Next-Generation Industrial Metrology and Inspection Market Global Industry Analysis and Forecast (2026-2032)

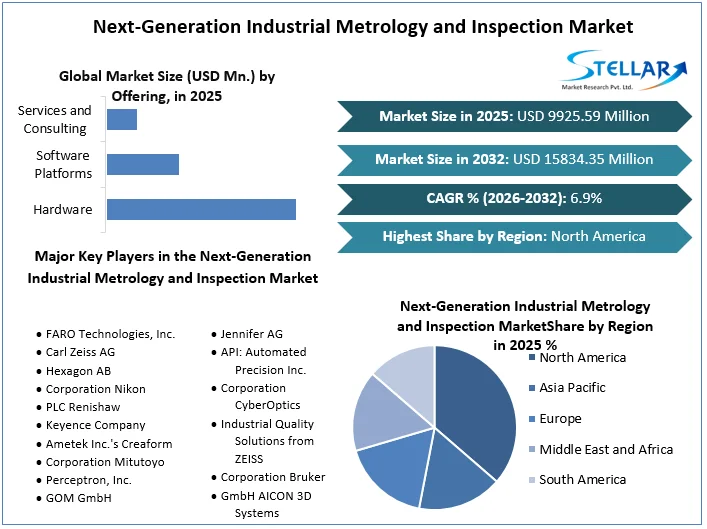

The Next-Generation Industrial Metrology and Inspection Market is expected to grow at a 6.9% CAGR from 2026 to 2032, from USD 9925.59 Million to USD 15834.35 Million.

Next-Generation Industrial Metrology and Inspection Market overview:

Technology improvements and the rising demand for accuracy and quality control across a variety of industries are driving a dramatic shift in the market for next-generation industrial metrology and inspection. This market includes a broad spectrum of cutting-edge technologies, including 3D scanning, laser-based measurement devices, sophisticated imaging methods, and analytics powered by artificial intelligence. By making it possible for complicated components, assemblies, and products to be inspected more quickly, accurately, and automatically, these advances are altering traditional manufacturing processes.

These cutting-edge metrology and inspection technologies are being used by manufacturers to increase production efficiency, decrease faults, and guarantee compliance with high industry standards. Given their struggles with complex designs, close tolerances, and the demand for trustworthy quality assurance, the automotive, aerospace, electronics, and healthcare industries stand to gain the most from these developments. Operations are further streamlined by the integration of real-time data analysis and cloud-based systems, enabling predictive maintenance and process optimization.

To get more Insights: Request Free Sample Report

Next-Generation Industrial Metrology and Inspection Market dynamics:

Drivers: Numerous dynamic forces that are altering the precise measurement and quality assurance landscape are propelling the next generation of industrial metrology and inspection markets. The main force behind this shift is technological innovation, which has redefined conventional inspection techniques through breakthroughs like 3D scanning, laser-based measurements, and AI-powered analytics. These developments not only improve accuracy but also enable automation, meeting the need for quicker and more effective inspection processes in the sector. Real-time data analysis and predictive maintenance are integrated as part of the Industry 4.0 paradigm, which is a key factor in raising quality control to a proactive level. Demand is increasing as a result of this metrology and smart manufacturing convergence, especially in industries like aerospace and electronics where strict quality standards are crucial.

In addition, the growth of additive manufacturing has created a critical demand for new metrology technologies to confirm the accuracy and integrity of complex 3D-printed components. Established metrology organizations and creative entrepreneurs are working together to create partnerships and collaborations that are fostering synergy and producing comprehensive answers to complex problems. The need for uniform quality across diverse sites is growing as global supply chains become more complex, supporting the adoption of unified metrology and inspection standards. These factors work together to support the market's transition and catapult it into an era of previously unheard-of accuracy, efficiency, and quality control across many industries.

Restraints: The Next-Generation Industrial Metrology and Inspection Market has a bright future, but it also faces some obstacles that will slow its expansion. The difficulty of incorporating these cutting-edge technologies into current manufacturing processes is one major challenge. Particularly for small and medium-sized firms (SMEs) with limited resources, the high initial expenses of procuring and integrating next-generation metrology and inspection systems might be a hurdle. A skills gap that could impede the seamless adoption of these technologies is also created by the requirement for competent staff capable of operating and maintaining these complex systems.

Opportunities: Opportunities that could transform businesses and propel technical improvements abound in the Next-Generation Industrial Metrology and Inspection Market. The expansion of applications across several sectors represents one important opportunity. A burgeoning market for customised systems catering to particular industry needs is being created as companies come to understand the need of exact measurements and quality control.

A huge development opportunity is presented by the combination of machine learning and artificial intelligence. By enabling real-time data analysis, proactive maintenance, and anomaly detection, these technologies can improve the effectiveness of industrial operations and cut down on downtime. The development of sophisticated imaging methods and high-resolution sensors also creates opportunities for greater precision and accuracy, enabling industries to push the limits of what can be measured and inspected.

Given the growing popularity of 3D printing, the field of additive manufacturing presents a particularly interesting possibility. For additive manufacturing to be widely used in important industries, metrology solutions that address the difficulties of confirming the quality and integrity of complex 3D-printed parts are essential.

Next-Generation Industrial Metrology and Inspection Market segment analysis:

By Offering,

In 2025, the hardware sector will be in the lead.

The segmentation of the Next-Generation Industrial Metrology and Inspection Market may be used to examine it effectively since it caters to a large range of industries and applications. A sizeable portion of the market is devoted to hardware solutions, which include cutting-edge devices like 3D scanners, laser trackers, and optical inspection systems. Accurate quality control is based on these hardware solutions, which enable precise measurements, dimensions analyses, and surface evaluations.

Additionally, software platforms play a crucial role in this, providing advanced metrology software with built-in AI capabilities. By enabling automated measurements, data interpretation, and predictive analytics, these platforms enable industries to make wise decisions based on current information.

By Equipment,

The equipment segment analysis of the market for next-generation industrial metrology and inspection, "Driving Growth through Innovation"

The segmentation of the Next-Generation Industrial Metrology and Inspection Market based on the cutting-edge equipment it provides, meeting the complex requirements of many sectors and applications, enables a thorough understanding of the market. The use of 3D scanners and laser scanning systems, which make use of cutting-edge technology to record precise surface data and object dimensions, is one important area. Coordinate measuring machines (CMMs), which use tactile or non-contact probes to ensure accuracy and quality verification, are crucial in dimensional analysis.

Another important category is optical inspection systems, which employ advanced imaging methods like structured light to evaluate surface properties, dimensions, and flaws without direct physical touch. With the addition of Computed Tomography (CT) Scanners, a potent 3D imaging solution is now available that combines X-ray technology and computer reconstruction to provide thorough interior and external component insights.

By Application,

The automotive and transportation sector is anticipated to have rapid growth.

Automobile Industry is a crucial sector, the automobile industry depends on sophisticated inspection and metrology technology to guarantee the precision and dependability of parts. These solutions help meet safety requirements, enhance performance, and guarantee high-quality vehicles in general. In aerospace and defense applications, where precision is essential, metrology is crucial. Precision measurement and inspection are necessary to achieve high quality standards, assuring operational safety and reliability for anything from defense equipment to aircraft components.

Next-Generation Industrial Metrology and Inspection Market regional insights:

The Next-Generation Industrial Metrology and Inspection Market benefits from North America's leadership in technological innovation and implementation. High-precision measurement and inspection solutions are required by the region's developed manufacturing sectors, including the automotive and aerospace industries, to guarantee product quality, safety, and legal compliance. Numerous advanced metrology equipment producers and service companies, serving a variety of industries, are located in the United States and Canada. Furthermore, the demand for state-of-the-art metrology technology is being further fueled by the explosive rise of sectors like additive manufacturing and medical devices.

Industrial growth in the Asia-Pacific area is accelerating, propelled by developing economies in Southeast Asia as well as nations like China, Japan, and South Korea. Manufacturing behemoths are implementing next-generation metrology technologies to guarantee quality, accuracy, and efficiency, particularly in the electronics and automotive sectors. Advanced metrology tools are crucial for the electronics sector since its components' complexity and miniaturization need for exact measurement. Further accelerating the use of cutting-edge metrology solutions is Asia-Pacific's growing emphasis on technical development and automation in manufacturing processes.

The Middle East and Africa are seeing considerable industrial growth, especially in the manufacturing, construction, and oil and gas industries. The region is seeing an increase in demand for precise metrology and inspection instruments as it makes infrastructure investments and diversifies its economy. High-precision measurement is necessary for safety and performance in sectors like aerospace and the energy industry. Advanced metrology solutions are being used even though the market is still in its early stages of development due to a greater emphasis on quality, safety, and compliance.

Due to its growing manufacturing sector, automotive industry, investments in technology, and innovation, China in particular has been a major engine of growth. The advanced electronics and automotive sectors of Japan and South Korea have also significantly fueled the demand for solutions for precise measurement and quality control.

In conclusion, regional perspectives demonstrate how the Next-Generation Industrial Metrology and Inspection Market adapts to various industrial settings. The demand, adoption, and innovation of precision measurement and quality control systems across many industries are shaped by the distinctive economic, technological, and regulatory aspects of each region.

Next-Generation Industrial Metrology and Inspection Market Scope:

|

Next-Generation Industrial Metrology and Inspection Market |

|

|

Market Size in 2025 |

USD 9925.59 Million |

|

Market Size in 2032 |

USD 15834.35 Million |

|

CAGR (2026-2032) |

6.9% |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segment Scope |

By Offering

|

|

By Equipment

|

|

|

By Application

|

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Next-Generation Industrial Metrology and Inspection Market, key players are:

- FARO Technologies, Inc.

- Carl Zeiss AG

- Hexagon AB

- Corporation Nikon

- PLC Renishaw

- Keyence Company

- Ametek Inc.'s Creaform

- Corporation Mitutoyo

- Perceptron, Inc.

- GOM GmbH

- Jennifer AG

- API: Automated Precision Inc.

- Corporation CyberOptics

- Industrial Quality Solutions from ZEISS

- Corporation Bruker

- GmbH AICON 3D Systems

- Group Metrologic

- (QVI) Quality Vision International

- Software Innovations Inc.

- KLA Group Inc.

Frequently Asked Questions

The segments covered in the market report are by Offering by Equipment, by Application and Region.

The global Next-Generation Industrial Metrology and Inspection market is growing at a significant rate of 6.9% during the forecast period.

The global Next-Generation Industrial Metrology and Inspection Market is studied from 2025 to 2032.

The market size of the market in 2025 was valued at USD 9925.59 million.

1. Research Methodology

1.1 Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Research Assumption

2. Next-Generation Industrial Metrology and Inspection Market: Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026– 2032) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Global Next-Generation Industrial Metrology and Inspection Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Business Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. New Launches and Innovations

4. Next-Generation Industrial Metrology and Inspection Market: Dynamics

4.1. Next-Generation Industrial Metrology and Inspection Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Next-Generation Industrial Metrology and Inspection Market Drivers

4.3. Next-Generation Industrial Metrology and Inspection Market Restraints

4.4. Next-Generation Industrial Metrology and Inspection Market Opportunities

4.5. Next-Generation Industrial Metrology and Inspection Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factor

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Regulatory Landscape

4.9.1. Market Regulation by Region

4.9.1.1. North America

4.9.1.2. Europe

4.9.1.3. Asia Pacific

4.9.1.4. Middle East and Africa

4.9.1.5. South America

4.9.2. Impact of Regulations on Market Dynamics

4.9.3. Government Schemes and Initiatives

5. Next-Generation Industrial Metrology and Inspection Market: Global Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

5.1. Next-Generation Industrial Metrology and Inspection Market Size and Forecast, by Offering (2025-2032)

5.1.1. Hardware

5.1.2. Software Platforms

5.1.3. Services and Consulting

5.2. Next-Generation Industrial Metrology and Inspection Market Size and Forecast, by Equipment (2025-2032)

5.2.1. 3D Scanners and Laser Scanning Systems

5.2.2. Coordinate Measuring Machines (CMMs)

5.2.3. Optical Inspection Systems

5.2.4. Computed Tomography (CT) Scanners

5.2.5. Non-Destructive Testing (NDT) Equipment

5.3. Next-Generation Industrial Metrology and Inspection Market Size and Forecast, by Application (2025-2032)

5.3.1. Automotive Industry

5.3.2. Aerospace and Defense

5.3.3. Electronics and Semiconductor Manufacturing

5.3.4. Medical Devices and Healthcare

5.4. Next-Generation Industrial Metrology and Inspection Market Size and Forecast, by Region (2025-2032)

5.4.1. North America

5.4.2. Europe

5.4.3. Asia Pacific

5.4.4. Middle East and Africa

5.4.5. South America

6. North America Next-Generation Industrial Metrology and Inspection Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

6.1. North America Next-Generation Industrial Metrology and Inspection Market Size and Forecast, by Offering (2025-2032)

6.1.1. Hardware

6.1.2. Software Platforms

6.1.3. Services and Consulting

6.2. North America Next-Generation Industrial Metrology and Inspection Market Size and Forecast, by Equipment (2025-2032)

6.2.1. 3D Scanners and Laser Scanning Systems

6.2.2. Coordinate Measuring Machines (CMMs)

6.2.3. Optical Inspection Systems

6.2.4. Computed Tomography (CT) Scanners

6.2.5. Non-Destructive Testing (NDT) Equipment

6.3. North America Next-Generation Industrial Metrology and Inspection Market Size and Forecast, by Application (2025-2032)

6.3.1. Automotive Industry

6.3.2. Aerospace and Defense

6.3.3. Electronics and Semiconductor Manufacturing

6.3.4. Medical Devices and Healthcare

6.4. North America Next-Generation Industrial Metrology and Inspection Market Size and Forecast, by Country (2025-2032)

6.4.1. United States

6.4.2. Canada

6.4.3. Mexico

7. Europe Next-Generation Industrial Metrology and Inspection Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

7.1. Europe Next-Generation Industrial Metrology and Inspection Market Size and Forecast, by Offering (2025-2032)

7.2. Europe Next-Generation Industrial Metrology and Inspection Market Size and Forecast, by Equipment (2025-2032)

7.3. Europe Next-Generation Industrial Metrology and Inspection Market Size and Forecast, by Application (2025-2032)

7.4. Europe Next-Generation Industrial Metrology and Inspection Market Size and Forecast, by Country (2025-2032)

7.4.1. United Kingdom

7.4.2. France

7.4.3. Germany

7.4.4. Italy

7.4.5. Spain

7.4.6. Sweden

7.4.7. Austria

7.4.8. Rest of Europe

8. Asia Pacific Next-Generation Industrial Metrology and Inspection Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

8.1. Asia Pacific Next-Generation Industrial Metrology and Inspection Market Size and Forecast, by Offering (2025-2032)

8.2. Asia Pacific Next-Generation Industrial Metrology and Inspection Market Size and Forecast, by Equipment (2025-2032)

8.3. Asia Pacific Next-Generation Industrial Metrology and Inspection Market Size and Forecast, by Application (2025-2032)

8.4. Asia Pacific Next-Generation Industrial Metrology and Inspection Market Size and Forecast, by Country (2025-2032)

8.4.1. China

8.4.2. S Korea

8.4.3. Japan

8.4.4. India

8.4.5. Australia

8.4.6. Indonesia

8.4.7. Malaysia

8.4.8. Vietnam

8.4.9. Taiwan

8.4.10. Rest of Asia Pacific

9. Middle East and Africa Next-Generation Industrial Metrology and Inspection Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

9.1. Middle East and Africa Next-Generation Industrial Metrology and Inspection Market Size and Forecast, by Offering (2025-2032)

9.2. Middle East and Africa Next-Generation Industrial Metrology and Inspection Market Size and Forecast, by Equipment (2025-2032)

9.3. Middle East and Africa Next-Generation Industrial Metrology and Inspection Market Size and Forecast, by Application (2025-2032)

9.4. Middle East and Africa Next-Generation Industrial Metrology and Inspection Market Size and Forecast, by Country (2025-2032)

9.4.1. South Africa

9.4.2. GCC

9.4.3. Nigeria

9.4.4. Rest of ME&A

10. South America Next-Generation Industrial Metrology and Inspection Market Size and Forecast by Segmentation (by Value in USD Million) (2025-2032)

10.1. South America Next-Generation Industrial Metrology and Inspection Market Size and Forecast, by Offering (2025-2032)

10.2. South America Next-Generation Industrial Metrology and Inspection Market Size and Forecast, by Equipment (2025-2032)

10.3. South America Next-Generation Industrial Metrology and Inspection Market Size and Forecast, by Application (2025-2032)

10.4. South America Next-Generation Industrial Metrology and Inspection Market Size and Forecast, by Country (2025-2032)

10.4.1. Brazil

10.4.2. Argentina

10.4.3. Rest Of South America

11. Company Profile: Key Players

11.1. FARO Technologies, Inc.

11.1.1. Company Overview

11.1.2. Business Portfolio

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Carl Zeiss AG

11.3. Hexagon AB

11.4. Corporation Nikon

11.5. PLC Renishaw

11.6. Keyence Company

11.7. Ametek Inc.'s Creaform

11.8. Corporation Mitutoyo

11.9. Perceptron, Inc.

11.10. GOM GmbH

11.11. Jennifer AG

11.12. API: Automated Precision Inc.

11.13. Corporation CyberOptics

11.14. Industrial Quality Solutions from ZEISS

11.15. Corporation Bruker

11.16. GmbH AICON 3D Systems

11.17. Group Metrologic

11.18. (QVI) Quality Vision International

11.19. Software Innovations Inc.

11.20. KLA Group Inc.

12. Key Findings

13. Analyst Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook