Containerboard Market Size, Share & Forecast (2026-2032) Sustainability & E-Commerce Demand

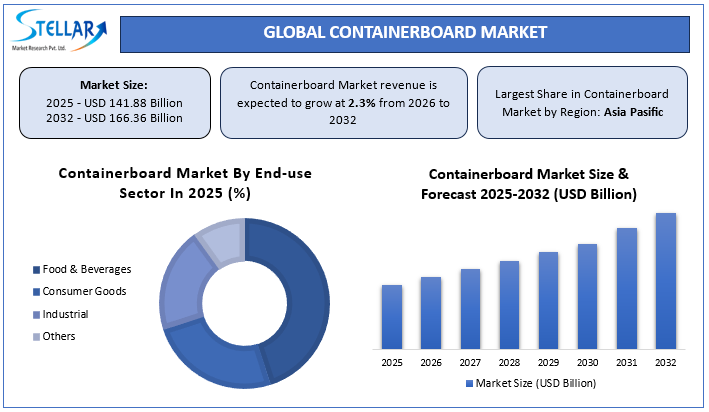

Global Containerboard Market size was USD 141.88 Billion in 2025 and is forecast to reach USD 166.36 Billion by 2032, with a CAGR of 2.3%, driven by increasing e-commerce shipments and demand for durable, recyclable packaging.

Global Containerboard Market Overview:

Containerboard is a paper-based material made from virgin or recycled fibers, used mainly to produce corrugated boxes. Global Containerboard Market size was USD 141.88?Billion in 2025 and is forecast to reach USD 166.36?Billion by 2032, with a CAGR of 2.3%. It provides strength, protection, and recyclability, making it essential for packaging, shipping, and e-commerce while supporting sustainable and circular packaging systems. Global Containerboard Market is driven by sustainable packaging policies, high recycling rates, and rising e-commerce demand. Strong circular economy frameworks in North America and Europe, combined with expanding packaging infrastructure in Asia Pacific, support long-term stability. Regulatory compliance and strategic investments reinforce positive size, share, trends, and forecast fundamentals.

Key Highlights

- High recycling rates and EU/US packaging directives position containerboard as a sustainable, circular packaging solution.

- Asia Pacific leads the market with industrialization and manufacturing infrastructure, while North America benefits from mature recycling systems and regulatory support.

- Advances in pulping technologies, automation, and sustainable production enhance efficiency and reduce environmental impact in containerboard manufacturing.

- Recycled fibers dominate production, and the food & beverage sector drives consistent end-use demand aligned with sustainability policies.

- Strategic investments, policy incentives, and expanding packaging infrastructure support long-term containerboard market growth, size, share, trends, and forecast.

To get more Insights: Request Free Sample Report

Sustainable Containerboard and Circular Packaging Leadership in Containerboard Market

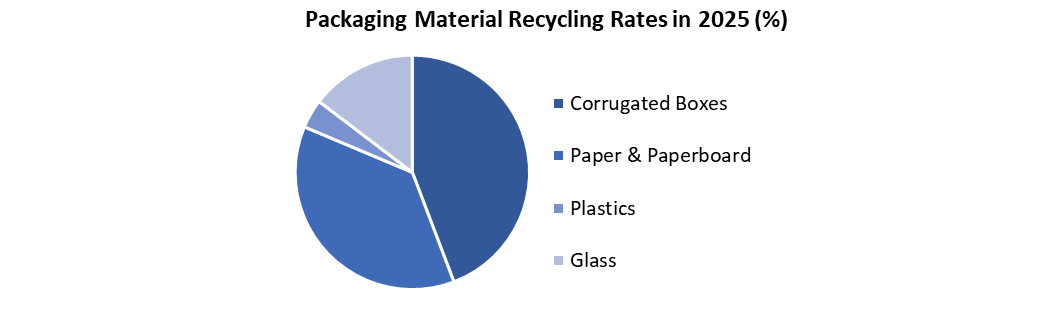

- Sustainability & Eco-Friendly Packaging: Containerboard is a highly recycled and sustainable packaging solution, aligned with circular economy policies in North America and Europe.

- U.S. EPA 2018: Corrugated boxes recycled at 96.5%, overall paper and paperboard packaging at 80.9%.

- AF&PA: Nearly 33 million tons of cardboard are recycled annually in the U.S., with recycling rates between 69-74%.

- EU 2023: Paper and cardboard constitute 40.4% of total packaging waste; strict directives like the Packaging and Packaging Waste Directive reinforce recyclability.

Rising E-Commerce Shipments Fuel Containerboard Demand

The sustained growth of online retail is a key driver of containerboard demand, as increasing e-commerce activity elevates the need for durable, protective packaging solutions.

In the U.S., e-commerce sales accounted for 16.4% of total retail in 2025, valued at USD 310.3?Billion, while USPS delivered 127.3?Billion parcels in FY2022.

Rising parcel volumes and consumer demand for reliable shipping directly support containerboard utilization. Growth of online retail directly drives containerboard demand.

E-Commerce Expansion Accelerates Containerboard Demand

Containerboard increasingly serves as a strategic branding and marketing medium, supported by mandatory labelling and compliance requirements across major economies. Its printable surface enables brand storytelling, regulatory transparency, and sustainability messaging, aligning packaging with consumer expectations for clarity, traceability, and environmentally responsible communication.

- U.S. Fair Packaging & Labelling Act supports standardized on-pack information display.

- India FSSAI mandates detailed food labelling and traceability.

- EU labelling directives reinforce compliance, visibility, and consumer information standards.

Containerboard as a Strategic Branding and Compliance Tool

Despite sustainability momentum, alternative packaging materials such as plastics, glass, and metals continue to maintain market presence due to entrenched supply chains, cost efficiencies, and long-standing consumer acceptance. Regulatory frameworks across major economies ensure functional equivalence among packaging materials, preventing rapid displacement and sustaining competitive pressure on fiber-based solutions.

U.S. EPA 2018: Plastics 14.5% of total waste, recycling rate only 8.7%, highlighting competitive pressure.

EU Packaging Regulations ensure functional equivalence for all materials, maintaining alternative material presence.

Global Containerboard Market Segmentation Analysis

The material and end-use segments define the structural strength of the Global Containerboard Market, reflecting both supply-side circularity and demand-side consumption stability. Together, they underpin long-term size, share, trends, and forecast dynamics.

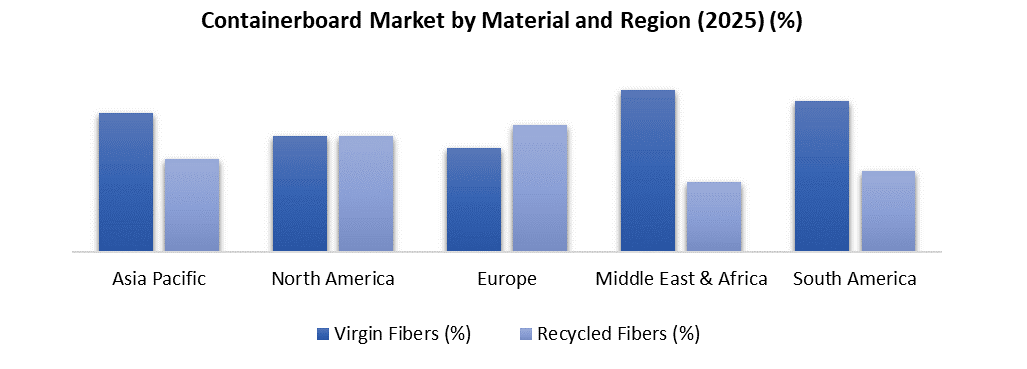

Containerboard Market Size by Material: Recycled fibers dominate containerboard production due to high recovery rates and strong circular economy systems, with North America leading this segment through robust recycling infrastructure, regulatory alignment, and consistent recovered fiber supply.

Containerboard Market size by End-Use:

Food and beverages remain the largest containerboard end-use segment, driven by continuous packaging demand for essential goods, with Europe emerging as a dominant region due to high paper-based packaging share and regulated food logistics systems.

Global Containerboard Market Regional Insights

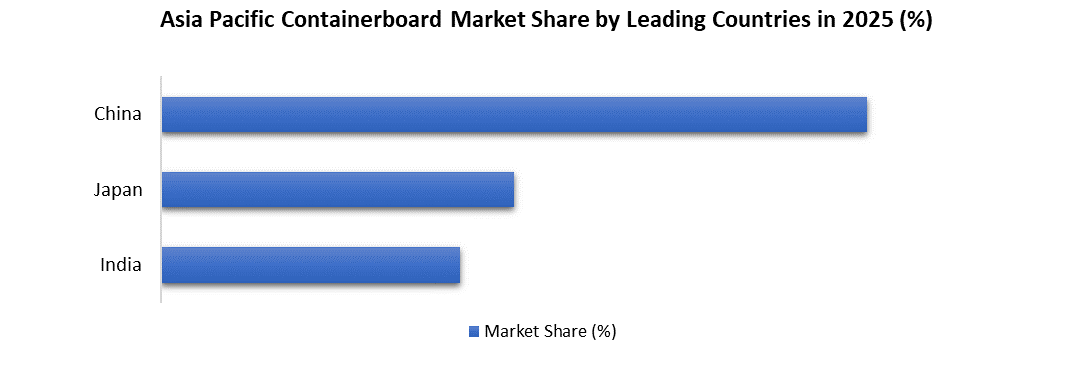

Asia Pacific held the largest market share in 2025, it is the leading centre for paper and cardboard usage, driven by rapid industrialisation and the growth of rising consumer markets.

- Sustainability & Zero-Waste Policies: Paper and cardboard represent 46.8?% of zero-waste packaging revenue in 2024, reflecting strong alignment with recyclable, fiber-based containerboard solutions.

- Manufacturing Infrastructure: The region hosts the majority of global paper packaging plants, ensuring robust production capacity and steady containerboard input supply.

- Investment Implication: Policy focus on sustainable materials and large-scale packaging consumption supports long-term capital allocation in containerboard manufacturing, recycling, and fiber recovery systems.

Global Leaders Strengthening Scale and Sustainability in Containerboard

- International Paper: Nearly 37,000 employees; global operations across North America, Europe, Latin America, and North Africa; completed strategic acquisition in 2025 to expand sustainable containerboard production.

- Smurfit Westrock: Nearly 100,000 employees, 500+ facilities in 40 countries; integrates recycled fiber and circular economy principles; operational scale supports global supply and ESG-aligned investment strategies.

Global Containerboard Market Recent Developments

|

Company |

Year |

Recent Development |

|

International Paper |

2025 |

Completed acquisition of DS Smith, issuing Nearly 179.85 million shares; transaction expected to deliver synergies of USD 0.514?Billion; expanded operations across 30+ countries; divestment of five European plants to satisfy regulatory requirements. |

|

Smurfit Westrock |

2025 |

Third-quarter net sales of USD 8.003?Billion, net income USD 0.245?Billion, adjusted EBITDA USD 1.302?Billion, with net cash from operations USD 1.133?Billion; first-quarter net sales USD 7.656?Billion, net income USD 0.382?Billion, adjusted EBITDA USD 1.252?Billion; successful post-merger integration and operational synergies. |

|

Packaging Corporation of America (PCA) |

2025 |

Third-quarter net sales USD 2.3?Billion, net income USD 0.227?Billion; permanent shutdown of No. 2 paper machine and kraft pulping (Nearly 0.25?Million tons capacity reduction); streamlining operations to improve cost competitiveness. |

|

Sappi Ltd |

2025 |

Issued sustainability-linked senior notes of USD 0.3?Billion; strengthened balance sheet and ESG strategy; recognized for sustainability performance and transparent reporting. |

|

Nippon Paper Industries |

2025 |

Published Integrated Report and ESG Databook 2025; advanced R&D initiatives for bioethanol from woody biomass; management restructuring to support strategic growth and sustainability objectives. |

Global Containerboard Market Scope:

|

Global Containerboard Market |

|||

|

Report Coverage |

Details |

||

|

Base Year: |

2025 |

Forecast Period: |

2026-2032 |

|

Historical Data: |

2020 to 2025 |

Market Size in 2025: |

USD 141.88 Billion |

|

Forecast Period 2026 to 2032 CAGR: |

2.3% |

Market Size in 2032: |

USD 166.36 Billion |

|

Global Containerboard Market Segment Analysis |

By Type |

Kraftliners Testliners Flutings |

|

|

By Material |

Virgin Fibers Recycled Fibers |

||

|

By End-user |

Food & Beverages Consumer Goods Industrial Others |

||

Global Containerboard Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Global Containerboard Market Key Players

- Mondi Group

- Smurfit Kappa

- International Paper

- WestRock Company

- Rengo Co. Ltd.

- Georgia-Pacific LLC

- Hamburger Containerboard

- Nine Dragon Paper

- Stora Enso

- DS Smith plc

- Oji Fibre Solutions (NZ) Limited

- Independent Paperboard Marketing

- Corrboard UK Ltd

- Atlantic Packaging Products Ltd.

- Aviretta GmbH

- International Forest Products (IFP)

- Eltracom

- Packaging Corporation of America (PCA)

- Cascades Inc.

- Sappi Ltd

- Nippon Paper Industries Corporation

- Pratt Industries Inc.

- Sonoco Products Company

- KapStone Paper and Packaging Corporation

- Klabin S.A.

- Others

Regional Breakdown:

Asia-Pacific Containerboard Market - Industry Analysis and Forecast (2024-2030)

North America Containerboard Market: Industry Analysis and Forecast (2024-2030)

Frequently Asked Questions

Growth is driven by sustainable packaging regulations, high recycling rates, expanding e-commerce shipments, and strong circular economy frameworks across major regions

Asia Pacific leads the market due to rapid industrialization, large-scale packaging consumption, and extensive manufacturing infrastructure.

Recycled fibers ensure cost efficiency, regulatory compliance, and supply stability while supporting circular economy and sustainability goals.

Rising online retail and parcel shipments are increasing demand for durable corrugated packaging, reinforcing positive market size, share, trends, and forecast outlook.

- 1. Containerboard Market Introduction

1.1. Study Assumption and Market Definition

1.2. Scope of the Study

1.3. Executive Summary

- 2. Global Containerboard Market: Competitive Landscape

- 2.1. SMR Competition Matrix

2.2. Competitive Landscape

2.3. Key Players Benchmarking

2.3.1. Company Name

2.3.2. Product

2.3.3. End-user

2.3.4. Revenue (2025)

2.3.5. Profit Margin

2.3.6. Revenue Growth

2.3.7. Geographical Locations

2.4. Market Structure

2.4.1. Market Leaders

2.4.2. Market Followers

2.4.3. Emerging Players

2.5. Mergers and Acquisitions Details

- 3. Containerboard Market: Dynamics

3.1. Containerboard Market Trends

3.2. Containerboard Market Dynamics

3.2.1. North America

3.2.2. Europe

3.2.3. Asia Pacific

3.2.4. Middle East and Africa

3.2.5. South America

3.3. PORTER’s Five Forces Analysis

3.4. PESTLE Analysis

4. Technological Advancements and Product Innovation in the Containerboard Market

4.1. Innovations in linerboard and corrugating medium manufacturing technologies

4.2. Advancements in recycled fiber processing and strength optimization

4.3. Light-weighting technologies and high-performance containerboard grades

4.4. Automation, AI, and Industry 4.0 adoption in containerboard production

4.5. Development of specialty, coated, and high-burst containerboard products

5. Global Containerboard Market Pricing Analysis (2020–2025)

5.1. Global containerboard price trends by product type (linerboard and medium)

5.2. Raw material cost structure including recycled fiber, virgin fiber, energy, and chemicals

5.3. Regional price variations driven by demand–supply balance

5.4. Price sensitivity across developed and emerging economies

5.5. Pricing premiums for sustainable, certified, and lightweight containerboard

6. Policy and Regulatory Environment for the Containerboard Market

6.1. Environmental regulations governing emissions, water use, and waste

6.2. Packaging waste, recycling, and circular economy regulations

6.3. Forestry, recycled content, and chain-of-custody certifications

6.4. Trade policies, tariffs, and compliance requirements affecting containerboard

7. Role of the Containerboard Market in the Circular Economy

7.1. Integration of recycled fiber and closed-loop packaging systems

7.2. Contribution of containerboard to sustainable packaging goals

7.3. Environmental and economic benefits of recyclable paper-based packaging

7.4. Industry collaboration and government initiatives supporting circularity

8. Impact of E-Commerce and Digitalization on Containerboard Market Demand

8.1. Growth of e-commerce and its influence on corrugated packaging demand

8.2. Shift from plastic to paper-based protective packaging

8.3. Digital optimization of containerboard logistics and inventory management

8.4. Long-term demand outlook driven by online retail and omnichannel trade

9. Containerboard Market: Global Market Size and Forecast by Segmentation (by Value in USD Billion) (2025-2032)

9.1. Containerboard Market Size and Forecast, by Type (2025-2032)

9.1.1. Kraftliners

9.1.2. Testliners

9.1.3. Flutings

9.2. Containerboard Market Size and Forecast, by Material (2025-2032)

9.2.1. Virgin Fibers

9.2.2. Recycled Fibers

9.3. Containerboard Market Size and Forecast, by End-User (2025-2032)

9.3.1. Food & Beverages

9.3.2. Consumer Goods

9.3.3. Industrial

9.3.4. Others

9.4. Containerboard Market Size and Forecast, by Region (2025-2032)

9.4.1. North America

9.4.2. Europe

9.4.3. Asia Pacific

9.4.4. Middle East and Africa

9.4.5. South America

10. North America Containerboard Market Size and Forecast by Segmentation (by Value in USD Billion) (2025-2032)

10.1. North America Containerboard Market Size and Forecast, by Type (2025-2032)

10.1.1. Kraftliners

10.1.2. Testliners

10.1.3. Flutings

10.2. North America Containerboard Market Size and Forecast, by Material (2025-2032)

10.2.1. Food & Beverages

10.2.2. Consumer Goods

10.2.3. Industrial

10.2.4. Others

10.3. North America Containerboard Market Size and Forecast, by End-User (2025-2032)

10.3.1. Food & Beverages

10.3.2. Consumer Goods

10.3.3. Industrial

10.3.4. Others

10.4. North America Containerboard Market Size and Forecast, by Country (2025-2032)

10.4.1. United States

10.4.2. Canada

10.4.3. Mexico

11. Europe Containerboard Market Size and Forecast by Segmentation (by Value in USD Billion) (2025-2032)

11.1. Europe Containerboard Market Size and Forecast, by Type (2025-2032)

11.2. Europe Containerboard Market Size and Forecast, by Material (2025-2032)

11.3. Europe Containerboard Market Size and Forecast, by End-User (2025-2032)

11.4. Europe Containerboard Market Size and Forecast, by Country (2025-2032)

11.4.1. United Kingdom

11.4.2. France

11.4.3. Germany

11.4.4. Italy

11.4.5. Spain

11.4.6. Sweden

11.4.7. Austria

11.4.8. Rest of Europe

12. Asia Pacific Containerboard Market Size and Forecast by Segmentation (by Value in USD Billion) (2025-2032)

12.1. Asia Pacific Containerboard Market Size and Forecast, by Type (2025-2032)

12.2. Asia Pacific Containerboard Market Size and Forecast, by Material (2025-2032)

12.3. Asia Pacific Containerboard Market Size and Forecast, by End-User (2025-2032)

12.4. Asia Pacific Containerboard Market Size and Forecast, by Country (2025-2032)

12.4.1. China

12.4.2. S Korea

12.4.3. Japan

12.4.4. India

12.4.5. Australia

12.4.6. Indonesia

12.4.7. Malaysia

12.4.8. Vietnam

12.4.9. Taiwan

12.4.10. Rest of Asia Pacific

13. Middle East and Africa Containerboard Market Size and Forecast by Segmentation (by Value in USD Billion) (2025-2032)

13.1. Middle East and Africa Containerboard Market Size and Forecast, by Type (2025-2032)

13.2. Middle East and Africa Containerboard Market Size and Forecast, by Material (2025-2032)

13.3. Middle East and Africa Containerboard Market Size and Forecast, by End-User (2025-2032)

13.4. Middle East and Africa Containerboard Market Size and Forecast, by Country (2025-2032)

13.4.1. South Africa

13.4.2. GCC

13.4.3. Egypt

13.4.4. Nigeria

13.4.5. Rest of ME&A

14. South America Containerboard Market Size and Forecast by Segmentation (by Value in USD Billion) (2025-2032)

14.1. South America Containerboard Market Size and Forecast, by Type (2025-2032)

14.2. South America Containerboard Market Size and Forecast, by Material (2025-2032)

14.3. South America Containerboard Market Size and Forecast, by End-User (2025-2032)

14.4. South America Containerboard Market Size and Forecast, by Country (2025-2032)

14.4.1. Brazil

14.4.2. Argentina

14.4.3. Chile

14.4.4. Colombia

14.4.5. Rest Of South America

15. Company Profile: Key Players

15.1. Mondi Group

15.1.1. Company Overview

15.1.2. Business Portfolio

15.1.3. Financial Overview

15.1.4. SWOT Analysis

15.1.5. Strategic Analysis

15.1.6. Recent Developments

15.2. Smurfit Kappa

15.3. International Paper

15.4. WestRock Company

15.5. Rengo Co. Ltd.

15.6. Georgia-Pacific LLC

15.7. Hamburger Containerboard

15.8. Nine Dragon Paper

15.9. Stora Enso

15.10. DS Smith plc

15.11. Oji Fibre Solutions (NZ) Limited

15.12. Independent Paperboard Marketing

15.13. Corrboard UK Ltd

15.14. Atlantic Packaging Products Ltd.

15.15. Aviretta GmbH

15.16. International Forest Products (IFP)

15.17. Eltracom

15.18. Packaging Corporation of America (PCA)

15.19. Cascades Inc.

15.20. Sappi Ltd

15.21. Nippon Paper Industries Corporation

15.22. Pratt Industries Inc.

15.23. Sonoco Products Company

15.24. KapStone Paper and Packaging Corporation

15.25. Klabin S.A.

15.26. Others

16. Key Findings

17. Industry Recommendations

18. Containerboard Market: Research Methodology