Major Depressive Disorder Market Industry Analysis and Forecast (2026-2032)

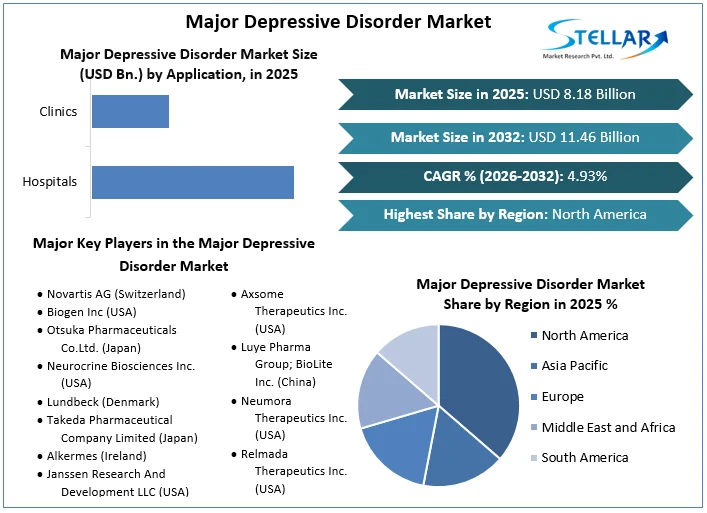

The Major Depressive Disorder Market size was valued at USD 8.18 Bn. in 2025 and the total Global Major Depressive Disorder revenue is expected to grow at a CAGR of 4.93 % from 2026 to 2032, reaching nearly USD 11.46 Bn. by 2032.

Major Depressive Disorder Market Overview

Major Depressive Disorder (MDD) is a community mental illness characterized by a persistently low mood that conflicts with the person’s ability to work, sleep, eat, and other activities. MDD is also indicated as clinical depression or recurrent depression. The symptoms of this mental disorder are loss of interest, recurrent thoughts of death, insomnia, feelings of worthlessness, and decreased ability to think.

- Depression is the fourth leading cause of disability across the globe and is associated with severely high rates of suicidal behavior and mortality.

Stellar Market Research published a report that analyzes Major Depressive Disorder Market trends to predict the market's growth. The report begins with a description of the business environment and explains the commercial summary of the chain structure. Additionally, it illustrates the corporate profiles and situation of the competitive landscape amongst numerous associated corporations including the analysis of market evaluation and options associated with the worth chain. This Major Depressive Disorder research report provides insights on market overview, market segmentation, current and future pricing, growth analysis, competitive landscape, and other such premium insights within the forecast period.

The research objective of the report is to provide a report with an in-depth analysis of the major depressive disorder market by types of therapeutic drugs and region. It also offers data points and comprehensive data on factors affecting the market and evaluates competition -mergers and expansions, product launches, and technological advancements within the market. Key players play a crucial role in driving innovation and improving product efficacy, underscoring the importance of targeted strategies to meet evolving consumer demands.

The market scope includes opportunities in new product development and advancements in drug formulation technologies, which propel market growth and innovation. Through quantitative research methods, the report offers statistical data on the effectiveness of Major Depressive Disorder and its impact on market trends. Competitive intelligence analysis aids in comprehending market dynamics, competitor strategies, and customer perceptions, empowering market players to gain a competitive advantage in the global Major Depressive Disorder market.

To get more Insights: Request Free Sample Report

Major Depressive Disorder Market Dynamics

Embracing Mental Health Focus and Therapeutic Innovations

The global Major Depressive Disorder (MDD) market presents a significant market opportunity due to the increasing focus on mental health. Several factors are fueling this trend and impacting the market opportunities and feasibility studies for companies. The growing public awareness and reduced stigma surrounding mental health conditions are the key trends driving the major depressive disorder market. This translates to a larger pool of potential patients seeking diagnosis and treatment, expanding the market penetration strategies for pharmaceutical companies. The high prevalence of MDD, estimated to affect over 4% of the global population, creates a substantial economic impact.

