Packaging Material Market - Global Industry Analysis and Forecast 2026 to 2034

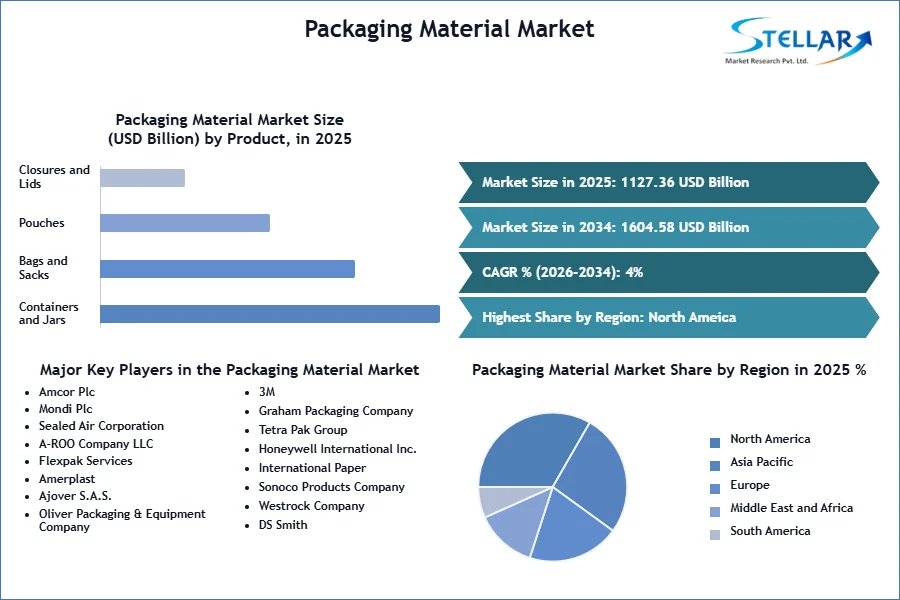

The Packaging Material Market size was valued at USD 1127.36 Bn. in 2025 and the total Global Packaging Material revenue is expected to grow at a CAGR of 4% from 2026 to 2034, reaching nearly USD 1604.58 Bn. by 2034.

Packaging Material Market Overview

Packaging material refers to any materials used to enclose, protect, and present products for transportation, storage, and sale. The report provides a comprehensive analysis of the market, including key trends, challenges, regional insights, and competitive landscape. The packaging material market is driven by sustainability and eco-friendly packaging as consumers and companies seek recyclable and biodegradable solutions. Technological advancements, such as smart packaging with QR codes and sensors, improve tracking and inventory management.

Regulatory pressures, including environmental regulations and Extended Producer Responsibility (EPR) policies, require manufacturers to adopt sustainable practices. The rapid growth of e-commerce and retail demands innovative packaging that balances protection and appeal. Consumer preferences for convenience and aesthetic appeal further drive market innovation. Additionally, economic growth and urbanization in emerging markets increase the demand for packaged goods, increasing market growth.

Investing in sustainable packaging materials, such as recyclable, biodegradable, and compostable options, is lucrative because of increasing consumer and regulatory demands. Companies developing smart packaging technologies, including QR codes, NFC tags, and advanced materials like bio-based plastics, show significant potential. Regulatory-driven innovations, particularly those aiding compliance with environmental laws and Extended Producer Responsibility (EPR) policies, present valuable opportunities. The growing e-commerce sector drives the need for durable, customizable, and eco-friendly packaging solutions. Additionally, consumer-driven innovations focusing on convenience, reseal ability, and aesthetic appeal are poised for market growth and attractive investment returns.

To get more Insights: Request Free Sample Report

Packaging Material Market Dynamics

Innovative and Smart Packaging

The integration of technologies such as QR codes, NFC tags, and sensors in packaging is becoming more common. These smart packaging solutions enhance product tracking, provide consumers with additional information, and improve inventory management. In the food and beverage sector alone, the adoption rate of smart packaging technologies increased by 12% annually from 2026 to 2032. By 2025, it is projected that two-thirds of the world’s population is expected to be urbanized. Rapid urbanization is driving a growing demand for convenient and value-added foods that meet high-quality standards.

To meet these requirements, innovations are necessary not only in the food processing sector but also in food packaging. Despite being one of the largest producers of food and agro-based products, India faces significant challenges, with 20% of these products going to waste due to inadequate processing and packaging facilities. The food processing sector in India has the potential to attract investments of Rs. 1, 50,000 crores over the next decade and generate employment for 9 million people. At present, the Indian packaging industry is increasing at a rate of 12% per annum, supported by approximately 22,000 packaging companies ranging from raw material manufacturers to machinery suppliers.

Sustainability Concerns

The growing awareness and concern about environmental sustainability have put significant pressure on the packaging industry to reduce its carbon footprint and reliance on non-renewable resources. Traditional packaging materials, especially plastics, are under scrutiny for their environmental impact. The increasing volume of packaging waste, particularly single-use plastics, presents a substantial challenge for waste management systems worldwide. According to SMR analysis, 93% of companies face challenges in delivering sustainable packaging, with the primary obstacles being the lack of necessary infrastructure (38%), consumer unwillingness to pay for solutions (38%), and retail outlets not being set up to handle changes (36%).

The shift towards sustainable materials and technologies in packaging involves higher costs, impacting profitability and pricing strategies. Sustainable packaging solutions are 20-30% more expensive than traditional options. Rising consumer demand for eco-friendly packaging, with 73% willing to change habits for reduced environmental impact, drives market growth and innovation. Stricter regulations, such as the EU’s Single-Use Plastics Directive, increase operational costs and require continuous adaptation.

Companies are exploring various sustainable packaging solutions to address environmental concerns:

Packaging Material Market Segment Analysis

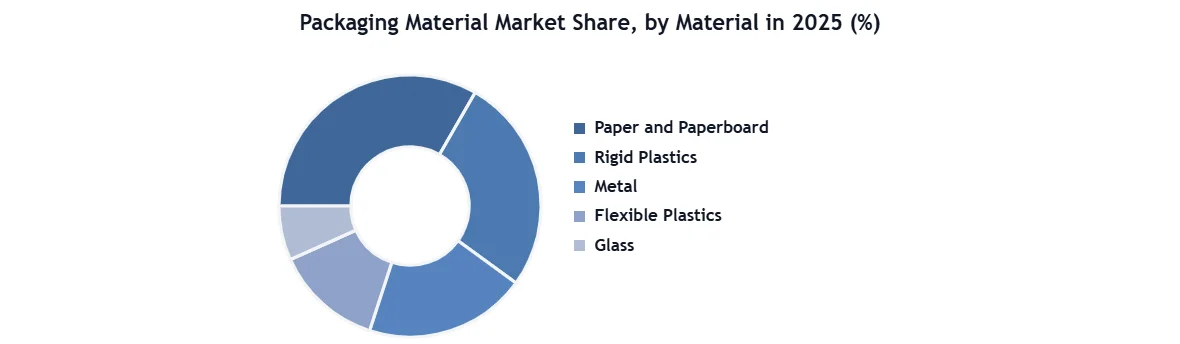

By Material, the Paper, and paperboard segment emerged as the leading market segment within the Global Packaging Material Market. As per SMR analysis, the segment is projected to maintain its dominance and exhibit a steady growth trajectory, with an anticipated Compound Annual Growth Rate (CAGR) of XX% throughout the forecast period. Paper and paperboard are highly sustainable and recyclable materials, aligning with the growing demand for eco-friendly packaging solutions. Their recyclability makes them attractive to environmentally conscious consumers and brands seeking to reduce their carbon footprint and environmental impact. Paper and paperboard are cost-effective options for packaging, particularly for mass-produced items.

They are readily available and relatively inexpensive compared to alternative materials, making them a preferred choice for budget-conscious businesses. Their affordability contributes to their widespread use in packaging across diverse sectors. Despite being a traditional packaging material, paper and paperboard continue to evolve with technological advancements and innovations. Manufacturers are developing enhanced paperboard grades with improved strength, durability, and barrier properties, expanding the range of applications for paper-based packaging. These advancements further solidify paper and paperboard's position as a leading material in the packaging industry, driving continued market growth and innovation.

Packaging Material Market Regional Insights

The packaging material market in North America is experiencing significant growth driven by technological advancements, increasing demand for sustainable packaging, and strong consumer preferences for convenience and quality. The market's growth is also supported by robust industrial activities and a well-developed retail sector. The shift to eco-friendly packaging is driven by consumer awareness and stringent environmental regulations. Smart packaging technologies, such as QR codes, NFC tags, and sensors, are increasingly used to enhance product tracking, consumer engagement, and inventory management. Major companies like Coca-Cola and PepsiCo are investing in sustainable packaging, aiming for 100% recyclable materials. Efforts to improve recycling rates and infrastructure are underway, with several states implementing robust recycling programs to support the initiative.

In North America, the cost of packaging services varies depending on factors like complexity and materials used. High-tech smart packaging and sustainable materials generally incur higher costs. On average, packaging services range from USD 0.20 to USD 0.50 per unit, contingent on the chosen materials and technologies. Raw material costs fluctuate based on market dynamics, availability, and geopolitical factors. As of 2025, plastic raw materials averaged around USD 1,200 per ton, paper materials cost approximately USD 700 per ton, and metals like aluminum were priced at about USD 2,500 per ton. These costs directly impact the overall pricing and profitability of packaging services, influencing industry dynamics and market trends.

- The U.S. Environmental Protection Agency (EPA) reported that the recycling rate for packaging materials was about 50% in 2025, indicating room for improvement and growth.

Packaging Material Market Competitive Landscape

Companies like Amcor and Berry Global have introduced biodegradable packaging options made from renewable materials such as plant-based plastics or compostable materials. These products provide to the growing demand for eco-friendly packaging solutions and contribute to reducing environmental impact. Advancements in smart packaging technologies, including NFC tags, QR codes, and sensors, have been introduced by companies like Sealed Air and Sonoco. These technologies enhance product tracking, provide real-time information to consumers, and improve supply chain efficiency, driving market growth and differentiation.

- In October 2025, Berry Global unveiled its innovative Slimline collection, a lightweight tube closure solution that merges contemporary style with material versatility while reducing greenhouse gas emissions. This eco-friendly range of tube closures offers a sleek design and adaptability, significantly minimizing carbon footprints compared to traditional caps.

- September 2025 saw ProAmpac introducing its patented ProActive Recyclable RP-1000 High Barrier (HB) paper-based technology. This groundbreaking addition to ProAmpac's product portfolio delivers superior grease resistance and exceptional barrier performance against oxygen and moisture. Ideal for dry food items like candy, flavored oatmeal, and dehydrated fruit, this innovation underscores ProAmpac's commitment to sustainability and product quality.

- In April 2024, Sealed Air and Koenig & Bauer AG announced a non-binding letter of intent to expand their strategic partnership for digital printing machines. This collaboration aims to revolutionize packaging design capabilities by leveraging cutting-edge digital printing technology, equipment, and services. The partnership will accelerate the production of digitally printed materials, empowering brand owners to enhance product promotion and consumer engagement through digitally enhanced packaging.

|

Packaging Material Market Scope |

|

|

Market Size in 2025 |

USD 1127.36 Bn. |

|

Market Size in 2034 |

USD 1604.58 Bn. |

|

CAGR (2026-2034) |

4% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Segments |

By Material Paper and Paperboard Rigid Plastics Metal Flexible Plastics Glass Wood Others |

|

By Level of Packaging Primary Packaging Secondary Packaging Tertiary Packaging |

|

|

By Product Containers and Jars Bags and Sacks Pouches Closures and Lids Films and Wraps Drums & IBCs Boxes & Cartons Crates and Pallets Others |

|

|

By End Use Food & Beverages Pharmaceuticals and Healthcare Personal Care and Cosmetics Automotive Electrical and Electronics Chemicals Household Products Others |

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Player in the Packaging Material Market

- Amcor Plc

- Mondi Plc

- Sealed Air Corporation

- A-ROO Company LLC

- Flexpak Services

- Amerplast

- Ajover S.A.S.

- Oliver Packaging & Equipment Company

- 3M

- Graham Packaging Company

- Tetra Pak Group

- Honeywell International Inc.

- International Paper

- Sonoco Products Company

- Westrock Company

- DS Smith

- Berry Global

- Avery Dennison Corporation

- CCL Industries Inc

- Mayr-Melnhof Karton AG

- ProAmpac

- XXX Inc.

Frequently Asked Questions

Government regulations play a significant role in shaping the packaging material market, particularly regarding sustainability and waste management. Regulations may include mandates for recyclable or biodegradable packaging, restrictions on certain materials, and requirements for labeling and disposal.

Challenges facing the packaging material market include environmental concerns such as plastic pollution and waste management, regulatory compliance, cost pressures, and the need for continuous innovation to meet evolving consumer demands.

The Market size was valued at USD 1127.36 Billion in 2025 and the total Market revenue is expected to grow at a CAGR of 9.04% from 2026 to 2034, reaching nearly USD 1604.58 billion.

The segments covered in the market report are by Material, Level of Packaging, Product, and End Use.

1. Packaging Material Market: Research Methodology

2. Packaging Material Market: Executive Summary

3. Packaging Material Market: Competitive Landscape

3.1. Stellar Competition Matrix

3.2. Competitive Landscape

3.3. Key Players Benchmarking

3.4. Market Structure

3.4.1. Market Leaders

3.4.2. Market Followers

3.4.3. Emerging Players

3.5. Consolidation of the Market

4. Packaging Material Market: Dynamics

4.1. Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Market Restraints

4.3. Market Opportunities

4.4. Market Challenges

4.5. PORTER’s Five Forces Analysis

4.6. PESTLE Analysis

4.7. Strategies for New Entrants to Penetrate the Market

4.8. Regulatory Landscape by Region

4.8.1. North America

4.8.2. Europe

4.8.3. Asia Pacific

4.8.4. Middle East and Africa

4.8.5. South America

5. Packaging Material Market Size and Forecast by Segments (by Value in USD Billion)

5.1. Packaging Material Market Size and Forecast, by Material (2026-2034)

5.1.1. Paper and Paperboard

5.1.2. Rigid Plastics

5.1.3. Metal

5.1.4. Flexible Plastics

5.1.5. Glass

5.1.6. Wood

5.1.7. Others

5.2. Packaging Material Market Size and Forecast, by Level of Packaging (2026-2034)

5.2.1. Primary Packaging

5.2.2. Secondary Packaging

5.2.3. Tertiary Packaging

5.3. Packaging Material Market Size and Forecast, by Product (2026-2034)

5.3.1. Containers and Jars

5.3.2. Bags and Sacks

5.3.3. Pouches

5.3.4. Closures and Lids

5.3.5. Films and Wraps

5.3.6. Drums & IBCs

5.3.7. Boxes & Cartons

5.3.8. Crates and Pallets

5.3.9. Others

5.4. Packaging Material Market Size and Forecast, by End Use (2026-2034)

5.4.1. Food & Beverages

5.4.2. Pharmaceuticals and Healthcare

5.4.3. Personal Care and Cosmetics

5.4.4. Automotive

5.4.5. Electrical and Electronics

5.4.6. Chemicals

5.4.7. Household Products

5.4.8. Others

5.5. Packaging Material Market Size and Forecast, by Region (2026-2034)

5.5.1. North America

5.5.2. Europe

5.5.3. Asia Pacific

5.5.4. Middle East and Africa

5.5.5. South America

6. North America Packaging Material Market Size and Forecast (by Value in USD Billion)

6.1. North America Packaging Material Market Size and Forecast, by Material (2026-2034)

6.1.1. Paper and Paperboard

6.1.2. Rigid Plastics

6.1.3. Metal

6.1.4. Flexible Plastics

6.1.5. Glass

6.1.6. Wood

6.1.7. Others

6.2. North America Packaging Material Market Size and Forecast, by Level of Packaging (2026-2034)

6.2.1. Primary Packaging

6.2.2. Secondary Packaging

6.2.3. Tertiary Packaging

6.3. North America Packaging Material Market Size and Forecast, by Product (2026-2034)

6.3.1. Containers and Jars

6.3.2. Bags and Sacks

6.3.3. Pouches

6.3.4. Closures and Lids

6.3.5. Films and Wraps

6.3.6. Drums & IBCs

6.3.7. Boxes & Cartons

6.3.8. Crates and Pallets

6.3.9. Others

6.4. North America Packaging Material Market Size and Forecast, by End Use (2026-2034)

6.4.1. Food & Beverages

6.4.2. Pharmaceuticals and Healthcare

6.4.3. Personal Care and Cosmetics

6.4.4. Automotive

6.4.5. Electrical and Electronics

6.4.6. Chemicals

6.4.7. Household Products

6.4.8. Others

6.5. North America Packaging Material Market Size and Forecast, by Country (2026-2034)

6.5.1. UK

6.5.2. France

6.5.3. Germany

6.5.4. Italy

6.5.5. Spain

6.5.6. Sweden

6.5.7. Austria

6.5.8. Rest of Europe

7. Asia Pacific Packaging Material Market Size and Forecast (by Value in USD Billion)

7.1. Asia Pacific Packaging Material Market Size and Forecast, by Material (2026-2034)

7.1.1. Paper and Paperboard

7.1.2. Rigid Plastics

7.1.3. Metal

7.1.4. Flexible Plastics

7.1.5. Glass

7.1.6. Wood

7.1.7. Others

7.2. Asia Pacific Packaging Material Market Size and Forecast, by Level of Packaging (2026-2034)

7.2.1. Primary Packaging

7.2.2. Secondary Packaging

7.2.3. Tertiary Packaging

7.3. Asia Pacific Packaging Material Market Size and Forecast, by Product (2026-2034)

7.3.1. Containers and Jars

7.3.2. Bags and Sacks

7.3.3. Pouches

7.3.4. Closures and Lids

7.3.5. Films and Wraps

7.3.6. Drums & IBCs

7.3.7. Boxes & Cartons

7.3.8. Crates and Pallets

7.3.9. Others

7.4. Asia Pacific Packaging Material Market Size and Forecast, by End Use (2026-2034)

7.4.1. Food & Beverages

7.4.2. Pharmaceuticals and Healthcare

7.4.3. Personal Care and Cosmetics

7.4.4. Automotive

7.4.5. Electrical and Electronics

7.4.6. Chemicals

7.4.7. Household Products

7.4.8. Others

7.5. Asia Pacific Packaging Material Market Size and Forecast, by Country (2026-2034)

7.5.1. China

7.5.2. S Korea

7.5.3. Japan

7.5.4. India

7.5.5. Australia

7.5.6. Indonesia

7.5.7. Malaysia

7.5.8. Vietnam

7.5.9. Taiwan

7.5.10. Bangladesh

7.5.11. Pakistan

7.5.12. Rest of Asia Pacific

8. Middle East and Africa Packaging Material Market Size and Forecast (by Value in USD Billion)

8.1. Middle East and Africa Packaging Material Market Size and Forecast, by Material (2026-2034)

8.1.1. Paper and Paperboard

8.1.2. Rigid Plastics

8.1.3. Metal

8.1.4. Flexible Plastics

8.1.5. Glass

8.1.6. Wood

8.1.7. Others

8.2. Middle East and Africa Packaging Material Market Size and Forecast, by Level of Packaging (2026-2034)

8.2.1. Primary Packaging

8.2.2. Secondary Packaging

8.2.3. Tertiary Packaging

8.3. Middle East and Africa Packaging Material Market Size and Forecast, by Product (2026-2034)

8.3.1. Containers and Jars

8.3.2. Bags and Sacks

8.3.3. Pouches

8.3.4. Closures and Lids

8.3.5. Films and Wraps

8.3.6. Drums & IBCs

8.3.7. Boxes & Cartons

8.3.8. Crates and Pallets

8.3.9. Others

8.4. Middle East and Africa Packaging Material Market Size and Forecast, by End Use (2026-2034)

8.4.1. Food & Beverages

8.4.2. Pharmaceuticals and Healthcare

8.4.3. Personal Care and Cosmetics

8.4.4. Automotive

8.4.5. Electrical and Electronics

8.4.6. Chemicals

8.4.7. Household Products

8.4.8. Others

8.5. Middle East and Africa Packaging Material Market Size and Forecast, by Country (2026-2034)

8.5.1. South Africa

8.5.2. GCC

8.5.3. Egypt

8.5.4. Nigeria

8.5.5. Rest of ME&A

9. South America Packaging Material Market Size and Forecast (by Value in USD Billion)

9.1. South America Packaging Material Market Size and Forecast, by Material (2026-2034)

9.1.1. Paper and Paperboard

9.1.2. Rigid Plastics

9.1.3. Metal

9.1.4. Flexible Plastics

9.1.5. Glass

9.1.6. Wood

9.1.7. Others

9.2. South America Packaging Material Market Size and Forecast, by Level of Packaging (2026-2034)

9.2.1. Primary Packaging

9.2.2. Secondary Packaging

9.2.3. Tertiary Packaging

9.3. South America Packaging Material Market Size and Forecast, by Product (2026-2034)

9.3.1. Containers and Jars

9.3.2. Bags and Sacks

9.3.3. Pouches

9.3.4. Closures and Lids

9.3.5. Films and Wraps

9.3.6. Drums & IBCs

9.3.7. Boxes & Cartons

9.3.8. Crates and Pallets

9.3.9. Others

9.4. South America Packaging Material Market Size and Forecast, by End Use (2026-2034)

9.4.1. Food & Beverages

9.4.2. Pharmaceuticals and Healthcare

9.4.3. Personal Care and Cosmetics

9.4.4. Automotive

9.4.5. Electrical and Electronics

9.4.6. Chemicals

9.4.7. Household Products

9.4.8. Others

9.5. South America Packaging Material Market Size and Forecast, by Country (2026-2034)

9.5.1. Brazil

9.5.2. Argentina

9.5.3. Rest of South America

10. Company Profile: Key players

10.1. Amcor Plc

10.1.1. Company Overview

10.1.2. Financial Overview

10.1.3. Business Portfolio

10.1.4. SWOT Analysis

10.1.5. Business Strategy

10.1.6. Recent Developments

10.2. Mondi Plc

10.3. Sealed Air Corporation

10.4. A-ROO Company LLC

10.5. Flexpak Services

10.6. Amerplast

10.7. Ajover S.A.S.

10.8. Oliver Packaging & Equipment Company

10.9. 3M

10.10. Graham Packaging Company

10.11. Tetra Pak Group

10.12. Honeywell International Inc.

10.13. International Paper

10.14. Sonoco Products Company

10.15. Westrock Company

10.16. DS Smith

10.17. Berry Global

10.18. Avery Dennison Corporation

10.19. CCL Industries Inc

10.20. Mayr-Melnhof Karton AG

10.21. ProAmpac

10.22. XXX Inc.

11. Key Findings

12. Industry Recommendation