Fuel Station Market Global Industry Analysis and Forecast (2026-2032)

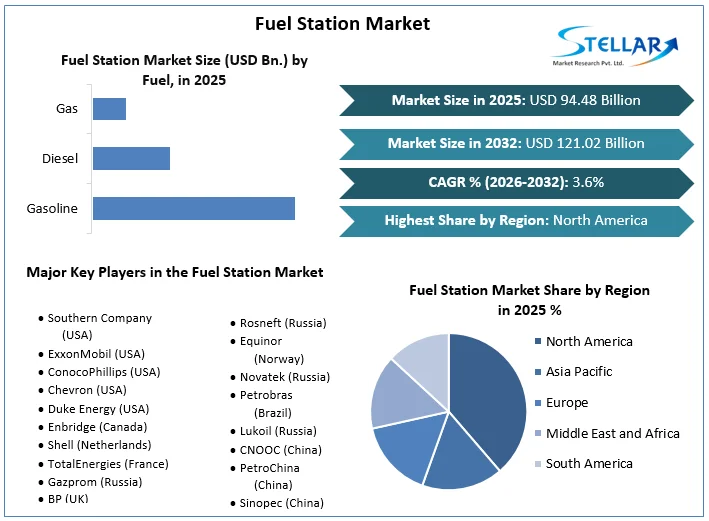

The Fuel Station Market size was valued at USD 94.48 Bn. in 2025 and the total Global Fuel Station Market revenue is expected to grow at a CAGR of 3.6 % from 2026 to 2032, reaching nearly USD 121.02 Bn. by 2032.

Fuel Station Market Overview

A fuel station is a portion of a facility dedicated to storing and dispensing motor fuels. The Fuel Station Market is experiencing significant growth, driven by increasing vehicle sales and the expansion of fuel station networks. For Instance, Bharat Petroleum operates over 14,802 fuel stations in India, with 13,648 of them fully automated. Meanwhile, the United Kingdom has 8,353 operational petrol stations, with additional ones under development. Similarly, the United States boasts an extensive fuel station network, with over 121,000 stations across the country. With its rapidly growing economy and rising vehicle ownership, China also has a substantial number of fuel stations, exceeding 100,000 in total.

The fuel station market's primary driver remains the continuous demand for gasoline and diesel, particularly in developing regions where vehicle ownership is rising. Innovations in fuel efficiency and the introduction of cleaner fuel options are attracting environmentally conscious consumers, further stimulating market growth. The shift towards sustainable energy and advanced customer engagement technologies positions the Fuel Station Market for continued growth and evolution.

Innovations in fuel efficiency have had a significant impact on the fuel station market. As vehicles become more fuel-efficient, the demand for gasoline and diesel decreases, leading to a potential decrease in fuel station sales. However, this also presents an opportunity for fuel stations to adapt and evolve by offering alternative fuel options, such as electric vehicle charging stations or hydrogen fueling stations, to provide the changing needs of consumers and stay relevant in the market.

Stellar Market Research recently released an extensive report examining trends within the Fuel Station Industry, aiming to predict its growth trajectory. This thorough analysis covers essential elements such as industry size, market share, scope, growth potential, and more, providing valuable insights for businesses to navigate opportunities and risks effectively. The report meticulously investigates various aspects including market overview, segmentation, current and future growth forecasts, competitive landscape, and beyond.

With a research goal focused on delivering a comprehensive understanding of the Fuel Station market across parameters such as Fuel, End User, and Region, the report offers rich data on factors shaping market dynamics. It assesses competitive strategies, including mergers, expansions, product launches, and technological advancements, highlighting key players propelling innovation in diagnostics technology. Utilizing quantitative research methodologies, the report presents statistical analyses to showcase the effectiveness of Fuel Station and its impact on market trends. Moreover, the incorporation of competitive intelligence analysis assists in deciphering market dynamics, competitor strategies, and customer perceptions. These insights enable market participants to devise targeted strategies, thus gaining a competitive advantage in the global Fuel Station Market landscape.

To get more Insights: Request Free Sample Report

Fuel Station Market: Dynamics

Rising Passenger vehicle penetration helps to drive the fuel station market growth

The increasing number of passenger vehicles drives significant growth in the fuel station market by boosting fuel demand. This necessitates the expansion of fuel station networks to accommodate the higher number of vehicles, particularly in rapidly urbanizing areas. As each additional vehicle requires regular refueling, there is a greater need for conveniently located fuel stations. This growth in fuel stations also stimulates local economies by creating jobs and increasing economic activity around new stations. The higher number of vehicles drives demand for ancillary services such as convenience stores and maintenance, enhancing the profitability of fuel stations.

Technological advancements, such as automated payment systems and digital fuel management, improve efficiency and customer experience, further attracting business. Competitive pricing and promotional offers due to increased competition also draw more customers. Urbanization and greater mobility trends contribute to this growth, as densely populated urban areas need more fuel stations. Global market dynamics, especially in emerging markets, influence the expansion of multinational fuel station chains, reinforcing overall fuel station market growth. The domestic passenger vehicle (PV) industry in India has shown strong growth compared to its global peers. According to the SMR study report the domestic PV market (including cars, vans, and utility vehicles) grew rapidly.

This growth rate is higher than in France, Britain, Germany, and China, while Japan, the US, and Brazil have declined. In absolute numbers, the increase in vehicles sold in India (approximately 180,000 units) surpassed Germany (151,000 units), Britain (143,000 units), and France (101,000 units). This growth to new vehicle launches, declining fuel prices, and lower interest rates. The growth in the Indian market is helping multinational automobile makers with operations in India to offset declines in other markets. Factors such as low vehicle penetration, rising disposable income, and increasing road infrastructure are expected to further boost growth in the Indian passenger car industry compared to other leading markets. By 2026, passenger vehicles in India are expected to increase to between 9.4 and 13.4 million units.

Strict Environmental regulation restrains the growth of the Fuel station Market

Stringent environmental regulations present formidable obstacles to the fuel station market's Growth. These mandates necessitate costly upgrades to meet emissions standards, pollution controls, and safety protocols, imposing significant financial strains and operational complexities on fuel station operators. Also, regulatory uncertainties deter potential investors from entering or expanding within the market. The increasing promotion of alternative fuels and energy sources, such as electric vehicles and renewables, further diminishes the demand for traditional fuel stations, compelling operators to reconsider their business strategies to remain competitive in a changing landscape.

Despite these challenges, there are avenues for growth through innovation and sustainable practices. In the UK, fuel stations encounter a strict regulatory framework that includes authorizations from the Environment Agency, water companies, and local authorities, all aimed at ensuring environmental protection. Internationally, guidelines emphasize environmental safeguards, including vapor recovery and risk assessments for groundwater contamination, fire, and explosions. Environmental impact assessments are conducted for new fuel stations to evaluate potential ecological ramifications and devise mitigation strategies. Adhering to these regulations while embracing innovation potentially alleviates adverse effects and creates long-term growth opportunities within the fuel station industry.

Integration of digital technology creates lucrative growth opportunities for the Fuel station Market

Digital Technology enhances customer experience, improving operational efficiency, and enabling innovative services. For instance, implementing mobile payment solutions allows customers to pay for fuel without cash or cards, streamlining transactions and reducing wait times. Digital signage is used to display real-time fuel prices, promotions, and advertisements, attracting customers and increasing sales. Loyalty programs and mobile apps personalize offers, provide discounts, and gather valuable customer data for targeted marketing strategies.

Also, digital technology enables remote monitoring of fuel levels, equipment maintenance, and security systems, optimizing operations and reducing costs. Also, the emergence of electric vehicles (EVs) presents an opportunity for fuel stations to install EV charging stations, leveraging digital platforms to manage charging sessions and offer value-added services. Embracing digital technology not only improves the efficiency and profitability of fuel stations but also enhances the overall customer experience, driving growth and competitiveness in the Fuel Station Market.

Fuel Station Market: Segment Analysis

Based On Fuel, the gasoline sub-segment dominated the Fuel Station Market in the year 2025. The widespread adoption of gasoline-powered vehicles has been a major driver. For decades, gasoline vehicles have been the preferred choice for personal and commercial transportation due to their cost-effectiveness, reliability, and established infrastructure. This has created a large, consistent demand for gasoline at fuel stations. Also, the extensive network of gasoline refineries and distribution channels has made gasoline readily available and relatively inexpensive compared to alternative fuels. The established supply chain ensures that gasoline is delivered efficiently to a vast number of fuel stations, maintaining a stable supply to meet consumer demand.

