Military Simulation and Virtual Training Market - Global Industry Analysis and Forecast 2026-2032 by Platform, Application, Software

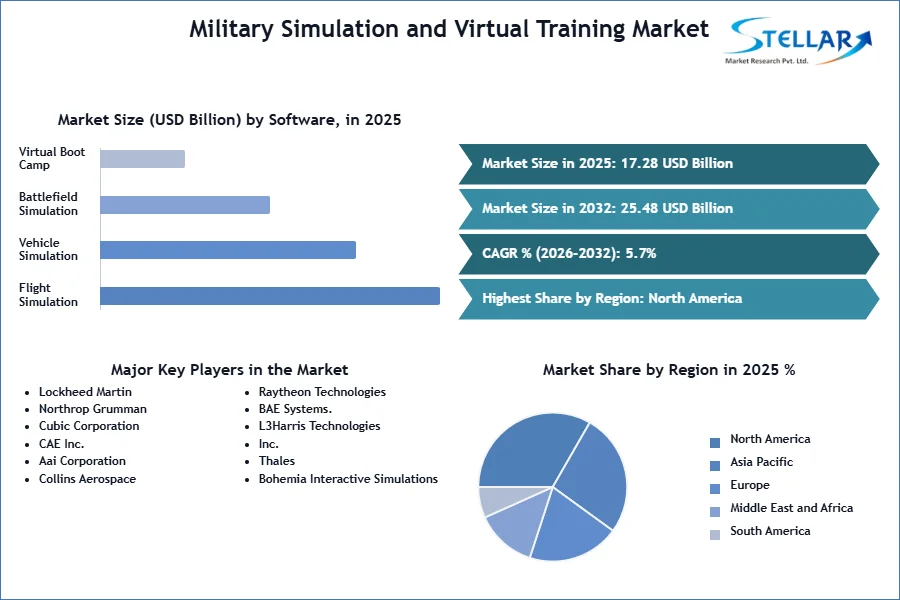

Military Simulation and Virtual Training Market size was valued at USD 17.28 Bn. in 2025 and is expected to reach USD 25.48 Bn. by 2032, at a CAGR of 5.7%.

Military Simulation and Virtual Training Market Overview

Military simulation and virtual training are training methods that use virtual and live elements to help soldiers practice skills in realistic combat scenarios, and involve training individuals on a variety of military tasks through the use of simulation technologies to generate realistic scenarios that soldiers may face in combat or during operations, this training system integrates software and technological solutions. The idea is to give military troops access to a safe, regulated, and affordable environment where they can obtain real-world experience without facing the risk of being injured during live training exercises.

Military Simulation and Virtual Training Market experiencing significant growth of XX% every year and is expected to continue its growth during the forecast period. Lockheed Martin, Northrop Grumman, L3Harris Technologies, Inc., and Raytheon Technologies are well-established players in the Military Simulation and Virtual Training Market. Lockheed Martin is a global leader in the Military Simulation and Virtual Training Market which offers a wide range of simulation solutions for various military platforms, including aircraft, ground vehicles, and naval vessels. North America region held the dominant segment in the Military Simulation and Virtual Training Market in 2025.

The Military Simulation and Virtual Training Market is mainly driven by a Safe and Realistic immersive experience of Training and a Cost-effective way of Training, which will lead to the rapid growth of the Military Simulation and Virtual Training Market globally in the forecast year 2026-2032. Cybersecurity Concerns are the main challenges in the Military Simulation and Virtual Training Market. Based on the Application, the Air segment dominated the Military Simulation and Virtual Training Market in 2025 with a share of XX%. Due to the high operational costs associated with flight training, including fuel consumption, aircraft maintenance, and pilot salaries are very high.

To get more Insights: Request Free Sample Report

Military Simulation and Virtual Training Market Dynamics

Safe and Realistic immersive experience of Training drives the Military Simulation and Virtual Training Market

The main advantages include reduced risk, increased training effectiveness, and realistic training environments. Simulators offer a safe environment that reduces risks and enhances scenario-based learning and repeated practice. By developing extremely realistic training environments, modern technologies like VR, AR, and AI train participants for the difficulties they will face in the real world. Furthermore, simulators generate useful data that may be examined to enhance training techniques and identify areas of development. Virtual pilot training was introduced mainly for safety reasons.

To conduct real-time training, there is a lot of risk involved, and requires an extensive amount of time and resources, like explosives and fuel. As a result, defense ministries are adopting simulation-based games and virtual training more frequently which drives the Military Simulation and Virtual Training Market. According to information provided by the Army’s Program Executive Office Simulation, Training and Instrumentation (PEO STRI), the STE intends to interact with and augment live training, which will enable the Army to deliver training service directly where needed.

- In January 2025, L3Harris Technologies a leading technology company, announced that it had acquired ForceX Simulation, a virtual reality (VR) and augmented reality (AR) training solutions provider for military applications.

Cost-effective way of Training drives the Military Simulation and Virtual Training Market

Defense organizations are increasingly using simulation-based training because it reduces costs while enhancing operational performance. Soldiers can be placed in different environments, situations, or locations using this software. Governments all across the world are reducing their military expenditures. Several countries' defense ministries are reducing their military spending and training allocations. The military is now more focused on finding more affordable and efficient solutions to meet their needs. Throughout the estimated time frame, these factors will likely further propel the market. These factors are expected to drive the Military Simulation and Virtual Training Market.

According to reports, the projected cost of running an F-35A aircraft operated by the USAF is USD 44,000 per flight hour. Because of virtual training the F-35 Full Mission Simulator with a 360-degree visual display system, which accurately replicates all sensors and weapons employment and uses the same software as the aircraft. The Full Mission Simulator cockpit can be reconfigured to support training on all three F-35 variants. Pilots complete roughly half of the initial qualification flights in the Full Mission Simulator for affordability and effectiveness.

- According to the US Government Accountability Office (GAO), the F-35 program sustainment costs have increased by 44%, from USD 1.1 trillion in 2018 to USD 1.58 trillion in 2025, even as the use of the F-35, and its availability, has decreased, with the F-35 Joint Program Office reporting a 21% reduction in flight hours across the program.

Military Simulation and Virtual Training Market Challenges

Cybersecurity Concerns

As VR becomes more integrated into military systems, protecting sensitive training data and simulations from cyber threats is crucial. Because these networked systems depend on computer technology, they are at risk of hacking and other cyber incursions. The Indian armed forces today face a significant threat of cyberattacks, particularly from hostile neighboring states like China and Pakistan. Cyberattacks could potentially damage or cripple critical weapons platforms, major communications and ISR (intelligence, surveillance, and reconnaissance) systems, and vital infrastructure, undermining the military’s preparedness and war-fighting capabilities.

India received 2,138 weekly cyberattacks per organization in 2025, making it the second most targeted nation in the Asia Pacific region after Taiwan. According to a recent report, released by The IBM Security Data Breach Report of 2022, the average data breach costs in India have reached a record high of ?17.5 crores, or around USD 2.2 million for the fiscal year of 2022 which is the main challenge in Military Simulation and Virtual Training Market.

The Department of Homeland Security (DHS), through the Federal Emergency Management Agency (FEMA) and the Cybersecurity and Infrastructure Security Agency (CISA), announced more than USD 18.2 million in Tribal Cybersecurity Grant Program (TCGP) awards to assist Tribal Nations with managing and reducing systemic cyber risk and threats. Any military training session and data on it is confidential, virtual simulation systems are connected with different networks to transfer data and interact with other systems, which puts them at risk of cyberattacks and hackers. Ensuring the security of these systems could incur additional costs and further limit market growth potential in the long run.

- In 2025, India received 2,138 weekly cyberattacks per organization. Even within the Asia Pacific region, India is the second most targeted nation, trailing only behind Taiwan's 3,050 incidents. There was a 15 percent surge since 2022 which was again the second highest, following Korea's 21 percent increase since 2022.

- In the 2025 NATO Summit in Washington, D.C., Allies agreed to establish the NATO Integrated Cyber Defence Centre to enhance network protection, situational awareness, and the implementation of cyberspace as an operational domain.

Military Simulation and Virtual Training Market Segment Analysis

Based on the Application, the Military Simulation and Virtual Training Market is segmented into Ground, Air, and Naval. The Air segment held the largest market share, accounting for XX% in 2025. Due to the high operational costs associated with flight training, including fuel consumption, aircraft maintenance, and pilot salaries are very high. Defense organizations are increasingly using simulation-based training because it reduces costs while enhancing operational performance. The cost of training a basic qualified fighter pilot adds up to an estimated USD 5.6 million for an F-16 pilot, USD 10.17 million for an F-35A pilot, and USD 10.9 million for an F-22 pilot. Legal requirements requiring simulator training to obtain pilot certification, and technological developments that improve the effectiveness and enhance simulator realism.

- According to the U.S. Congressional Budget Office, the outlays for defense will rise to 1.1 trillion U.S. dollars by 2033. The largest parts of the budget are dedicated to the Departments of the Navy and the Air Force. The budget for the U.S. Air Force for 2025was nearly 260 billion U.S. dollars.

- China announced a 7.2% increase in its defense budget for the coming year, up slightly from last year’s 7.1% rate of increase. which is already the world’s second-highest behind the United States at 1.6 trillion yuan.

Military Simulation and Virtual Training Market Regional Insights

North America dominated the market and accounted for the largest revenue share of XX% in 2025. This is because of North America’s well-established research and development infrastructure, Strong Defense Budgets, Robust Aerospace & Defense Industry, early adoption of cutting-edge technologies, they have large defense systems, and the presence of important market players in the region like Lockheed Martin Corporation, General Dynamics Corporation, Cubic Corporation, and many others. The U.S. Army has received the first of tens of thousands of augmented reality goggles designed to make soldiers more effective in close combat.

The Integrated Visual Augmentation System (IVAS) uses augmented reality to project data in a soldier’s field of view, including maps, enemy positions, key friendly positions, and other information. Furthermore, the Army is fielding the Enhanced Night Vision Goggle–Binocular (ENVG-B), a next-generation set of image-intensification night vision goggles that not only provide stereoscopic night vision but can wirelessly connect to night vision sights mounted on weapons. A soldier with the ENVG-B package could, for example, raise a weapon over a wall, aim at a target, and open fire—all without exposing him or herself to enemy fire these are the factors which drive the growth of Military Simulation and Virtual Training Market in North America region.

- The STE-IS is an intelligent suite of training simulation and management software that enables intuitive access and simultaneous training at multiple locations. The STE-IS also uses the “One World Terrain” 3D mapping dataset that integrates actual terrain imagery from around the world. U.S. Department of Defense (DoD) to cost more than $20 billion plans to bring night vision, thermal vision, tactical edge computing, and enhanced situational awareness to infantry soldiers. U.S. Army ordered as many as 40,000 of the headsets of IVAS 1.0 versions.

- Sigma Defense Systems the Georgia-based firm will build, demonstrate, and deploy a next-generation training platform for the army’s Operator Maintainer Immersive Virtual Reality Environment for Intelligence Training (OMNIVORE-IT) project and signed a USD 4.7 million task order to build a virtual reality intelligence training ecosystem for the US Army.

Military Simulation and Virtual Training Market Scope

|

Military Simulation and Virtual Training Market |

|

|

Market Size in 2025 |

USD 17.28 billion |

|

Market Size in 2032 |

USD 25.48 billion |

|

CAGR (2026-2032) |

5.7%. |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

By Platform Type

|

|

|

Military Simulation and Virtual Training Market Segments |

By Application

|

|

By Software

|

|

Military Simulation and Virtual Training Market by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest)

South America (Brazil, Argentina, Rest of South America)

Military Simulation and Virtual Training Market Key Players.

- Lockheed Martin

- Northrop Grumman

- Cubic Corporation

- CAE Inc.

- Aai Corporation

- Collins Aerospace

- Raytheon Technologies

- BAE Systems.

- L3Harris Technologies, Inc.

- Thales

- Bohemia Interactive Simulations

Frequently Asked Questions

North America region is expected to hold the highest share in the Military Simulation and Virtual Training Market.

The market size of the Military Simulation and Virtual Training Market by 2032 is expected to reach USD 25.46 billion.

The forecast period for the Military Simulation and Virtual Training Market is 2026-2032.

The market size of the Military Simulation and Virtual Training Market in 2025 was valued at USD 17.28 billion.

1. Military Simulation and Virtual Training Market: Research Methodology

2. Military Simulation and Virtual Training Market Introduction

2.1. Study Assumption and Market Definition

2.2. Scope of the Study

2.3. Executive Summar

3. Global Military Simulation and Virtual Training Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Competitive Landscape

3.3. Key Players Benchmarking

3.3.1. Company Name

3.3.2. Product Segment

3.3.3. End-user Segment

3.3.4. Revenue (2025)

3.3.5. Company Headquarter

3.4. Market Structure

3.4.1. Market Leaders

3.4.2. Market Followers

3.4.3. Emerging Players

3.5. Mergers and Acquisitions Details

4. Military Simulation and Virtual Training Market: Dynamics

4.1. Military Simulation and Virtual Training Market Dynamics

4.1.1. Drivers

4.1.2. Restraints

4.1.3. Opportunities

4.1.4. Challenges

4.2. PORTER’s Five Forces Analysis

4.3. PESTLE Analysis

4.4. Technological Roadmap

4.5. Regulatory Landscape by Region

4.5.1. North America

4.5.2. Europe

4.5.3. Asia Pacific

4.5.4. Middle East and Africa

4.5.5. South America

5. Global Military Simulation and Virtual Training Market: Global Market Size and Forecast (Value in USD Billion) (2026-2032)

5.1. Global Military Simulation and Virtual Training Market Size and Forecast, By Platform Type (2026-2032)

5.1.1. Flight Simulation

5.1.2. Vehicle Simulation

5.1.3. Battlefield Simulation

5.1.4. Virtual Boot Camp

5.2. Global Military Simulation and Virtual Training Market Size and Forecast, By Application (2026-2032)

5.2.1. Ground

5.2.2. Air

5.2.3. Naval

5.3. Global Military Simulation and Virtual Training Market Size and Forecast, By Software (2026-2032)

5.3.1. Virtual Training Environments (VR)

5.3.2. Augmented Training Environments (AR)

5.3.3. Mix Reality

5.3.4. Digital Twin

5.3.5. Other

5.4. Global Military Simulation and Virtual Training Market Size and Forecast, by Region (2026-2032)

5.4.1. North America

5.4.2. Europe

5.4.3. Asia Pacific

5.4.4. Middle East and Africa

5.4.5. South America

6. North America Military Simulation and Virtual Training Market Size and Forecast by Segmentation (Value in USD Billion) (2026-2032)

6.1. North America Military Simulation and Virtual Training Market Size and Forecast, By Platform Type (2026-2032)

6.1.1. Flight Simulation

6.1.2. Vehicle Simulation

6.1.3. Battlefield Simulation

6.1.4. Virtual Boot Camp

6.2. North America Military Simulation and Virtual Training Market Size and Forecast, By Application (2026-2032)

6.2.1. Ground

6.2.2. Air

6.2.3. Naval

6.3. North America Military Simulation and Virtual Training Market Size and Forecast, By Software (2026-2032)

6.3.1. Virtual Training Environments (VR)

6.3.2. Augmented Training Environments (AR)

6.3.3. Mix Reality

6.3.4. Digital Twin

6.3.5. Other

6.4. North America Military Simulation and Virtual Training Market Size and Forecast, by Country (2026-2032)

6.4.1. United States

6.4.2. Canada

6.4.3. Mexico

7. Europe Military Simulation and Virtual Training Market Size and Forecast by Segmentation (Value in USD Billion) (2026-2032)

7.1. Europe Military Simulation and Virtual Training Market Size and Forecast, By Platform Type (2026-2032)

7.1.1. Flight Simulation

7.1.2. Vehicle Simulation

7.1.3. Battlefield Simulation

7.1.4. Virtual Boot Camp

7.2. Europe Military Simulation and Virtual Training Market Size and Forecast, By Application (2026-2032)

7.2.1. Ground

7.2.2. Air

7.2.3. Naval

7.3. Europe Military Simulation and Virtual Training Market Size and Forecast, By Software (2026-2032)

7.3.1. Virtual Training Environments (VR)

7.3.2. Augmented Training Environments (AR)

7.3.3. Mix Reality

7.3.4. Digital Twin

7.3.5. Other

7.4. Europe Military Simulation and Virtual Training Market Size and Forecast, by Country (2026-2032)

7.4.1. United Kingdom

7.4.2. France

7.4.3. Germany

7.4.4. Italy

7.4.5. Spain

7.4.6. Sweden

7.4.7. Russia

7.4.8. Rest of Europe

8. Asia Pacific Military Simulation and Virtual Training Market Size and Forecast by Segmentation (Value in USD Billion) (2026-2032)

8.1. Asia Pacific Military Simulation and Virtual Training Market Size and Forecast, By Platform Type (2026-2032)

8.1.1. Flight Simulation

8.1.2. Vehicle Simulation

8.1.3. Battlefield Simulation

8.1.4. Virtual Boot Camp

8.2. Asia Pacific Military Simulation and Virtual Training Market Size and Forecast, By Application (2026-2032)

8.2.1. Ground

8.2.2. Air

8.2.3. Naval

8.3. Asia Pacific Military Simulation and Virtual Training Market Size and Forecast, By Software (2026-2032)

8.3.1. Virtual Training Environments (VR)

8.3.2. Augmented Training Environments (AR)

8.3.3. Mix Reality

8.3.4. Digital Twin

8.3.5. Other

8.4. Asia Pacific Military Simulation and Virtual Training Market Size and Forecast, by Country (2026-2032)

8.4.1. China

8.4.2. S Korea

8.4.3. Japan

8.4.4. India

8.4.5. Australia

8.4.6. ASEAN

8.4.7. Rest of Asia Pacific

9. Middle East and Africa Military Simulation and Virtual Training Market Size and Forecast by Segmentation (Value in USD Billion) (2026-2032)

9.1. Middle East and Africa Military Simulation and Virtual Training Market Size and Forecast, By Platform Type (2026-2032)

9.1.1. Flight Simulation

9.1.2. Vehicle Simulation

9.1.3. Battlefield Simulation

9.1.4. Virtual Boot Camp

9.2. Middle East and Africa Military Simulation and Virtual Training Market Size and Forecast, By Application (2026-2032)

9.2.1. Ground

9.2.2. Air

9.2.3. Naval

9.3. Middle East and Africa Military Simulation and Virtual Training Market Size and Forecast, By Software (2026-2032)

9.3.1. Virtual Training Environments (VR)

9.3.2. Augmented Training Environments (AR)

9.3.3. Mix Reality

9.3.4. Digital Twin

9.3.5. Other

9.4. Middle East and Africa Military Simulation and Virtual Training Market Size and Forecast, by Country (2026-2032)

9.4.1. South Africa

9.4.2. GCC

9.4.3. Nigeria

9.4.4. Rest of ME&A

10. South America Military Simulation and Virtual Training Market Size and Forecast by Segmentation (Value in USD Billion) (2026-2032)

10.1. South America Military Simulation and Virtual Training Market Size and Forecast, By Platform Type (2026-2032)

10.1.1. Flight Simulation

10.1.2. Vehicle Simulation

10.1.3. Battlefield Simulation

10.1.4. Virtual Boot Camp

10.2. South America Military Simulation and Virtual Training Market Size and Forecast, By Application (2026-2032)

10.2.1. Ground

10.2.2. Air

10.2.3. Naval

10.3. South America Military Simulation and Virtual Training Market Size and Forecast, By Software (2026-2032)

10.3.1. Virtual Training Environments (VR)

10.3.2. Augmented Training Environments (AR)

10.3.3. Mix Reality

10.3.4. Digital Twin

10.3.5. Other

10.4. South America Military Simulation and Virtual Training Market Size and Forecast, by Country (2026-2032)

10.4.1. Brazil

10.4.2. Argentina

10.4.3. Rest Of South America

11. Company Profile: Key Players

11.1. Lockheed Martin

11.1.1. Company Overview

11.1.2. Business Portfolio

11.1.3. Financial Overview

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Northrop Grumman

11.3. Cubic Corporation

11.4. CAE Inc.

11.5. Aai Corporation

11.6. Raytheon Technologies

11.7. Collins Aerospace

11.8. BAE Systems.

11.9. L3Harris Technologies, Inc.

11.10. Thales

11.11. Bohemia Interactive Simulations

12. Key Findings

13. Industry Recommendations