Europe Wireless Display Market Size, Share, Growth Trends, Research Insights, Industry Analysis and Forecast (2025–2032)

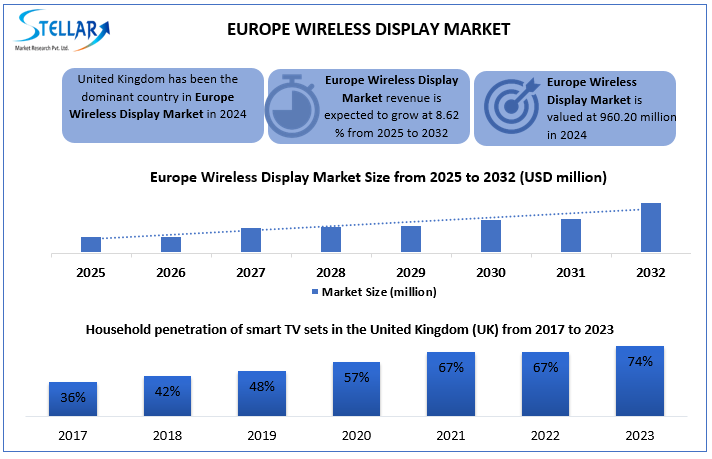

The Europe Wireless Display Market size was valued at USD 960.20 million in 2024 and the total Europe Wireless Display revenue is expected to grow at a CAGR of 8.62% from 2025 to 2032, reaching nearly USD 1860.54 million by 2032.

Europe Wireless Display Market Overview

A wireless display refers to technology that allows users to transmit video, audio, and other multimedia content from a device, such as a smartphone, tablet, laptop, or computer, to a display screen, such as a TV, monitor, or projector, without the need for physical cables or wires. This technology typically uses wireless communication protocols like Wi-Fi, Bluetooth, or proprietary standards like Miracast, Google Cast, or Apple's AirPlay. Wireless displays are commonly used in both consumer and professional settings to enable easy content sharing, presentations, and media streaming.

The convenience of wireless displays lies in their ability to eliminate the clutter of cables while providing a seamless, user-friendly experience for displaying content across different devices and platforms. In 2024, Lenovo Group Limited made significant strides in the Europe wireless display market by introducing new laptops and tablets with enhanced wireless display capabilities, powered by advanced Wi-Fi 6 and Wi-Fi 6E technology for faster and more reliable connections. The company also upgraded its proprietary software, such as Lenovo Smart Display and Lenovo Connect, to provide a more seamless user experience, enabling effortless content projection from Lenovo devices to larger screens.

To get more Insights: Request Free Sample Report

Europe Wireless Display Market Dynamics

The Driving Force Behind Europe's Wireless Display Market

The growing popularity of smart and connected TVs is a major driving factor for the Europe wireless display market. Consumers are increasingly seeking televisions that offer more than traditional programming, with the ability to connect to the internet and access a wide range of content. This trend is evident globally, with the United States expecting to see connected TV ownership reach approximately 115 million households by 2024. In Europe, the market is equally dynamic. For instance, in the United Kingdom, the penetration rate of smart TV sets surged to nearly 75 percent in 2023. In Germany, almost all TVs sold in the same year were smart, indicating a strong consumer preference for these advanced devices.

As technology advances and devices improve, the Europe Wireless Display industry must continuously innovate in the TV Sector to remain competitive. Manufacturers are compelled to introduce new models with cutting-edge functionalities to capture the interest of consumers. Smart TVs, capable of running apps and accessing the internet, are now a common feature in many UK households. Ownership has dramatically increased from 36 percent in 2017 to nearly 74 percent in 2023. These connected devices offer much more than traditional TVs, with a significant portion of UK residents using them to go online, accounting for 26 percent of their total online time. The demand for smart and Ultra HD TVs is robust, as evidenced by the fourth quarter of 2018 when 76.5 percent of all televisions shipped in Western Europe were Smart TVs, and 63 percent were Ultra High-Definition sets.

Innovation and Consumer Demand for TVs have bolstered the Europe Wireless Display Industry

The high penetration rates and growing shipment figures for smart and Ultra HD TVs underscore the transformative impact of these technologies on the Europe Wireless Display market. The rising demand for enhanced viewing experiences is pushing the boundaries of innovation in the Europe Wireless Display Market. Consumers are no longer satisfied with basic television functions; they seek devices that integrate seamlessly with their digital lifestyles. This shift is driving manufacturers to focus on developing wireless display technologies that offer greater convenience and connectivity.

The Europe Wireless Display Market's rapid growth reflects a broader trend towards interconnected, smart home environments. As more households adopt these devices, the need for advanced wireless display solutions becomes increasingly critical. This creates a fertile ground for the growth of the Europe Wireless Display market, driven by the desire for high-quality, versatile viewing experiences. The industry’s future lies in its ability to adapt to evolving consumer preferences and technological advancements, ensuring that smart TVs and wireless displays continue to dominate the consumer electronics landscape.

Europe Wireless Display Market Regional Analysis

The Europe Wireless Display Market is experiencing significant growth in both the United Kingdom and Germany, driven by several key factors. In the United Kingdom, the adoption of wireless displays has surged due to the increasing demand for flexible and seamless connectivity in both professional and consumer settings. Businesses are increasingly integrating wireless display solutions for collaborative work environments, allowing for more efficient meetings and presentations without the need for physical connections. The rise of remote work and hybrid work models has further fueled this demand, as organizations seek to enhance productivity with reliable and user-friendly display technology.

In Germany, the market is also booming, supported by the country's strong emphasis on technological innovation and smart home integration. The German market is witnessing a growing trend in the adoption of wireless displays within smart home ecosystems, where consumers prioritize convenience and connectivity. The education sector in Germany has also been a significant contributor to the market's growth, with educational institutions increasingly investing in wireless display technology to enhance interactive learning experiences. These countries are benefiting from advancements in wireless display technologies, such as improved connectivity standards like Wi-Fi 6 and the proliferation of 5G networks, which are making wireless displays more reliable and efficient. As these trends continue, the wireless display market in the United Kingdom and Germany is expected to increase further, catering to the evolving needs of both businesses and consumers in the Europe Wireless Display Market.

Europe Wireless Display Market Segment Analysis

Based on Offerings, into two notable categories hardware and software services. In 2024, the hardware segment held a dominant position in the Europe wireless display market, capturing 63.9% of the market share. This dominance can be attributed to the growing demand for physical devices that facilitate wireless display capabilities, such as receivers, transmitters, and adapters. Hardware components are crucial for ensuring seamless connectivity and high-quality display outputs, making them indispensable in the wireless display ecosystem. The hardware segment is also projected to grow at a robust CAGR of XX% during the forecast period, driven by continuous advancements in technology and the increasing adoption of smart TVs and other wireless display-enabled devices. The rising trend of home automation and the growing preference for high-definition viewing experiences are further propelling the demand for wireless display hardware across Europe.

Instead, software services, while not as dominant as hardware, play a critical role in enhancing the functionality and user experience of wireless display solutions in the Europe Wireless Display Market. Software services include applications and platforms that enable smooth content sharing, remote management, and integration with various operating systems and devices. As the market evolves, the importance of software services is expected to grow, complementing the hardware segment and driving overall market expansion. The synergy between hardware and software offerings is essential for providing comprehensive wireless display solutions that cater to diverse consumer and commercial needs in the European market.

Based on application, the Europe wireless display market is divided into consumer and commercial segments. The consumer segment, which encompasses individual users and households, is projected to dominate the market, holding 57.5% of the market share in 2018. This dominance is largely driven by the increasing popularity of smart and connected TVs, which enable users to stream content wirelessly from various devices. The growing trend of cord-cutting, where consumers shift away from traditional cable and satellite TV services in favor of streaming services, is significantly contributing to the consumer segment's growth. Additionally, the rise of smart homes, where wireless display solutions integrate with other smart devices, is further enhancing the appeal of consumer wireless display applications.

The commercial segment is further sub-segmented into corporate and broadcast, digital signage, education, healthcare, and government. Among these, the corporate and broadcast sub-segment is experiencing significant growth due to the increasing need for efficient presentation and collaboration tools in business environments. Wireless display solutions are becoming essential in modern offices and conference rooms, facilitating seamless sharing of information and enhancing productivity. Similarly, digital signage applications are gaining traction in retail and advertising, providing dynamic and engaging content delivery. In education, wireless displays are transforming classrooms by enabling interactive and collaborative learning experiences. The healthcare and government sectors are also adopting wireless display technologies to improve communication, training, and operational efficiency that boosting the sales growth in the Europe Wireless Display Market.

Europe Wireless Display Market Competitive Analysis

In 2024, Samsung Electronics, LG Electronics, and Sony Corporation emerged as the dominant players in the European wireless display market, each leveraging its unique strengths to capture market share and drive innovation. Samsung Electronics maintained its competitive edge through a series of strategic product launches and technological advancements. The company introduced its latest series of wireless smart monitors and interactive displays, featuring enhanced connectivity options such as Wi-Fi 6 and improved integration with smart home ecosystems. Samsung's emphasis on high-resolution displays and advanced features positioned it as a leader in both consumer and commercial wireless display segments. Additionally, Samsung's robust marketing strategies and strong distribution network have bolstered its market presence in Europe.

LG Electronics focused on increasing its portfolio with new wireless display solutions tailored for both home entertainment and professional environments. In 2024, LG launched its latest range of wireless smart TVs and interactive displays, incorporating innovations such as advanced wireless projection capabilities and seamless integration with LG's smart home ecosystem. The company’s emphasis on OLED technology and superior picture quality has strengthened its position in the high-end market segment. LG's strategic partnerships and collaborations with tech firms have further enhanced its market reach and product offerings in the Europe Wireless Display Market. Meanwhile, Sony Corporation has made significant strides in the wireless display market by introducing new wireless projectors and interactive flat panels designed for education and corporate settings. Sony’s emphasis on high-performance imaging and connectivity has resonated well with enterprise and educational customers. The company's acquisitions in the display technology sector, aimed at enhancing its product capabilities and escalating its market share, have played a crucial role in solidifying its competitive position in Europe.

In Conclusion, To remain competitive in the European wireless display market, companies should focus on continuous innovation, particularly in integrating advanced features like Wi-Fi 6 and 5G, while enhancing user experience through seamless software. Leading players like Samsung, LG, and Sony are driving growth by launching cutting-edge products and forming strategic partnerships. As demand for smart and connected TVs rises, especially in consumer and commercial sectors, ongoing R&D in wireless connectivity and user-centric solutions will be crucial for sustaining market leadership.

|

Europe Wireless Display Market Scope |

|

|

Market Size in 2024 |

USD 960.20 billion. |

|

Market Size in 2032 |

USD 1860.54 billion. |

|

CAGR (2025-2032) |

8.62% |

|

Historic Data |

2019-2024 |

|

Base Year |

2024 |

|

Forecast Period |

2025-2032 |

|

Segments |

By Offering Hardware Software |

|

By Technology Wi-Fi Bluetooth Wireless HD Others |

|

|

By Application Consumer Electronics Corporate & Broadcast Digital Signage Government Healthcare Education Industrial Others |

|

|

Regional Scope |

Europe – UK, France, Germany, Italy, Spain, Sweden, Russia, and Rest of Europe |

Key Players in the Europe Wireless Display Market

- Samsung Electronics Co., Ltd. (Suwon, South Korea)

- LG Electronics Inc. (Seoul, South Korea)

- Sony Corporation (Tokyo, Japan)

- Panasonic Corporation (Osaka, Japan)

- Huawei Technologies Co., Ltd. (Shenzhen, China)

- Xiaomi Corporation (Beijing, China)

- Toshiba Corporation (Tokyo, Japan)

- Sharp Corporation (Osaka, Japan)

- Google LLC (Tokyo, Japan)

- Apple Inc. (Shanghai, China)

- Microsoft Corporation (Beijing, China)

- ASUSTeK Computer Inc. (Taipei, Taiwan)

- Lenovo Group Limited (Beijing, China)

- BenQ Corporation (Taipei, Taiwan)

- Acer Inc. (New Taipei, Taiwan)

- Hisense Group (Qingdao, China)

- Vizio Inc. (Shenzhen, China)

- Roku, Inc. (Shanghai, China)

- Intel Corporation (Beijing, China)

- Qualcomm Technologies, Inc. (Shanghai, China)

Frequently Asked Questions

Ans: Wi-Fi technology dominates due to its effective wireless connectivity and content sharing.

Ans: Consumer Electronics, driven by smart TVs and streaming devices

Ans: Advanced Wi-Fi standards, innovation in display technologies, and rising adoption in smart cities and entertainment.

Ans: Google launched Chromecast with Google TV in March 2024.

- Europe Wireless Display Market: Research Methodology

- Europe Wireless Display Market Introduction

- Study Assumption and Market Definition

- Scope of the Study

- Executive Summary

- Europe Wireless Display Market: Competitive Landscape

- SMR Competition Matrix

- Competitive Landscape

- Key Players Benchmarking

- Company Name

- Product Segment

- End-user Segment

- Revenue (2024)

- Company Headquarter

- Market Structure

- Market Leaders

- Market Followers

- Emerging Players

- Mergers and Acquisitions Details

- Europe Wireless Display Market: Dynamics

- Semiconductor Memory Market Trends

- Semiconductor Memory Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- PORTER’s Five Forces Analysis

- PESTLE Analysis

- Application Roadmap

- Regulatory Landscape

- Europe Wireless Display Market Size and Forecast by Segmentation (Value in USD Million) (2024-2032)

- Europe Wireless Display Market Size and Forecast, By Offering (2024-2032)

- Hardware

- Software

- Europe Wireless Display Market Size and Forecast, By Technology (2024-2032)

- Wi-Fi

- Bluetooth

- Wireless HD

- Others

- Europe Wireless Display Market Size and Forecast, By Application (2024-2032)

- Consumer Electronics

- Corporate & Broadcast

- Digital Signage

- Government

- Healthcare

- Education

- Industrial

- Others

- Europe Wireless Display Market Size and Forecast, by Country (2024-2032)

- China

- S Korea

- Japan

- India

- Australia

- ASEAN

- Europe Wireless Display Market Size and Forecast, By Offering (2024-2032)

- Company Profile: Key Players

- Samsung Electronics Co., Ltd. (Suwon, South Korea)

- Company Overview

- Business Portfolio

- Financial Overview

- SWOT Analysis

- Strategic Analysis

- Recent Developments

- LG Electronics Inc. (Seoul, South Korea)

- Sony Corporation (Tokyo, Japan)

- Panasonic Corporation (Osaka, Japan)

- Huawei Technologies Co., Ltd. (Shenzhen, China)

- Xiaomi Corporation (Beijing, China)

- Toshiba Corporation (Tokyo, Japan)

- Sharp Corporation (Osaka, Japan)

- Google LLC (Tokyo, Japan)

- Apple Inc. (Shanghai, China)

- Microsoft Corporation (Beijing, China)

- ASUSTeK Computer Inc. (Taipei, Taiwan)

- Lenovo Group Limited (Beijing, China)

- BenQ Corporation (Taipei, Taiwan)

- Acer Inc. (New Taipei, Taiwan)

- Hisense Group (Qingdao, China)

- Vizio Inc. (Shenzhen, China)

- Roku, Inc. (Shanghai, China)

- Intel Corporation (Beijing, China)

- Qualcomm Technologies, Inc. (Shanghai, China)

- Samsung Electronics Co., Ltd. (Suwon, South Korea)

- Key Findings

- Industry Recommendations