Laminated Labels Market Global Market Outlook and Forecast (2026-2032) Trends, Statistics, Dynamics, Segmentation by Composition, Type, Form, and Region.

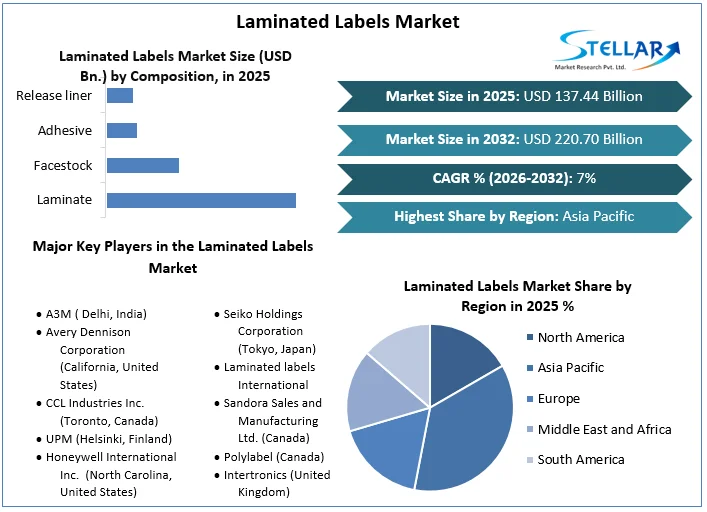

Laminated Labels Market was valued at USD 137.44 billion in 2025. Global Laminated Labels Market size is estimated to grow at a CAGR of 7% over the forecast period.

Laminated Labels Market Definition:

A protective coating on laminate labels improves their life by allowing them to survive harsh environments such as chemicals, dampness, and solvents. When high friction and weather resistance are important, laminated labels provide the best durability and lifespan. Laminated labels endure the harsh conditions that might cause physical damage to unlaminated objects, such as excessive temperatures and UV light. Product information such as the product name, address, market information, ingredients, QR code, barcode, and more are included on the laminated label. Topcoats, adhesives, face materials, liners, and substrates with labels are the primary components of laminated labels Furthermore, laminated labels protect printing and are more durable than coatings. The report on the Laminated Labels Market by Stellar Market Research is come up with the PESTLE, PORTER's five force and segment analysis on the basis of composition, type, form and region.

To get more Insights: Request Free Sample Report

Laminated Labels Market Dynamics:

One of the key factors driving the laminated labels market is the preference for semi-glossy or matte laminate finishes over glossy labels when scanning the barcode on the matte finish label.

Aesthetics and high performance with growing pressure-sensitive technology and the availability of other choices, such as printing directly on the container, along with the supplier's low switching costs are likely to boost bargaining leverage even further. Increased product demand comes from the food and beverage industry, and consumer goods demand, logistics, and manufacturing activity expansion are the key drivers of growth in the laminated labels market.

The introduction of nanotechnology in label and packaging applications has created a business opportunity. For invisible brand protection coding and smart indicator labels that signal temperature changes, spy dust or nanotags are utilised. Nanoscale particles can be disseminated directly into liquids and utilised as printing inks and coating materials, according to new procedures being developed by manufacturers.

The laminated labels market is also benefiting from the increased use of smart labels in RFID. RFID is used to track commodities across the supply chain, track parts on manufacturing lines, and implement cashless payment systems, among other applications.

In the packaging business, there are alternatives that can simply replace laminated labels. Flexible packaging and pouches are packaging products that do not require additional labels to be attached to the packaged item. These factors are restraining the laminated labels market growth.

Glossed labels can also be utilised to generate high-gloss finishes, which reduces the necessity for laminated labels. Laminated label producers' profit margins have shrunk due to fierce market rivalry. The big consumer business distributes its products at a low cost due to severe competition, resulting in minimal profit margins for label makers.

Adhesive labels are becoming more important in the industry as an advanced labelling technology. Label geometry, multi-process imaging, fast automatic and accurate output are all provided by pressure-sensitive technology, which is ideal for premium labelling applications. Pressure-sensitive technology is far superior to other technologies, especially in applications involving information labelling.