Consumer preferences and habits also play a significant role. Drivers are accustomed to gasoline's performance characteristics and the convenience of rapid refueling, which contrasts with the longer charging times required by electric vehicles or the limited availability of alternative fuels like hydrogen. Regulatory frameworks and government policies have historically supported the gasoline market through subsidies and infrastructure investments, further entrenching its dominance. While there is a growing shift towards more sustainable fuel options, gasoline remains the primary fuel source for vehicles, ensuring its continued prevalence in the Fuel Station Market.

Fuel Station Market: Regional Analysis

North America dominated the Fuel Station Market in the year 2025. North America's dominance in the fuel station market. The extensive and well-developed road network in North America, particularly in the United States and Canada, has necessitated a large number of fuel stations to support the high volume of vehicular traffic. The U.S. boasts over 4 million miles of public roads, which underpin a significant demand for fuel and associated services.

North America has a high vehicle ownership rate, with the U.S. alone having around 276 million registered vehicles as of 2025. This translates into a substantial demand for gasoline and diesel, driving the proliferation of fuel stations. The preference for larger vehicles, such as SUVs and trucks, which generally consume more fuel, further amplifies this demand. North America, with its robust economy and high disposable income levels, has seen a historical preference for personal vehicle use over public transportation. This cultural inclination towards car ownership and frequent use has boosted the growth of the fuel station market.

North America is home to some of the world's largest oil and gas companies, which have established a vast network of refineries and distribution channels. This infrastructure ensures a steady and reliable supply of fuel, reinforcing the region's dominance in the market. Regulatory policies have also historically supported the fuel industry. Government investments in highway construction and maintenance, along with subsidies for oil production, have created a conducive environment for the growth of the Fuel Station Market.

|

Fuel Station Market Scope |

|

|

Market Size in 2025 |

USD 94.48 Bn. |

|

Market Size in 2032 |

USD 121.02 Bn. |

|

CAGR (2026-2032) |

3.6 % |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segments |

By Fuel Gasoline Diesel Gas Others |

|

By End User Road Transport Vehicle Air Transport Vehicle Water Transport Vehicle |

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Russia, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Players in the Fuel Station Market

North America Fuel Station Market Giants

- Southern Company (USA)

- ExxonMobil (USA)

- ConocoPhillips (USA)

- Chevron (USA)

- Duke Energy (USA)

- Enbridge (Canada)

Europe Fuel Station Market Key Players

- Shell (Netherlands)

- TotalEnergies (France)

- Gazprom (Russia)

- BP (UK)

- Rosneft (Russia)

- Equinor (Norway)

- Novatek (Russia)

- Petrobras (Brazil)

- Lukoil (Russia)

Asia Pacific Fuel Station Industry Leaders

- CNOOC (China)

- PetroChina (China)

- Sinopec (China)

Frequently Asked Questions

As incomes rise, consumers are more likely to purchase vehicles and use fuel stations, driving demand for fuel stations.

Investors can capitalize on opportunities in the Fuel Station market by focusing on companies that are leading in innovation trends such as advanced technology adoption. Additionally, investing in companies with strong distribution channels and a growing online retail presence can offer the potential for growth as the market grows globally.

The Market size was valued at USD 94.48 Billion in 2025 and the total Market revenue is expected to grow at a CAGR of 3.6 % from 2026 to 2032, reaching nearly USD 121.02 Billion.

The segments covered in the market report are, Fuel, End User, and region.

1. Fuel Station Market: Research Methodology

1.1. Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market breakdown and Data Triangulation

1.4. Assumptions

2. Fuel Station Market: Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026 – 2032) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Fuel Station Market: Competitive Landscape

3.1. Stellar Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Business Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. Developments and Innovations