The associated costs of lost productivity, absenteeism, and comorbid health issues drive healthcare systems and private insurers to invest in effective treatments. This spurs company financial matrix considerations for pharmaceutical companies, pushing them to develop and deliver cost-effective solutions. While traditional antidepressants have limitations, the development of novel therapies, such as rapid-acting antidepressants and neuromodulation techniques, addresses these limitations. These advancements promise improved patient outcomes and adherence to treatment plans, potentially leading to higher profit margins for companies with successful product launches further driving the major depressive disorder market.

The increasing focus on mental health and the development of novel therapies create a compelling market opportunity for the global major depressive disorder market. Companies that effectively address the unmet needs of patients through innovative treatment solutions and efficient distribution channels are poised to capture significant market share and achieve strong financial performance in the major depressive disorder market.

- In adults, major depressive disorder is most common in those who are 25-44 years of age. Within an entire lifetime, major depression affects 10% - 25% of women and 5%- 12% of men.

Limited Treatment Efficacy & Ensuring Affordability

Limited treatment efficacy refers to the shortcomings of current therapies. Traditional antidepressants have several side effects and take a long time to produce results, leading to patients being less likely to adhere to the treatment, resulting in reduced success rates. This not only affects the patients' well-being but also strains healthcare systems due to repeat consultations and potential hospitalizations. Additionally, affordability is another challenge as the high cost of treatment acts as a significant barrier to entry for novel therapies, especially those needing specialized administration or monitoring.

The policies of insurance companies and government agencies significantly impact patient access to treatment. Market consolidation among major pharmaceutical companies further restricts access to affordable treatments. Mergers and acquisitions limit competition and potentially lead to higher drug prices. Additionally, trade policy decisions disrupt supply chains and influence drug pricing. Companies need to consider these factors and develop strategies to ensure their treatments remain affordable for patients and healthcare systems. The limited treatment efficacy and affordability are significant challenges for the major depressive disorder market. Companies that can address these restraints by developing more effective and affordable therapies will be better positioned to gain market share and improve patient outcomes.

Major Depressive Disorder Market Segment Analysis

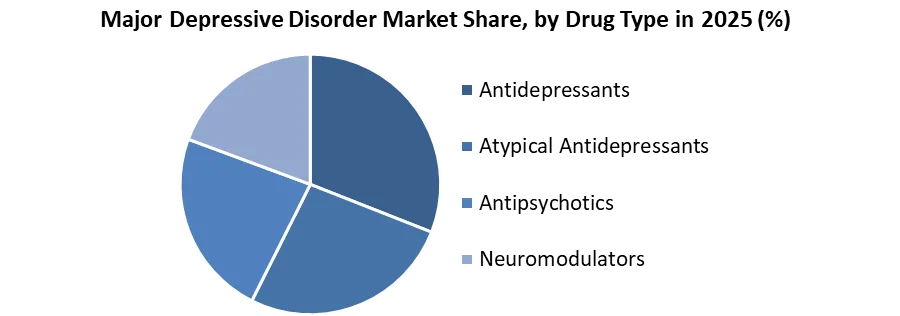

By Drug Type, According to SMR research, the Antidepressant Drugs segment is the largest in 2025 and dominates the Major Depressive Disorder market. The Major Depressive Disorder (MDD) market is effectively dominated by the Antidepressant Drugs segment, which employs a strategic and comprehensive approach. Through market segmentation, pharmaceutical companies are able to tailor their strategies to specific patient needs and preferences, with subcategories such as SSRIs and SNRIs. This targeted approach is reinforced by the cost advantage of manufacturing established medications within this segment.

The affordability of these drugs leads to increased production volume and greater market penetration. The distribution channels for these medications are well-established, with easy access through traditional pharmacies. However, the sector is recognizing the rising trend of online retail and is increasingly utilizing this platform to ensure convenient availability for patients, reducing interruptions in treatment adherence.

