Frozen Seafood Packaging Market- Global Industry Analysis and Forecast 2026-2032

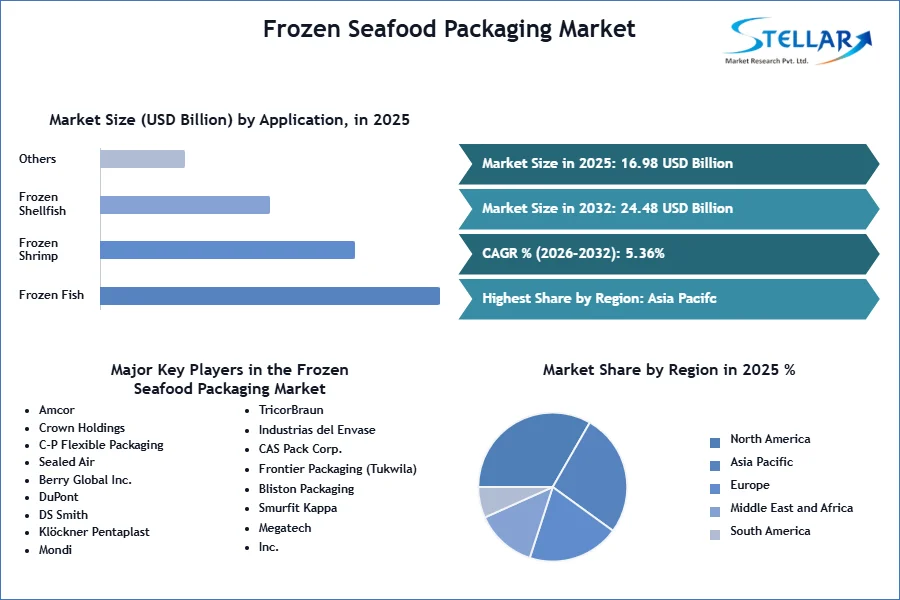

Frozen Seafood Packaging Market size was valued at USD 16.98 Bn. in 2025 and the Frozen Seafood Packaging revenue is expected to grow at a CAGR of 5.36% from 2026 to 2032, reaching nearly USD 24.48 Bn. by 2032.

Frozen Seafood Packaging Market Overview:

Frozen seafood is a type of conservation in which seafood products are frozen to keep them fresh and prolong their shelf life. Such fish are packaged in materials that offer insulation against the change of temperatures, moisture resistance, and protection against exposure to light. Lipid oxidation, browning, nutrient loss, and microbial growth slows down at freezing temperatures, which is driving the demand for frozen packaging. Different types of packaging include vacuum-sealed bags, plastic trays with wraps, frozen seafood boxes, and pouches. Such packaging usually consists of plastic, cardboard, and aluminium foil.

The major function of packaging of frozen seafood is to maintain quality and freshness from storage to delivery to customers. By proper freezing and packaging, retailers and consumers are able to receive seafood all year round, conveniently, and with reduced loss. This meets consumer demand and reduces the environmental impact of food waste. Properly packaged frozen fish enables customers to buy in quantity, preserve it for longer periods of time, and enjoy their favourite seafood items much more readily. Packaging of frozen seafood plays a significant role in assuring the availability, quality, and convenience of seafood products around the world.

To get more Insights: Request Free Sample Report

Frozen Seafood Packaging Market Dynamics:

Increasing demand for frozen seafood is driving the frozen seafood packaging market.

Seafood that is frozen works great for busy schedules because it is fast and easy to make type food. The demand of frozen seafood packaging is also growing because of increased awareness of the nutritional benefits of seafood, which is high in vital nutrients such as proteins, vitamins, and omega-3 fatty acids. Frozen seafood retains most of these nutritional benefits for a long time. Another reason is innovations in freezing technologies, such as IQF (Individually Quick Frozen) and flash freezing, which contribute to preserving seafood with better texture, flavour, and nutritional value, thus making the product more quality and appealing to consumers. Improving freezing techniques means that they extend the freshness of seafood products, decrease food waste, and make the products available in more distant markets. All these factors are driving the demand of frozen seafood packaging in the market.

Rising Concerns about Quality Control and Preservation.

One of the major challenges faced is to ensure that frozen seafood maintains its texture, freshness, and nutritional value during storage and transport. Inadequate freezing and packaging cause freezer burn, loss of flavour, and deterioration of quality. There is a need for proper temperature control at all stages of the supply chain. Temperature fluctuations are detrimental to frozen seafood and lead to spoilage and quality compromise. The cost to a company of using advanced packaging materials and state of the art technology, such as high-barrier films and environmentally friendly alternatives, is usually high. Such costs for small producers are high. General downturns in the economy, coupled with fluctuations in the cost of raw materials, exerts financial pressures on packaging companies, affecting the availability and cost of packaging materials.

Frozen Seafood Packaging Market Segment Analysis:

By Type, Frozen Seafood Packaging market is divided into Flexible packaging, and Rigid packaging. The flexible packaging sector dominated the market. The seafood delivery packaging industry is mainly influenced by the high usage of flexible packaging, which consists of various materials. Flexible packaging options are made for easy cooking and with steam valves, which enables the consumers to steam and cook chilled food. To reduce the criticism of harming the environment, the producers of packages are adopting environmentally friendly materials to produce pouches, which instantly cook frozen food in a microwave oven.

Frozen Seafood Packaging Market Regional Insight:

In 2024, North America emerged as the world's largest industry in the packaging of frozen seafood. Consumer demand for frozen seafood is high in the region because of its convenience, variety, and extended shelf life. Advanced packaging methods have been developed in the region to help enhance the quality and safety of the product. High standards of food safety ensure that frozen fish packaging meets the set standards. The competition between markets forces companies to innovate and invest in packaging techniques in order to make their products different. Such a competitive environment fosters further enhancement and innovation in the choices for packaging frozen seafood. Infrastructure and distribution networks in North America are well developed, and these makes the transportation and distribution of frozen fish very easy. All these factors are driving the growth of the frozen seafood packaging market.

Frozen Seafood Packaging Market Competitive Landscape:

- 8 August 2022, Iceland is using a newly developed recyclable paper pouch for its Northcoast frozen seafood range, in a claimed milestone in the quest for alternatives to plastic.

- February 2021, In February 2021, ProAmpac introduced the ProActive Recyclable R-2000F, featuring innovative technology aimed at supporting the brand's sustainability objectives. This packaging solution offers superior heat resistance, robust sealant technology, and exceptional dimpling resistance, positioning it as an optimal alternative for gusseted frozen food packaging traditionally made from non-recyclable PET/PE or OPP/PE laminations.

Frozen Seafood Packaging Market Scope:

|

Frozen Seafood Packaging Market |

|

|

Market Size in 2025 |

USD 16.98 Bn. |

|

Market Size in 2032 |

USD 24.48 Bn. |

|

CAGR (2026-2032) |

5.36 % |

|

Historic Data |

2020-2025 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2032 |

|

Segments |

By Type Flexible Packaging Rigid Packaging |

|

By Application Frozen Fish Frozen Shrimp Frozen Shellfish Others |

|

|

Regional Scope |

North America- United States, Canada, and Mexico Europe – UK, France, Germany, Italy, Spain, Sweden, Russia, and Rest of Europe Asia Pacific – China, India, Japan, South Korea, Australia, ASEAN, Rest of APAC Middle East and Africa - South Africa, GCC, Egypt, Rest of the Middle East and Africa South America – Brazil, Argentina, Rest of South America |

Frozen Seafood Packaging Market Key Players:

- Amcor

- Crown Holdings

- C-P Flexible Packaging

- Sealed Air

- Berry Global Inc.

- DuPont

- DS Smith

- Klöckner Pentaplast

- Mondi

- TricorBraun

- Industrias del Envase

- CAS Pack Corp.

- Frontier Packaging (Tukwila)

- Bliston Packaging

- Smurfit Kappa

- Megatech, Inc.

- Constantia FFP Ltd

- Crown Packaging

- Silgan Containers

- WINPAK LTD.

- XX Ltd

Frequently Asked Questions

Rising concerns about quality control and preservation is the challenge in the Frozen Seafood Packaging Market.

The Market size was valued at USD 16.98 Billion in 2025 and the total Market revenue is expected to grow at a CAGR of 5.36 % from 2026 to 2032, reaching nearly USD 24.48 Billion.

The segments covered in the market report are by Type, and Application.

1. Research Methodology

1.1 Research Data

1.1.1. Primary Data

1.1.2. Secondary Data

1.2. Market Size Estimation

1.2.1. Bottom-Up Approach

1.2.2. Top-Down Approach

1.3. Market Breakdown and Data Triangulation

1.4. Research Assumption

2. Frozen Seafood Packaging Market: Executive Summary

2.1. Market Overview

2.2. Market Size (2025) and Forecast (2026 – 2032) and Y-O-Y%

2.3. Market Size (USD) and Market Share (%) – By Segments and Regions

3. Global Frozen Seafood Packaging Market: Competitive Landscape

3.1. SMR Competition Matrix

3.2. Key Players Benchmarking

3.2.1. Company Name

3.2.2. Headquarter

3.2.3. Product Segment

3.2.4. End-user Segment

3.2.5. Y-O-Y%

3.2.6. Revenue (2025)

3.2.7. Profit Margin

3.2.8. Market Share

3.2.9. Company Locations

3.3. Market Structure

3.3.1. Market Leaders

3.3.2. Market Followers

3.3.3. Emerging Players

3.4. Consolidation of the Market

3.4.1. Strategic Initiatives and Developments

3.4.2. Mergers and Acquisitions

3.4.3. Collaborations and Partnerships

3.4.4. Product Launches and Innovations

4. Frozen Seafood Packaging Market: Dynamics

4.1. Frozen Seafood Packaging Market Trends by Region

4.1.1. North America

4.1.2. Europe

4.1.3. Asia Pacific

4.1.4. Middle East and Africa

4.1.5. South America

4.2. Frozen Seafood Packaging Market Drivers

4.3. Frozen Seafood Packaging Market Restraints

4.4. Frozen Seafood Packaging Market Opportunities

4.5. Frozen Seafood Packaging Market Challenges

4.6. PORTER’s Five Forces Analysis

4.6.1. Intensity of the Rivalry

4.6.2. Threat of New Entrants

4.6.3. Bargaining Power of Suppliers

4.6.4. Bargaining Power of Buyers

4.6.5. Threat of Substitutes

4.7. PESTLE Analysis

4.7.1. Political Factors

4.7.2. Economic Factors

4.7.3. Social Factors

4.7.4. Technological Factor

4.7.5. Legal Factors

4.7.6. Environmental Factors

4.8. Technological Roadmap

4.9. Value Chain Analysis

4.10. Regulatory Landscape

4.10.1. Market Regulation by Region

4.10.1.1. North America

4.10.1.2. Europe

4.10.1.3. Asia Pacific

4.10.1.4. Middle East and Africa

4.10.1.5. South America

4.10.2. Impact of Regulations on Market Dynamics

4.10.3. Government Schemes and Initiatives

5. Frozen Seafood Packaging Market: Global Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2032)

5.1. Frozen Seafood Packaging Market Size and Forecast, by Type (2026-2032)

5.1.1. Flexible Packaging

5.1.2. Rigid Packaging

5.2. Frozen Seafood Packaging Market Size and Forecast, by Application (2026-2032)

5.2.1. Frozen Fish

5.2.2. Frozen Shrimp

5.2.3. Frozen Shellfish

5.2.4. Others

5.3. Frozen Seafood Packaging Market Size and Forecast, by Region (2026-2032)

5.3.1. North America

5.3.2. Europe

5.3.3. Asia Pacific

5.3.4. Middle East and Africa

5.3.5. South America

6. North America Frozen Seafood Packaging Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2032)

6.1. North America Frozen Seafood Packaging Market Size and Forecast, by Type (2026-2032)

6.1.1. Flexible Packaging

6.1.2. Rigid Packaging

6.2. North America Frozen Seafood Packaging Market Size and Forecast, by Application (2026-2032)

6.2.1. Frozen Fish

6.2.2. Frozen Shrimp

6.2.3. Frozen Shellfish

6.2.4. Others

6.3. North America Frozen Seafood Packaging Market Size and Forecast, by Country (2026-2032)

6.3.1. United States

6.3.2. Canada

6.3.3. Mexico

7. Europe Frozen Seafood Packaging Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2032)

7.1. Europe Frozen Seafood Packaging Market Size and Forecast, by Type (2026-2032)

7.2. Europe Frozen Seafood Packaging Market Size and Forecast, by Application (2026-2032)

7.3. Europe Frozen Seafood Packaging Market Size and Forecast, by Country (2026-2032)

7.3.1. United Kingdom

7.3.2. France

7.3.3. Germany

7.3.4. Italy

7.3.5. Spain

7.3.6. Sweden

7.3.7. Austria

7.3.8. Rest of Europe

8. Asia Pacific Frozen Seafood Packaging Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2032)

8.1. Asia Pacific Frozen Seafood Packaging Market Size and Forecast, by Type (2026-2032)

8.2. Asia Pacific Frozen Seafood Packaging Market Size and Forecast, by Application (2026-2032)

8.3. Asia Pacific Frozen Seafood Packaging Market Size and Forecast, by Country (2026-2032)

8.3.1. China

8.3.2. S Korea

8.3.3. Japan

8.3.4. India

8.3.5. Australia

8.3.6. Indonesia

8.3.7. Malaysia

8.3.8. Vietnam

8.3.9. Taiwan

8.3.10. Rest of Asia Pacific

9. Middle East and Africa Frozen Seafood Packaging Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2032)

9.1. Middle East and Africa Frozen Seafood Packaging Market Size and Forecast, by Type (2026-2032)

9.2. Middle East and Africa Frozen Seafood Packaging Market Size and Forecast, by Application (2026-2032)

9.3. Middle East and Africa Frozen Seafood Packaging Market Size and Forecast, by Country (2026-2032)

9.3.1. South Africa

9.3.2. GCC

9.3.3. Nigeria

9.3.4. Rest of ME&A

10. South America Frozen Seafood Packaging Market Size and Forecast by Segmentation (by Value in USD Billion) (2026-2032)

10.1. South America Frozen Seafood Packaging Market Size and Forecast, by Type (2026-2032)

10.2. South America Frozen Seafood Packaging Market Size and Forecast, by Application (2026-2032)

10.3. South America Frozen Seafood Packaging Market Size and Forecast, by Country (2026-2032)

10.3.1. Brazil

10.3.2. Argentina

10.3.3. Rest Of South America

11. Company Profile: Key Players

11.1. Amcor

11.1.1. Company Overview

11.1.2. Business Portfolio

11.1.2.1. Product Name

11.1.2.2. Product Details

11.1.3. Financial Overview

11.1.3.1. Total Revenue

11.1.3.2. Segment Revenue

11.1.3.3. Regional Revenue

11.1.4. SWOT Analysis

11.1.5. Strategic Analysis

11.1.6. Recent Developments

11.2. Crown Holdings

11.3. C-P Flexible Packaging

11.4. Sealed Air

11.5. Berry Global Inc.

11.6. DuPont

11.7. DS Smith

11.8. Klöckner Pentaplast

11.9. Mondi

11.10. TricorBraun

11.11. Industrias del Envase

11.12. CAS Pack Corp.

11.13. Frontier Packaging (Tukwila)

11.14. Bliston Packaging

11.15. Smurfit Kappa

11.16. Megatech, Inc.

11.17. Constantia FFP Ltd

11.18. Crown Packaging

11.19. Silgan Containers

11.20. WINPAK LTD.

11.21. XX Ltd

12. Key Findings

13. Analyst Recommendations

13.1. Strategic Recommendations

13.2. Future Outlook