The rise of in-mold labelling in the label industry is driving the laminated labels market growth. In-mold labelling is a manufacturing technique that produces and labels the container at the same time, using high-speed injection moulding and blow moulding with robot assistance. The in-mold labelling approach is preferred by most brand owners since it is suitable for large volumes of containers and decreases the weight and expense of the packing process.

Laminated Labels Market Segment Analysis:

By Composition, Facestock dominated the laminated labels market with a 42.1 % share in 2025. It serves as a moisture and steam barrier as well as a protective laminate. It is commonly used as a spacer material for the layered construction and is placed on top of the laminated label.

Through the forecast period, the release liner segment is expected to grow at a CAGR of 6.2 %. Paper, coated paper, or silicone coated film can be used as the release film. It also aids in keeping the glue in place until the label is applied. These reasons are expected to fuel the segment's expansion in the market.

By Type, Polyester dominated the laminated labels market with 43.4 % in 2025. Durable labels with strong chemical and heat resistance are becoming increasingly popular. It has increased demand in numerous industries as a result of these qualities. These reasons are driving the segment demand.

The UV sunscreen polyester and UL-certified laminate segments are expected to expand rapidly. There is a growing demand for UV-resistant labels that are attractive and do not fade over time. Throughout the projection period, these factors are expected to drive the segment's growth in the laminated labels market.

By Form, Reels dominated the market with 68 % share in 2025. For large-area marking, most labelling equipment uses roll-shaped labels. These reasons are driving the segment's expansion in the market.

Through the forecast period, sheets are expected to increase at a CAGR of 4 %. Demand for consumer and institutional labelling products for utilities, desktops, drawers, files, cabinets, cartons, and other personal items is increasing. These reasons are projected to fuel the segment's growth in the laminated labels market.

Laminated Labels Market Regional Insights:

In 2025, Asia Pacific dominated the market with a share of 40 %. Demand in the region is being driven by growth in the food and beverage, consumer durables, and pharmaceutical industries. The CLP Regulation on the categorization, labelling, and packaging of chemicals and mixtures is being enforced. Increased manufacturing investment in rising economies like China and India. These factors are driving the APAC laminated labels market.

Throughout the forecast period, Europe is expected to increase at a CAGR of 6 %. Growing demand for high-quality labels, film laminated labels, and other factors are projected to drive the market forward throughout the forecast period.

Laminated Labels Market Key Players Insights:

The market is characterized by the existence of a number of well-known firms. These companies control a large portion of the market, have a wide product portfolio, and have a global presence. In addition, the market comprises small to mid-sized competitors that sell a limited variety of items, some of which are self-publishing organizations.

The laminated labels market's major companies have a significant impact because most of them have extensive global networks through which they can reach their massive client bases. To drive revenue growth and strengthen their positions in the global market, key players in the market, particularly in Europe and North America, are focusing on strategic initiatives such as acquisitions, new collection launches, and partnerships.

The objective of the report is to present a comprehensive analysis of the Global Laminated Labels market to the stakeholders in the industry. The report provides trends that are most dominant in the Global Laminated Labels market and how these trends will influence new business investments and market development throughout the forecast period. The report also aids in the comprehension of the global market dynamics and competitive structure of the market by analyzing market leaders, market followers, and regional players.

The qualitative and quantitative data provided in the Global Laminated Labels market report is to help understand which market segments, regions are expected to grow at higher rates, factors affecting the market, and key opportunity areas, which will drive the industry and market growth through the forecast period. The report also includes the competitive landscape of key players in the industry along with their recent developments in the Global Laminated Labels market. The report studies factors such as company size, market share, market growth, revenue, production volume, and profits of the key players in the global market.

The report provides Porter's Five Force Model, which helps in designing the business strategies in the market. The report helps in identifying how many rivals are existing, who they are, and how their product quality is in the Global Laminated Labels market. The report also analyses if the Global Laminated Labels market is easy for a new player to gain a foothold in the market, do they enter or exit the market regularly if the market is dominated by a few players, etc.

The report also includes a PESTEL Analysis, which aids in the development of company strategies. Political variables help in figuring out how much a government can influence the Global Laminated Labels market. Economic variables aid in the analysis of economic performance drivers that have an impact on the Global Laminated Labels market. Understanding the impact of the surrounding environment and the influence of environmental concerns on the global market is aided by legal factors.

Laminated Labels Market Scope:

|

Laminated Labels Market |

|

|

Market Size in 2025 |

USD 137.44 Bn. |

|

Market Size in 2032 |

USD 220.70 Bn. |

|

CAGR (2026-2032) |

7% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segment Scope |

By Composition

|

|

By Type

|

|

|

By Form

|

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

LAMINATED LABELS MARKET KEY PLAYERS:

- A3M ( Delhi, India)

- Avery Dennison Corporation (California, United States)

- CCL Industries Inc. (Toronto, Canada)

- UPM (Helsinki, Finland)

- Honeywell International Inc. (North Carolina, United States)

- Tesa SE-A Beiersdorf Company (Hamburg, Germany)

- Seiko Holdings Corporation (Tokyo, Japan)

- Laminated labels International

- Sandora Sales and Manufacturing Ltd. (Canada)

- Polylabel (Canada)

- Intertronics (United Kingdom)

- R. Donnelley & Sons Company ( Chicago, United States)

- OpSec Security Group Ltd. (Colorado, United States)

- Guangzhou Manborui Material Technology Co Ltd. (China)

- Constania (Vienna , Austria)

- (* Key Players List Not Exhaustive)

Frequently Asked Questions

Asia Pacific region is expected to hold the highest share in the Laminated Labels Market.

The market size of the Laminated Labels Market by 2032 is expected to reach USD 220.70 Billion.

The forecast period for the Laminated Labels Market is 2026-2032.

The market size of the Laminated Labels Market in 2025 was valued at USD 137.44 Billion.

1. Research Methodology

1.1 Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Up Approach

1.3. Market Breakdown and Data Triangulation

1.4. Research Assumption

2. Laminated Labels Market Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026 – 2032) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Global Laminated Labels Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Product Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Magin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. Product Launches and Innovations

4. Laminated Labels Market: Dynamics

4.1. Laminated Labels Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Laminated Labels Market Drivers

4.3. Laminated Labels Market Restraints

4.4. Laminated Labels Market Opportunities

4.5. Laminated Labels Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Legal Factors

4.7.5. Environmental Factors

4.8. Technological Analysis

4.8.1. Innovations in Laminated Label Design and Functionality

4.8.2. Technological Roadmap

4.9. Value Chain Analysis

4.10. Regulatory Landscape by Region

4.10.1. North America

4.10.2. Europe

4.10.3. Asia Pacific

4.10.4. Middle East and Africa

4.10.5. South America

5. Laminated Labels Market: Global Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

5.1. Laminated Labels Market Size and Forecast, by Composition (2025-2032)

5.1.1. Laminate

5.1.2. Face stock

5.1.3. Adhesive

5.1.4. Release liner

5.2. Laminated Labels Market Size and Forecast, by Type (2025-2032)

5.2.1. Polyester

5.2.2. Polypropylene

5.2.3. UV sunscreen polyester

5.2.4. Others

5.3. Laminated Labels Market Size and Forecast, by Form (2025-2032)

5.3.1. Reels

5.3.2. Sheets

5.4. Laminated Labels Market Size and Forecast, by Region (2025-2032)

5.4.1. North America

5.4.2. Europe

5.4.3. Asia Pacific

5.4.4. Middle East and Africa

5.4.5. South America

6. North America Laminated Labels Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

6.1. North America Laminated Labels Market Size and Forecast, by Composition (2025-2032)

6.1.1. Laminate

6.1.2. Face stock

6.1.3. Adhesive

6.1.4. Release liner

6.2. North America Laminated Labels Market Size and Forecast, by Type (2025-2032)

6.2.1. Polyester

6.2.2. Polypropylene

6.2.3. UV sunscreen polyester

6.2.4. Others

6.3. North America Laminated Labels Market Size and Forecast, by Form (2025-2032)

6.3.1. Reels

6.3.2. Sheets

6.4. North America Laminated Labels Market Size and Forecast, by Country (2025-2032)

6.4.1. United States

6.4.2. Canada

6.4.3. Mexico

7. Europe Laminated Labels Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

7.1. Europe Laminated Labels Market Size and Forecast, by Composition (2025-2032)

7.2. Europe Laminated Labels Market Size and Forecast, by Type (2025-2032)

7.3. Europe Laminated Labels Market Size and Forecast, by Form (2025-2032)

7.4. Europe Laminated Labels Market Size and Forecast, by Country (2025-2032)

7.4.1. United Kingdom

7.4.2. France

7.4.3. Germany

7.4.4. Italy

7.4.5. Spain

7.4.6. Sweden

7.4.7. Austria

7.4.8. Rest of Europe

8. Asia Pacific Laminated Labels Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

8.1. Asia Pacific Laminated Labels Market Size and Forecast, by Composition (2025-2032)

8.2. Asia Pacific Laminated Labels Market Size and Forecast, by Type (2025-2032)

8.3. Asia Pacific Laminated Labels Market Size and Forecast, by Form (2025-2032)

8.4. Asia Pacific Laminated Labels Market Size and Forecast, by Country (2025-2032)

8.4.1. China

8.4.2. S Korea

8.4.3. Japan

8.4.4. India

8.4.5. Australia

8.4.6. Indonesia

8.4.7. Malaysia

8.4.8. Vietnam

8.4.9. Taiwan

8.4.10. Rest of Asia Pacific

9. Middle East and Africa Laminated Labels Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

9.1. Middle East and Africa Laminated Labels Market Size and Forecast, by Composition (2025-2032)

9.2. Middle East and Africa Laminated Labels Market Size and Forecast, by Type (2025-2032)

9.3. Middle East and Africa Laminated Labels Market Size and Forecast, by Form (2025-2032)

9.4. Middle East and Africa Laminated Labels Market Size and Forecast, by Country (2025-2032)

9.4.1. South Africa

9.4.2. GCC

9.4.3. Nigeria

9.4.4. Rest of ME&A

10. South America Laminated Labels Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

10.1. South America Laminated Labels Market Size and Forecast, by Composition (2025-2032)

10.2. South America Laminated Labels Market Size and Forecast, by Type (2025-2032)

10.3. South America Laminated Labels Market Size and Forecast, by Form (2025-2032)

10.4. South America Laminated Labels Market Size and Forecast, by Country (2025-2032)

10.4.1. Brazil

10.4.2. Argentina

10.4.3. Rest Of South America

11. Company Profile: Key Players

11.1. A3M ( Delhi, India)

11.1.1. Company Overview

11.1.2. Business Portfolio

11.1.2.1. Product Name

11.1.2.2. Product Details (Price, Features, etc)

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Avery Dennison Corporation (California, United States)

11.3. CCL Industries Inc. (Toronto, Canada)

11.4. UPM (Helsinki, Finland)

11.5. Honeywell International Inc. (North Carolina, United States)

11.6. Tesa SE-A Beiersdorf Company (Hamburg, Germany)

11.7. Seiko Holdings Corporation (Tokyo, Japan)

11.8. Laminated labels International

11.9. Sandora Sales and Manufacturing Ltd. (Canada)

11.10. Polylabel (Canada)

11.11. Intertronics (United Kingdom)

11.12. R. Donnelley & Sons Company ( Chicago, United States)

11.13. OpSec Security Group Ltd. (Colorado, United States)

11.14. Guangzhou Manborui Material Technology Co Ltd. (China)

11.15. Constania (Vienna , Austria)

12. Key Findings

13. Analyst Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook