Smart Airport Construction Market Global Industry Analysis and Forecast (2026-2032) Trends, Statistics, Dynamics, Segment Analysis

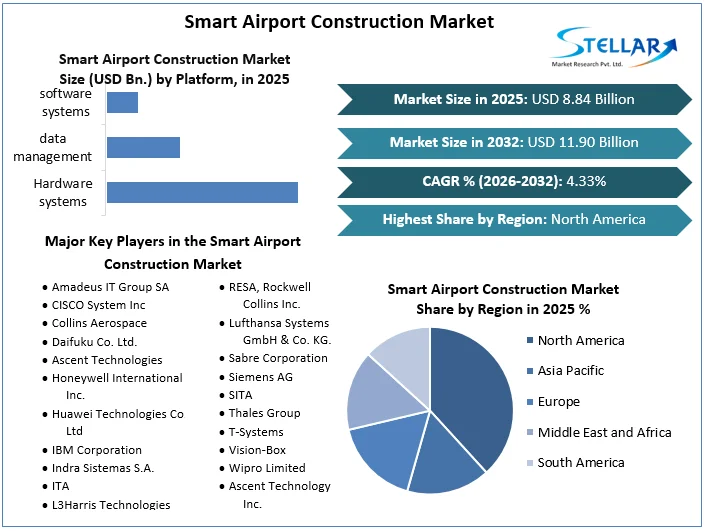

The Global Smart Airport Construction Market size reached USD 8.84 Billion in 2025 and expects the market to reach USD 11.90 Billion by 2032, exhibiting a growth rate (CAGR) of 4.33% during 2025-2032.

Smart Airport Construction Market Overview:

The concept of "Smart Airport Construction" refers to the development of airports that incorporate advanced technologies and smart infrastructure to enhance efficiency, safety, and passenger experience. These technologies often include automation, data analytics, Internet of Things devices, artificial intelligence (AI), and sustainable practices.

The analysis of trends and other factors that have a significant impact on the market is part of the research, which is broken up into numerous areas. The drivers, restraints, opportunities, and challenges that are used to characterize how these elements affect the market are among these factors, sometimes referred to as the market dynamics. Market drivers and restraints are intrinsic, whereas opportunities and challenges are extrinsic. The analysis of the global smart airport construction market offers a projection of the sector's revenue growth over the anticipated time frame.

To get more Insights: Request Free Sample Report

Smart Airport Construction Market Dynamics:

The driving factors include adoption of the Internet of Things, the advancement of technology

The rapid advancement of technology, especially in the areas of IoT (Internet of Things), artificial intelligence (AI), and data analytics, has made it possible for smart airports to be built. The improvements to security, airport operations, and passenger experience are all positive.

Because of the growth of air travel, especially in developing countries, there is a greater need for airport infrastructure. Smart airports are more effective overall and can accommodate a greater volume of passengers.

A wide range of conveniences, such as self-check-in kiosks, rapid security checks, and specialized services, enhance the visitor experience.

Enhanced security measures are required for the aviation industry. Smart airports can employ current security techniques like biometrics and AI-driven surveillance systems to improve passenger safety.

The development of remote and autonomous technologies, including remote air traffic control towers and autonomous ground vehicles, is influencing smart airport construction to improve efficiency and safety.

Smart Airport Construction Market Restraints:

High Initial Investment Costs

Building a smart airport requires a significant upfront investment in advanced technologies, infrastructure, and systems. This can be a major barrier for many airports, especially smaller ones or those in economically challenged regions.

Smart airports collect vast amounts of passenger data for various purposes, including security and passenger experience enhancements. Ensuring the privacy of this data and complying with data protection regulations is a significant challenge.

Smart airports are vulnerable to cyber-attacks, which could disrupt airport operations, compromise passenger safety, and result in data breaches. Ensuring robust cyber security measures is a critical challenge.

Smart Airport Construction Market Opportunities:

The Smart Airport Construction Market Opportunities include Expansion and Modernization, Air Traffic Control Towers, Airport City Development

Many airports are expanding their terminals to accommodate more passengers and provide better facilities. This creates opportunities for construction companies to bid on terminal construction and renovation projects.

Modernizing and building new air traffic control towers with advanced technologies is another avenue for construction companies. These towers need to integrate with digital communication and navigation systems.

Some airports are evolving into airport cities, featuring hotels, shopping centers, and office complexes. Construction companies can participate in these large-scale mixed-use developments.

Smart Airport Construction Market Challenges:

Smart Airport Construction Market Challenges include Environmental Impact, Regulatory Compliance

Airports produce a considerable amount of carbon emissions. As some technologies may demand additional energy consumption, it can be difficult to balance the adoption of smart technology with environmental sustainability goals.

Airports are required to abide by a number of national and international laws and norms. Compliantly implementing smart technologies can be difficult and time-consuming.

Smart airport construction often requires upgrades to existing infrastructure. Managing these construction projects without causing significant disruptions to airport operations can be challenging.

Smart Airport Construction Market Trends:

Airports were increasingly using robots and automation for tasks such as baggage handling, cleaning, and security patrols. These technologies help reduce labor costs and improve operational efficiency.

Some airports were exploring opportunities related to UAM, including the construction of vertiports or infrastructure to accommodate electric vertical takeoff and landing (eVTOL) aircraft.

Many airports were focusing on sustainability by adopting eco-friendly construction materials, energy-efficient technologies, and waste reduction measures. Some were also investing in renewable energy sources to reduce their carbon footprint.

Smart Airport Construction Market Regional Insights:

North America held the largest industry market share in 2025. The introduction of RFID/NFC-based baggage tracking systems and smart security gates, as well as the rising demand for real-time information, unmanned immigration systems, real-time CCTV surveillance, on-demand self-service, user-specific offerings, and system-generated alerts, are just a few of the factors driving the rapid advancements at smart airports across the U.S.

The fastest growth is anticipated in the Asia-Pacific area. Robotics, artificial intelligence, and biometric bag drop facilities are becoming more and more common in the region, especially in China and Japan. By offering passengers cutting-edge airport solutions like automatic luggage drop and self-service check-ins, Southeast Asia is expected to advance in terms of security, technology, infrastructure, and services.

Over the course of the estimated time frame, the Middle East and Africa (MEA) area is anticipated to grow significantly, mostly as a result of increased passenger volume and the extension of airport modernization initiatives at key airports. In order to give travelers real-time information, busy airports around the UAE have begun implementing voice-based artificial intelligence tools and digital support.

Smart Airport Construction Market Segment Analysis:

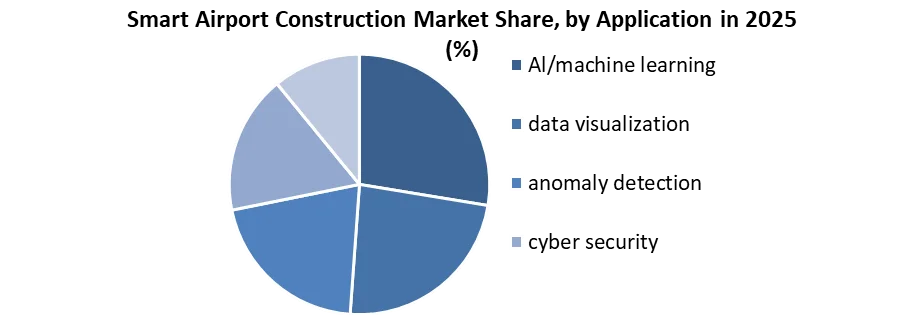

By Application The market is segmented into Al/machine learning, data visualization, anomaly detection, cyber security, asset/resource management, and others based on application. During the estimated time frame, it is expected that the Application.1 sector will rule the market. The segment is also anticipated to experience the highest CAGR growth during the research period. The installation of innovative systems and equipment powered by artificial intelligence on the terminal side of airports is in higher demand, which is responsible for this rise. An Al-based EZ Edge VRS deployment kit that permits vehicle entry and exit at Philadelphia International Airport will be installed.

By Platform, Hardware systems, data management, software systems, and other market segments are platform-based. It is anticipated that the hardware sector will dominate market growth during the estimated period. The growth of the sector is due to the creation of hardware tools for building digital airports.

The software systems market is anticipated to grow significantly over the estimated time span. The increasing demand for face detection and real-time information software are the main forces behind the market's rise at airports.

By Airport Model, The market has Airport 1.0, Airport 2.0, Airport 3.0, and Airport 4.0, according to the airport model. Throughout the anticipated time span, Airport 3.0 is anticipated to maintain a dominant market share. The widespread use of this paradigm in terminal-side, airside, and landside operations at North American airports is responsible for the region's growth.

Over the course of the period of projection, the smart airport industry is expected to experience the fastest CAGR growth in Airport 4.0. Airport 4 links all relevant stakeholders in a seamless digital environment with a focus on communication and real-time data.

By Location The market is divided into three sections: airside, landside, and terminal side. With a 44.3% market share, the airside segment dominates the industry as it is largely used to improve the management of ground personnel and speed up aircraft turnaround. Airside procedures like aircraft parking are therefore estimated to be more necessary throughout the forecast timeframe.

Facilities on the airside offer general security for the safe operation of aircraft, including video monitoring systems, radar obstacle detection, and warning alarms for the protection of passengers. Facilities on land include parking lots, loading docks, road networks, and terminals for people and freight. However, a sizeable share of the global smart airport industry is also made up of the terminal side segment.

Smart Airport Construction Market Competitive Landscape:

In July 2022 SITA established a co-innovation partnership with Indicio, a leader in open-source verifiable data technology and trusted digital ecosystems, to hasten the creation and adoption of travel-related digital IDs.

Under the Clean Aviation HECATE project of the European Union in 2025, Collins Aerospace will oversee the development of new high-voltage electric power distribution technology. Collins will be in charge of the project's steering committee for HECATE, which stands for Hybrid-ElectriC Regional Aircraft Distribution Technologies, while Safran will be the technical coordinator. In addition to Thales, Diehl Aerospace, Airbus Defence and Space, Leonardo, and numerous institutions, the two businesses will collaborate with a group of 37 partners from the European aerospace industry spread over ten nations. Approximately €34 million ($36.76 million) in financing will go to the HECATE partnership from Clean Aviation, while €6 million ($6.49 million) will come from UK Research and Innovation.

Smart Airport Construction Market Scope:

|

Smart Airport Construction Market |

|

|

Market Size in 2025 |

USD 8.84 Billion |

|

Market Size in 2032 |

USD 11.90 Billion |

|

CAGR (2026-2032) |

4.33% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segment Scope |

By Application

|

|

By Platform

|

|

|

By Airport Model

|

|

|

By Location

|

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Smart Airport Construction Market Key Players:

- Amadeus IT Group SA

- CISCO System Inc

- Collins Aerospace

- Daifuku Co. Ltd.

- Ascent Technologies

- Honeywell International Inc.

- Huawei Technologies Co. Ltd

- IBM Corporation

- Indra Sistemas S.A.

- ITA

- L3Harris Technologies Inc.

- Raytheon Company

- RESA, Rockwell Collins Inc.

- Lufthansa Systems GmbH & Co. KG.

- Sabre Corporation

- Siemens AG

- SITA

- Thales Group

- T-Systems

- Vision-Box

- Wipro Limited

- Ascent Technology Inc.

- Amadeus IT Group

- Huawei Investment & Holding Co. Ltd.

- Ascent technology, Inc

Frequently Asked Questions

The Smart Airport Construction Market size is expected to reach USD 11.90 Billion by 2032.

The major players in the Smart Airport Construction Market include Amadeus IT Group SA CISCO System Inc. Collins Aerospace Daifuku Co. Ltd. Ascent Technologies Honeywell International Inc. Huawei Technologies Co. Ltd IBM Corporation Indra Sistemas S.A. ITA L3Harris Technologies Inc. Raytheon Company RESA, Rockwell Collins Inc. Lufthansa Systems GmbH & Co. KG. Sabre Corporation Siemens AG SITA Thales Group T-Systems Vision-Box Wipro Limited Ascent Technology Inc. Amadeus IT Group Huawei Investment & Holding Co. Ltd. Ascent technology, inc.

The expected CAGR of the Smart Airport Construction Market is 4.33% from 2026 to 2032.

The North American market dominated the Smart Airport Construction Market by Region in 2025.

1. Global Smart Airport Construction Market: Research Methodology

2. Global Smart Airport Construction Market: Executive Summary

3. Global Smart Airport Construction Market: Competitive Landscape

3.1. Stellar Competition Matrix

3.2. Competitive Landscape

3.3. Key Players Benchmarking

3.4. Market Structure

3.4.1. Market Leaders

3.4.2. Market Followers

3.4.3. Emerging Players

3.5. Consolidation of the Market

4. Global Smart Airport Construction Market: Dynamics

4.1. Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Market Drivers by Region

4.2.1. North America

4.2.2. Europe

4.2.3. Asia Pacific

4.2.4. Middle East and Africa

4.2.5. South America

4.3. Market Restraints

4.4. Market Opportunities

4.5. Market Challenges

4.6. PORTER’s Five Forces Analysis

4.7. PESTLE Analysis

4.8. Value Chain Analysis

4.9. Regulatory Landscape by Region

4.9.1. North America

4.9.2. Europe

4.9.3. Asia Pacific

4.9.4. Middle East and Africa

4.9.5. South America

5. Global Smart Airport Construction Market Size and Forecast by Segments (by Value USD and Volume Units)

5.1. Global Smart Airport Construction Market Size and Forecast, by Application (2025-2032)

5.1.1. Al/machine learning

5.1.2. Data visualization

5.1.3. Anomaly detection

5.1.4. Cyber security

5.1.5. Asset/resource management

5.2. Global Smart Airport Construction Market Size and Forecast, by Platform (2025-2032)

5.2.1. Hardware systems

5.2.2. Data management

5.2.3. Software systems

5.3. Global Smart Airport Construction Market Size and Forecast, by Airport Model (2025-2032)

5.3.1. Airport 1.0

5.3.2. Airport 2.0

5.3.3. Airport 3.0

5.3.4. Airport 4.0

5.4. Global Smart Airport Construction Market Size and Forecast, by Location (2025-2032)

5.4.1. Airside

5.4.2. Landside

5.4.3. Terminal side

5.5. Global Smart Airport Construction Market Size and Forecast, by Region (2025-2032)

5.5.1. North America

5.5.2. Europe

5.5.3. Asia Pacific

5.5.4. Middle East and Africa

5.5.5. South America

6. North America Global Smart Airport Construction Market Size and Forecast (by Value USD and Volume Units)

6.1. North America Global Smart Airport Construction Market Size and Forecast, by Application (2025-2032)

6.1.1. Al/machine learning

6.1.2. Data visualization

6.1.3. Anomaly detection

6.1.4. Cyber security

6.1.5. Asset/resource management

6.2. North America Global Smart Airport Construction Market Size and Forecast, by Platform (2025-2032)

6.2.1. Hardware systems

6.2.2. Data management

6.2.3. Software systems

6.3. North America Global Smart Airport Construction Market Size and Forecast, by Airport Model (2025-2032)

6.3.1. Airport 1.0

6.3.2. Airport 2.0

6.3.3. Airport 3.0

6.3.4. Airport 4.0

6.4. North America Global Smart Airport Construction Market Size and Forecast, by Location (2025-2032)

6.4.1. Airside

6.4.2. Landside

6.4.3. Terminal side

6.5. North America Global Smart Airport Construction Market Size and Forecast, by Country (2025-2032)

6.5.1. United States

6.5.2. Canada

6.5.3. Mexico

7. Europe Global Smart Airport Construction Market Size and Forecast (by Value USD and Volume Units)

7.1. Europe Global Smart Airport Construction Market Size and Forecast, by Application (2025-2032)

7.1.1. Al/machine learning

7.1.2. Data visualization

7.1.3. Anomaly detection

7.1.4. Cyber security

7.1.5. Asset/resource management

7.2. Europe Global Smart Airport Construction Market Size and Forecast, by Platform (2025-2032)

7.2.1. Hardware systems

7.2.2. Data management

7.2.3. Software systems

7.3. Europe Global Smart Airport Construction Market Size and Forecast, by Airport Model (2025-2032)

7.3.1. Airport 1.0

7.3.2. Airport 2.0

7.3.3. Airport 3.0

7.3.4. Airport 4.0

7.4. Europe Global Smart Airport Construction Market Size and Forecast, by Location (2025-2032)

7.4.1. Airside

7.4.2. Landside

7.4.3. Terminal side

7.5. Europe Global Smart Airport Construction Market Size and Forecast, by Country (2025-2032)

7.5.1. UK

7.5.2. France

7.5.3. Germany

7.5.4. Italy

7.5.5. Spain

7.5.6. Sweden

7.5.7. Austria

7.5.8. Rest of Europe

8. Asia Pacific Global Smart Airport Construction Market Size and Forecast (by Value USD and Volume Units)

8.1. Asia Pacific Global Smart Airport Construction Market Size and Forecast, by Application (2025-2032)

8.1.1. Al/machine learning

8.1.2. Data visualization

8.1.3. Anomaly detection

8.1.4. Cyber security

8.1.5. Asset/resource management

8.2. Asia Pacific Global Smart Airport Construction Market Size and Forecast, by Platform (2025-2032)

8.2.1. Hardware systems

8.2.2. Data management

8.2.3. Software systems

8.3. Asia Pacific Global Smart Airport Construction Market Size and Forecast, by Airport Model (2025-2032)

8.3.1. Airport 1.0

8.3.2. Airport 2.0

8.3.3. Airport 3.0

8.3.4. Airport 4.0

8.4. Asia Pacific Global Smart Airport Construction Market Size and Forecast, by Location (2025-2032)

8.4.1. Airside

8.4.2. Landside

8.4.3. Terminal side

8.5. Asia Pacific Global Smart Airport Construction Market Size and Forecast, by Country (2025-2032)

8.5.1. China

8.5.2. S Korea

8.5.3. Japan

8.5.4. India

8.5.5. Australia

8.5.6. Indonesia

8.5.7. Malaysia

8.5.8. Vietnam

8.5.9. Taiwan

8.5.10. Bangladesh

8.5.11. Pakistan

8.5.12. Rest of Asia Pacific

9. Middle East and Africa Global Smart Airport Construction Market Size and Forecast (by Value USD and Volume Units)

9.1. Middle East and Africa Global Smart Airport Construction Market Size and Forecast, by Application (2025-2032)

9.1.1. Al/machine learning

9.1.2. Data visualization

9.1.3. Anomaly detection

9.1.4. Cyber security

9.1.5. Asset/resource management

9.2. Middle East and Africa Global Smart Airport Construction Market Size and Forecast, by Platform (2025-2032)

9.2.1. Hardware systems

9.2.2. Data management

9.2.3. Software systems

9.3. Middle East and Africa Global Smart Airport Construction Market Size and Forecast, by Airport Model (2025-2032)

9.3.1. Airport 1.0

9.3.2. Airport 2.0

9.3.3. Airport 3.0

9.3.4. Airport 4.0

9.4. Middle East and Africa Global Smart Airport Construction Market Size and Forecast, by Location (2025-2032)

9.4.1. Airside

9.4.2. Landside

9.4.3. Terminal side

9.5. Middle East and Africa Global Smart Airport Construction Market Size and Forecast, by Country (2025-2032)

9.5.1. South Africa

9.5.2. GCC

9.5.3. Egypt

9.5.4. Nigeria

9.5.5. Rest of ME&A

10. South America Global Smart Airport Construction Market Size and Forecast (by Value USD and Volume Units)

10.1. South America Global Smart Airport Construction Market Size and Forecast, by Application (2025-2032)

10.1.1. Al/machine learning

10.1.2. Data visualization

10.1.3. Anomaly detection

10.1.4. Cyber security

10.1.5. Asset/resource management

10.2. South America Global Smart Airport Construction Market Size and Forecast, by Platform (2025-2032)

10.2.1. Hardware systems

10.2.2. Data management

10.2.3. Software systems

10.3. South America Global Smart Airport Construction Market Size and Forecast, by Airport Model (2025-2032)

10.3.1. Airport 1.0

10.3.2. Airport 2.0

10.3.3. Airport 3.0

10.3.4. Airport 4.0

10.4. South America Global Smart Airport Construction Market Size and Forecast, by Location (2025-2032)

10.4.1. Airside

10.4.2. Landside

10.4.3. Terminal side

10.5. South America Global Smart Airport Construction Market Size and Forecast, by Country (2025-2032)

10.5.1. Brazil

10.5.2. Argentina

10.5.3. Rest of South America

11. Company Profile: Key players

11.1.1. Amadeus IT Group SA

11.1.2. Company Overview

11.1.3. Financial Overview

11.1.4. Business Portfolio

11.1.5. SWOT Analysis

11.1.6. Business Strategy

11.1.7. Recent Developments

11.2. CISCO System Inc

11.3. Collins Aerospace

11.4. Daifuku Co. Ltd.

11.5. Ascent Technologies

11.6. Honeywell International Inc.

11.7. Huawei Technologies Co. Ltd

11.8. IBM Corporation

11.9. Indra Sistemas S.A.

11.10. ITA

11.11. L3Harris Technologies Inc.

11.12. Raytheon Company

11.13. RESA, Rockwell Collins Inc.

11.14. Lufthansa Systems GmbH & Co. KG.

11.15. Sabre Corporation

11.16. Siemens AG

11.17. SITA

11.18. Thales Group

11.19. T-Systems

11.20. Vision-Box

11.21. Wipro Limited

11.22. Ascent Technology Inc.

11.23. Amadeus IT Group

11.24. Huawei Investment & Holding Co. Ltd.

11.25. Ascent technology, Inc

12. Key Findings

13. Industry Recommendation