7. Equinor (Texas, USA)

11.8. Vestas Wind Systems (Aarhus, Denmark)

11.9. Siemens Gamesa (Zamudio, Spain)

11.10. Nordex SE (Hamburg, Germany)

11.11. Iberdrola (Bilbao, Spain)

11.12. EDF Renewables (Paris, France)

11.13. SSE Renewables (Perth, Scotland)

11.14. Goldwind (Beijing, China)

11.15. Mingyang Smart Energy (Zhongshan, China)

11.16. Envision Energy (Shanghai, China)

11.17. Windey (Hangzhou, China)

11.18. Hitachi Ltd. (Tokyo, Japan)

11.19. MHI Vestas Offshore Wind (Tokyo, Japan)

11.20. Doosan Heavy Industries & Construction (Changwon, South Korea)

11.21. Nordex Group (South Africa)

11.22. Enercon GmbH (South Africa)

11.23. GE Renewable Energy ( Brazil)

11.24. ACCIONA Windpower (Brazil)

12. Key Findings

13. Industry Recommendations