Automatic Test Equipment Market Global Industry Analysis and Forecast (2026-2032) Trends, Statistics, Dynamics, Segmentation by Types, Components, Applications, and Region

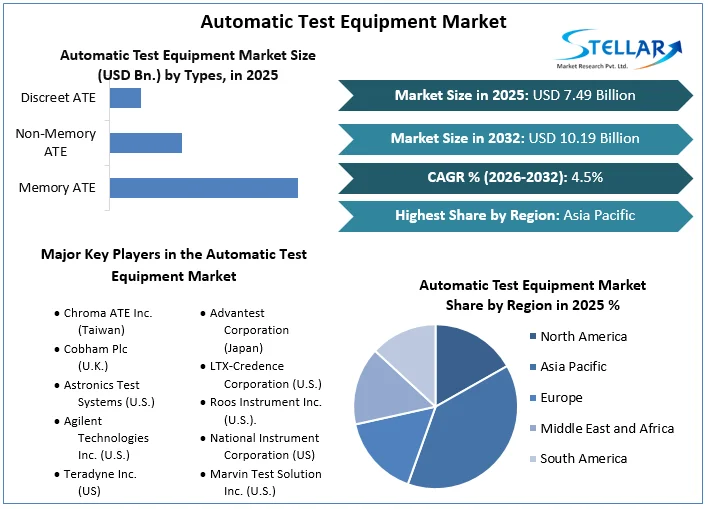

Automatic Test Equipment Market size was valued at USD 7.49 Bn. in 2025 and the total Automatic Test Equipment is expected to grow by 4.5% from 2026 to 2032, reaching nearly USD 10.19 Bn.

Automatic Test Equipment Market Overview:

Automatic Test Equipment (ATE) is one of the most widely used circuit and device test in modern electronics It is used in the fault detection of printed circuit board in electronics and electrical equipment and are relatively swift and faster compared to manual test methodology it performs test on a device, known as the Device under Test (DUT) or Unit under Test (UUT), using automation to quickly perform- measurements and evaluate the test results and thus ensuring quality of device. The automatic test equipment market has a significant role in reducing the cost of manufacturing and assisting in eliminating defective devices from the market. Automated test equipment market diagnoses and tests faults in chips, integrated circuits, printed circuit boards, semiconductor waters, and other electronic parts. Semiconductor ATE finds extensive application in system-on-chip products within consumer electronics, including tablets. smartphones and laptops. ATE has applications in the avionics and various electronic components of automobiles. It is widely used in the testing of wireless communication devices such as radar, CDMA, and GSM modules.

The rapid growth of the automotive and semiconductor industry is expected to drive market growth. The surge in demand for high-quality consumer electronics products will contribute positively towards market growth. The semiconductor companies deployed test equipment in order to amplify the performance capability, and speed of operation and to reduce the cost of production of the semiconductor devices. These attributes are expected to drive the growth of the automatic test equipment market. The rise in demand for Small on-chip devices will fuel the market growth. Also, the increase in electronic components in automobiles and the rapid increase in demand for electric vehicles in the market is anticipated to boost the market. Furthermore, the enhancement of technology integrated with the design complexity of the electronic components that needs essential testing is a factor that will positively impact the growth of the automatic test equipment market.

To get more Insights: Request Free Sample Report

Automatic Test Equipment Market Dynamics:

Automated Test Equipment (ATE) reduces both manufacturing time and cost.

Manual testing involves executing each test step carefully. Automated test equipment uses automation tools to execute the test case suite and generate detailed test reports. This equipment is useful for testing semiconductor devices, such as PCBs, quickly and efficiently. The goal is to reduce production time and costs. The semiconductor industry is designing more complex devices for better applications. To reduce maintenance costs, it's essential to increase the throughput of test systems. Automated test equipment (ATE) is concerned with increasing the throughput and reliability of the manufacturing test system. One method of ATE is a hardware handshaking form of scanning which helps increase throughput by allowing direct communication between the switch and the instrument without any software intervention. This minimizes the time wasted between measurements and guarantees maximum throughput. ATE increases system longevity for long-term success and is in high demand due to its high efficiency, maximum reliability, and high throughput. More manufacturers are adopting ATE testing to reduce manufacturing time and cost.

Automatic Test Equipment Market Restraints:

High Costs Associated with Testers and Testing Components of the Market

Automated test equipment systems are not adopted by many manufacturers due to the high cost associated with them. The testers and testing components, such as handlers and probers, are too expensive for many start-ups in the semiconductor industry. The cost of the automated test equipment handler used for memory testing is more expensive than the cost of the memory tester. Even in the case of automated test equipment for MEMS and sensor testing, the handlers used are very costly. Hence, it is not possible for every semiconductor device manufacturer to adopt automated test equipment testing. Hence, several manufacturers prefer other testing methods, such as manual testing. This has been hampering the consumption of automated test equipment systems, thereby restraining the growth of the overall automated test equipment market.

Automatic Test Equipment Market Opportunities:

Advancements in the Automotive Sector

Semiconductor devices are widely used in the automotive industry, especially in advanced driving assistant systems (ADAS) that provide features like adaptive cruise control, automatic brakes, and blind-spot monitoring. The future of automotive applications such as advanced car structures, hybrid electric vehicles, and rail tractions is promising. According to a US International Trade Commission report published in May 2019, the semiconductor components' value in hybrid electric vehicles has increased from USD 1,000 to USD 3,500. Testing of electronic devices used in the automotive semiconductor and electronics industry is essential to provide a higher level of system performance. Due to the growth of the HEV industry and the constant increase in demand for complex systems, such as braking systems, efficient and reliable automated testing solutions are crucial. The automated test equipment industry, therefore, will have a huge demand in the automotive sector.

Automatic Test Equipment Market Segment Analysis:

Based on Type, The Memory ATE segment dominated the Automatic Test Equipment Market in the year 2025 & is expected to continue its dominance during the forecast period. Based on Components, the Automated Test Equipment market data includes Memory ATE, Non-Memory ATE, and Discreet ATE. The non-memory ATE segment leads the automated test equipment market. Recent innovations in loT devices, autonomous vehicles, and major advancements in the defense and aerospace sectors have dramatically changed the market dynamics. Companies are working to increase customer satisfaction. These factors are significant growth drivers for the market.

Based on the Component, The Industrial PC segment dominated the Automatic Test Equipment Market in the year 2025 & is expected to continue its dominance during the forecast period. Based on Components, the Automated Test Equipment market segmentation includes Industrial PC, Mass Interconnect, Handlers, Probers, and Semiconductors. Handlers are expected to hold the highest share of the market. Automatic test equipment systems for testing such integrated systems and packaged devices interface with automated placement tools called handlers. The handler physically places the DUT on the interface test adapter (ITA) so that the device can measure it. A custom test device and the processor have replaced the generic tester and can directly meet the specified requirements. This helps to achieve goals quickly and reduces the cost of testing. At the back end of the integrated chip (IC) process, handlers help classify the packages available in 15. Therefore, automated test equipment can successfully test ICs in a real environment rather than through simulation by an IC tester. This helps to test complex ICs with high fault coverage at low cost and further improves test quality.

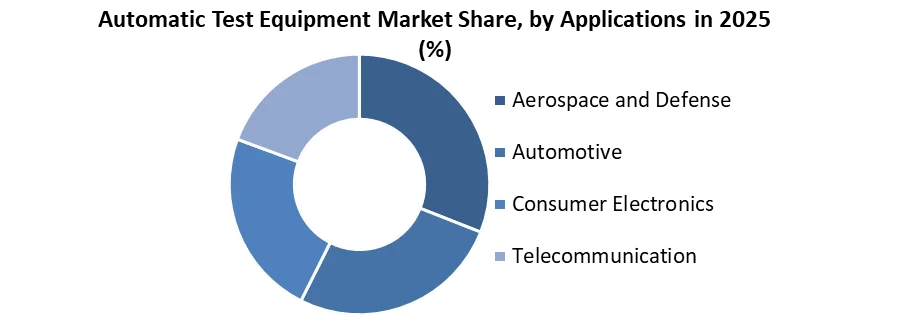

Based on the Application, The Aerospace & Defense segment dominated the Automatic Test Equipment Market in the year 2025 & is expected to continue its dominance during the forecast period. Based on Application, the Automated Test Equipment market segmentation

includes Consumer Electronics, Automotive, Aerospace & Defense, and Telecommunication. The adoption of complex equipment in the aerospace and defense industry has increased over the past three decades owing to increasing government spending in various regions. This has led to rapid technological development, with innovations leading to increased efficiency of existing tools and further coverage of new operating ranges useful for a wide range of functions. Along with rising revenues, the aerospace industry is expected to invest heavily in automated test equipment. According to the US Census Bureau. US aerospace product and component manufacturing revenues are increasing yearly. Revenue fell slightly during the pandemic and has gradually increased since.

Automatic Test Equipment Market Regional Insights:

The Asia Pacific region dominated the Automatic Test Equipment Market in the year 2025 & is expected to continue its dominance during the forecast period. The MRFR analysis reports suggest that the Asia-Pacific region secured the top position across the global market for automated test equipment in 2025, contributing to nearly 75% of the net market share. The significant presence of semiconductor companies across the region is considered the main parameter supporting regional market growth. Taiwan and China are likely to have the most considerable contribution to the revenue in the region overall. Several upcoming technologies, like design standards, fine-pitch probe cards, adaptive testing, quicker mixed-signal testers, improved Design-for-Test (DFT), and others, are anticipated to play a crucial part in the growth of the regional market over the coming years.

The increase in government efforts by countries such as Thailand, Singapore, Malaysia, Taiwan, Indonesia, and China to generate refined production processes is also likely to take part in the development, as in the launch of the latest technologies. The North American regional market for automated test equipment is anticipated to record substantial growth over the assessment timeframe. The rising utilization of automated test equipment in the aerospace and military industries is considered the main parameter that is boosting the growth of the regional market.

Automatic Test Equipment Market Scope:

|

Automatic Test Equipment Market |

|

|

Market Size in 2025 |

USD 7.49 Bn. |

|

Market Size in 2032 |

USD 10.19 Bn. |

|

CAGR (2026-2032) |

4.5% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segment Scope |

Based on the Types Memory ATE Non-Memory ATE Discreet ATE |

|

Based on the Components Industrial PC Mass Interconnect Handlers Probers Semiconductors |

|

|

Based on the Applications Aerospace and Defense Automotive Consumer Electronics Telecommunication |

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe North America – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Automatic Test Equipment Market Key Players

- Chroma ATE Inc. (Taiwan)

- Cobham Plc (U.K.)

- Astronics Test Systems (U.S.)

- Agilent Technologies Inc. (U.S.)

- Teradyne Inc. (US)

- Advantest Corporation (Japan)

- LTX-Credence Corporation (U.S.)

- Roos Instrument Inc. (U.S.).

- National Instrument Corporation (US)

- Marvin Test Solution Inc. (U.S.)

Frequently Asked Questions

The Asia Pacific region is expected to hold the highest share of the Automatic Test Equipment Market.

The market size of the Automatic Test Equipment Market by 2032 is expected to reach US$ 10.19 Bn.

The forecast period for the Automatic Test Equipment Market is 2026-2032.

The market size of the Automatic Test Equipment Market in 2025 was valued at US$ 7.49 Bn.

1. Research Methodology

1.1 Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Research Assumption

2. Automatic Test Equipment Market Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026– 2032) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Global Automatic Test Equipment Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Product Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. Product Launches and Innovations

4. Automatic Test Equipment Market: Dynamics

4.1. Automatic Test Equipment Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Automatic Test Equipment Market Drivers

4.3. Automatic Test Equipment Market Restraints

4.4. Automatic Test Equipment Market Opportunities

4.5. Automatic Test Equipment Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factor

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Analysis

4.8.1. Commercialization of IoT Technology

4.8.2. Inclination Toward Adoption of Ate Equipment on Rental Basis

4.8.3. Trend of Modular Test Instruments

4.8.4. Emergence of 5g Network

4.8.5. Technological Roadmap

4.9. Value Chain Analysis

4.10. Regulatory Landscape by Region

4.10.1. North America

4.10.2. Europe

4.10.3. Asia Pacific

4.10.4. Middle East and Africa

4.10.5. South America

5. Automatic Test Equipment Market: Global Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

5.1. Automatic Test Equipment Market Size and Forecast, by Types (2025-2032)

5.1.1. Memory ATE

5.1.2. Non-Memory ATE

5.1.3. Discreet ATE

5.2. Automatic Test Equipment Market Size and Forecast, by Components (2025-2032)

5.2.1. Industrial PC

5.2.2. Mass Interconnect

5.2.3. Handlers

5.2.4. Probers

5.2.5. Semiconductors

5.3. Automatic Test Equipment Market Size and Forecast, by Applications (2025-2032)

5.3.1. Aerospace and Defense

5.3.2. Automotive

5.3.3. Consumer Electronics

5.3.4. Telecommunication

5.4. Automatic Test Equipment Market Size and Forecast, by Region (2025-2032)

5.4.1. North America

5.4.2. Europe

5.4.3. Asia Pacific

5.4.4. Middle East and Africa

5.4.5. South America

6. North America Automatic Test Equipment Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

6.1. North America Automatic Test Equipment Market Size and Forecast, by Types (2025-2032)

6.1.1. Memory ATE

6.1.2. Non-Memory ATE

6.1.3. Discreet ATE

6.2. North America Automatic Test Equipment Market Size and Forecast, by Components (2025-2032)

6.2.1. Industrial PC

6.2.2. Mass Interconnect

6.2.3. Handlers

6.2.4. Probers

6.2.5. Semiconductors

6.3. North America Automatic Test Equipment Market Size and Forecast, by Applications (2025-2032)

6.3.1. Aerospace and Defense

6.3.2. Automotive

6.3.3. Consumer Electronics

6.3.4. Telecommunication

6.4. North America Automatic Test Equipment Market Size and Forecast, by Country (2025-2032)

6.4.1. United States

6.4.2. Canada

6.4.3. Mexico

7. Europe Automatic Test Equipment Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

7.1. Europe Automatic Test Equipment Market Size and Forecast, by Types (2025-2032)

7.2. Europe Automatic Test Equipment Market Size and Forecast, by Components (2025-2032)

7.3. Europe Automatic Test Equipment Market Size and Forecast, by Applications (2025-2032)

7.4. Europe Automatic Test Equipment Market Size and Forecast, by Country (2025-2032)

7.4.1. United Kingdom

7.4.2. France

7.4.3. Germany

7.4.4. Italy

7.4.5. Spain

7.4.6. Sweden

7.4.7. Austria

7.4.8. Rest of Europe

8. Asia Pacific Automatic Test Equipment Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

8.1. Asia Pacific Automatic Test Equipment Market Size and Forecast, by Types (2025-2032)

8.2. Asia Pacific Automatic Test Equipment Market Size and Forecast, by Components (2025-2032)

8.3. Asia Pacific Automatic Test Equipment Market Size and Forecast, by Applications (2025-2032)

8.4. Asia Pacific Automatic Test Equipment Market Size and Forecast, by Country (2025-2032)

8.4.1. China

8.4.2. S Korea

8.4.3. Japan

8.4.4. India

8.4.5. Australia

8.4.6. Indonesia

8.4.7. Malaysia

8.4.8. Vietnam

8.4.9. Taiwan

8.4.10. Rest of Asia Pacific

9. Middle East and Africa Automatic Test Equipment Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

9.1. Middle East and Africa Automatic Test Equipment Market Size and Forecast, by Types (2025-2032)

9.2. Middle East and Africa Automatic Test Equipment Market Size and Forecast, by Components (2025-2032)

9.3. Middle East and Africa Automatic Test Equipment Market Size and Forecast, by Applications (2025-2032)

9.4. Middle East and Africa Automatic Test Equipment Market Size and Forecast, by Country (2025-2032)

9.4.1. South Africa

9.4.2. GCC

9.4.3. Nigeria

9.4.4. Rest of ME&A

10. South America Automatic Test Equipment Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

10.1. South America Automatic Test Equipment Market Size and Forecast, by Types (2025-2032)

10.2. South America Automatic Test Equipment Market Size and Forecast, by Components (2025-2032)

10.3. South America Automatic Test Equipment Market Size and Forecast, by Applications (2025-2032)

10.4. South America Automatic Test Equipment Market Size and Forecast, by Country (2025-2032)

10.4.1. Brazil

10.4.2. Argentina

10.4.3. Rest Of South America

11. Company Profile: Key Players

11.1. Chroma ATE Inc. (Taiwan)

11.1.1. Company Overview

11.1.2. Product Portfolio

11.1.2.1. Product Name

11.1.2.2. Product Details (Price, Features, etc)

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Cobham Plc (U.K.)

11.3. Astronics Test Systems (U.S.)

11.4. Agilent Technologies Inc. (U.S.)

11.5. Teradyne Inc. (US)

11.6. Advantest Corporation (Japan)

11.7. LTX-Credence Corporation (U.S.)

11.8. Roos Instrument Inc. (U.S.).

11.9. National Instrument Corporation (US)

11.10. Marvin Test Solution Inc. (U.S.)

12. Key Findings

13. Analyst Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook