Hydraulic Fracturing Market-Global Industry Analysis and Forecast (2026-2032)

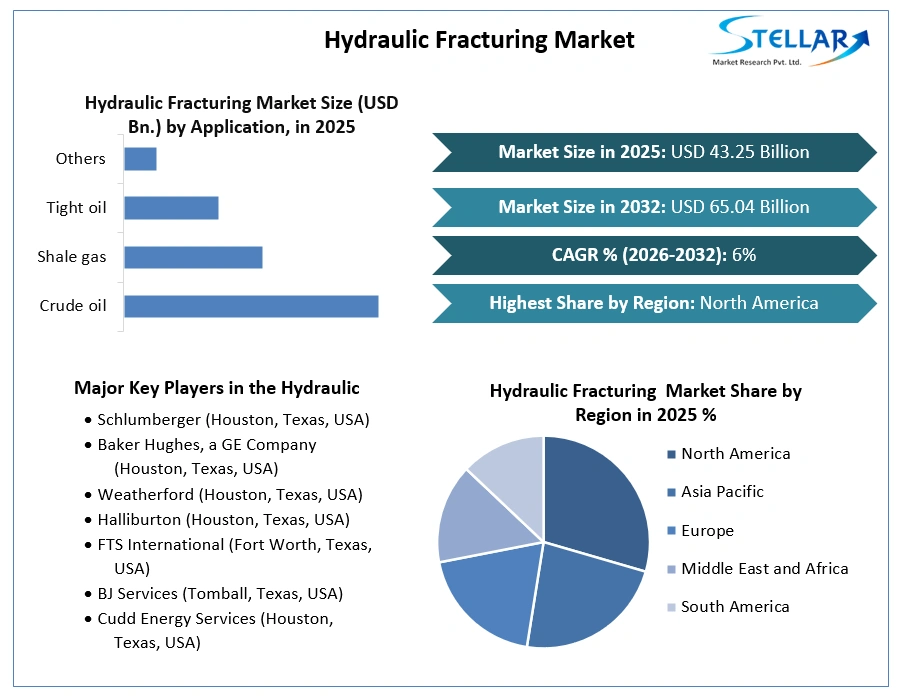

Hydraulic Fracturing Market size was valued at USD 43.25 Bn. in 2025 and is expected to reach USD 65.04 Bn. by 2032, at a CAGR of 6%.

Hydraulic Fracturing Market Overview:

Hydraulic fracturing, commonly known as "fracking", is a process that injects high-pressure liquid into an oil- or gas-bearing rock formation to create fractures. This pressure typically yields improved flows, making it useful for oil and gas firms seeking more economical production in areas that would otherwise produce low-flow wells. The liquid includes water, chemicals, and sand. In oil and gas production, it is generally used to enhance the production of oil and gas reservoirs to keep the well sticky, and also fracturing fluids are used in this technique to create a fracture of good width. It is used to generate oil and gas from wells. Many oil and natural gas companies provide fracking techniques. It is also used in many applications such as crude, tight, shale, etc.

Growing global energy demand, driven by industrialization and population growth, has increased the need for new oil and gas sources, thus driving the hydraulic fracturing market. This is being accompanied by High oil and natural gas prices making hydraulic fracturing more economically viable. Furthermore, increase in offshore and onshore oil and gas exploration activities. It is widely used to refurbish well base expansion, oil fields, and the exploration of new offshore projects for crude oil and natural gas extraction.

The hydraulic fracturing market is facing massive lashes due to its environmental impact. Environmental concerns linked to hydraulic fracturing include air pollution from methane emissions, groundwater contamination, and the potential risk of induced earthquakes. The disposal of wastewater from the drilling process plays a primary role in many disagreements about how to weigh the technology’s risks against its benefits.

To get more Insights: Request Free Sample Report

Hydraulic Fracturing Market Trends:

- The drilling activities, redevelopment of fields and new offshore projects are increasing in the US which will drive the market of hydraulic fracturing.

- The new well drilling and well base expansion is carried out in North America. Also. North America is the producer of natural gas and crude oil. This will drive the growth of the Hydraulic Fracturing market in North America.

- The energy demand for energy is increasing in developing countries like India, China and hence to fulfill this demand and enhance growth hydraulic fracturing will increase and will be beneficial for these countries.

- The market players adopt strategies such as mergers and acquisitions, new product launches, and contract agreements to grow hydraulic fracturing service and equipment supply.

- The shale gas exploration and development activities are increasing, it increases the hydraulic fracturing market.

Hydraulic Fracturing Market Dynamics

Drivers: Increase in global energy demand and fluctuating crude oil prices.

Global crude oil demand is projected to hit 104.46 million barrels per day (bpd) in 2025, driving up oil and natural gas prices. This rising energy demand makes hydraulic fracturing projects more economically appealing, prompting companies to invest in new wells and advanced technologies to meet this demand. The increasing need for hydraulic fracturing technology is driven by the growing energy requirements.

According to a monthly report from the Organization of the Petroleum Exporting Countries (OPEC), global oil demand is expected to increase by 2.25 million bpd in 2025. By 2032. global oil consumption is anticipated to reach 3.2 million bpd. Additionally, the Asia-Pacific region is forecasted to become the largest consumer of oil and gas over the next decade. This region has seen a significant rise in oil and gas demand due to factors such as population growth, higher per capita income, urbanization, and the expansion of petrochemical refineries. From 2011 to 2025, Asia-Pacific accounted for about two-thirds of the world's oil and gas demand on average.

The widening supply-demand gap for primary energy sources is a key driver of the hydraulic fracturing market growth. As oil and gas demand continues to increase while production capacities for existing reserves remain constrained, the focus is shifting towards unconventional gas. Unconventional gas constitutes 44% of total natural gas production, with shale gas making up 28% of this segment. In contrast, Eastern Europe, Eurasia (including Russia), and the Middle East hold 61% of conventional gas reserves but only 16.6% of unconventional gas. Consequently, regions outside these areas have a higher proportion of unconventional gas. As onshore and shallow water fields become depleted, oil companies are turning to deepwater and unconventional reserves, where hydraulic fracturing is increasingly seen as a viable method for exploration and production.

This huge demand drives the increase in prices of crude prices. Higher prices, there is an incentive for increased production from hydraulic fracturing operations. Companies often ramp up their drilling activities and complete more wells to take advantage of favorable market conditions. The U.S. shale oil boom is a prime example, where high oil prices led to a rapid increase in the hydraulic fracturing market, significantly boosting U.S. oil production.

Increase in exploration activities in deep water/offshore:

As onshore conventional oil and gas resources become depleted, there is a growing focus on offshore reserves. Hydraulic fracturing technology becomes increasingly important to unlock the potential of these offshore unconventional resources. The exploration of deepwater and ultra-deepwater reserves has led to the discovery of new oil and gas resources that are often accessed using hydraulic fracturing. These reserves require advanced fracking techniques due to their challenging environments.

The potential for significant reserves in offshore fields leads to substantial investments in the hydraulic fracturing market. High oil prices make offshore exploration and hydraulic fracturing more economically viable. When oil prices are elevated, the higher costs associated with offshore fracking can be offset by the increased revenue from oil production. Companies are willing to invest in advanced fracking solutions to tap into these high-value projects. This has created the need for the development of extensive infrastructure, including platforms, pipelines, and support vessels, which supports the growth of the hydraulic fracturing market.

The Gulf of Mexico is a major region for offshore exploration and hydraulic fracturing, with numerous deepwater and ultra-deepwater projects. Companies in this region invest heavily in advanced fracking technologies to access valuable reserves. The Asia-Pacific region, including countries like China and India, is increasingly focusing on offshore exploration to meet growing energy demands. Hydraulic fracturing plays a role in unlocking unconventional resources in this region.

Challenges: Environmental concerns and Hydraulic fracturing

One of the main pollutants released in the hydraulic fracturing process is methane, a greenhouse gas that traps 25 times more heat than carbon dioxide. Research indicates the U.S. oil and gas industry emits 16.9 million metric tons of methane every year, according to the International Energy Agency. Some of this methane is inadvertently leaked through faulty equipment or deliberately vented into the atmosphere between extractions. The Environmental Protection Agency (EPA) estimates that the U.S. accounts for more methane emissions than 164 countries combined. In addition to methane, hydraulic fracturing also releases toxic compounds such as nitrogen oxides, benzene, hydrogen sulfide, and other hydrocarbons, forming smog and ozone that can cause health problems to those living nearby. Local air pollution can aggravate asthma and other respiratory conditions.

hydraulic fracturing uses large amounts of water and releases toxic chemicals into the surrounding water table. Each well consumes a median of 1.5 million gallons, according to the EPA, adding up to billions of gallons nationwide every year. Not only does this reduce the amount of water available for drinking and irrigation, but it also threatens to pollute local sources with contaminated wastewater, creating obstacles to hydraulic fracturing market growth.

The byproduct of fracking's water consumption is billions of gallons of wastewater that may be contaminated by petrochemicals. The majority is injected into underground wells, and what isn't injected is transported for treatment. The EPA highlights potential leakage from wastewater storage pits, or accidental releases during transport, as risks to drinking water supplies.

Hydraulic Fracturing Market Segment Analysis:

By Well Type: Horizontal wells held the largest market share in 2024. Horizontal wells are the primary driver of growth in the hydraulic fracturing market, particularly due to the surge in unconventional oil and gas resources. Advances in horizontal drilling and fracturing technologies have made this type of well increasingly efficient and cost-effective for extracting hydrocarbons from shale and other tight formations. It can access a larger portion of the reservoir compared to vertical wells, which significantly increases production rates and recovery.

They allow for the drilling of multiple horizontal branches from a single vertical wellbore, optimizing reservoir contact and production. Fewer surface locations are required for horizontal wells, reducing the environmental impact and land use compared to multiple vertical wells. Their dominance is expected to continue as technology advances and demand for unconventional resources grows.

Vertical wells have been used for decades and are still relevant in the hydraulic fracturing market, particularly in conventional oil and gas fields. Vertical wells involve simpler and less expensive drilling processes compared to horizontal wells, making them suitable for certain applications. The cost of drilling and completing vertical wells is generally lower due to the simpler technology and less complex operational requirements. Vertical wells are sometimes used in conjunction with horizontal wells or other enhanced oil recovery methods to maximize resource extraction.

Hydraulic Fracturing Market Regional Insights:

North America, particularly the United States and Canada, is the largest and most advanced hydraulic fracturing market. It is well-established with a significant share of global hydraulic fracturing activities. It is home to major shale plays such as the Permian Basin, Eagle Ford, and Marcellus Shale. Along with this, it has Significant production from unconventional resources that drives demand for hydraulic fracturing. It is a leader in the development and deployment of advanced fracturing technologies, including horizontal drilling and multi-stage fracturing.

Asia-Pacific is an emerging and rapidly expanding hydraulic fracturing market, driven by increasing energy demands and investments in unconventional resources. It is characterized by rapid economic growth and urbanization and increased investment in hydraulic fracturing to reduce dependence on imported energy. Notable reserves are found in China, India, and Australia, with ongoing exploration and development. Asia-Pacific has significant growth potential due to large untapped reserves and increasing investment.

Europe is a relatively small market compared to North America and Asia-Pacific but shows potential for growth as it explores its unconventional resources. Potential reserves are found in countries like the United Kingdom, Poland, and Romania. Regulatory challenges and public opposition are major factors affecting the growth of the hydraulic fracturing market in Europe.

Developments in Hydraulic Fracturing Market:

- In June 2023, NexTier Oilfield Solutions and Patterson-UTI Energy, Inc. announced that they have entered into a definitive merger agreement to combine in an all-stock merger of equals transaction. The combined company will be an industry-leading drilling and completions services provider with operations in the most active major U.S. basins.

- In January 2024, ProFrac Holding Corp. acquired REV Energy Holdings, LLC ("REV"), a privately owned pressure pumping service provider with operations in the Eagle Ford and Rockies. ProFrac paid $140 million for REV. The acquisition will expand ProFrac's presence in both South Texas and the Rockles.

- In January 2024, ProFrac acquired Producers Services Holdings LLC, a pressure pumping services company serving Appalachia and the Mid-Continent. ProFrac bought Producers for about $35 million in total transaction value, according to the terms of the arrangement.

- In December 2024, ProPetro Holding Corp. signed an agreement with a top Independent Permian operator to use ProPetro's first electric-powered hydraulic fracturing fleet ("e-fleet"). ProPetro will provide committed services for three years following the delivery of the e-fleet under the terms of the agreement

Hydraulic Fracturing Market Scope

|

Hydraulic Fracturing Market |

|

|

Market Size in 2025 |

USD 43.25Bn. |

|

Market Size in 2032 |

USD 65.04 Bn. |

|

CAGR (2026-2032) |

6% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Hydraulic Fracturing Market Segments |

By Well Type

|

|

By Technology

|

|

|

|

By Application

|

|

Regional Scope |

North America (United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Russia, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa (South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Hydraulic Fracturing Key players

North America

- Schlumberger (Houston, Texas, USA)

- Baker Hughes, a GE Company (Houston, Texas, USA)

- Weatherford (Houston, Texas, USA)

- Halliburton (Houston, Texas, USA)

- FTS International (Fort Worth, Texas, USA)

- BJ Services (Tomball, Texas, USA)

- Cudd Energy Services (Houston, Texas, USA)

- ProPetro Holding Corp. (Midland, Texas, USA)

- Calfrac Well Services (Calgary, Alberta, Canada)

- Liberty Oilfield Services (Denver, Colorado, USA)

- Trican Well Services Ltd. (Calgary, Alberta, Canada)

- Basic Energy Services (Midland, Texas, USA)

- Superior Energy Services (Houston, Texas, USA)

- RockPile Energy Services (Denver, Colorado, USA)

- US Well Services (Houston, Texas, USA)

Europe

- Weatherford International (London, United Kingdom)

- Tenaris (Luxembourg)

- KCA Deutag (Aberdeen, Scotland)

- Expro Group (Aberdeen, Scotland, United Kingdom)

Asia Pacific

- Jereh Group (Yantai, China)

Frequently Asked Questions

North America is expected to dominate the Hydraulic Fracturing Market during the forecast period.

The Hydraulic Fracturing Market size is expected to reach USD 65.04 billion by 2032.

Top players in the Global Hydraulic Fracturing Market are Schlumberger - Houston, Texas, USA, Baker Hughes, a GE Company - Houston, Texas, USA, Weatherford - Houston, Texas, USA, Halliburton - Houston, Texas, USA, FTS International - Fort Worth, Texas, USA, BJ Services - Tomball, Texas, USA, Cudd Energy Services - Houston, Texas, USA, ProPetro Holding Corp. - Midland, Texas, USA, Calfrac Well Services - Calgary, Alberta, Canada, Liberty Oilfield Services - Denver, Colorado, USA, Trican Well Services Ltd. - Calgary, Alberta, Canada, Basic Energy Services - Midland, Texas, USA, Superior Energy Services - Houston, Texas, USA, RockPile Energy Services - Denver, Colorado, USA, US Well Services - Houston, Texas, USA

An increase in global energy demand, fluctuating crude oil prices and an increase in exploration activities in deep water/offshore are the major factors driving the Global Hydraulic Fracturing Market growth.

1. Hydraulic Fracturing Market: Research Methodology

2. Hydraulic Fracturing Market Introduction

2.1. Study Assumption and Market Definition

2.2. Scope of the Study

2.3. Executive Summary

3. Global Hydraulic Fracturing Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Competitive Landscape

3.3. Key Players Benchmarking

3.3.1. Company Name

3.3.2. Product Segment

3.3.3. End-user Segment

3.3.4. Revenue (2025)

3.3.5. Company Headquarter

3.4. Market Structure

3.4.1. Market Leaders

3.4.2. Market Followers

3.4.3. Emerging Players

3.5. Mergers and Acquisitions Details

4. Hydraulic Fracturing Market: Dynamics

4.1. Hydraulic Fracturing Market Trends

4.2. Hydraulic Fracturing Market Dynamics

4.2.1.1. Drivers

4.2.1.2. Restraints

4.2.1.3. Opportunities

4.2.1.4. Challenges

4.3. PORTER’s Five Forces Analysis

4.4. PESTLE Analysis

4.5. Regulatory Landscape by Region

4.5.1. North America

4.5.2. Europe

4.5.3. Asia Pacific

4.5.4. Middle East and Africa

4.5.5. South America

5. Hydraulic Fracturing Market: Global Market Size and Forecast (Value in USD Billion) (2026-2032)

5.1. Hydraulic Fracturing Market Size and Forecast, By Well Type(2026-2032)

5.1.1. Horizontal

5.1.2. Vertical

5.2. Hydraulic Fracturing Market Size and Forecast, By Technology (2026-2032)

5.2.1. Plug-and-perforation

5.2.2. Sliding sleeve

5.2.3. Others

5.3. Hydraulic Fracturing Market Size and Forecast, Application (2026-2032)

5.3.1. Crude oil

5.3.2. Shale gas

5.3.3. Tight oil

5.3.4. Others

5.4. Hydraulic Fracturing Market Size and Forecast, by Region (2026-2032)

5.4.1. North America

5.4.2. Europe

5.4.3. Asia Pacific

5.4.4. Middle East and Africa

5.4.5. South America

6. North America Hydraulic Fracturing Market Size and Forecast by Segmentation (Value in USD Billion) (2026-2032)

6.1. North America Hydraulic Fracturing Market Size and Forecast, By Well Type (2026-2032)

6.1.1. Horizontal

6.1.2. Vertical

6.2. North America Hydraulic Fracturing Market Size and Forecast, By Technology (2026-2032)

6.2.1. Plug-and-perforation

6.2.2. Sliding sleeve

6.2.3. Others

6.3. North America Hydraulic Fracturing Market Size and Forecast, Application (2026-2032)

6.3.1. Crude oil

6.3.2. Shale gas

6.3.3. Tight oil

6.3.4. Others

6.4. Size and Forecast, by Country (2026-2032)

6.4.1. United States

6.4.2. Canada

6.4.3. Mexico

7. Europe Hydraulic Fracturing Market Size and Forecast by Segmentation (Value in USD Billion) (2026-2032)

7.1. Europe Hydraulic Fracturing Market Size and Forecast, By Well Type (2026-2032)

7.2. Europe Hydraulic Fracturing Market Size and Forecast, By Technology (2026-2032)

7.3. Europe Hydraulic Fracturing Market Size and Forecast, Application (2026-2032)

7.4. Europe Hydraulic Fracturing Market Size and Forecast, by Country (2026-2032)

7.4.1. United Kingdom

7.4.2. France

7.4.3. Germany

7.4.4. Italy

7.4.5. Spain

7.4.6. Sweden

7.4.7. Russia

7.4.8. Rest of Europe

8. Asia Pacific Hydraulic Fracturing Market Size and Forecast by Segmentation (Value in USD Billion) (2026-2032)

8.1. Asia Pacific Hydraulic Fracturing Market Size and Forecast, By Well Type (2026-2032)

8.2. Asia Pacific Hydraulic Fracturing Market Size and Forecast, By Technology (2026-2032)

8.3. Asia Pacific Hydraulic Fracturing Market Size and Forecast, Application (2026-2032)

8.4. Asia Pacific Hydraulic Fracturing Market Size and Forecast, by Country (2026-2032)

8.4.1. China

8.4.2. S Korea

8.4.3. Japan

8.4.4. India

8.4.5. Australia

8.4.6. ASEAN

8.4.7. Rest of Asia Pacific

9. Middle East and Africa Hydraulic Fracturing Market Size and Forecast by Segmentation (Value in USD Billion) (2026-2032)

9.1. Middle East and Africa Hydraulic Fracturing Market Size and Forecast, By Well Type (2026-2032)

9.2. Middle East and Africa Hydraulic Fracturing Market Size and Forecast, By Technology (2026-2032)

9.3. Middle East and Africa Hydraulic Fracturing Market Size and Forecast, Application (2026-2032)

9.4. Middle East and Africa Hydraulic Fracturing Market Size and Forecast, by Country (2026-2032)

9.4.1. South Africa

9.4.2. GCC

9.4.3. Nigeria

9.4.4. Rest of ME&A

10. South America Hydraulic Fracturing Market Size and Forecast by Segmentation (Value in USD Billion) (2026-2032)

10.1. South America Hydraulic Fracturing Market Size and Forecast, By Well Type (2026-2032)

10.2. South America Hydraulic Fracturing Market Size and Forecast, By Technology (2026-2032)

10.3. South America Hydraulic Fracturing Market Size and Forecast, Application (2026-2032)

10.4. South America Hydraulic Fracturing Market Size and Forecast, by Country (2026-2032)

10.4.1. Brazil

10.4.2. Argentina

10.4.3. Rest Of South America

11. Company Profile: Key Players

11.1. Schlumberger (Houston, Texas, USA

11.1.1. Company Overview

11.1.2. Business Portfolio

11.1.3. Financial Overview

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Baker Hughes, a GE Company (Houston, Texas, USA)

11.3. Weatherford (Houston, Texas, USA)

11.4. Halliburton (Houston, Texas, USA)

11.5. FTS International (Fort Worth, Texas, USA)

11.6. BJ Services (Tomball, Texas, USA)

11.7. Cudd Energy Services (Houston, Texas, USA)

11.8. ProPetro Holding Corp. (Midland, Texas, USA)

11.9. Calfrac Well Services (Calgary, Alberta, Canada)

11.10. Liberty Oilfield Services (Denver, Colorado, USA)

11.11. Trican Well Services Ltd. (Calgary, Alberta, Canada)

11.12. Basic Energy Services (Midland, Texas, USA)

11.13. Superior Energy Services (Houston, Texas, USA)

11.14. RockPile Energy Services (Denver, Colorado, USA)

11.15. US Well Services (Houston, Texas, USA)

11.16. Weatherford International (London, United Kingdom)

11.17. Tenaris (Luxembourg)

11.18. KCA Deutag (Aberdeen, Scotland)

11.19. Expro Group (Aberdeen, Scotland, United Kingdom)

11.20. Jereh Group (Yantai, China)

12. Key Findings

13. Industry Recommendations