Pharmaceutical firms consistently invest in research and development (R&D) to develop new formulations, combination therapies, or medications with enhanced side-effect profiles. This emphasis on innovation directly impacts product positioning strategies. By emphasizing the unique selling points of new medications, companies set themselves apart in a competitive market. Pricing strategies play a crucial role in the pharmaceutical industry, especially with the rise of online retail. By implementing strategic pricing, companies drive market growth while ensuring that essential medications remain accessible to those who need them. The dominance of the Antidepressant Drugs segment is attributed to a well-defined market segmentation strategy, efficient production processes, accessible distribution channels, and a focus on innovation driving the Major Depressive Disorder market.

Major Depressive Disorder Market Regional Analysis

North America holds a major share of the Major Depressive Disorder (MDD) market, with several key companies, manufacturers, and leading players operating in the region. The high prevalence of Major Depressive Disorder in North America has resulted in tremendous growth in the market. Countries like the United States and Canada have significant populations diagnosed with Major Depressive Disorder, creating a strong demand for effective treatments and brand recognition. As a result, many pharmaceutical companies headquartered in North America invest heavily in research and development (R&D) for novel Major Depressive Disorder medications, consolidating their positions as top-selling forces within the region.

The region has a robust healthcare infrastructure that has facilitated the development of well-established trade finance channels and streamlined distribution networks for Major Depressive Disorder medications. Additionally, brand loyalty programs encourage patients to remain loyal to particular medications, thereby enhancing the major depressive disorder market dominance of leading pharmaceutical companies.

North America benefits from a supportive regulatory environment that includes agencies like the Food and Drug Administration (FDA) in the US. These agencies ensure rigorous yet efficient drug approval processes, fostering innovation and creating a level playing field for manufacturers. This streamlined approach makes North America an attractive market for international pharmaceutical companies seeking to expand their global footprint further making the dominance of the region in the Major Depressive Disorder market. The region’s dominance in the Major Depressive Disorder market is a result of the high disease burden, robust healthcare infrastructure, and favorable regulatory environment in the region.

Major Depressive Disorder Market Competitive Landscape

The market for Major Depressive Disorder is competitive with key players including Novartis AG, Biogen Inc, Otsuka Pharmaceuticals Co.Ltd., Neurocrine Biosciences Inc., Lundbeck, Takeda Pharmaceutical Company Limited, Alkermes, etc. The key players are adopting collaborative strategies like mergers and acquisitions, product launches, and joint ventures to expand the consumer base in the market. The market for Major Depressive Disorder is competitive and dynamic, thanks to technological advancements in drug production and diagnosis, emerging markets, and an increase in healthcare expenditure and infrastructure.

- In 2024, Otsuka Pharmaceutical, Co. Ltd. (Otsuka) and Click Therapeutics, Inc., (Click) announce that the U.S. Food and Drug Administration (FDA) has cleared Rejoyn™ (developed as CT-152), the first prescription digital therapeutic authorized for the treatment of major depressive disorder (MDD) symptoms as an adjunct to clinician-managed outpatient care for adult patients with MDD age 22 years and older who are on antidepressant medication.

- In 2024, Neurocrine Biosciences, Inc. announced that the first patient has been randomized for its Phase 2 clinical study to evaluate the efficacy, safety, and tolerability of investigational compound NBI-1070770 in adults with major depressive disorder.

- In 2024, Intra-Cellular Therapies, Inc. announced positive topline results from Study 501 evaluating lumateperone 42 mg as an adjunctive therapy to antidepressants for the treatment of major depressive disorder (MDD).

- In 2023, Biogen announced the FDA approval of ZURZUVAE™ (zuranolone), the First and Only Oral Treatment Approved for Women with Postpartum Depression, and Issued a Complete Response Letter for Major Depressive Disorder.

- In 2022, Sun Pharma and Lundbeck signed a licensing agreement to introduce a novel antidepressant medication in India.

- In 2022, Sunosi from Jazz Pharmaceuticals was acquired by Axsome Therapeutics strengthening its position as a leader in the neuroscience field.

- In 2022, Cariprazine (VRAYLAR) for the Adjunctive Treatment of Major Depressive Disorder Supplemental New Drug Application by AbbVie to the FDA.

|

Major Depressive Disorder Market Scope |

|

|

Market Size in 2025 |

USD 8.18 Bn. |

|

Market Size in 2032 |

USD 11.46 Bn. |

|

CAGR (2026-2032) |

4.93 % |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segments |

By Drug Type Antidepressants Atypical Antidepressants Antipsychotics Neuromodulators Others |

|

By Application Hospitals Clinics Others |

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Player in the Major Depressive Disorder Market

- Novartis AG (Switzerland)

- Biogen Inc (USA)

- Otsuka Pharmaceuticals Co.Ltd. (Japan)

- Neurocrine Biosciences Inc. (USA)

- Lundbeck (Denmark)

- Takeda Pharmaceutical Company Limited (Japan)

- Alkermes (Ireland)

- Janssen Research And Development LLC (USA)

- Intra-Cellular Therapies Inc. (USA)

- Axsome Therapeutics Inc. (USA)

- Luye Pharma Group; BioLite Inc. (China)

- Neumora Therapeutics Inc. (USA)

- Relmada Therapeutics Inc. (USA)

- Fabre-Kramer (USA)

- Vistagen Therapeutics Inc. (USA)

- Pfizer Inc (USA)

- Johnson & Johnson (United States)

- Abbott Laboratories (USA)

- AbbVie Inc. (USA)

- Merck & Co., Inc. (USA)

- Bristol-Myers Squibb (United States)

- Eli Lilly and Co (United States)

- AstraZeneca PLC (England)

- GlaxoSmithKline plc (United Kingdom)

- Sanofi S.A (France)

Frequently Asked Questions

The rising prevalence of MDD, increasing focus on mental health, and government initiatives to raise awareness are the drivers of the Major Depressive Disorder market.

Investors can capitalize on the MDD market by considering companies developing novel therapies or expanding access through telehealth while keeping an eye on government funding trends in mental health.

The Market size was valued at USD 8.18 Billion in 2025 and the total Market revenue is expected to grow at a CAGR of 4.93 % from 2026 to 2032, reaching nearly USD 11.46 billion.

The segments covered in the market report are diagnosis, drug type, and region.

1. Major Depressive Disorder Market: Research Methodology

1.1. Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market breakdown and Data Triangulation

1.4. Assumptions

2. Major Depressive Disorder Market: Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026 – 2032) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Major Depressive Disorder Market: Competitive Landscape

3.1. Stellar Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Business Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. Product Launches and Innovation

4. Major Depressive Disorder Market: Dynamics

4.1. Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Market Drivers

4.3. Market Restraints

4.4. Market Opportunities

4.5. Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factors

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Regulatory Landscape by Region

4.9.1. North America

4.9.2. Europe

4.9.3. Asia Pacific

4.9.4. Middle East and Africa

4.9.5. South America

5. Major Depressive Disorder Market Size and Forecast by Segments (by Value USD Million)

5.1. Major Depressive Disorder Market Size and Forecast, By Drug Type (2025-2032)

5.1.1. Antidepressants

5.1.2. Atypical Antidepressants

5.1.3. Antipsychotics

5.1.4. Neuromodulators

5.1.5. Others

5.2. Major Depressive Disorder Market Size and Forecast, By Application (2025-2032)

5.2.1. Hospitals

5.2.2. Clinics

5.2.3. Others

5.3. Major Depressive Disorder Market Size and Forecast, by Region (2025-2032)

5.3.1. North America

5.3.2. Europe

5.3.3. Asia Pacific

5.3.4. Middle East and Africa

5.3.5. South America

6. North America Major Depressive Disorder Market Size and Forecast (by Value USD Million)

6.1. North America Major Depressive Disorder Market Size and Forecast, By Drug Type (2025-2032)

6.1.1. Antidepressants

6.1.2. Atypical Antidepressants

6.1.3. Antipsychotics

6.1.4. Neuromodulators

6.1.5. Others

6.2. North America Major Depressive Disorder Market Size and Forecast, By Application (2025-2032)

6.2.1. Hospitals

6.2.2. Clinics

6.2.3. Others

6.3. North America Major Depressive Disorder Market Size and Forecast, by Country (2025-2032)

6.3.1. United States

6.3.2. Canada

6.3.3. Mexico

7. Europe Major Depressive Disorder Market Size and Forecast (by Value USD Million)

7.1. Europe Major Depressive Disorder Market Size and Forecast, By Drug Type (2025-2032)

7.2. Europe Major Depressive Disorder Market Size and Forecast, By Application (2025-2032)

7.3. Europe Major Depressive Disorder Market Size and Forecast, by Country (2025-2032)

7.3.1. UK

7.3.2. France

7.3.3. Germany

7.3.4. Italy

7.3.5. Spain

7.3.6. Sweden

7.3.7. Austria

7.3.8. Rest of Europe

8. Asia Pacific Major Depressive Disorder Market Size and Forecast (by Value USD Million)

8.1. Asia Pacific Major Depressive Disorder Market Size and Forecast, By Drug Type (2025-2032)

8.2. Asia Pacific Major Depressive Disorder Market Size and Forecast, By Application (2025-2032)

8.3. Asia Pacific Major Depressive Disorder Market Size and Forecast, by Country (2025-2032)

8.3.1. China

8.3.2. S Korea

8.3.3. Japan

8.3.4. India

8.3.5. Australia

8.3.6. Indonesia

8.3.7. Malaysia

8.3.8. Vietnam

8.3.9. Taiwan

8.3.10. Bangladesh

8.3.11. Pakistan

8.3.12. Rest of Asia Pacific

9. Middle East and Africa Major Depressive Disorder Market Size and Forecast (by Value USD Million)

9.1. Middle East and Africa Major Depressive Disorder Market Size and Forecast, By Drug Type (2025-2032)

9.2. Middle East and Africa Major Depressive Disorder Market Size and Forecast, By Application (2025-2032)

9.3. Middle East and Africa Major Depressive Disorder Market Size and Forecast, by Country (2025-2032)

9.3.1. South Africa

9.3.2. GCC

9.3.3. Egypt

9.3.4. Nigeria

9.3.5. Rest of ME&A

10. South America Major Depressive Disorder Market Size and Forecast (by Value USD Million)

10.1. South America Major Depressive Disorder Market Size and Forecast, By Drug Type (2025-2032)

10.2. South America Major Depressive Disorder Market Size and Forecast, By Application (2025-2032)

10.3. South America Major Depressive Disorder Market Size and Forecast, by Country (2025-2032)

10.3.1. Brazil

10.3.2. Argentina

10.3.3. Rest of South America

11. Company Profile: Key players

11.1. Novartis AG (Switzerland)

11.1.1. Company Overview

11.1.2. Business Portfolio

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Biogen Inc (USA)

11.3. Otsuka Pharmaceuticals Co.Ltd. (Japan)

11.4. Neurocrine Biosciences Inc. (USA)

11.5. Lundbeck (Denmark)

11.6. Takeda Pharmaceutical Company Limited (Japan)

11.7. Alkermes (Ireland)

11.8. Janssen Research And Development LLC (USA)

11.9. Intra-Cellular Therapies Inc. (USA)

11.10. Axsome Therapeutics Inc. (USA)

11.11. Luye Pharma Group; BioLite Inc. (China)

11.12. Neumora Therapeutics Inc. (USA)

11.13. Relmada Therapeutics Inc. (USA)

11.14. Fabre-Kramer (USA)

11.15. Vistagen Therapeutics Inc. (USA)

11.16. Pfizer Inc (USA)

11.17. Johnson & Johnson (United States)

11.18. Abbott Laboratories (USA)

11.19. AbbVie Inc. (USA)

11.20. Merck & Co., Inc. (USA)

11.21. Bristol-Myers Squibb (United States)

11.22. Eli Lilly and Co (United States)

11.23. AstraZeneca PLC (England)

11.24. GlaxoSmithKline plc (United Kingdom)

11.25. Sanofi S.A (France)

12. Key Findings

13. Industry Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook