ISO Container Market Global Industry Analysis and Forecast (2026-2032)

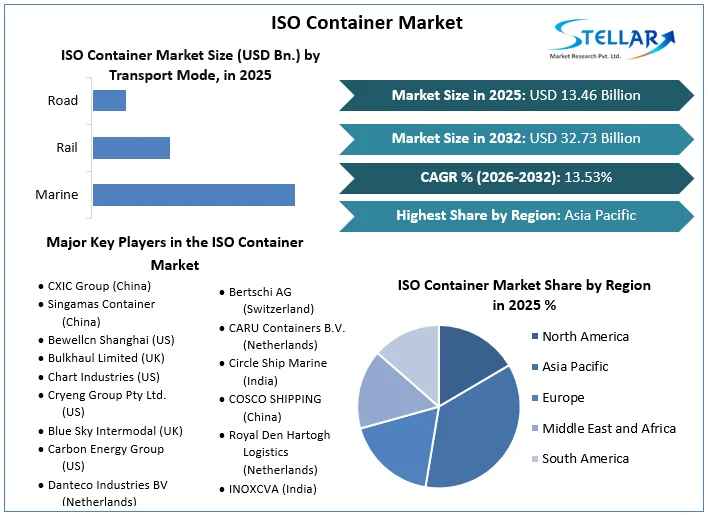

The ISO Container Market size was valued at USD 13.46 billion in 2025 and the total ISO Container Market size is expected to grow at a CAGR of 13.53% from 2026 to 2032, reaching nearly USD 32.73 billion by 2032.

ISO Container Market Overview

ISO Containers are International Intermodal containers that meet the standards specified by the International Organization for Standardization (ISO). They are cargo containers used to ship the products through trucks, boats or trains. In 2024, China broke approximately 5 trillion USD record for global trade in a single year. Thus, the growing demand for global trade and logistics drives the growth of the ISO Container market. As online shopping continues to grow which creates an increasing demand for efficient and scalable logistics solutions to handle the rising volume of packages and ensure timely delivery. Thus, expansion in the e-commerce sector and last-mile delivery solutions create a significant opportunity for the ISO Container market.

The market faces several challenges including fluctuating demand and supply chain disruption in which Business faces difficulties in adjusting their container supply in response to rapid fluctuations in demand. The market is segmented into container type, transport modes, capacity, end-use, and geographic elements. The Asia Pacific region dominates the ISO Container market. This is due to its essential role in trade and shipping worldwide. The strong container manufacturing capabilities, growing trade volumes, and vast port network are major factors that help to continue the dominance of Asia Pacific in the ISO Container market. CXIC Group, Singamas Container, Bewellcn Shanghai, Bulkhaul Limited, Chart Industries, Cryeng Group Pty Ltd., Blue Sky Intermodal, and Carbon Energy Group are most of the leading players within the ISO Container market.

To get more Insights: Request Free Sample Report

ISO Container Market Dynamics:

The Growing Demand for Global Trade and Logistics Drives the Growth of The ISO Container Market

The growing demand for global trade and logistics drives the growth of the ISO Container market. As international trade volumes continue to expand the need for efficient and reliable transportation solutions which becomes increasingly critical. ISO Containers play an important role in this supply chain. They offer standardized, durable, and versatile solutions for shipping goods. The rise in global trade is driven by various factors such as economic globalization, trade agreements, and the expansion of emerging markets. There is an increasing demand for containers that can manage a wide range of cargo types and survive a variety of environmental conditions as more businesses engage in cross-border trade. The International Maritime Organization (IMO) and other trade organizations report consistent growth in container shipping volumes. The global container fleet has been expanding with containers throughout reaching over 800 million TEUs (Twenty-foot Equivalent Units) annually. This expansion of global trade and logistics boosts the growth of the ISO Container market.

The Expansion of E-commerce and Last-Mile Delivery Solutions is a Significant Opportunity for the ISO Container Market.

The e-commerce sector and last-mile delivery solutions create a significant opportunity for the ISO Container market. As online shopping continues to grow which creates an increasing demand for efficient and scalable logistics solutions to handle the rising volume of packages and ensure timely delivery. The modular and standardized design of ISO Containers leads them to help this expanding industry. The ease of online shopping, the growth of digital payment methods, and the increase in internet usage are some of the key factors driving the growth of the e-commerce sector. A strong logistics infrastructure that can handle a variety of shipping requirements such as large shipments as well as last-mile is required for this growth. Thus, ISO containers are adopted for various uses including distribution centers and mobile fulfilment units to meet these evolving demands. Thus, the expansion of the e-commerce sector creates an opportunity for the ISO Container market. The ISO Containers offer versatile solutions for last-mile logistics such as transforming into mobile distribution centres or temporary storage units in urban areas. This helps address challenges related to congestion and space constraints in heavily populated locations improving overall delivery performance. The integration of advanced technologies such as IoT and real-time tracking increases the benefits of using ISO containers in e-commerce logistics. These technologies enable better management, monitoring, and optimization of container usage throughout the supply chain improving overall efficiency and reducing operational costs. As e-commerce continues to grow the adoption of ISO containers for these purposes is likely to increase and create a significant opportunity for market expansion.

The Fluctuation in Demand and its Effect on Supply Chain is a Major Challenge for the ISO Container Market

The fluctuation in demand affects supply chain efficiency and record management which creates a major challenge for the ISO Container market. The business faces difficulties in adjusting its container supply in response to rapid fluctuations in demand. The overcapacity led to increased storage costs and underutilization of assets while undercapacity resulted in delays and missed business opportunities. This imbalance forces container providers to constantly adjust their supply levels and operational strategies to remain competitive which strains resources and complicates logistics. The inconsistency in demand affects the pricing and availability of ISO Containers. During periods of high demand container shortages drive up prices and make it more expensive for companies to secure the containers they need. On the other hand, during periods of low demand an oversupply of containers leads to reduced rental rates and financial losses for container producers. These fluctuations can impact profitability and stability within the container market and make it challenging for producers to maintain a steady profit stream and plan long-term investments. Also, the need to rapidly adapt to changing demand conditions often requires investment in technology and infrastructure. These fluctuations in demand and their effects on the supply chain create a significant challenge for the ISO Container market.

ISO Container Market Segment Analysis:

Based on the Container Type, the market is classified as Lined Tanks, Reefer Tanks, Cryogenic & Gas Tanks, Swap Body Tanks, and Multi-Compartment Tanks. Multi-compartment tanks held the largest shares in the ISO container market. This is due to their unique versatility and efficiency in transporting several types of liquids and chemicals. These tanks are designed with multiple compartments and permit the simultaneous transportation of different products inside a single container. This characteristic of a multi-compartment tank creates an advantage for industries that need to deliver multiple substances without cross-contamination which includes food and beverage, chemicals, and other sectors. The cryogenic & Gas tanks are expected to dominate in the forecast year. This is due to their important role in handling specialized and high-volume cargo that requires strictly controlled conditions. These tanks are designed to transport liquefied gases and cryogenic fluids such as liquid nitrogen and oxygen, and natural gases at very low temperatures. Their ability to safely and efficiently manage these substances helps this segment to dominate it in the forecast year.

Based on Transport Mode Analysis the market is classified into Rail, Marine, and Road. The marine transport held the largest shares in the ISO Container market. This is due to the extensive use of containers for international trade. Marine transport is the most common mode where containers are loaded onto cargo ships. They are secured on deck and transported across oceans and seas. Marine transport is essential to worldwide supply chains and ISO containers are suited for this mode due to their standardization and suitability for handling a wide range of goods. The rail segment is expected to hold the largest shares in the forecast year. This is due to its efficiency in moving large volumes of goods over long distances. Rail systems offer a cost-effective and reliable mode of transport for ISO containers benefiting from economies of scale and the ability to handle high-capacity loads. This segment provides a continuous path for containerized cargo and also helps to minimize handling and transfer times as compared to other modes of transport. This led rail transport to dominate the ISO container market in the forecast year.

ISO Container Market Regional Insight:

Asia Pacific is the dominant region in the ISO Container market in 2025 and is expected to continue its dominance during the forecast period. The dominance is attributed to factors such as advanced research and development, a huge industrial base, government funding, and regulatory framework. This is due to its essential role in trade and shipping worldwide. The strong container manufacturing capabilities, growing trade volumes, and vast port network are major factors that help to continue the dominance of Asia Pacific in the ISO Container market. Countries like China, India, and South Korea are the leading countries in the Asia-Pacific region. China is the largest manufacturer of ISO containers in that region. CIMC is a Chinese ISO Container manufacturing leader that has introduced several advanced container designs. CIMC also uses smart technology in containers such as IoT-enabled tracking systems that provide real-time data on container conditions, location, and security. The rising industrialization, expanding international trade, and infrastructure development are the key factors driving the growth of the ISO Container market in Asia Pacific. It also focuses on the research and development sector which allows to support the market growth of ISO Container in that region.

ISO Container Market Competitive Landscape:

The market is a highly competitive global sector with many participants striving to be leaders. The prominent players operating in the ISO Container market are constantly adopting various growth strategies to survive in the market. Innovations, product launches, adoption of new technologies, collaboration, and partnership are some of the growth strategies that are adopted by these key players. In the ISO Container market, Singamas Container and Bewellcn Shanghai are the two important key players.

Singamas Container is a leading player in the ISO Container market, headquartered in Hong Kong, China. The company has developed a strong presence in the container manufacturing industry with a diverse range of container products including dry containers, refrigerated containers, and special-purpose containers. Singamas has been involved in advancing container design and technology. The company has adopted state-of-the-art manufacturing techniques and materials to improve container durability and efficiency. Singamas has united advanced corrosion-resistant coatings and improved insulation technologies in their refrigerated containers to improve performance and durability. The company produce approximately tens of thousands of containers annually. Bewellcn Shanghai is another leading player in the ISO Container market. This is due to the company’s focus on innovative container solutions. The company also focuses on advancements in the design and manufacturing of specialized containers. The company has been at the forefront of innovating new technologies into ISO containers. They developed advanced container systems that offer flexibility for various applications such as portable offices and retail units. Their containers have features such as enhanced thermal insulation and integrated smart technologies for monitoring and control. These features of Bewellcn Shanghai help it to maintain its leadership in the ISO Container market.

|

ISO Container Market Scope |

|

|

Market Size in 2025 |

USD 13.46 Bn. |

|

Market Size in 2032 |

USD 32.73 Bn. |

|

CAGR (2026-2032) |

13.53% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segments BY |

By Container Type

|

|

By Transport Mode

|

|

|

By Capacity

|

|

|

By End-User

|

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Switzerland, Netherlands, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Rest of APAC Latin America-Brazil, Argentina, Chile, Colombia Middle East and Africa - South Africa, Nigeria, Israel, Egypt, UAE, Rest of the Middle East and Africa |

Key Player in the ISO Container Market

- CXIC Group (China)

- Singamas Container (China)

- Bewellcn Shanghai (US)

- Bulkhaul Limited (UK)

- Chart Industries (US)

- Cryeng Group Pty Ltd. (US)

- Blue Sky Intermodal (UK)

- Carbon Energy Group (US)

- Danteco Industries BV (Netherlands)

- Bertschi AG (Switzerland)

- CARU Containers B.V. (Netherlands)

- Circle Ship Marine (India)

- COSCO SHIPPING (China)

- Royal Den Hartogh Logistics (Netherlands)

- INOXCVA (India)

- Tls Offshore Containers International (China)

- China International Marine Containers Co. (China)

- CIMC Furuise (China)

- M1 Engineering Holdings Limited (UK)

- Rootselaar Group (Netherlands)

Frequently Asked Questions

Asia Pacific is expected to lead the ISO Container Market during the forecast period.

The growing demand for global trade and logistics, innovations in advanced ISO Containers, and the growth of the e-commerce sector these factors are the profit outlook for companies operating in the ISO Container market.

The ISO Container Market size was valued at USD 13.46 billion in 2025 and the total ISO Container Market size is expected to grow at a CAGR of 13.53% from 2026 to 2032, reaching nearly USD 32.73 billion by 2032.

The segments covered in the market report are by Container Type, by Transport Modes, by Capacity, and by End User.

1. ISO Container Market: Research Methodology

2. ISO Container Market: Executive Summary

3. ISO Container Market: Competitive Landscape

4. Potential Areas for Investment

4.1. Stellar Competition Matrix

4.2. Competitive Landscape

4.3. Key Players Benchmarking

4.4. Market Structure

4.4.1. Market Leaders

4.4.2. Market Followers

4.4.3. Emerging Players

4.5. Consolidation of the Market

5. ISO Container Market: Dynamics

5.1. Market Driver

5.1.1. Increasing Consumer Awareness

5.1.2. Innovation in Product Offerings

5.2. Market Trends by Region

5.2.1. North America

5.2.2. Europe

5.2.3. Asia Pacific

5.2.4. South America

5.2.5. Middle East and Africa

5.3. Market Drivers by Region

5.3.1. North America

5.3.2. Europe

5.3.3. Asia Pacific

5.3.4. South America

5.3.5. Middle East and Africa

5.4. Market Restraints

5.5. Market Opportunities

5.6. Market Challenges

5.7. PORTER’s Five Forces Analysis

5.8. PESTLE Analysis

5.9. Strategies for New Entrants to Penetrate the Market

5.10. Regulatory Landscape by Region

5.10.1. North America

5.10.2. Europe

5.10.3. Asia Pacific

5.10.4. South America

5.10.5. Middle East and Africa

6. ISO Container Market Size and Forecast by Segments (by Value Units)

6.1. ISO Container Market Size and Forecast, by Container Type (2025-2032)

6.1.1. Lined Tanks

6.1.2. Reefer Tanks

6.1.3. Cryogenic & Gas Tanks

6.1.4. Swap Body Tanks

6.1.5. Multi-Compartment Tanks

6.2. ISO Container Market Size and Forecast, by Transport Modes (2025-2032)

6.2.1. Rail

6.2.2. Marine

6.2.3. Road

6.3. ISO Container Market Size and Forecast, by Capacity (2025-2032)

6.3.1. Below 20,000 litres

6.3.2. 20,000 - 35,000 litres

6.3.3. Above 35,000 litres

6.3.4. Others

6.4. ISO Container Market Size and Forecast, by End-Use (2025-2032)

6.4.1. Industrial gas

6.4.2. Petrochemicals

6.4.3. Food & Beverage

6.4.4. Chemicals

6.4.5. Pharmaceuticals

6.4.6. Others

6.5. ISO Container Market Size and Forecast, by Region (2025-2032)

6.5.1. North America

6.5.2. Europe

6.5.3. Asia Pacific

6.5.4. South America

6.5.5. Middle East and Africa

7. North America ISO Container Market Size and Forecast (by Value Units)

7.1. North America ISO Container Market Size and Forecast, by Container Type (2025-2032)

7.1.1. Lined Tanks

7.1.2. Reefer Tanks

7.1.3. Cryogenic Tanks

7.1.4. Gas Tanks

7.1.5. Swap Body Tanks

7.1.6. Multi-Compartment Tanks

7.1.7. Others

7.2. North America ISO Container Market Size and Forecast, by Transport Modes (2025-2032)

7.2.1. Rail

7.2.2. Marine

7.2.3. Road

7.3. North America ISO Container Market Size and Forecast, by Capacity (2025-2032)

7.3.1. Below 20,000 litres

7.3.2. 20,000 - 35,000 litres

7.3.3. Above 35,000 litres

7.3.4. Others

7.4. North America ISO Container Market Size and Forecast, by End-Use (2025-2032)

7.4.1. Industrial gas

7.4.2. Petrochemicals

7.4.3. Food & Beverage

7.4.4. Chemicals

7.4.5. Pharmaceuticals

7.4.6. Others

7.5. North America ISO Container Market Size and Forecast, by Country (2025-2032)

7.5.1. United States

7.5.2. Canada

7.5.3. Mexico

8. Europe ISO Container Market Size and Forecast (by Value Units)

8.1. Europe ISO Container Market Size and Forecast, by Container Type (2025-2032)

8.1.1. Lined Tanks

8.1.2. Reefer Tanks

8.1.3. Cryogenic Tanks

8.1.4. Gas Tanks

8.1.5. Swap Body Tanks

8.1.6. Multi-Compartment Tanks

8.1.7. Others

8.2. Europe ISO Container Market Size and Forecast, by Transport Modes (2025-2032)

8.2.1. Rail

8.2.2. Marine

8.2.3. Road

8.3. Europe ISO Container Market Size and Forecast, by Capacity (2025-2032)

8.3.1. Below 20,000 litres

8.3.2. 20,000 - 35,000 litres

8.3.3. Above 35,000 litres

8.3.4. Others

8.4. Europe ISO Container Market Size and Forecast, by End-Use (2025-2032)

8.4.1. Industrial gas

8.4.2. Petrochemicals

8.4.3. Food & Beverage

8.4.4. Chemicals

8.4.5. Pharmaceuticals

8.4.6. Others

8.5. Europe ISO Container Market Size and Forecast, by Country (2025-2032)

8.5.1. UK

8.5.2. France

8.5.3. Germany

8.5.4. Italy

8.5.5. Spain

8.5.6. Switzerland

8.5.7. Netherland