4. Fuel Station Market: Dynamics

4.1. Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Market Drivers

4.3. Market Restraints

4.4. Market Opportunities

4.5. Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factors

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Regulatory Landscape

4.9.1. Market Regulation by Region

4.9.1.1. North America

4.9.1.2. Europe

4.9.1.3. Asia Pacific

4.9.1.4. Middle East and Africa

4.9.1.5. South America

4.9.2. Impact of Regulations on Market Dynamics

4.9.3. Government Schemes and Initiatives

5. Fuel Station Market Size and Forecast by Segments (by Value USD Million)

5.1. Fuel Station Market Size and Forecast, By Fuel (2025-2032)

5.1.1. Gasoline

5.1.2. Diesel

5.1.3. Gas

5.1.4. Others

5.2. Fuel Station Market Size and Forecast, By End User (2025-2032)

5.2.1. Road Transport Vehicle

5.2.2. Air Transport Vehicle

5.2.3. Water Transport Vehicle

5.3. Fuel Station Market Size and Forecast, by Region (2025-2032)

5.3.1. North America

5.3.2. Europe

5.3.3. Asia Pacific

5.3.4. Middle East and Africa

5.3.5. South America

6. North America Fuel Station Market Size and Forecast (by Value USD Million)

6.1. North America Fuel Station Market Size and Forecast, By Fuel (2025-2032)

6.1.1. Gasoline

6.1.2. Diesel

6.1.3. Gas

6.1.4. Others

6.2. North America Fuel Station Market Size and Forecast, By End User (2025-2032)

6.2.1. Road Transport Vehicle

6.2.2. Air Transport Vehicle

6.2.3. Water Transport Vehicle

6.3. North America Fuel Station Market Size and Forecast, by Country (2025-2032)

6.3.1. United States

6.3.2. Canada

6.3.3. Mexico

7. Europe Fuel Station Market Size and Forecast (by Value USD Million)

7.1. Europe Fuel Station Market Size and Forecast, By Fuel (2025-2032)

7.2. Europe Fuel Station Market Size and Forecast, By End User (2025-2032)

7.3. Europe Fuel Station Market Size and Forecast, by Country (2025-2032)

7.3.1. UK

7.3.2. France

7.3.3. Germany

7.3.4. Italy

7.3.5. Spain

7.3.6. Sweden

7.3.7. Austria

7.3.8. Rest of Europe

8. Asia Pacific Fuel Station Market Size and Forecast (by Value USD Million)

8.1. Asia Pacific Fuel Station Market Size and Forecast, By Fuel (2025-2032)

8.2. Asia Pacific Fuel Station Market Size and Forecast, By End User (2025-2032)

8.3. Asia Pacific Fuel Station Market Size and Forecast, by Country (2025-2032)

8.3.1. China

8.3.2. S Korea

8.3.3. Japan

8.3.4. India

8.3.5. Australia

8.3.6. Indonesia

8.3.7. Malaysia

8.3.8. Vietnam

8.3.9. Taiwan

8.3.10. Bangladesh

8.3.11. Pakistan

8.3.12. Rest of Asia Pacific

9. Middle East and Africa Fuel Station Market Size and Forecast (by Value USD Million)

9.1. Middle East and Africa Fuel Station Market Size and Forecast, By Fuel (2025-2032)

9.2. Middle East and Africa Fuel Station Market Size and Forecast, By End User (2025-2032)

9.3. Middle East and Africa Fuel Station Market Size and Forecast, by Country (2025-2032)

9.3.1. South Africa

9.3.2. GCC

9.3.3. Egypt

9.3.4. Nigeria

9.3.5. Rest of ME&A

10. South America Fuel Station Market Size and Forecast (by Value USD Million)

10.1. South America Fuel Station Market Size and Forecast, By Fuel (2025-2032)

10.2. South America Fuel Station Market Size and Forecast, By End User (2025-2032)

10.3. South America Fuel Station Market Size and Forecast, by Country (2025-2032)

10.3.1. Brazil

10.3.2. Argentina

10.3.3. Rest of South America

11. Company Profile: Key players

11.1. Southern Company (USA)

11.1.1. Company Overview

11.1.2. Business Portfolio

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. ExxonMobil (USA)

11.3. ConocoPhillips (USA)

11.4. Chevron (USA)

11.5. Duke Energy (USA)

11.6. Enbridge (Canada)

11.7. Shell (Netherlands)

11.8. TotalEnergies (France)

11.9. Gazprom (Russia)

11.10. BP (UK)

11.11. Rosneft (Russia)

11.12. Equinor (Norway)

11.13. Novatek (Russia)

11.14. Petrobras (Brazil)

11.15. Lukoil (Russia)

11.16. CNOOC (China)

11.17. PetroChina (China)

11.18. Sinopec (China)

12. Key Findings

13. Industry Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook