Full-Service Carrier Market Industry Analysis and Forecast (2026-2032)

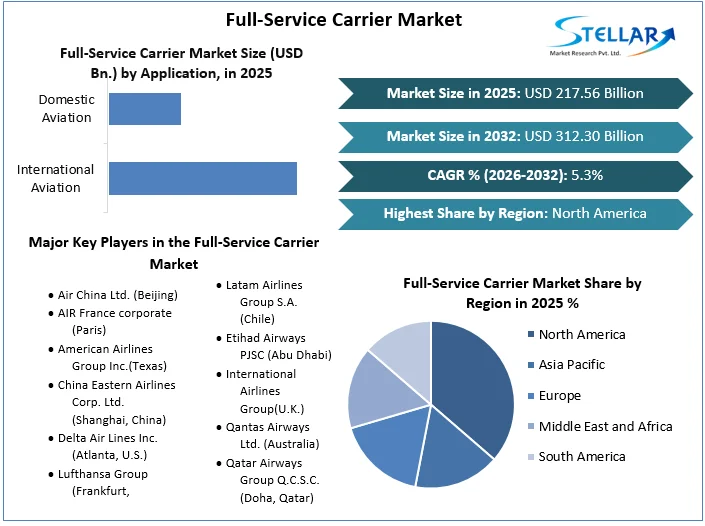

The Full-Service Carrier Market size was valued at USD 217.56 Bn. in 2025 and the total Global Full-Service Carrier revenue is expected to grow at a CAGR of 5.3% from 2026 to 2032, reaching nearly USD 312.30 Bn. by 2032.

Full-Service Carrier Market Overview

A Full-Service Carrier (FSC) refers to an airline that offers its passengers a wide range of services, including in-flight meals, entertainment, checked baggage, and various other amenities. FSCs focus on providing high customer service and comfort throughout the flight experience. These carriers usually operate on scheduled routes and cater to both domestic and international travel.

The growing middle-class population, rising levels of disposable income, and an increase in international tourism are all factors driving this growth. Also driving the market's growth are technological advancements and innovative aircraft, which have contributed to performance and improved passenger journey experience.

Our report on the Global Full-Service Carrier Market provides a comprehensive analysis of the market dynamics, such as drivers, restraints, opportunities, and challenges, which are expected to have a significant impact on the market during the forecast period. It also provides a detailed analysis of the competitive landscape and the key strategies adopted by the players in the market. The report provides an in-depth analysis of the market size, segmentation, growth prospects, and geographical presence. The competitive landscape section also includes key development strategies, market share, and market ranking analysis of the Key players globally. International routes require a lot of concern about full-service carriers because they regularly generate more income than domestic flights. Full-service carriers connect big cities and provide profitable long-haul markets through international flights.

- In 2023, Delta Airlines successfully served over 190 million customers. Delta has a team of 100,000 individuals dedicated to providing exceptional customer service daily across 4,000 flights to over 290 destinations worldwide. This network helps connect people with various locations on 6 continents.

- According to SMR, JetBlue secured the top 7th ranked and won the best U.S. airline for customer experience because it offers complimentary Wi-Fi and seatback TV screens for every passenger.

To get more Insights: Request Free Sample Report

Full-Service Carrier Market Dynamics

Full-Service Carrier Market Thrives on Growing Demand for Premium Travel Services and International Trade

The full-service carrier market is experiencing robust growth, driven by the increasing number of air passengers and international trade and tourism growth. With global economies recovering from the pandemic, there has been a significant rise in consumer expenditure on air travel, leading to a higher demand for the Premium flight services provided by full-service carriers. These airlines cater to passengers willing to pay higher fares for amenities like comfortable seating, gourmet meals, in-flight entertainment, and personalized service. With the increasing disposable incomes and the rise of the global middle-class families, particularly in developing countries, more individuals can afford air travel and choose the improved services offered by full-service airlines.

The growth of corporate travel budgets and the need for efficient business travel drives the demand for full-service carriers. One of the top-selling factor for these airlines is their enhanced comfort and amenities, catering to business and leisure travelers seeking a more luxurious journey. Full-service airlines offer luxurious amenities like lie-flat seats, gourmet meals, and exclusive lounges, making them a top choice for discerning travelers.