8.5.8. Rest of Europe

9. Asia Pacific ISO Container Market Size and Forecast (by Value Units)

9.1. Asia Pacific ISO Container Market Size and Forecast, by Container Type (2025-2032)

9.1.1. Lined Tanks

9.1.2. Reefer Tanks

9.1.3. Cryogenic Tanks

9.1.4. Gas Tanks

9.1.5. Swap Body Tanks

9.1.6. Multi-Compartment Tanks

9.1.7. Others

9.2. Asia Pacific ISO Container Market Size and Forecast, by Transport Modes (2025-2032)

9.2.1. Rail

9.2.2. Marine

9.2.3. Road

9.3. Asia Pacific ISO Container Market Size and Forecast, by Capacity (2025-2032)

9.3.1. Below 20,000 litres

9.3.2. 20,000 - 35,000 litres

9.3.3. Above 35,000 litres

9.3.4. Others

9.4. Asia Pacific ISO Container Market Size and Forecast, by End-Use (2025-2032)

9.4.1. Industrial gas

9.4.1. Petrochemicals

9.4.1. Food & Beverage

9.4.1. Chemicals

9.4.1. Pharmaceuticals

9.4.1. Others

9.5. Asia Pacific ISO Container Market Size and Forecast, by Country (2025-2032)

9.5.1. China

9.5.2. South Korea

9.5.3. Japan

9.5.4. India

9.5.5. Australia

9.5.6. Indonesia

9.5.7. Malaysia

9.5.8. Vietnam

9.5.9. Taiwan

9.5.10. Rest of Asia Pacific

10. South America ISO Container Market Size and Forecast (by Value USD Billion)

10.1. South America ISO Container Market Size and Forecast, by Container Type (2025-2032)

10.1.1. Lined Tanks

10.1.2. Reefer Tanks

10.1.3. Cryogenic Tanks

10.1.4. Gas Tanks

10.1.5. Swap Body Tanks

10.1.6. Multi-Compartment Tanks

10.1.7. Others

10.2. South America ISO Container Market Size and Forecast, by Transport Modes (2025-2032)

10.2.1. Rail

10.2.2. Marine

10.2.3. Road

10.3. South America ISO Container Market Size and Forecast, by Capacity (2025-2032)

10.3.1. Below 20,000 litres

10.3.2. 20,000 - 35,000 litres

10.3.3. Above 35,000 litres

10.3.4. Others

10.4. South America ISO Container Market Size and Forecast, by End-Use (2025-2032)

10.4.12. Industrial gas

10.4.13. Petrochemicals

10.4.14. Food & Beverage

10.4.15. Chemicals

10.4.16. Pharmaceuticals

10.4.17. Others

10.5. South America ISO Container Market Size and Forecast, by Country (2025-2032)

10.5.1. Brazil

10.5.2. Argentina

10.5.3. Chile

10.5.4. Colombia

11. Middle East and Africa ISO Container Market Size and Forecast (by Value USD Billion)

11.1. Middle East and Africa ISO Container Market Size and Forecast, by Container Type (2025-2032)

11.1.1. Lined Tanks

11.1.2. Reefer Tanks

11.1.3. Cryogenic Tanks

11.1.4. Gas Tanks

11.1.5. Swap Body Tanks

11.1.6. Multi-Compartment Tanks

11.1.7. Others

11.2. Middle East and Africa ISO Container Market Size and Forecast, by Transport Modes (2025-2032)

11.2.1. Rail

11.2.2. Marine

11.2.3. Road

11.3. Middle East and Africa ISO Container Market Size and Forecast, by Capacity (2025-2032)

11.3.1. Below 20,000 litres

11.3.2. 20,000 - 35,000 litres

11.3.3. Above 35,000 litres

11.3.4. Others

11.4. Middle East and Africa ISO Container Market Size and Forecast, by End-Use (2025-2032)

11.4.18. Industrial gas

11.4.19. Petrochemicals

11.4.20. Food & Beverage

11.4.21. Chemicals

11.4.22. Pharmaceuticals

11.4.23. Others

11.5. Middle East and Africa ISO Container Market Size and Forecast, by Country (2025-2032)

11.5.1. South Africa

11.5.2. Saudi Arebia

11.5.3. Egypt

11.5.4. UAE

11.5.5. Rest of ME&A

12. Company Profile: Key players

12.1. CXIC Group

12.1.1. Company Overview

12.1.2. Financial Overview

12.1.3. Business Portfolio

12.1.4. SWOT Analysis

12.1.5. Business Strategy

12.1.6. Recent Development

12.2. Singamas Container

12.3. Bewellcn Shanghai

12.4. Bulkhaul Limited

12.5. Chart Industries

12.6. Cryeng Group Pty Ltd.

12.7. Blue Sky Intermodal

12.8. Carbon Energy Group

12.9. Danteco Industries BV

12.10. Bertschi AG

12.11. CARU Containers B.V.

12.12. Circle Ship Marine

12.13. COSCO SHIPPING

12.14. Royal Den Hartogh Logistics

12.15. INOXCVA

12.16. Tls Offshore Containers International

12.17. China International Marine Containers Co.

12.18. CIMC Furuise

12.19. M1 Engineering Holdings Limited

12.20. Rootselaar Group

13. Key Findings

14. Industry Recommendations