The growth of international trade and globalization has increased the demand for full-service carriers. As businesses expand their operations across borders, there is an increasing need for convenient and efficient travel options for corporate executives, employees, and cargo. the growth of e-commerce and the need for timely delivery of goods have increased the demand for air cargo services, which full-service carriers provide alongside their passenger operations. These airlines have the capability to transport high-value cargo and offer specialized handling and logistics services, making them valuable partners for businesses engaged in international trade. Full-service carriers offer extensive route networks, connecting major business hubs globally, making them attractive choices for international business travel.

Strong Competition from Low-cost Carrier (LCC)

Intense competition from low-cost carriers (LCCs) and regional airlines is encountered in the market. Low-cost carrier (LCC) airlines frequently provide tickets at cheaper rates, thereby compelling full-service carriers to contend on price and potentially eroding their profit margins. Low-cost carriers are famous for offering lower fares by operating on a simple model, which has attracted budget travelers. Low-cost carriers have forced full-service carriers to rethink their pricing strategies. Some passengers are willing to exchange premium services for lower fares offered by LCC.

Full-service operators must find ways to differentiate their offerings and communicate their service value to build customer loyalty. LCCs typically focus on direct routes and smaller airports to cut expenses. Full-service airlines need to assess the profitability of routes and expand their network to stay competitive. the presence of low-cost carriers presents challenges to the global full-service airline market, hampering its growth in the forecast period.

- In 2020, low-cost airlines represented 35 percent of the total seat capacity available globally. Hence, the dramatic increase in the share of low-cost carriers hinder the full-service carrier market growth.

Full-service carriers in the industry are significantly hampered by capacity management issues. Effectively managing supply and demand while maximizing fleet utilization is difficult, especially when taking into account the competition, changing passenger volumes, and profitability of the routes. Overcapacity can lead to revenue dilution and increased operational costs, while under-capacity risks lost revenue opportunities and customer dissatisfaction. The long lead times for aircraft procurement and route planning further complicate capacity adjustments.

Full-Service Carrier Market Segment Analysis

Based on the Services, the In-Flight Entertainment service segment held the largest market share in the Full-Service Carrier Market in 2025. According to the SMR analysis, the segment is expected to grow during the forecast period and maintain its dominance till 2032. The In-Flight Entertainment service segment has dominated because Passengers boarding on lengthy flights yearn for means to occupy themselves and remain pleased. In-flight entertainment (IFE) systems offer an array of choices such as movies, TV shows, music, and even games, enhancing the choice of stable long journeys.

Emirates is considered the leader with its extensive ICE system offering thousands of channels and movies. Others like United Airlines, Delta, and Turkish Airlines also provide robust entertainment options. Some airlines are exploring options for passengers to access their own streaming services or content libraries on board through the IFE system, so this personalization enhances the entertainment value.

Meals and Beverages have the fastest-growing segment some airlines are looking to elevate their food and beverage offerings, it is a universally growing trend. Airlines target high-paying customers, who invest in high-quality dining experiences, including gourmet meals and curated beverage selections.

- Singapore Airlines is widely regarded as offering one of the best in-flight dining experiences across all classes. Other top carriers for catering include Emirates, Qatar Airways, and ANA (All Nippon Airways).

Full-Service Carrier Market Regional Analysis

North America dominated the Full-Service Carrier Market, with a leading market share of 47.88% in 2025. The region is expected to continue growing and maintain its dominance by 2032. North America region has dominated because of the region's rich consumer base with high disposable income levels, extensive network of routes, and established airline infrastructures. North America has home to some of the world's largest and well-established full-service carriers, including Delta Air Lines, American Airlines, and United Airlines. These airlines have extensive route networks spanning domestic, regional, and international destinations, enabling them to capture a significant share of the market.

North America serves as a prominent center for business operations, boasting key financial hubs like New York, Chicago, and Toronto that fuel the need for corporate travel. Full-service carriers cater to business travelers by providing premium services, airport lounges, and convenient schedules, further solidifying their dominance in the market. The Strict regulatory environment in North America is generally conducive to the operations of full-service carriers, providing stability and support for airline growth and development of the Full-Service Carrier Market.

For instance,

- IATA reported that although North American Airlines full-year passenger traffic decreased by 65.6% compared to 2019, the region still held the world's largest proportion of passenger traffic (RPK), accounting for approximately 32.6% of global RPKs.

- In March 2022, the Canadian government disclosed support packages aimed at enhancing the infrastructure at Toronto Pearson International Airport. These packages include fresh funding for crucial infrastructure projects, with the airport set to benefit from over CAD 142 million through Transport Canada's Airport Critical Infrastructure Program.

Full-Service Carrier Market Competitive Landscape

The global Full-Service Carrier market is highly competitive and fragmented, with several major players competing for market share. Several smaller companies and startups are operating in the Full-service carrier market. These companies are focused on developing innovative new technologies for the Full-Service Carrier market more quickly and adapting easily to changing market conditions. Overall, the competitive landscape in the Full-service carrier market is rapidly evolving, with new players and technologies continually entering the market.

The full-service carrier market is highly competitive, with key players such as American Airlines, Delta Airlines, United Airlines, China Eastern Airlines, and British Airways dominating the industry. These companies offer passengers a wide range of services, including premium cabin classes, in-flight entertainment, and frequent flyer programs.

- In March 2022, DNATA has partnered with EasyJet to manage the full-service onboard catering. This strategic alliance benefits EasyJet as DNATA will provide catering services to airlines across their vast global network.

- In 2022, International Airlines Group, launched the 8th edition of its Hangar 51 Accelerator program to support startups in the aviation industry

- In August 2023, Vistara, a joint venture between the Tata Group and Singapore Airlines and the country's full-service airline, announced the addition of a Maldives service to its international network.

- In September 2023, The Tata Group's initiatives to consolidate Air India and Vistara into a single full-service carrier advance received recent endorsements from the Competition Commission of India and continued Air India's fleet modernization and aircrew development.

- ANA (All Nippon Airways) launched a Pokémon-themed aircraft, the Pikachu Jet, which features a Boeing 787-9 Dreamliner turned into a Pikachu Jet.

Full-Service Carrier Market Scope

|

Full-Service Carrier Market |

|

|

Market Size in 2025 |

USD 217.56 Bn. |

|

Market Size in 2032 |

USD 312.30 Bn. |

|

CAGR (2026-2032) |

5.3 % |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segments |

By Aircraft Type Fixed-wing aircraft Rotary-wing aircraft

|

|

By Service Meals and Beverages In-Flight Entertainment Checked Baggage Comfort Others

|

|

|

By Application International Aviation Domestic Aviation

|

|

|

Regions |

North America(United States), Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Austria, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Nigeria, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Key Player in the Full-Service Carrier Market

- Air China Ltd. (Beijing)

- AIR France corporate (Paris)

- American Airlines Group Inc.(Texas)

- China Eastern Airlines Corp. Ltd. (Shanghai, China)

- Delta Air Lines Inc. (Atlanta, U.S.)

- Lufthansa Group (Frankfurt, Germany)

- Avianca(Colombia)

- Japan Airlines Co. Ltd. (TOKYO, Japan)

- Latam Airlines Group S.A. (Chile)

- Etihad Airways PJSC (Abu Dhabi)

- International Airlines Group(U.K.)

- Qantas Airways Ltd. (Australia)

- Qatar Airways Group Q.C.S.C. (Doha, Qatar)

- Singapore Airlines Ltd.(Singapore)

- All Nippon Airways (Tokyo, Japan)

- Southwest Airlines Co.(Texas)

- Thai Airways International Public Co. Ltd. (Bangkok)

- The Emirates Group (Dubai)

- Turkish Airlines (Istanbul)

- United Airlines Inc. (Chicago)

- Air Canada (Montreal, Canada)

- Cathay Pacific Airways (Hong Kong)

- Korean Air (Seoul)

- Saudi Arabian Airlines (Saudi Arabia)

- China Southern Airlines (China)

- Air India (Delhi)

- Air France-KLM Group (France, Netherland)

- XX.inc.

Frequently Asked Questions

North America is expected to hold the highest share of the Full- full-service carrier Market.

The Full-Service Carrier Market size was valued at USD 217.56 Billion in 2025 reaching nearly USD 312.30 Billion in 2032.

The key players in the market are American Airlines (US), China Eastern Airlines (China), China Southern Airlines (China), Delta Airlines (US), United Airlines (US), Air China (China), All Nippon Airways (Japan), British Airways (England), China Eastern Airlines (China), Emirates (UAE), Lufthansa (Germany) and Turkish Airlines (Turkey).

The segments covered in the Full-Service Carrier Market report are based on Aircraft Type, Service, and Application.

1. Full-Service Carrier Market: Research Methodology

2. Full-Service Carrier Market: Executive Summary

3. Full-Service Carrier Market: Competitive Landscape

4. Potential Areas for Investment

4.1. Stellar Competition Matrix

4.2. Competitive Landscape

4.3. Key Players Benchmarking

4.4. Market Structure

4.4.1. Market Leaders

4.4.2. Market Followers

4.4.3. Emerging Players

4.5. Consolidation of the Market

4.6. Global Import-Export Analysis

5. Full-Service Carrier Market: Dynamics

5.1. Market Driver

5.1.1. Increased Focus on Sterility

5.1.2. Technological Advancements in single-use filters

5.1.3. Regulatory Requirements on Product Quality & Safety

5.2. Market Trends by Region

5.2.1. North America

5.2.2. Europe

5.2.3. Asia Pacific

5.2.4. Middle East and Africa

5.2.5. South America

5.3. Market Drivers

5.4. Market Restraints

5.5. Market Opportunities

5.6. Market Challenges

5.7. PORTER’s Five Forces Analysis

5.8. PESTLE Analysis

5.9. Strategies for New Entrants to Penetrate the Market

5.10. Regulatory Landscape by Region

5.10.1. North America

5.10.2. Europe

5.10.3. Asia Pacific

5.10.4. Middle East and Africa

5.10.5. South America

6. Full-Service Carrier Market Size and Forecast by Segments (by Value in USD Billion)

6.1. Full-Service Carrier Market Size and Forecast, by Aircraft Type (2025-2032)

6.1.1. New Fixed-wing aircraft

6.1.2. Rotary- wing aircraft

6.2. Full-Service Carrier Market Size and Forecast, by Service (2025-2032)

6.2.1. Meals and Beverages

6.2.2. In-Flight Entertainment

6.2.3. Checked Baggage

6.2.4. Comfort

6.2.5. Others

6.3. Full-Service Carrier Market Size and Forecast, by Application (2025-2032)

6.3.1. International Aviation

6.3.2. Domestic Aviation

6.4. Full-Service Carrier Market Size and Forecast, by Region (2025-2032)

6.4.1. North America

6.4.2. Europe

6.4.3. Asia Pacific

6.4.4. Middle East and Africa

6.4.5. South America

7. North America Full-Service Carrier Market Size and Forecast (by Value in USD Billion)

7.1. North America Full-Service Carrier Market Size and Forecast, by Aircraft Type (2025-2032)

7.1.1. New Fixed-wing aircraft

7.1.2. Rotary- wing aircraft

7.2. North America Full-Service Carrier Market Size and Forecast, by Service (2025-2032)

7.2.1. Meals and Beverages

7.2.2. In-Flight Entertainment

7.2.3. Checked Baggage

7.2.4. Comfort

7.2.5. Others

7.3. Full-Service Carrier Market Size and Forecast, by Application (2025-2032)

7.3.1. International Aviation

7.3.2. Domestic Aviation

7.4. North America Full-Service Carrier Market Size and Forecast, by Country (2025-2032)

7.4.1. United States

7.4.2. Canada

7.4.3. Mexico

8. Europe Full-Service Carrier Market Size and Forecast (by Value in USD Billion)

8.1. Europe Full-Service Carrier Market Size and Forecast, by Aircraft Type (2025-2032)

8.1.1. New Fixed-wing aircraft

8.1.2. Rotary- wing aircraft

8.2. Europe Full-Service Carrier Market Size and Forecast, by Service (2025-2032)

8.2.1. Meals and Beverages

8.2.2. In-Flight Entertainment

8.2.3. Checked Baggage

8.2.4. Comfort

8.2.5. Others

8.3. Full-Service Carrier Market Size and Forecast, by Application (2025-2032)

8.3.1. International Aviation

8.3.2. Domestic Aviation

8.4. Europe Full-Service Carrier Market Size and Forecast, by Country (2025-2032)

8.4.1. UK

8.4.2. France

8.4.3. Germany

8.4.4. Italy

8.4.5. Spain

8.4.6. Sweden

8.4.7. Austria

8.4.8. Rest of Europe

9. Asia Pacific Full-Service Carrier Market Size and Forecast (by Value in USD Billion)

9.1. Asia Pacific Full-Service Carrier Market Size and Forecast, by Aircraft Type (2025-2032)

9.1.1. New Fixed-wing aircraft

9.1.2. Rotary- wing aircraft

9.2. Asia Pacific Full-Service Carrier Market Size and Forecast, by Service (2025-2032)

9.2.1. Meals and Beverages

9.2.2. In-Flight Entertainment

9.2.3. Checked Baggage

9.2.4. Comfort

9.2.5. Others

9.3. Full-Service Carrier Market Size and Forecast, by Application (2025-2032)

9.3.1. International Aviation

9.3.2. Domestic Aviation

9.4. Asia Pacific Full-Service Carrier Market Size and Forecast, by Country (2025-2032)

9.4.1. China

9.4.2. S Korea

9.4.3. Japan

9.4.4. India

9.4.5. Australia

9.4.6. Indonesia

9.4.7. Malaysia

9.4.8. Vietnam

9.4.9. Taiwan

9.4.10. Bangladesh

9.4.11. Pakistan

9.4.12. Rest of Asia Pacific

10. Middle East and Africa Full-Service Carrier Market Size and Forecast (by Value in USD Billion)

10.1. Middle East and Africa Full-Service Carrier Market Size and Forecast, by Aircraft Type (2025-2032)

10.1.1. New Fixed-wing aircraft

10.1.2. Rotary- wing aircraft

10.2. Middle East and Africa Full-Service Carrier Market Size and Forecast, by Service (2025-2032)

10.2.1. Meals and Beverages

10.2.2. In-Flight Entertainment

10.2.3. Checked Baggage

10.2.4. Comfort

10.2.5. Others

10.3. Full-Service Carrier Market Size and Forecast, by Application (2025-2032)

10.3.1. International Aviation

10.3.2. Domestic Aviation

10.4. Middle East and Africa Full-Service Carrier Market Size and Forecast, by Country (2025-2032)

10.4.1. South Africa

10.4.2. GCC

10.4.3. Egypt

10.4.4. Nigeria

10.4.5. Rest of ME&A

11. South America Full-Service Carrier Market Size and Forecast (by Value in USD Billion)

11.1. South America Full-Service Carrier Market Size and Forecast, by Aircraft Type (2025-2032)

11.1.1. New Fixed-wing aircraft

11.1.2. Rotary- wing aircraft

11.2. South America Full-Service Carrier Market Size and Forecast, by Service (2025-2032)

11.2.1. Meals and Beverages

11.2.2. In-Flight Entertainment

11.2.3. Checked Baggage

11.2.4. Comfort

11.2.5. Others

11.3. Full-Service Carrier Market Size and Forecast, by Application (2025-2032)

11.3.1. International Aviation

11.3.2. Domestic Aviation

11.4. South America Full-Service Carrier Market Size and Forecast, by Country (2025-2032)

11.4.1. Brazil

11.4.2. Argentina

11.4.3. Rest of South America

12. Company Profile: Key players

12.1. Delta Air Lines Inc. (Atlanta, U.S.)

12.1.1. Company Overview

12.1.2. Financial Overview

12.1.3. Business Portfolio

12.1.4. SWOT Analysis

12.1.5. Business Strategy

12.1.6. Recent Developments

12.2. Air China Ltd. (Beijing)

12.3. AIR France corporate (Paris)

12.4. American Airlines Group Inc.(Texas)

12.5. China Eastern Airlines Corp. Ltd. (Shanghai, China)

12.6. Lufthansa Group (Frankfurt, Germany)

12.7. Avianca(Colombia)

12.8. Japan Airlines Co. Ltd. (TOKYO,Japan)

12.9. LATAM AIRLINES GROUP S.A. (Chile)

12.10. Etihad Airways PJSC (Abu Dhabi)

12.11. International Airlines Group(U.K.)

12.12. Qantas Airways Ltd. (Australia)

12.13. Qatar Airways Group Q.C.S.C. (Doha,Qatar)

12.14. Singapore Airlines Ltd.(Singapore)

12.15. All Nippon Airways (Tokyo, Japan)

12.16. Southwest Airlines Co.(Texas)

12.17. THAI AIRWAYS INTERNATIONAL PUBLIC Co. Ltd. (Bangkok)

12.18. The Emirates Group (Dubai)

12.19. Turkish Airlines (Istanbul)

12.20. United Airlines Inc. (Chicago)

12.21. Air Canada (Montreal, Canada)

12.22. Cathay Pacific Airways (Hong Kong)

12.23. Korean Air (Seoul)

12.24. Saudi Arabian Airlines (Saudi Arabia)

12.25. China Southern Airlines (China)

12.26. Air India (Delhi)

12.27. Air France-KLM Group (France)

13. Key Findings

14. Industry Recommendations